|

시장보고서

상품코드

1911366

수술 후 통증 관리 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Post-Operative Pain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

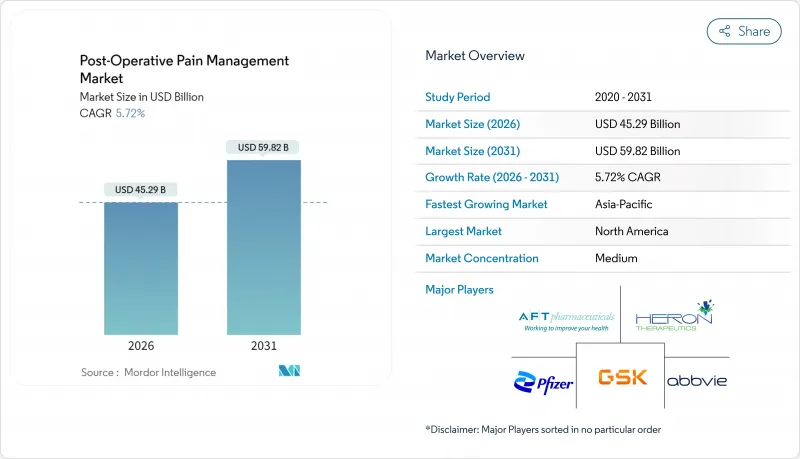

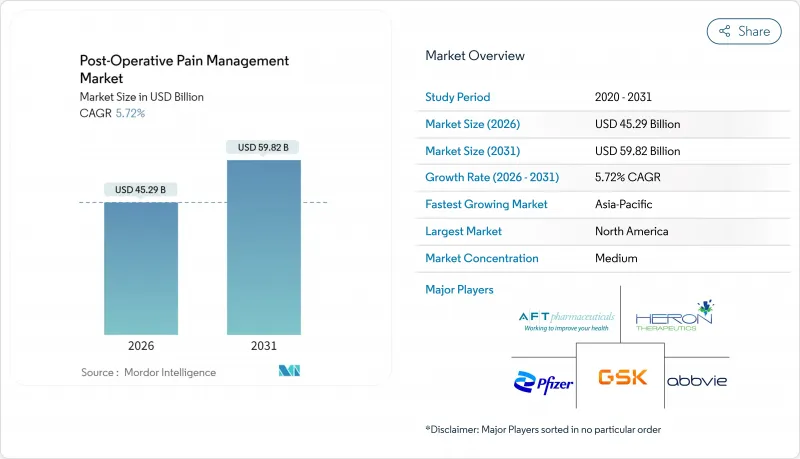

수술 후 통증 관리 시장 규모는 2026년에는 452억 9,000만 달러로 평가되었고, 2025년 428억 4,000만 달러에서 성장할 것으로 예측됩니다. 2031년까지의 예측으로는 598억 2,000만 달러에 달할 것으로 보이며, 2026-2031년에 걸쳐 CAGR5.72%로 성장할 전망입니다.

다중 모드 진통법의 꾸준한 도입, 비오피오이드 옵션에 대한 보험급여 인센티브, 장기 작용 국소 마취 기법이 외과 전문 부문 전반에 걸쳐 수요를 가속화하고 있습니다. 정형외과, 심혈관, 흉부 수술이 소비를 주도하는 가운데, 수술 후 회복 촉진(ERAS) 프로토콜은 국소 마취제와 표면 마취 혁신 기술의 비약적 성장을 이끌고 있습니다. 비용에 민감한 병원들은 고가의 정맥 주사제 사용을 줄이고 있지만, 인공지능 기반 맞춤형 투여량 조절과 디지털 약국 유통은 계속해서 효율성 향상을 이끌어내고 있습니다. 기존 제약사와 바이오테크 신생 기업들이 NaV1.8 억제제, 지속형 신경 차단 주사제, 스마트 경피 흡수 시스템 상용화를 두고 경쟁하면서 시장 경쟁은 더욱 치열해지고 있습니다.

세계의 수술 후 통증 관리 시장 동향 및 인사이트

수술 건수 증가

통증 치료 전문 시설인 외래 수술 센터는 2018년 612개소에서 2023년까지 800개소 이상으로 증가하여, 다중 모드 진통에 대한 기본 수요를 높이는 수술 건수 증가를 시사합니다. 선진국 인구의 고령화는 정형외과 및 심혈관 수술을 촉진하여 국소 마취제와 보조제의 꾸준한 소비를 이끌고 있습니다. ERAS(회복 가속화 수술 경로)가 주류화되며, 입원 기간 단축과 통증 관리 보장을 동시에 실현하는 근거 기반 프로토콜이 제도화되었습니다. 미국 식품의약국(FDA) 라벨링 하의 규제 지침은 표준화된 수술 후 투여량을 장려하여 병원에 명확한 규정 준수 로드맵을 제공합니다. 수술 건수가 증가함에 따라 투여 복잡성과 재고 관리를 간소화하는 공급업체들이 수술 후 통증 관리 시장에서 점유율을 확대할 전망입니다.

다각적 및 비 오피오이드 프로토콜로의 전환

2025년 1월 FDA가 승인한 수제트리진(Suzetrigine)은 최초의 NaV1.8 나트륨 채널 차단제 계열로, 오피오이드 의존성 위험 없이 진통 효과를 제공합니다. 임상 적용 결과, 특히 관절 치환술 및 흉부 절제술에서 수치 평가 척도 점수를 동등하게 유지하면서 오피오이드 사용량을 최대 50%까지 줄일 수 있음이 입증되었습니다. NOPAIN 법안의 보험급여 인센티브는 병원 도입을 촉진하며, 초음파 유도 신경 차단은 이제 일상 진료에서 약물 요법을 보완합니다. 전환에는 프로토콜 재교육이 필요하지만 호흡기 사건 감소, 회복 기간 단축, 환자 만족도 향상으로 이어져 수술 후 통증 관리 시장 확대에 기여하는 가시적인 비용 절감 효과를 창출합니다.

오피오이드 중독 위기와 규제 강화

처방약 모니터링 프로그램과 개정된 메디케어 및 메디케이드 서비스 센터(CMS) 지침은 수술 후 오피오이드 처방 일수를 제한하여 의료진의 행정 부담을 가중시킵니다. 의무적 지속교육 커리큘럼은 준수 비용을 증가시키고 보수적인 처방을 유도하여 복잡한 사례에서 진통제 공백을 남길 수 있습니다. 보험사들이 비오피오이드 치료법을 점점 더 보장하는 반면, 초기 구입 가격은 여전히 높아 소규모 병원의 광범위한 도입을 저해합니다. 오피오이드 공급과 관련된 불확실한 규제 동향은 공급망 비상 대책을 강요하여 재고 비용을 증가시킵니다. 이러한 요인들은 종합적으로 수술 후 통증 관리 시장의 오피오이드 부문 단기 수익 확대를 제약합니다.

부문 분석

국소 마취제는 2026-2031년의 7.94%의 가장 빠른 연평균 복합 성장률(CAGR) 전망을 보이며 오피오이드, 비스테로이드성 항염증제(NSAID), 선택적 COX-2 억제제(COX-2) 카테고리를 앞질렀습니다. 리포솜 부피바카인의 정형외과 및 복부 수술 부문 광범위한 적응증 확대는 실질적인 오피오이드 사용 감소와 입원 기간 단축을 보여줍니다. 국소 마취제의 수술 후 통증 관리 시장 규모는 ERAS 프로토콜 보급률과 함께 증가할 것으로 예상됩니다. 매출 기준으로 오피오이드는 2025년 수술 후 통증 관리 시장 점유율 41.73%를 유지했으나, 처방 제한과 사회적 감시로 인해 해당 부문의 미래 성장에는 한계가 있습니다. 중간 스펙트럼 NSAID 계열은 거의 모든 다중 모드 경로에 포함되는 이점을 누리지만, 위장관 관련 경고사항이 성장을 저해하고 있습니다. 후속 분자 승인 시 2027년까지 시장 점유율 변화를 가져올 수 있는 신개념 NaV1.8 억제제가 시장에 진입할 예정입니다. 지역 마취 파이프라인의 깊이는 비전신적 기전에 대한 지속적인 관심을 반영하며, 국소 마취제의 전략적 위치를 공고히 합니다.

2세대 저장형 리도카인과 지속 방출형 로피바카인 임플란트는 해당 카테고리의 지속 시간 우위를 확장할 수 있으며, 보조제로 사용되는 가바펜티노이드 및 알파-2 작용제와 함께 독성 증가 없이 시너지적 진통 효과를 제공합니다. 지불 기관이 총 치료 비용 지표를 검토함에 따라, 입원 중 오피오이드 구제 약물 및 재입원을 줄이는 장기 작용 국소 마취제를 처방 목록에서 선호하는 경향이 증가하고 있습니다. 이러한 경제적 논리는 제조사와 공급자 간 지속적인 사용 증가에 대한 공감대를 형성하며, 광범위한 수술 후 통증 관리 시장 내에서 국소 마취제의 매출 점유율 상승 전망을 뒷받침합니다.

경구 투여 방식은 확립된 용량 친숙도와 낮은 단위당 비용에 힘입어 2025년 매출의 56.03%를 유지했습니다. 그러나 마이크로니들 및 스마트 패치의 발전으로 국소 투여 시장 성장률은 2031년까지 연평균 7.25%의 CAGR을 기록하며 모든 투여 경로 중 가장 빠른 속도를 보일 전망입니다. 경피 전달 시스템은 일관된 혈장 농도 유지, 간호 개입 감소, 외래 환자 회복 지원 등 수술이 당일 퇴원 환경으로 전환됨에 따라 핵심적인 이점을 제공합니다. 현재 도입률이 지속될 경우, 국소 전달 방식과 연계된 수술 후 통증 관리 시장 규모는 2030년까지 100억 달러에 육박할 전망입니다.

주사제는 특히 외상 및 신속한 작용이 필요한 고위험 심장 질환 사례에서 수술 직후 단계에 여전히 필수적입니다. 그러나 병원들의 약제비 지출에 대한 집중으로 내약성이 허용될 경우 경구 대체제를 선호하는 정맥주사 처방 기준이 강화되고 있습니다. 지속형 신경 차단 주사제는 주요 관절 및 척추 수술 시 진통 효과를 연장시켜 전신 약물 수요를 감소시킵니다. 기술 협력으로 웨어러블 기기와 경피 패치를 결합해 스마트폰 앱을 통한 방출 조절이 가능해져 개인 맞춤화와 복약 순응도가 향상됩니다. 이러한 통합 솔루션은 경쟁이 치열한 수술 후 통증 관리 시장에서 공급업체 간 차별화 요소가 되고 있습니다.

지역별 분석

북미는 ERAS(회복 가속화 수술 관리)의 강력한 도입, 엄격한 오피오이드 규제, 비오피오이드 대체제를 선호하는 보험급여 정책으로 2025년 세계의 매출의 34.16%를 차지했습니다. NaV1.8 억제제에 대한 FDA 승인 및 외래 수술 센터 네트워크 확대로 수요가 유지되는 반면, 보험사들의 엄격한 심사는 증거 기반 제품 선택을 요구합니다. 4조 달러를 넘어서는 의료 시스템 예산은 프리미엄 지속형 국소 마취제 및 AI 기반 투약 소프트웨어에 대한 수용력을 보장하며, 이 지역의 선도적 위치를 공고히 합니다.

아시아태평양은 중국, 인도, 일본, 한국에서 수술 건수가 증가함에 따라 6.55%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다. 국민보험의 확충과 병원 근대화의 추진에 의해 2차 도시에도 ERAS(조기 회복술 후 케어) 경로가 도입되어, 다각적 통증 관리법의 채택이 촉진되고 있습니다. 국내 제조업체는 비용 경쟁력이 있는 제네릭 의약품을 활용하면서 다국적 기업과 디포 제제로 제휴함으로써 제품의 액세스 확대를 도모하고 있습니다. ASEAN 지역 내의 규제조화로 등록 과정이 가속화되고 수술 후 통증 관리 시장의 지역 확대가 더욱 진행되고 있습니다.

유럽은 통합된 임상 지침과 유럽의약품청(EMA)의 지속적인 오피오이드 절감 지침에 힘입어 꾸준한 성장세를 보이고 있습니다. 기술 도입이 빠른 것으로 유명한 스칸디나비아 및 DACH(독일, 오스트리아, 스위스) 국가에서는 국소 및 지역 마취제 혁신이 주목받고 있습니다. 중동 및 아프리카 및 남미는 여전히 신흥 시장이지만, 걸프협력회의(GCC) 투자와 브라질 공공 부문 조달이 프리미엄 진통제의 교두보 역할을 하고 있습니다. 종합적으로 이러한 역학은 수술 후 통증 관리 시장의 지리적으로 균형 잡힌 확장 가능성을 강조합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 증가하는 수술 건수

- 다중 모드 및 비오피오이드 프로토콜로의 전환

- 지속형 국소/신경 차단 마취제의 도입

- 외래수술센터(ASC)의 확대에 의한 신속 회복형 진통제 수요 창출

- ERAS 치료 경로의 AI 구동형 개별화 투여

- 비오피오이드 진통제의 상환에 관한 법적 인센티브

- 시장 성장 억제요인

- 오피오이드 중독 위기와 규제 강화

- 프리미엄 정맥 주사 제형 억제를 위한 병원 비용 절감

- 비스테로이드성 항염증제(NSAID) 및 COX-2 억제제의 소화기계 및 심혈관 리스크

- 주요 서방형 제형의 특허 만료

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체 위협

- 구매자 협상력

- 공급기업 협상력

- 대체품 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측(금액 : 달러)

- 약제 클래스별

- 오피오이드

- 비스테로이드성 항염증제(NSAID)

- COX-2 억제제

- 국소 마취제

- 보조 진통제

- 투여 경로별

- 주사제

- 경구

- 국소/경피제

- 척수강내/경막외

- 흡입제

- 수술 유형별

- 정형외과

- 순환기 및 흉부

- 복부 및 소화기계

- 산부인과

- 안과 및 이비인후과

- 기타

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- AbbVie(Allergan)

- Heron Therapeutics

- Cali Biosciences

- Innocoll

- Bayer AG

- GSK plc.

- Pacira BioSciences Inc.

- Johnson & Johnson(Janssen)

- AFT Pharmaceuticals

- Alembic Pharmaceuticals

- Cipla Inc.

- SiteOne Therapeutics

- Pfizer Inc.

- Teva Pharmaceutical Industries

- Endo International

- Eli Lilly & Co.

- Novartis AG

- Purdue Pharma

- Mallinckrodt plc

- Boston Scientific

- Medtronic

제7장 시장 기회와 장래의 전망

HBR 26.01.29Post Operative Pain Management Market size in 2026 is estimated at USD 45.29 billion, growing from 2025 value of USD 42.84 billion with 2031 projections showing USD 59.82 billion, growing at 5.72% CAGR over 2026-2031.

Steady adoption of multimodal analgesia, reimbursement incentives for non-opioid options, and long-acting regional techniques are accelerating demand across surgical specialties. Orthopedic, cardiovascular, and thoracic procedures anchor consumption, while Enhanced Recovery After Surgery (ERAS) protocols position local anesthetics and topical innovations for outsized growth. Cost-sensitive hospitals are trimming premium intravenous usage, yet AI-driven personalized dosing and digital pharmacy distribution continue to unlock efficiency gains. Competitive intensity is mounting as established pharmaceutical firms and biotech entrants vie to commercialize NaV1.8 inhibitors, extended-release nerve-block injectables, and smart transdermal systems.

Global Post-Operative Pain Management Market Trends and Insights

Growing Number of Surgical Procedures

Ambulatory surgery centers increased from 612 specialized pain-focused facilities in 2018 to more than 800 by 2023, signaling accelerating procedure volumes that heighten baseline demand for multimodal analgesia. Aging populations in developed economies fuel orthopedic and cardiovascular operations, driving consistent consumption of regional anesthetics and adjuvant agents. ERAS pathways have become mainstream, institutionalizing evidence-based protocols that reduce length of stay while safeguarding pain control. Regulatory guidance under United States Food and Drug Administration (FDA) labeling promotes standardized postoperative dosing, giving hospitals a clear compliance roadmap. As volumes rise, suppliers that streamline dosing complexity and inventory management stand to capture incremental share in the post operative pain management market.

Shift Toward Multimodal & Non-Opioid Protocols

January 2025 FDA approval of suzetrigine introduced the first NaV1.8 sodium-channel blocker class, delivering analgesia without opioid dependency risk. Clinical implementation demonstrates up to 50% opioid reduction while preserving equivalent Numeric Rating Scale scores, especially in joint replacement and thoracic resections. Reimbursement incentives under the NOPAIN Act bolster hospital adoption, and ultrasound-guided nerve blocks now complement pharmacologic regimens in routine practice. The changeover requires protocol re-training but yields fewer respiratory events, shorter recovery, and higher patient satisfaction, all driving measurable savings that enlarge the post operative pain management market.

Opioid Addiction Crisis & Tightening Regulations

Prescription-drug monitoring programs and updated Centers for Medicare & Medicaid Services (CMS) guidelines limit postoperative opioid days' supply, compounding administrative load for providers. Mandatory continuing-education curricula raise compliance costs and prompt conservative prescribing that may leave analgesic gaps in complex cases. While insurers increasingly cover non-opioid modalities, upfront acquisition prices remain higher, deterring broad adoption in smaller hospitals. The uncertain regulatory trajectory around opioid availability compels supply-chain contingencies, adding inventory expense. These factors collectively constrain near-term revenue expansion for opioid segments of the post operative pain management market.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Long-Acting Regional/Nerve-Block Anesthetics

- Expansion of Ambulatory Surgery Centers Creating Demand for Rapid-Recovery Analgesics

- Hospital Cost-Containment Curbing Premium IV Formulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Local anesthetics produced the fastest 7.94% CAGR outlook from 2026-2031, outpacing opioid, NSAID, and COX-2 categories. Liposomal bupivacaine's broad labeling across orthopedic and abdominal surgeries showcases tangible opioid reductions and shortened length of stay. The post operative pain management market size for local anesthetics is expected to rise in lockstep with ERAS protocol penetration. Measured by revenue, opioids still commanded a 41.73% post operative pain management market share in 2025, yet the segment's future is capped by prescribing limits and social scrutiny. The mid-spectrum NSAID class benefits from inclusion in nearly every multimodal pathway, though gastrointestinal warnings temper growth. Novel NaV1.8 inhibitors will enter the mix, potentially shifting share by 2027 when follow-on molecules gain approval. Regional anesthesia pipeline depth underlines sustained attention to non-systemic mechanisms, reinforcing local anesthetics' strategic position.

Second-generation depot lidocaine and sustained-release ropivacaine implants may extend the category's duration edge, while together with adjuvant gabapentinoids and alpha-2 agonists they deliver synergistic analgesia without additive toxicity. As payers examine total-cost-of-care metrics, formularies increasingly prefer long-acting local anesthetics that reduce inpatient opioid rescue meds and readmissions. This economic story aligns manufacturers and providers on continuous utilization increases, underpinning the rising revenue share forecast for local anesthetics within the broader post operative pain management market.

Oral modalities retained 56.03% of 2025 sales, driven by established dosing familiarity and low per-unit cost. Microneedle and smart-patch advances, however, push topical market growth to a 7.25% CAGR through 2031, the fastest across all routes. Transdermal systems deliver consistent plasma levels, reduce nursing interventions, and support outpatient recovery, a pivotal advantage as surgeries shift to same-day settings. The post operative pain management market size tied to topical delivery should approach double-digit billion-dollar levels by 2030 if current adoption rates persist.

Injectables remain indispensable for immediate postoperative phases, especially in trauma and high- acuity cardiac cases requiring rapid onset. Yet hospitals' focus on pharmacy spend prompts tighter criteria for IV orders in favor of oral equivalents when tolerated. Depot nerve-block injectables prolong analgesia for major joints and spine surgery, cutting demand for systemic medications. Technology collaborations pair wearables with transdermal patches that modulate release via smartphone apps, enhancing personalization and adherence. Such integrated solutions differentiate suppliers in the competitive post operative pain management market.

The Post-Operative Pain Management Market Report is Segmented by Drug Class (Opioids, Nsaids, and More), Route of Administration (Injectable, Oral, and More), Surgery Type (Orthopedic, Cardiovascular & Thoracic, and More), Distribution Channel (Hospital Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 34.16% of global revenue in 2025 amid strong ERAS adoption, stringent opioid regulations, and reimbursement levers that favor non-opioid alternatives. FDA green-lights for NaV1.8 inhibitors and expanding ambulatory surgery center networks sustain demand, while payer scrutiny compels evidence-backed product selection. Health-system budgets topping USD 4 trillion ensure capacity for premium extended-release local anesthetics and AI-enabled dosing software, cementing the region's leadership position.

Asia-Pacific is advancing at a 6.55% CAGR as surgical volumes climb in China, India, Japan, and South Korea. National insurance expansions and hospital-modernization drives bring ERAS pathways to secondary cities, stimulating uptake of multimodal regimens. Domestic manufacturers leverage cost-competitive generics while partnering with multinationals for depot formulations, thereby broadening product access. Regulatory harmonization across ASEAN accelerates registration timelines, further enlarging the post operative pain management market footprint in the region.

Europe posts steady growth tied to unified clinical guidelines and ongoing opioid-sparring directives from the European Medicines Agency. Topical and regional anesthetic innovations gain traction in Scandinavian and DACH countries renowned for early technology adoption. Middle East & Africa and South America remain emergent, yet Gulf Cooperation Council investments and Brazil's public-sector procurements provide beachheads for premium analgesics. Collectively, these dynamics underline geographically balanced expansion potential for the post operative pain management market.

- Abbvie

- Heron Therapeutics

- Cali Biosciences

- Innocoll

- Bayer

- GlaxoSmithKline

- Pacira BioSciences Inc.

- Johnson & Johnson

- AFT Pharmaceuticals

- Alembic Pharmaceuticals

- Cipla

- SiteOne Therapeutics

- Pfizer

- Teva Pharmaceutical Industries

- Endo International

- Eli Lilly and Company

- Novartis

- Purdue Pharma

- Mallinckrodt plc

- Boston Scientific

- Medtronic

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Number of Surgical Procedures

- 4.2.2 Shift Toward Multimodal & Non-Opioid Protocols

- 4.2.3 Adoption of Long-Acting Regional/Nerve-Block Anesthetics

- 4.2.4 Expansion of Ambulatory Surgery Centers (ASCs) Creating Demand for Rapid-Recovery Analgesics

- 4.2.5 AI-Driven Personalized Dosing Within ERAS Pathways

- 4.2.6 Legislative Incentives for Non-Opioid Analgesic Reimbursement

- 4.3 Market Restraints

- 4.3.1 Opioid Addiction Crisis & Tightening Regulations

- 4.3.2 Hospital Cost-Containment Curbing Premium IV Formulations

- 4.3.3 GI / Cardiovascular Risks of NSAIDs & Cox-2 Inhibitors

- 4.3.4 Patent Cliffs on Key Extended-Release Formulations

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Drug Class

- 5.1.1 Opioids

- 5.1.2 NSAIDs

- 5.1.3 COX-2 Inhibitors

- 5.1.4 Local Anesthetics

- 5.1.5 Adjuvant Analgesics

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Oral

- 5.2.3 Topical / Transdermal

- 5.2.4 Intrathecal / Epidural

- 5.2.5 Inhalational

- 5.3 By Surgery Type

- 5.3.1 Orthopedic

- 5.3.2 Cardiovascular & Thoracic

- 5.3.3 Abdominal & Gastrointestinal

- 5.3.4 Obstetrics & Gynecology

- 5.3.5 Ophthalmic & ENT

- 5.3.6 Others

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie (Allergan)

- 6.3.2 Heron Therapeutics

- 6.3.3 Cali Biosciences

- 6.3.4 Innocoll

- 6.3.5 Bayer AG

- 6.3.6 GSK plc.

- 6.3.7 Pacira BioSciences Inc.

- 6.3.8 Johnson & Johnson (Janssen)

- 6.3.9 AFT Pharmaceuticals

- 6.3.10 Alembic Pharmaceuticals

- 6.3.11 Cipla Inc.

- 6.3.12 SiteOne Therapeutics

- 6.3.13 Pfizer Inc.

- 6.3.14 Teva Pharmaceutical Industries

- 6.3.15 Endo International

- 6.3.16 Eli Lilly & Co.

- 6.3.17 Novartis AG

- 6.3.18 Purdue Pharma

- 6.3.19 Mallinckrodt plc

- 6.3.20 Boston Scientific

- 6.3.21 Medtronic

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment