|

시장보고서

상품코드

1911374

마이크로컨트롤러(MCU) 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Microcontroller (MCU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

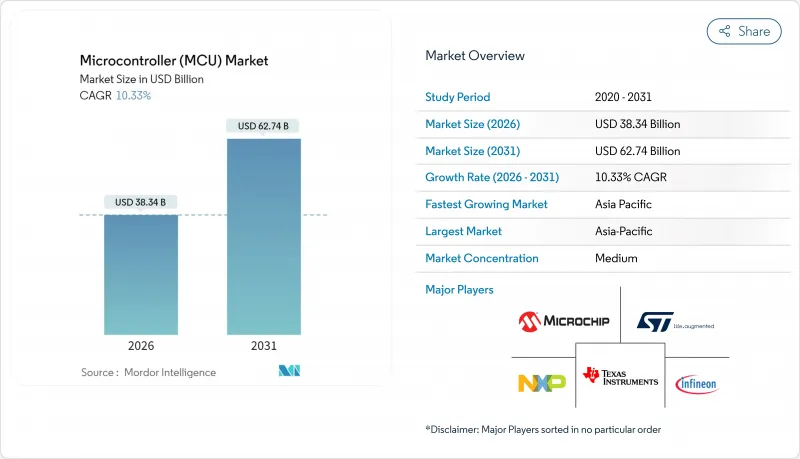

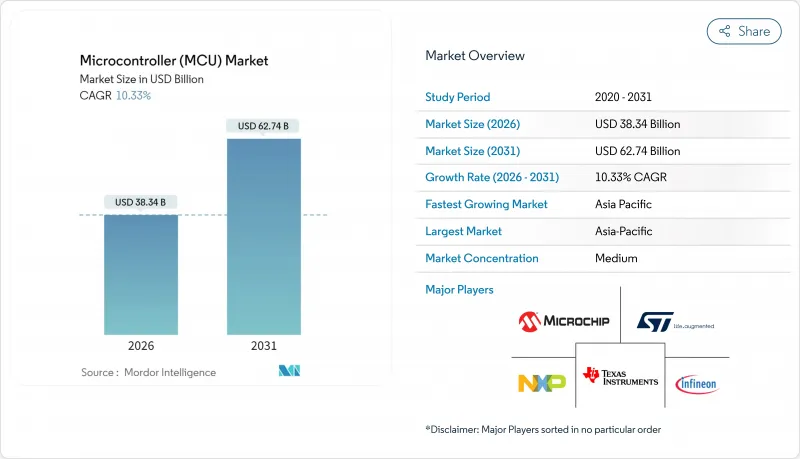

마이크로컨트롤러(MCU) 시장은 2025년 347억 5,000만 달러로 평가되었으며, 2026년 383억 4,000만 달러에서 2031년까지 627억 4,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 10.33%로 예상됩니다.

이 성장 궤적은 전기 차량, 사물 인터넷(IoT) 엔드포인트, 차세대 소비자를 위한 장치에서의 임베디드 인텔리전스 수요 증가를 반영합니다. 기능안전규제의 확대에 의해 자동차의 MCU 탑재수가 증가하는 한편, 공장에서의 예지보전 프로그램이 스마트 센서의 도입을 가속화하고 있습니다. 개방형 명령어 세트 아키텍처는 라이선스 비용을 절감하고 중소 벤더가 엣지 AI 워크로드를 지원할 수 있도록 뒷받침합니다. 한편 지역적 니어쇼어링과 공급망의 다양화로 평균 판매가격(ASP)이 계속 축소하고 있는 가운데 새로운 생산능력에 대한 투자가 촉진되고 있습니다.

세계의 마이크로컨트롤러(MCU) 시장의 동향 및 인사이트

IoT 노드 급증이 임베디드 인텔리전스의 수요 견인

연결된 엔드포인트는 2030년까지 200억 대를 초과할 것으로 예상되며 제조업체는 비용 중심 설계에 다중 프로토콜 무선 및 효율적인 프로세서를 통합해야 합니다. 노르딕 세미컨덕터의 nRF54 시리즈는 Bluetooth LE 5.4, Thread, Matter를 단일 디바이스에 통합하고 배터리 친화적인 전류 소비량을 유지함으로써 BOM(Boom Table) 비용과 펌웨어 복잡성을 줄입니다. 보다 풍부한 로컬 처리로 실현되는 고가의 분석 서비스는 순수 하드웨어 판매로부터 수익 모델을 전환합니다. Synaptics와 같은 반도체 공급업체는 범용 컴퓨팅을 추구하는 것이 아니라 IoT 최적화 솔루션을 위해 포트폴리오를 재구성하고 있습니다.

자동차의 전기화와 ADAS 통합이 MCU 탑재량 증가를 가속화

배터리형 전기자동차에는 최대 3,000개의 반도체 부품이 탑재되어 내연기관 모델에 비해 MCU의 탑재 수가 4배로 증가합니다. Mercedes-Benz는 ISO 26262를 준수하며 배터리, 열 관리 및 회생 제동 시스템을 관리하기 위해 이산 마이크로컨트롤러 클러스터를 채택합니다. 콘티넨탈과 NXP의 협력은 소프트웨어 업데이트가 가능한 도메인 컨트롤러에 여러 섀시 기능을 통합하여 배선 무게를 줄이고 원활한 무선 업데이트(OTA)를 제공합니다. 2026년까지 전차종에 대한 첨단 운전자 보조 시스템(ADAS) 탑재를 의무화하는 EU 규제가 이 변화를 더욱 가속화하고 있습니다. 혼다와 르네사스의 제휴에 의한 2,000 TOPS SoC의 공동 개발은 계산 처리 수요가 마이크로컨트롤러 시장을 재구축하고 있는 실태를 부각하고 있습니다.

공급망의 순환성은 재고와 가격 변동을 일으킵니다.

파운드리의 생산 일정 변화로 인해 MCU 공급업체는 갑작스런 웨이퍼 할당 변경에 노출되었습니다. 최근 재고 소화 국면에서는 노르딕 세미컨덕터사가 2023년 매출액이 30% 감소하여 직원의 8%를 해고할 수밖에 없었습니다. 금속 실리콘의 공급 과잉으로 인해 2025년 4월 벤치마크 스팟 가격은 2.3% 하락하여 2.95달러/kg가 되었지만 관세가 비용 절감 효과를 역전시킬 우려가 있습니다. 성숙 노드의 생산 능력이 대만, 중국 본토, 한국에 집중되어 지정학적 리스크 프리미엄이 증폭되고 OEM은 운전 자금을 구속하는 비축 재고에 대한 자금 조달을 요구받고 있습니다.

부문 분석

2025년에는 32비트 디바이스가 마이크로컨트롤러(MCU) 시장에서 점유율 56.35%를 차지하면서 복잡한 워크로드로의 명확한 전환을 보여주었습니다. 이 부문은 ADAS 센서 퓨전, 산업용 드라이브 제어 및 음성 대응 소비자 가젯의 수요 증가로 CAGR 8.76%를 보일 것으로 예측됩니다. 32비트 아키텍처는 더 큰 참조 가능 메모리를 구현하고 디지털 신호 처리 확장 기능을 통합하여 외부 부품의 필요성을 줄입니다. MCU 디자이너는 현재 신경 엔진과 사이버 보안 가속기를 다이에 직접 통합하여 이산 코프로세서의 필요성을 없앱니다. 저렴한 8비트 및 16비트 제품은 여전히 인터페이스 로직 부문에서 효과적이지만, 4비트 이하의 변형은 초박리 부문용 리모컨 및 서모스탯에 계속 사용되고 있습니다.

개발자는 보안 부팅, CAN-FD 및 멀티 프로토콜 라디오를 단일 패키징에 통합한 단일 칩 프로토타입을 요구하고 있습니다. 이 올인원 동향은 제품 라인을 가로질러 플랫폼 재사용을 가능하게 하여 펌웨어 유지보수를 줄입니다. 한편, 32비트 유닛에 통합된 FRAM 옵션은 차지 펌프 오버헤드 없이 즉각적인 쓰기 기능을 제공하며 이는 고진동 환경에서 작동하는 데이터 로깅 센서에 매우 중요합니다.

2025년에는 Cortex-M 코어가 매출의 68.25%를 차지했으며, 성숙한 툴체인과 견고한 미들웨어 스택이 이를 뒷받침했습니다. 고객은 디버깅 주기를 단축하는 가용 RTOS 지원과 풍부한 커뮤니티 라이브러리를 높이 평가합니다. 그러나 RISC-V의 CAGR 15.09%는 로열티 비용이 없는 명령어 세트 커스터마이징에 대한 요구가 높아지고 있음을 보여줍니다. 각국 정부는 기술 주권을 지키기 위해 국내 RISC-V 프로그램을 전개하고, 웨어러블에서 자동차 게이트웨이 노드까지 커버하는 오픈 ISA 칩렛에 보조금을 투입하고 있습니다. 한편, 결정론적이고 사이클 정밀도가 높은 응답이 요구되는 아비오닉스나 산업용 드라이브의 틈새 부문에서는 독자적인 코어가 계속 사용되고, 서버 클래스의 보드 관리 컨트롤러에는 x86 프로세서가 도입되고 있습니다.

마이크로컨트롤러(MCU) 시장에서 벤더의 성공은 개발 환경의 충실도에 달려 있습니다. ARM은 TrustZone, PSA 인증 보안, M-Profile 벡터 확장을 계속 확대하는 반면, RISC-V 그룹은 부문화를 방지하기 위해 소프트웨어 계층의 통합에 주력하고 있습니다. 일부 공급업체는 동일한 제품군 내에서 핀 호환 ARM 또는 RISC-V 대체품을 제공하여 위험 분산을 도모합니다.

지역별 분석

아시아태평양은 중국의 가전 조립 에코시스템과 일본의 자동차용 반도체 부문의 강점을 배경으로 2025년에도 세계 매출의 47.30%를 차지했습니다. 중국의 '실리콘 자율'을 목표로 하는 5개년 계획은 가전제품 및 공공충전 인프라용 국내 MCU의 테이프아웃 수요를 창출하고 있습니다. 일본 공급업체는 기존 OEM과의 협력을 활용하여 하이브리드 구동 사이클을 위해 특별히 설계된 파워트레인 인증 마이크로컨트롤러로 존재감을 유지하고 있습니다. 한국의 대기업은 네이티브 메모리 IP와 로직 블록을 통합하여 스마트폰과 스마트 TV용 원칩 솔루션을 구축하고 있습니다. 노동력 에너지 비용의 상승과 지정학적 리스크 증가로 베트남과 태국으로의 분산이 진행되는 한편, 이 지역의 결속된 부품 에코시스템이 비교 우위성을 유지해, 마이크로컨트롤러(MCU) 시장에서 가장 성장이 빠른 지역으로서의 지위를 유지하고 있습니다.

남미는 마이크로컨트롤러(MCU) 시장에서 가장 성장이 현저한 지역의 하나로 대두하고 있으며, 2020-2031년에 걸쳐 CAGR 10.22%가 전망되고 있습니다. 브라질에서의 자동차 생산 장려책 재개와 미국, 멕시코 및 캐나다 협정(USMCA)에 의한 멕시코 수출 회랑은 현지 조달된 마이크로컨트롤러가 필요한 전기자동차 플랫폼의 조립을 유치하고 있습니다. 정부 주도의 재생에너지망은 스마트 미터의 도입을 촉진하고, 이는 안전하고 저전력인 32비트 컨트롤러 수요를 높이고 있습니다. 현지 조달률 의무화로 세계 반도체 벤더와 지역 설계 회사의 합작 사업이 촉진되어 임베디드 소프트웨어 스택 부문의 인재 육성이 가속화되고 있습니다. 북미는 고부가가치 안전 부문에 주력하고 있습니다. CHIPS법은 웨이퍼 공장 건설에 수십억 달러를 계상하고 있지만, 대부분의 생산 능력은 성숙한 MCU 프로세스가 아니라 10nm 이하의 노드를 목표로 하고 있습니다. 방위 관련 기업은 국내 생산과 공급망 보증을 요구하고 있으며 ITAR 준수 부품의 안정적인 수요를 확보하고 있습니다. 유럽에서는 자동차 및 공정 자동화 부문에서 ISO 26262 및 IEC 62443을 준수하는 데 주력하고 있습니다. TSMC가 계획하고 있는 드레스덴 공장은 유럽의 티어 1 기업에 월 4만장의 300mm 웨이퍼를 공급하여 고신뢰성 마이크로컨트롤러의 리드 타임 단축을 실현합니다.

기타 혜택

- 시장 예측(ME) 엑셀 시트

- 3개월 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 촉진요인

- IoT 노드의 보급

- 자동차의 전동화와 ADAS(첨단 운전자 보조 시스템)

- 스마트 홈과 가전용 마이크로컴퓨터의 통합

- RISC-V 오픈 ISA로의 이행

- 초저전력 엣지 AI 마이크로컴퓨터

- 산업용 사이버 보안의 의무화

- 억제요인

- 공급망의 주기성

- 중국 팹에 의한 평균 판매 가격(ASP)의 저하

- 28nm 이하 내장 플래시 메모리의 개발 비용(NRE) 증가

- 혼합 신호 설계의 인재 부족

- 가치 및 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급자의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 비트 클래스별

- 4비트 이하

- 8비트

- 16비트

- 32비트

- 코어 아키텍처별

- ARM Cortex-M

- RISC-V

- x86

- 독자 기술 및 기타

- 온칩 메모리 유형별

- 임베디드 플래시 메모리

- FRAM

- EEPROM/OTP

- SRAM 전용(코드인 RAM)

- 용도별

- 자동차

- 가전과 가전제품

- 산업 및 공장 자동화

- 의료

- 항공우주 및 방위

- 데이터 통신 클라우드 인프라

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 대만

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Infineon Technologies AG

- Microchip Technology Inc.

- NXP Semiconductors NV

- STMicroelectronics NV

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- Silicon Laboratories Inc.

- Nordic Semiconductor ASA

- Espressif Systems(Shanghai) Co., Ltd.

- GigaDevice Semiconductor Inc.

- Nuvoton Technology Corporation

- Toshiba Electronic Devices and Storage Corporation

- Rohm Co., Ltd.

- onsemi Corporation

- Holtek Semiconductor Inc.

- Ambiq Micro, Inc.

- ASR Microelectronics(Shanghai) Co., Ltd.

- Realtek Semiconductor Corp.

- Zilog, Inc.

- Analog Devices, Inc.

제7장 시장 기회 및 미래 전망

CSM 26.02.04The Microcontroller market was valued at USD 34.75 billion in 2025 and estimated to grow from USD 38.34 billion in 2026 to reach USD 62.74 billion by 2031, at a CAGR of 10.33% during the forecast period (2026-2031).

This trajectory reflects the rising demand for embedded intelligence across electrified vehicles, Internet of Things (IoT) endpoints, and next-generation consumer devices. Content per car is increasing as functional-safety mandates expand MCU counts, while predictive-maintenance programs in factories accelerate the rollout of smart sensors. Open instruction-set architectures reduce licensing costs, helping smaller vendors address edge-AI workloads. Meanwhile, regional near-shoring and supply-chain diversification stimulate fresh capacity investments even as average selling prices (ASP) remain under pressure.

Global Microcontroller (MCU) Market Trends and Insights

IoT Node Proliferation Drives Embedded Intelligence Demand

Connected endpoints are projected to exceed 20 billion units by 2030, forcing manufacturers to embed multi-protocol radios and efficient processors into cost-sensitive designs. Nordic Semiconductor's nRF54 series combines Bluetooth LE 5.4, Thread, and Matter in a single device, while maintaining a battery-friendly current draw, thereby reducing the bill of materials and firmware complexity . Premium-priced analytics services, enabled by richer local processing, shift revenue models away from pure hardware sales. Semiconductor suppliers, such as Synaptics, are repositioning their portfolios toward IoT-optimized solutions rather than pursuing general-purpose computing.

Automotive Electrification and ADAS Integration Accelerate MCU Content Growth

A battery-electric vehicle can host up to 3,000 semiconductor components, quadrupling the MCU footprint versus internal-combustion models. Mercedes-Benz relies on discrete microcontroller clusters to manage the battery, thermal, and regenerative braking systems in accordance with ISO 26262. Continental's cooperation with NXP centralizes multiple chassis functions into software-upgradable domain controllers, cutting wiring weight and enabling seamless over-the-air updates. EU regulations mandating the deployment of advanced driver-assistance systems across all classes by 2026 further amplify this shift. Honda's partnership with Renesas to co-develop 2,000 TOPS SoCs highlights how computational demands are reshaping the Microcontroller market.

Supply-Chain Cyclicality Creates Inventory and Pricing Volatility

Foundry scheduling swings expose MCU vendors to abrupt wafer-allocation shifts. Recent inventory digestion phases forced Nordic Semiconductor to cut 8% of its workforce after revenue fell 30% in 2023 . The oversupply of metal-silicon pulled benchmark spot prices down 2.3% to USD 2.95/kg in April 2025, yet tariffs threaten to reverse the cost gains . The concentration of mature-node capacity in Taiwan, mainland China, and South Korea magnifies geopolitical risk premiums, prompting OEMs to fund buffer stocks that tie up working capital.

Other drivers and restraints analyzed in the detailed report include:

- Smart-Home and Appliance MCU Integration Transforms Consumer Electronics

- Shift to RISC-V Open ISA Disrupts Traditional Licensing Models

- ASP Erosion from Chinese Fabs Intensifies Pricing Competition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, 32-bit devices captured 56.35% of the Microcontroller market share, illustrating a decisive tilt toward complex workloads. The segment is projected to grow at an 8.76% CAGR, driven by ADAS sensor fusion, industrial drive control, and voice-enabled consumer gadgets. 32-bit architectures enable larger addressable memory and integrate digital-signal-processing extensions, thereby reducing the need for external components. MCU designers now embed neural engines and cybersecurity accelerators directly on the die, eliminating the need for discrete coprocessors. Lower-cost 8-bit and 16-bit parts remain viable in interface logic, while sub-4-bit variants linger in remote controls and thermostats serving ultra-thin margin categories.

Developers are increasingly requesting single-chip prototypes that incorporate secure boot, CAN-FD, and multi-protocol radio in a single package. This all-in-one trend supports platform reuse across product lines, reducing firmware maintenance. Meanwhile, integrated FRAM options on 32-bit units provide instant-write capability without charge-pump overhead, which is critical for data-logging sensors that operate in high-vibration environments.

Cortex-M cores supplied 68.25% of shipments in 2025, bolstered by mature toolchains and robust middleware stacks. Customers value out-of-the-box RTOS support and expansive community libraries that shorten debug cycles. Yet RISC-V's 15.09% CAGR points to mounting enthusiasm for instruction-set customization at zero royalty cost. Governments deploy domestic RISC-V programs to safeguard technology sovereignty, funneling subsidies toward open-ISA chiplets spanning wearables to automotive gateway nodes. Proprietary cores persist in niche avionics and industrial drives that require deterministic, cycle-accurate responses, whereas x86 processors are used in server-class board management controllers.

For the Microcontroller market, vendor success hinges on the richness of the development environment. ARM continues to extend TrustZone, PSA-Certified security, and M-Profile Vector Extensions, whereas RISC-V groups invest in unified software-layer harmonization to stave off fragmentation. Some suppliers hedge bets by offering pin-compatible ARM or RISC-V alternatives within the same product family.

The Microcontroller Market Report is Segmented by Bit Class (4-Bit and Below, 8-Bit, 16-Bit, and More), Core Architecture (ARM Cortex-M, RISC-V, X86, and More), On-Chip Memory Type (Embedded Flash, FRAM, and More), Application (Automotive, Industrial and Factory Automation, Healthcare, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

APAC retained 47.30% of global revenue in 2025 on the strength of China's consumer-electronics assembly ecosystem and Japan's automotive semiconductor depth. Chinese five-year plans targeting local silicon autonomy create pull for domestic MCU tape-outs across home appliances and public-charging infrastructure. Japanese suppliers maintain traction with powertrain-qualified microcontrollers specifically designed for hybrid drive cycles, leveraging their long-standing OEM ties. South Korean conglomerates integrate native memory IP with logic blocks to build one-chip solutions for smartphones and smart TVs. Rising labor, energy, and geopolitical costs prompt some diversification into Vietnam and Thailand, yet the region's cohesive component ecosystem preserves its comparative advantage, keeping it as the fastest-growing market for microcontrollers.

South America emerges as one of the fastest-growing regions in the microcontroller market, with a 10.22% CAGR from 2020 to 2031. Brazil's renewed automotive-production incentives and Mexico's USMCA-enabled export corridors lure EV platform assembly that requires localized MCU sourcing. Government-directed renewable energy grids are driving the rollout of smart meters, which in turn boosts demand for secure, low-power 32-bit controllers. Local-content mandates spur joint ventures between global silicon vendors and regional design houses, catalyzing the development of talent around embedded software stacks. North America centers on high-value safety-critical niches. The CHIPS Act earmarks billions for wafer-fab construction, though most capacity targets sub-10 nm nodes rather than mature MCU geometries. Defense contractors stipulate onshore production and supply-chain attestations, ensuring steady demand for ITAR-compliant parts. Europe focuses on adhering to ISO 26262 and IEC 62443 within the automotive and process automation verticals. TSMC's planned Dresden fab will supply 40,000 300 mm wafers monthly to European Tier-1s, shortening lead times for high-reliability microcontrollers .

- Infineon Technologies AG

- Microchip Technology Inc.

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- Silicon Laboratories Inc.

- Nordic Semiconductor ASA

- Espressif Systems (Shanghai) Co., Ltd.

- GigaDevice Semiconductor Inc.

- Nuvoton Technology Corporation

- Toshiba Electronic Devices and Storage Corporation

- Rohm Co., Ltd.

- onsemi Corporation

- Holtek Semiconductor Inc.

- Ambiq Micro, Inc.

- ASR Microelectronics (Shanghai) Co., Ltd.

- Realtek Semiconductor Corp.

- Zilog, Inc.

- Analog Devices, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IoT Node Proliferation

- 4.2.2 Automotive Electrification and ADAS

- 4.2.3 Smart-Home and Appliance MCU Integration

- 4.2.4 Shift to RISC-V Open ISA

- 4.2.5 Ultra-Low-Power Edge AI MCUs

- 4.2.6 Industrial Cybersecurity Mandates

- 4.3 Market Restraints

- 4.3.1 Supply-chain Cyclicality

- 4.3.2 ASP Erosion from Chinese Fabs

- 4.3.3 Rising NRE for sub-28 nm Embedded Flash

- 4.3.4 Talent Shortage in Mixed-Signal Design

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Bit Class

- 5.1.1 4-bit and below

- 5.1.2 8-bit

- 5.1.3 16-bit

- 5.1.4 32-bit

- 5.2 By Core Architecture

- 5.2.1 ARM Cortex-M

- 5.2.2 RISC-V

- 5.2.3 x86

- 5.2.4 Proprietary / Others

- 5.3 By On-Chip Memory Type

- 5.3.1 Embedded Flash

- 5.3.2 FRAM

- 5.3.3 EEPROM/OTP

- 5.3.4 SRAM-only (code-in-RAM)

- 5.4 By Application

- 5.4.1 Automotive

- 5.4.2 Consumer Electronics and Home Appliances

- 5.4.3 Industrial and Factory Automation

- 5.4.4 Healthcare

- 5.4.5 Aerospace and Defense

- 5.4.6 Data-Com and Cloud Infrastructure

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Taiwan

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Microchip Technology Inc.

- 6.4.3 NXP Semiconductors N.V.

- 6.4.4 STMicroelectronics N.V.

- 6.4.5 Texas Instruments Incorporated

- 6.4.6 Renesas Electronics Corporation

- 6.4.7 Silicon Laboratories Inc.

- 6.4.8 Nordic Semiconductor ASA

- 6.4.9 Espressif Systems (Shanghai) Co., Ltd.

- 6.4.10 GigaDevice Semiconductor Inc.

- 6.4.11 Nuvoton Technology Corporation

- 6.4.12 Toshiba Electronic Devices and Storage Corporation

- 6.4.13 Rohm Co., Ltd.

- 6.4.14 onsemi Corporation

- 6.4.15 Holtek Semiconductor Inc.

- 6.4.16 Ambiq Micro, Inc.

- 6.4.17 ASR Microelectronics (Shanghai) Co., Ltd.

- 6.4.18 Realtek Semiconductor Corp.

- 6.4.19 Zilog, Inc.

- 6.4.20 Analog Devices, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment