|

시장보고서

상품코드

1911362

mRNA 백신 및 치료제 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)MRNA Vaccines And Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

mRNA 백신 및 치료제 시장 규모에 있어서, 구조 유형별로는 여전히 기존 비복제 형식이 주도하고 있습니다. 기존 시설, 규제 선례 및 검증된 분석법이 규모 확대 시 마찰을 최소화함에 따라 이 계통은 2025년 기준 65.10%의 점유율을 유지했습니다. RSV 및 인플루엔자 부스터에 대한 수요는 지속되어 경쟁 압력이 가중되는 상황에서도 기본 수익을 유지하고 있습니다. 자가 증폭 mRNA는 낮은 투여량 요구와 개선된 항원 지속성으로 환자당 치료 비용을 낮추는 효과 덕분에 2026-2031년의 연평균 17.10%의 성장률을 보이며 가속화되고 있습니다.

주요 하이라이트

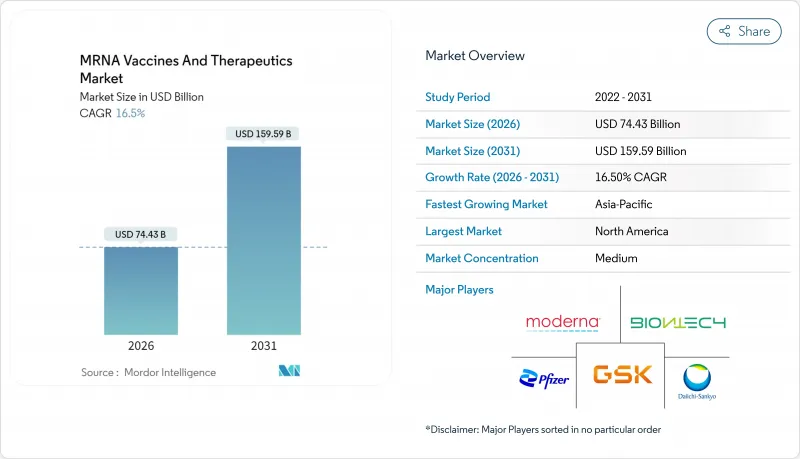

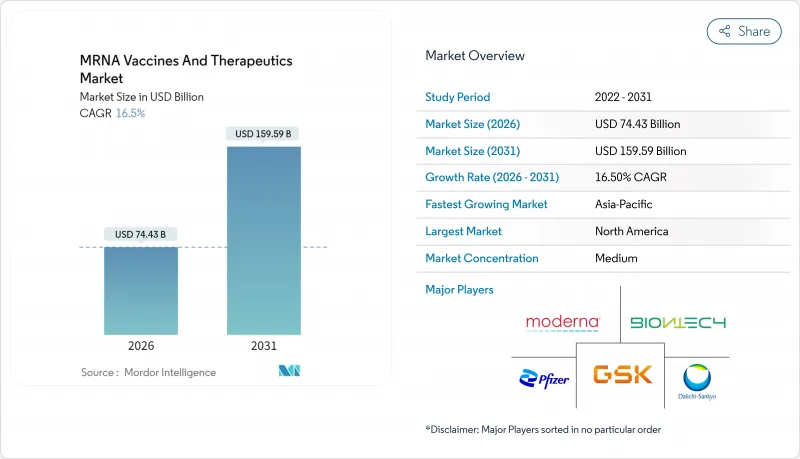

- mRNA 백신 및 치료제 시장은 2025년에 638억 9,000만 달러로 평가되었고, 2026년 744억 3,000만 달러에서 2031년까지 1,595억 9,000만 달러에 이를 것으로 예측됩니다. 예측 기간(2026-2031년)의 CAGR은 16.5%를 나타낼 전망입니다. 규모 확대 자본이 전문 제조 허브로 유입되고 있으며, 전략적 공공-민간 협력으로 임상 파이프라인이 확대되고, 차세대 구조체가 학술 연구실에서 중추적 임상시험 단계로 진입하고 있습니다. 실제 세계 효과성 데이터가 COVID-19, RSV 및 여러 종양학 환경에서 플랫폼의 유효성을 입증함에 따라 투자자들의 관심은 여전히 견고합니다. FDA 플랫폼 지정 프로그램 및 일본 및 싱가포르의 유사 신속 심사 제도를 통한 규제 공백 해소로 개발 기간이 단축되고 있으며, 모듈식 폐쇄형 시스템 플랜트는 자본 지출과 배치 간 변동성을 동시에 감소시키고 있습니다. 동시에 공급망 혁신?특히 연속적 지질 나노입자 생산 및 개선된 콜드체인 모니터링?은 투여량당 비용을 낮추고 신흥 지역의 접근성을 확대하고 있습니다.

세계의 mRNA 백신 및 치료제 시장 동향과 전망

유행 대책 수요 급증

보건 당국이 COVID-19를 넘어 인플루엔자, 원숭이두창, 결핵까지 시야를 넓히면서 정부의 대비 자금 지원이 mRNA 백신 및 치료제 시장을 지탱하고 있습니다. BARDA가 모더나에 H5 인플루엔자 후보물질 개발을 위해 수여한 1억 7,600만 달러 지원금은 다년간 조달 로드맵의 핵심을 이룹니다. CEPI는 이어 1억 4,500만 달러 시설 지원 약속을 통해 바이오엔테크가 르완다에 말라리아 항원 충전 및 완성 공정을 공동 배치할 수 있도록 했습니다. 이러한 프로그램에는 향후 유행 시 자동 확장을 촉발하는 조건부 구매 조항이 포함되어 상업적 생산 능력 투자 위험을 완화합니다. 전염병 대비 혁신 연합(CEPI)은 또한 분석적 출시 시험을 표준화하는 화학-제조-관리 프레임워크를 발표하여 백신 개발의 '죽음의 계곡' 단계에서 역사적으로 높았던 실패율을 억제하고 있습니다. 이러한 노력들은 종합적으로 세계의 수요 가시성을 확장하여 중견 개발사들의 자본 비용을 낮추는 효과를 가져옵니다.

증가하는 만성 질환 및 감염의 부담

흑색종, 자궁경부암, 호흡기 감염의 발생률 증가로 mRNA 치료제의 적용 가능 대상이 확대되고 있습니다. 종양학 부문에서 mRNA-4157과 펨브롤리주맙 병용 요법은 3년간의 추적 관찰 결과 흑색종 재발률을 49% 감소시켰습니다. 희귀질환 파이프라인 역시 호조를 보이고 있습니다. 프로피온산혈증 환자 대상 긍정적 안전성 데이터는 대사 장애 치료에서의 플랫폼 잠재력을 입증했습니다. 자가면역 부문 전망도 성숙 단계에 접어들어, 카르테시안 테라퓨틱스가 중증근무력증 치료제 데카르트-08의 3상 임상시험에 진입한 것이 이를 증명합니다. 이러한 임상 성과는 고가 치료제에 대한 보험사 보상 의지로 이어져 mRNA 백신 및 치료제 시장의 수익 전망을 강화하고 있습니다.

콜드체인 및 엄격한 규제 준수

주요 하이라이트

- 초저온 유통은 여전히 많은 제형에 대해 -20°C에서-80°C의 저온 보관을 요구하여 적도 기후 지역에서 물류 부담을 가중시킵니다. 일본 개발사들은 8°C에서 14일간 효능을 유지하는 내열성 부형제를 시험 중이지만, 상용화 단계는 아직 초기 단계입니다. 규제 측면에서는 FDA의 개정된 CMC 지침이 공정 분석 및 핵심 품질 속성에 대한 세분화된 보고를 의무화하여 서류 준비 기간을 연장하고 있습니다. FDA의 플랫폼 지정(Platform Designation) 라벨은 신속 심사를 제공하지만, 현재까지 이를 획득한 신청자는 극소수에 불과하여 단기적 완화 효과는 제한적입니다.

부문 분석

일본의 ARCT-154 승인은 규제상의 모델 사례가 되고, 다른 관할 구역이 이를 연구 대상으로 하고 있기 때문에 스타트업 기업의 개발 리스크 인식이 저하하고 있습니다.

상업적 노출은 제한적이지만 2세대 순환 RNA가 주목받고 있습니다. 세일 바이오메디신즈는 벤치 규모로 8,000 뉴클레오티드 구조체를 합성하여 대규모 치료적 페이로드의 기술적 실현 가능성을 입증했습니다. 업계 관측통들은 순환형 모달리티가 엑소뉴클레아제 분해에 저항하여 단백질 발현 기간을 연장하기 때문에 10년 이내에 선형 템플릿을 대체할 것으로 전망합니다. 나고야 대학의 병행 학술 연구는 질병 세포 선택적 번역 개시를 제시하며, 최소한의 오프타겟 독성을 가진 종양학 적용 가능성을 시사합니다. 이러한 혁신들은 종합적으로 mRNA 백신 및 치료제 시장을 다각화하며, 내부 RNA 화학 전문성이 부족한 기업들의 플랫폼 라이선싱 계약을 유치하고 있습니다.

감염성 질환은 2025년 매출의 49.85%를 차지하며 주요 수익원으로 자리매김했는데, 이는 코로나19 부스터, RSV 백신, 소아 복합백신이 공공 부문 조달 파이프라인을 채웠기 때문입니다. 호흡기 바이러스 외에도 노로바이러스 및 거대세포바이러스 프로그램이 후기 임상시험 단계로 진전되며 물량 전망을 강화하고 있습니다. 그러나 mRNA-4155와 펨브롤리주맙 병용요법이 흑색종 재발률을 49% 감소시키는 획기적 성과를 달성하며, 종양학 부문이 연평균 17.20% 성장률로 가장 빠른 확장세를 보이고 있습니다. 해당 요법에 대한 FDA의 획기적 치료제 지정이 폐암 및 방광암 임상 시험 환자 모집을 가속화하며 대상 환자 풀을 확대했습니다.

종양학 부문은 지역적 다양화도 진행 중입니다. 리캉 라이프사이언스(Likang Life Sciences)는 서양 유사 프로토콜 대비 10분의 1 비용으로 제조된 맞춤형 신항원 백신에 대해 FDA 임상시험계획(IND) 승인을 획득했습니다. 중국 병원들은 민간 지불 모델 하에 이러한 요법을 시범 운영 중이며, 이는 효능 평가 지표가 설득력 있을 경우 지불 주체의 유연성을 시사합니다. 자가면역 연구도 유사한 궤적을 따르고 있습니다. 카르테시안 테라퓨틱스의 '데카르트-08'은 중증근무력증에서 3상 단계에 진입했으며, OSE 이뮤노테라퓨틱스는 자가면역성 간염 치료를 위한 IL-35 내성 유도 구조체를 개발 중입니다. 이러한 성공 사례들은 mRNA 백신 및 치료제 시장이 감염병 부문를 넘어 지속적 성장을 이룰 수 있다는 확신을 심어주고 있습니다.

지역별 분석

북미는 2025년 세계의 수익의 41.95%를 차지하며 견조한 연방 정부 자금, 밀접한 수탁 제조 네트워크, mRNA 기술을 최초로 승인한 규제 환경이 기반이 되고 있습니다. BARDA의 인플루엔자 계약과 Blackstone의 수십억 달러 규모의 R&D 지원은 제도적 신뢰를 뒷받침합니다. 텍사스주와 매사추세츠주에서 모듈식 플랜트에 대한 지속적인 투자로 유행성이 높은 생산 능력을 유지하면서 유행적인 생산 능력을 유지하며, 이 지역의 주도적 지위가 지속되고 있습니다.

아시아태평양 지역은 2026-2031년의 연평균 17.35%의 성장률(CAGR)을 기록할 것으로 예상되며, 이는 전 지역 중 가장 빠른 속도입니다. 규제 유연성이 핵심 동력으로 작용하고 있습니다. 일본은 최초의 자가 증폭형 mRNA 백신을 승인했으며, 싱가포르는 순환형 RNA를 완전히 새로운 방식이 아닌 점진적 변형으로 간주하는 지침을 발표해 심사 주기를 단축했습니다. 정부는 국내 공급망 지원에도 나서고 있습니다. 호주의 RNA 청사진은 80억 호주 달러의 GDP 기여를 전망하며, 한국의 GC바이오파마는 이메타스와 자가면역 후보물질 공동 개발 중입니다. 비용 혁신 역학은 중국에서 특히 두드러지는데, 현지 생산을 통해 서구 기준 대비 99% 저렴한 맞춤형 암 백신을 공급함으로써 환자 접근성을 효과적으로 확대하고 mRNA 백신 및 치료제 시장의 기존 가격 전략에 도전장을 내밀고 있습니다.

유럽은 전략적 산업 정책에 힘입어 꾸준히 10% 중반대 성장을 유지하고 있습니다. 바이오엔테크는 유전체학 및 재생의학 전문 영국 연구개발(R&D) 허브 2곳에 10억 파운드를 투자했으며, 이 프로젝트는 정부 보조금 1억 2900만 파운드로 지원됩니다. CEPI의 1억 4500만 달러 규모 르완다 시설은 아프리카에 위치하지만 유럽의 공정 기술과 품질 관리 프로토콜을 적용해 유럽의 영향력을 확대하고 있습니다. 한편 라틴아메리카는 PAHO(범미보건기구)의 역량 강화 프로그램을 활용 중입니다. 이 프로그램은 캐나다 자금으로 아르헨티나와 브라질 공장에 모듈형 클린룸과 기술 이전 패키지를 제공합니다. 이러한 노력들은 종합적으로 제조 노하우를 확산시키고 단일 지역 공급 의존도를 낮춰 mRNA 백신 및 치료제 시장 전반의 회복탄력성을 강화하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 팬데믹 대비 수요 급증

- 만성 및 감염병 부담 증가

- 정부 및 벤처기업에 의한 연구개발자금 확대

- 코로나19 이후 상업적 개념 증명

- 모듈식 폐쇄형 mRNA 제조 시스템 도입

- 자가 증폭/순환형 mRNA 기술 발전

- 시장 성장 억제요인

- 콜드체인 및 엄격한 규제 준수

- 높은 생산 비용 및 규모 확대 복잡성

- LNP 첨가제공급 병목과 특허 밀집 상태

- 백신 주저 현상 및 허위 정보의 역풍

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체 위협

- 구매자 협상력

- 공급기업 협상력

- 대체품 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- mRNA 구조 유형별

- 기존 비복제형 mRNA

- 자기 증폭형 mRNA

- 환상 mRNA

- 기타

- 치유 영역별

- 감염성 질환

- 종양학

- 자가면역질환

- 기타

- 투여 시스템별

- 리포좀 나노입자(LNP)

- 폴리머 기반 나노캐리어

- 양이온성 나노에멀젼

- 바이러스 벡터

- 기타

- 유통 채널별

- 공공

- 민간

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Pfizer Inc.

- Moderna Inc.

- BioNTech SE

- CureVac SE

- Arcturus Therapeutics

- GSK plc

- Sanofi

- Daiichi Sankyo

- AstraZeneca

- CSL Seqirus

- Chugai Pharmaceutical

- Gennova Biopharmaceuticals

- eTheRNA Immunotherapies

- Orbital Therapeutics

- SAB Biotherapeutics

- Strand Therapeutics

- GreenLight Biosciences

- Providence Therapeutics

- CanSino Biologics

- Walvax Biotechnology

제7장 시장 기회와 장래의 전망

HBR 26.01.29The mRNA vaccines and therapeutics market size for construct types remains dominated by conventional non-replicating formats. This lineage retained 65.10% share in 2025 because existing facilities, regulatory precedents, and validated analytical assays minimize scale-up friction. Demand continues in RSV and influenza boosters, preserving baseline revenue even as competitive pressure mounts. Self-amplifying mRNA is accelerating at 17.10% CAGR between 2026 and 2031 owing to its lower dose requirement and improved antigen persistence, which collectively lower per-patient treatment cost.

Key Highlights

- The mRNA vaccines and therapeutics market was valued at USD 63.89 billion in 2025 and estimated to grow from USD 74.43 billion in 2026 to reach USD 159.59 billion by 2031, at a CAGR of 16.5% during the forecast period (2026-2031). Scale-up capital is flowing into specialized manufacturing hubs, strategic public-private alliances are broadening clinical pipelines, and next-generation constructs are moving from academic labs to pivotal trials. Investor appetite remains resilient because real-world effectiveness data validate the platform across COVID-19, RSV, and several oncology settings . Closing regulatory gaps through the FDA Platform Designation Program and similar fast-track schemes in Japan and Singapore is shortening development timelines, while modular closed-system plants reduce both capex and batch-to-batch variability. At the same time, supply-chain innovations-particularly continuous lipid-nanoparticle production and improved cold-chain monitors-are lowering cost per dose and expanding access in emerging regions.

Global MRNA Vaccines And Therapeutics Market Trends and Insights

Pandemic-preparedness demand surge

Government preparedness funding sustains the mRNA vaccines and therapeutics market as health agencies look beyond COVID-19 to influenza, mpox, and tuberculosis. BARDA's USD 176 million award to Moderna for an H5 influenza candidate anchors a multiyear procurement roadmap . CEPI followed with a USD 145 million facility commitment that enables BioNTech to co-locate fill-finish capabilities for malaria antigens in Rwanda. These programs embed contingent purchasing clauses that trigger automatic scale-up during future outbreaks, de-risking commercial capacity investments. The Coalition for Epidemic Preparedness Innovations has also published a Chemistry-Manufacturing-Control Framework that standardizes analytical release testing, curbing the historically high attrition seen at the "valley of death" stage of vaccine development. Collectively, these efforts extend global demand visibility, unlocking lower cost of capital for mid-sized developers.

Rising chronic & infectious disease burden

Escalating incidence of melanoma, cervical cancer, and respiratory infections is broadening the addressable pool for mRNA therapeutics. In oncology, the mRNA-4157 plus pembrolizumab combination demonstrated a 49% reduction in melanoma recurrence across a three-year readout. Rare-disease pipelines are equally buoyant; positive safety data in propionic acidemia patients confirmed the platform's potential in metabolic disorders. Autoimmune prospects are maturing, evident in Cartesian Therapeutics entering Phase 3 trials for Descartes-08 in myasthenia gravis. These clinical milestones translate into payer willingness to reimburse high-value therapies, reinforcing revenue forecasts for the mRNA vaccines and therapeutics market.

Cold-chain & stringent regulatory compliance

Key Highlights

- Deep-freeze distribution still demands -20 °C to -80 °C storage for many formulations, stressing logistics in equatorial climates. Japanese developers are testing thermostable excipients that hold potency for 14 days at 8 °C, yet commercial rollout remains nascent. On the regulatory front, the FDA's updated CMC guidance mandates granular reporting on process analytics and critical-quality attributes, extending dossier preparation timelines. While the agency's Platform Designation label offers accelerated reviews, only a handful of applicants have secured it to date, limiting near-term relief .

Other drivers and restraints analyzed in the detailed report include:

- Government & venture R&D funding escalation

- Commercial proof-of-concept post-COVID-19

- Elevated production cost & scale-up complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Japan's approval of ARCT-154 created a regulatory template that other jurisdictions are now studying, reducing the perceived development risk for startups.

Second-generation circular RNA is gathering momentum despite limited commercial exposure. Sail Biomedicines synthesized 8,000-nucleotide constructs at bench scale, demonstrating technical feasibility for large therapeutic payloads. Industry observers expect circular modalities to supplant linear templates within a decade because they resist exonuclease degradation and therefore prolong protein expression windows. Parallel academic research at Nagoya University presents disease-cell-selective translation initiation, hinting at oncology applications with minimal off-target toxicity. Collectively, these innovations diversify the mRNA vaccines and therapeutics market and attract platform licensing deals from companies that lack internal RNA chemistry expertise.

Infectious diseases remained the primary revenue pillar, securing 49.85% of 2025 turnover as COVID-19 boosters, RSV shots, and pediatric combination vaccines filled public-sector procurement pipelines. Beyond respiratory viruses, norovirus and cytomegalovirus programs are progressing toward late-stage trials, reinforcing the volume outlook. Yet oncology is registering the fastest expansion at 17.20% CAGR, catalyzed by the milestone 49% reduction in melanoma recurrence achieved by mRNA-4157 plus pembrolizumab. FDA Breakthrough Therapy Designation for that regimen accelerated trial enrollment in lung and bladder cancers, broadening addressable patient pools.

The oncology wave is also geo-diversifying. Likang Life Sciences received FDA IND clearance for a personalized neoantigen vaccine manufactured at one-tenth the cost of comparable Western protocols. Chinese hospitals are piloting these regimens under private payment models, signaling payer flexibility when efficacy endpoints are compelling. Autoimmune research is following a similar trajectory; Cartesian Therapeutics' Descartes-08 reached Phase 3 in myasthenia gravis, and OSE Immunotherapeutics is advancing IL-35 tolerizing constructs for autoimmune hepatitis. Each success story builds confidence that the mRNA vaccines and therapeutics market can sustain growth outside its infectious-disease origins.

The MRNA Vaccines and Therapeutics Market is Segmented by MRNA Construct Type (Conventional Non-Replicating MRNA, and More), Therapeutic Area (Infectious Diseases, Oncology, and More), Delivery System (Polymer-Based Nanocarriers, Cationic Nano-Emulsions, and More), Distribution Channel (Public and Private), and Geography (North America, Europe, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 41.95% of global revenue in 2025, anchored by robust federal funding, dense contract-manufacturing networks, and a regulatory environment that first validated mRNA technology. BARDA's influenza contract and Blackstone's multibillion-dollar R&D support underscore institutional confidence. Ongoing investment in modular plants across Texas and Massachusetts keeps capacity flexible for both pandemic surges and therapeutic rollouts, sustaining the regional leadership position.

Asia-Pacific is expected to register a 17.35% CAGR from 2026 to 2031, the fastest across all regions. Regulatory agility is a key driver; Japan approved the first self-amplifying mRNA vaccine, and Singapore has issued guidance that treats circular RNA as an incremental modification rather than a brand-new modality, shortening review cycles. Governments are also funding domestic supply chains-Australia's RNA Blueprint forecasts an AUD 8 billion GDP contribution, and South Korea's GC Biopharma is co-developing autoimmune candidates with Immetas. Cost-innovation dynamics are particularly acute in China, where localized manufacturing is delivering individualized cancer vaccines at prices 99% below Western benchmarks, effectively expanding patient access and challenging incumbent pricing strategies across the mRNA vaccines and therapeutics market.

Europe maintains steady mid-teens growth, supported by strategic industrial policy. BioNTech committed GBP 1 billion for two UK R&D hubs specializing in genomics and regenerative medicine, a project subsidized by GBP 129 million in government grants. CEPI's USD 145 million facility in Rwanda, although located in Africa, employs European process technology and quality-management protocols, extending the continent's influence. Meanwhile, Latin America is leveraging PAHO's capacity-building program, which equips plants in Argentina and Brazil with modular cleanrooms and knowledge transfer packages provided by Canadian funding. These initiatives collectively diffuse manufacturing know-how and reduce single-region supply dependence, boosting resilience across the mRNA vaccines and therapeutics market.

- Pfizer

- Moderna

- BioNTech

- CureVac SE

- Arcturus Therapeutics

- GlaxoSmithKline

- Sanofi

- Daiichi Sankyo

- AstraZeneca

- CSL Seqirus

- Chugai Pharmaceutical

- Gennova Biopharmaceuticals

- eTheRNA Immunotherapies

- Orbital Therapeutics

- SAB Biotherapeutics

- Strand Therapeutics

- GreenLight Biosciences

- Providence Therapeutics

- CanSino Biologics

- Walvax Biotechnology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pandemic-Preparedness Demand Surge

- 4.2.2 Rising Chronic & Infectious Disease Burden

- 4.2.3 Government & Venture R&D Funding Escalation

- 4.2.4 Commercial Proof-Of-Concept Post-COVID-19

- 4.2.5 Modular Closed-System mRNA Manufacturing Roll-Out

- 4.2.6 Advancements in Self-Amplifying/Circular mRNA

- 4.3 Market Restraints

- 4.3.1 Cold-Chain & Stringent Regulatory Compliance

- 4.3.2 Elevated Production Cost & Scale-Up Complexity

- 4.3.3 LNP Excipient Supply Bottlenecks & Patent Thickets

- 4.3.4 Vaccine-Hesitancy & Misinformation Headwinds

- 4.4 Regulatory Landscape

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By mRNA Construct Type

- 5.1.1 Conventional non-replicating mRNA

- 5.1.2 Self-amplifying mRNA

- 5.1.3 Circular mRNA

- 5.1.4 Others

- 5.2 By Therapeutic Area

- 5.2.1 Infectious Diseases

- 5.2.2 Oncology

- 5.2.3 Autoimmune Disorders

- 5.2.4 Others

- 5.3 By Delivery System

- 5.3.1 Lipid Nanoparticles (LNP)

- 5.3.2 Polymer-based Nanocarriers

- 5.3.3 Cationic Nano-emulsions

- 5.3.4 Viral Vectors

- 5.3.5 Others

- 5.4 By Distribution Channel

- 5.4.1 Public

- 5.4.2 Private

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Pfizer Inc.

- 6.3.2 Moderna Inc.

- 6.3.3 BioNTech SE

- 6.3.4 CureVac SE

- 6.3.5 Arcturus Therapeutics

- 6.3.6 GSK plc

- 6.3.7 Sanofi

- 6.3.8 Daiichi Sankyo

- 6.3.9 AstraZeneca

- 6.3.10 CSL Seqirus

- 6.3.11 Chugai Pharmaceutical

- 6.3.12 Gennova Biopharmaceuticals

- 6.3.13 eTheRNA Immunotherapies

- 6.3.14 Orbital Therapeutics

- 6.3.15 SAB Biotherapeutics

- 6.3.16 Strand Therapeutics

- 6.3.17 GreenLight Biosciences

- 6.3.18 Providence Therapeutics

- 6.3.19 CanSino Biologics

- 6.3.20 Walvax Biotechnology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment