|

시장보고서

상품코드

1911716

피스톤 엔진 항공기 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Piston Engine Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

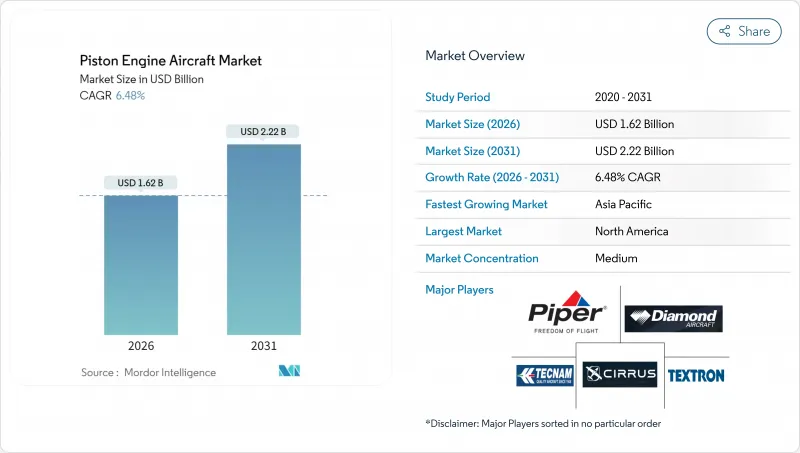

피스톤 엔진 항공기 시장은 2025년 15억 2,000만 달러로 평가되었으며, 2026년 16억 2,000만 달러, 2031년까지 22억 2,000만 달러에 이를 것으로 예측됩니다. 예측기간(2026-2031년)의 CAGR은 6.48%를 나타낼 전망입니다.

파일럿 부족의 심각화, 비행 훈련용 장비의 확충, 경제적인 개인용 및 전세 비행 솔루션에 대한 수요 증가가 이 성장 궤도를 지원하고 있습니다. 비행 훈련교에서는 터빈 엔진기와 비교하여 도입 및 운용 비용이 낮은 신뢰성이 높은 피스톤 설계가 선호되고 있습니다. 제조업체 각사는 전자 점화 장치와 전권 디지털 엔진 제어(FADEC) 기술을 통합하여 경쟁력을 강화하여 정비 비용 절감과 운항 신뢰성 향상을 도모하고 있습니다. 연방항공국(FAA)의 MOSAIC 규정에 따른 경스포츠 항공기의 적용 범위 확대 등 규제면에서의 진전이 보다 중량급으로 장비의 충실한 피스톤 모델에 대한 추가 수요를 환기하고 있습니다. 제트 A-1 연료가 세계적으로 저렴하고 입수하기 쉽기 때문에 비용 의식이 높은 사업자에게 디젤 엔진으로의 개조와 신규 도입의 매력이 높아지고 있습니다.

세계의 피스톤 엔진 항공기 시장 동향과 인사이트

조종사 부족으로 훈련용 항공기 수요 증가

보잉사의 추계에 의하면 항공사 및 비즈니스 항공사는 2043년까지 67만 4,000명의 신규 파일럿을 필요로 하고 있으며, 이 부족으로 비행훈련 수요의 고 정지를 초래하고 있습니다. 엠블리 리들 항공 대학 등의 유력 훈련 기관은 2024년 파이퍼 아처 TX기 50기를 장비에 추가해 현대적인 피스톤식 훈련기에 대한 지속적인 수요를 뒷받침하고 있습니다. 아시아태평양의 지역 항공사는 파일럿 라이선싱의 각 단계에서 단발기와 쌍발기를 필요로 하는 초등 훈련 프로그램을 시작하고 있습니다. 피스톤 엔진기에서의 비행 시간 적산을 의무화하는 규제에 의해 안정된 가동률이 확보되고 있습니다. 이러한 요인은 제조업체와 애프터마켓 공급자에게 수년간 수익원을 확립하고 있습니다.

연료 효율 향상을 위한 피스톤식 디젤 엔진 채택 확대

디젤 엔진은 항공 가솔린 엔진에 비해 최대 40%의 연료 소비 절감이 가능하며 널리 이용 가능한 제트 A-1 연료를 사용할 수 있으므로 북미 이외 지역에서의 물류 부담을 경감합니다. 파이퍼사가 델타호크사와 제휴해 PA-44 세미놀 훈련기의 개조를 실시한 사례는 OEM 제조업체가 직접 운용 비용 절감을 목표로 하는 운항회사를 어떻게 받아들이려고 하고 있는지를 나타내고 있습니다. 다이아몬드사의 오스트로제 엔진 탑재 모델인 DA40 NG 및 DA42 NG는 유럽의 비행 훈련 학교 장비를 석권하고 있으며, 시장에서의 수용성을 뒷받침하고 있습니다. 디젤 엔진은 오버홀 간격을 약 25% 연장하므로 라이프사이클 비용 절감과 재판매 가치 향상에도 기여합니다.

유연항공연료에 대한 엄격한 배출규제

유럽 연합(EU)과 미국 몇 주에서는 2030년까지 100-LL 항공 가솔린의 단계적 폐지를 진행하고 있으며, 소유자는 인증 취득 중 무연 연료로의 이행을 강요받고 있습니다. 스위프트 연료 및 쉘은 100옥탄 무연 연료의 배합 시험을 실시 중이지만, 모든 기대에서의 승인은 2026년 이전에는 어려운 것으로 보입니다. 구식 엔진 탑재기의 운항자는 개조 비용 부담이나 재판매 가치의 저하에 직면할 수 있습니다. 지역에 따라 연료의 입수 상황에 편차가 생길 가능성이 있으며, 이행 기간 중에는 국경을 넘은 운항이 제한될 우려가 있습니다. 이로 인해 구형 항공기의 가동률이 저하될 수 있습니다.

부문 분석

2025년 시점에서 쌍발기는 피스톤 엔진 항공기 시장의 51.15%를 차지하고 있습니다. 이것은 다발기 조종 훈련의 의무화와 전세 사업자의 중복성 확보 요구에 의한 것입니다. 파이퍼 세미놀이나 테컴 P2006T 등 확립된 모델이 같은 부문을 지원하고 있습니다. 그러나 초등 훈련과 개인 소유의 낮은 운영 비용 수요에 힘입어 단발기 변형은 견고한 6.83%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다.

세스나 172S와 실러스 SR20의 견고한 주문 잔여는 단발 기계의 경제성에 대한 신뢰를 보여줍니다. 디젤 쌍발기로의 개조도 2기의 동력원에 의한 복합적인 비용 절감 효과로부터 주목을 받고 있습니다. Leicaming IO-540 및 Continental IO-550 제품군을 전자 점화 장치로 업그레이드하면 직접 운영 비용을 더욱 줄이고 점화 신뢰성을 향상시키기 위해 고 가동률 환경에서 양발기의 매력을 유지합니다.

지역별 분석

북미는 2025년 시점에서 피스톤 엔진 항공기 시장의 39.10%를 차지했으며, 그 배경에는 미국에 5,000개가 넘는 공공이용공항의 광범위한 네트워크와 정비시설의 충실을 들 수 있습니다. 이 지역은 2020년부터 2025년에 걸쳐 4.12%라는 역사적인 CAGR을 기록해, 파일럿 부족에 의한 훈련용 기재의 확충을 배경으로, 2031년까지 5.62%로 성장이 가속할 것으로 전망됩니다. 캐나다와 멕시코에서는 실용·레크리에이션 용도 수요가 증가하고 있어 미국 연방 항공국(FAA)의 규제 개정이 신규 항공기의 인증을 촉진하고 있습니다.

아시아태평양은 성장의 견인 역할로 2031년까지 6.98%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예상됩니다. 중국이 2024년에 239개의 신규 일반항공공항을 허가함에 따라, 이 나라는 주요 구매국으로서의 지위를 확립했습니다. 인도에서는 전세 사업자 라이선싱 요건이 완화되어 진입 장벽이 저하되고, 동남아시아에서는 관광업이 회복되어 전세 수요가 재연하고 있습니다. 호주와 인도네시아에서는 농업용 살포 및 원격지 물류와 같은 특수 시장이 확대되어 견고한 피스톤 엔진 기계가 선호되고 있습니다.

유럽에서는 디젤 엔진 탑재기의 우위성과 레크리에이션 비행에 의해 꾸준한 확대가 전망됩니다. 유럽항공안전기관(EASA)의 통일규칙에 의해 국경을 넘은 원활한 운항이 가능해지고, 환경정책에 의해 유연항공연료에서 무연혼합연료로의 이행이 가속화되고 있습니다. 중동에서는 사우디아라비아의 '비전 2030' 계획에 따라 대규모 투자가 이루어지고, 아프리카에서는 남아프리카와 나이지리아에서 전세 서비스가 교통망의 공백을 채우는 등 국소적인 성장을 볼 수 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 파일럿 부족에 의한 훈련용 항공기 수요 증가

- 연료 효율 향상을 위한 피스톤 디젤 엔진 채택 확대

- 신흥 시장의 일반 항공 인프라 확충

- 부유층(HNWIs)에서의 레저 비행 열풍

- 경량 스포츠 항공기 관련 규제 완화

- 전자 점화 장치 및 FADEC의 혁신 기술에 의한 유지 보수 비용 절감

- 시장 성장 억제요인

- 유연 항공유(Avgas)에 대한 엄격한 배출 규제

- 핵심 엔진 부품의 공급망 중단 및 차질

- 일반 항공 운영사에 대한 높은 보험료 부담

- 첨단 eVTOL 및 터보프롭 항공기와의 경쟁 심화

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 엔진 유형별

- 단발 엔진

- 쌍발 엔진

- 최종 사용자 서비스별

- 민간 및 상업용

- 정부 및 군사용

- 용도별

- 스포츠

- 파일럿 훈련

- 항공 측량

- 농림업

- 에어택시 및 전세기

- 특수 임무

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 독일

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 인도네시아

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- American Champion Aircraft Corporation

- Cirrus Design Corporation(Aviation Industry Corporation of China)

- Cub Crafters, Inc.

- Diamond Aircraft Industries GmbH

- Extra Flugzeugproduktions-und Vertriebs-GmbH

- Flight Design general aviation GmbH

- Piper Aircraft, Inc.

- Costruzioni Aeronautiche TECNAM SpA

- Textron Inc.

- Mooney International Corporation

- COMPAGNIE DAHER SA

- Vulcanair SpA

- Vashon Aircraft

- ICON Aircraft, Inc.

- Glasair Aviation USA, LLC(Hanxing Group)

- Van's Aircraft, Inc.

- Sonex, LLC

- Zenith Aircraft Co.

- BRM AERO, sro

제7장 시장 기회와 장래의 전망

제8장 CEO에 대한 주요 전략적 질문

SHW 26.01.28The piston engine aircraft market was valued at USD 1.52 billion in 2025 and estimated to grow from USD 1.62 billion in 2026 to reach USD 2.22 billion by 2031, at a CAGR of 6.48% during the forecast period (2026-2031).

Escalating pilot shortages, an expanding flight-training fleet, and rising demand for economical personal and charter flying solutions anchor this growth trajectory. Flight schools favor reliable piston designs because their acquisition and operating costs are lower than those of turbine alternatives. Manufacturers sharpen competitive edges by integrating electronic ignition and Full Authority Digital Engine Control (FADEC) technology to trim maintenance expenses and improve dispatch reliability. Regulatory momentum, including the Federal Aviation Administration's (FAA's) MOSAIC rule that widens the scope of light-sport aircraft, unlocks additional demand for higher-weight, better-equipped piston models. Diesel engine retrofits and new installations enhance the appeal for cost-conscious operators, as Jet A-1 fuel is cheaper and widely available globally.

Global Piston Engine Aircraft Market Trends and Insights

Growing Demand for Training Aircraft due to Pilot Shortage

Boeing estimates that airlines and business aviation operators will need 674,000 new pilots by 2043, a gap that keeps flight training demand elevated. Prominent academies, such as Embry-Riddle, expanded their fleets in 2024 with 50 Piper Archer TX aircraft, underscoring a sustained appetite for modern piston trainers. Regional airlines in Asia-Pacific are launching ab-initio programs that demand single- and twin-engine aircraft for every pilot-licensing stage. Regulations requiring hour-building on piston types ensure a steady utilization profile. These factors establish a multi-year revenue stream for manufacturers and aftermarket providers.

Rising Adoption of Piston-diesel Engines for Fuel Efficiency

Diesel powerplants consume up to 40% less fuel than avgas engines and can burn widely available Jet A-1, easing logistics outside North America. Piper's tie-up with DeltaHawk to retrofit PA-44 Seminole trainers illustrates how OEMs court operators chasing lower direct-operating costs. Diamond's Austro-powered DA40 NG and DA42 NG models dominate European flight-school fleets, confirming market acceptance. Diesel engines also extend the time between overhauls by roughly 25%, which contributes to total lifecycle savings and improves resale values.

Stringent Emission Regulations on Leaded Avgas

The European Union (EU) and several US states are moving to phase out 100-LL avgas by 2030, compelling owners to transition toward unleaded options that remain under certification. Swift Fuels and Shell are testing 100-octane unleaded formulations, but fleet-wide approval is unlikely before 2026. Operators of older engines face retrofit costs or erosion of resale value. Uneven regional fuel availability could restrict cross-border operations during the transition period, depressing the utilization of legacy aircraft.

Other drivers and restraints analyzed in the detailed report include:

- Expanding General Aviation Infrastructure in Emerging Markets

- Recreational Flying Boom Among HNWIs

- Supply-chain Disruptions for Critical Engine Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Twin-engine aircraft held 51.15% of the piston-engine aircraft market share in 2025, thanks to mandatory multi-engine training and the redundancy needs of charter operators. The segment benefits from established models, such as the Piper Seminole and Tecnam P2006T. Nevertheless, single-engine variants post a robust 6.83% CAGR, propelled by demand for lower operating costs within primary training and personal ownership.

The strong forward-order book for the Cessna 172S and Cirrus SR20 illustrates confidence in the economics of single-engine aircraft. Diesel dual-engine retrofits also gain traction because savings compound across two power plants. Electronic-ignition upgrades for the Lycoming IO-540 and Continental IO-550 families further reduce direct operating costs and enhance ignition reliability, thereby sustaining twin appeal in higher-utilization settings.

The Piston Engine Aircraft Market Report is Segmented by Engine Type (Single Engine and Twin Engine), End-User Service (Civil/Commercial, and Government and Military), Application (Sports, Pilot Training, Aerial Surveying, Agriculture and Forestry, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 39.10% of the piston engine aircraft market share in 2025, primarily driven by the US's extensive network of over 5,000 public-use airports and well-developed maintenance facilities. The region recorded a historical 4.12% CAGR from 2020 to 2025, and momentum is expected to strengthen to 5.62% through 2031 as pilot shortages drive training fleet expansion. Canada and Mexico add incremental demand for utility and recreational roles, and FAA regulatory updates accelerate new-aircraft certifications.

The Asia-Pacific region is the growth engine, with a projected 6.98% CAGR to 2031. China's approval of 239 new general-aviation airports in 2024 positions the country as a key buyer. India's faster charter-operator licensing rules shrink barriers to entry, and Southeast Asian tourism rebounds, reviving charter demand. Australia and Indonesia add specialized markets in agricultural spraying and remote logistics, favoring rugged piston models.

Europe delivers steady expansion through diesel-power leadership and recreational flying. Harmonized EASA rules enable seamless cross-border operations, while environmental policies accelerate the shift from leaded avgas to unleaded blends. The Middle East invests heavily under Saudi Arabia's Vision 2030, and Africa shows pockets of growth in South Africa and Nigeria, where charter services fill connectivity gaps.

- American Champion Aircraft Corporation

- Cirrus Design Corporation (Aviation Industry Corporation of China)

- Cub Crafters, Inc.

- Diamond Aircraft Industries GmbH

- Extra Flugzeugproduktions- und Vertriebs- GmbH

- Flight Design general aviation GmbH

- Piper Aircraft, Inc.

- Costruzioni Aeronautiche TECNAM S.p.A.

- Textron Inc.

- Mooney International Corporation

- COMPAGNIE DAHER SA

- Vulcanair S.p.A.

- Vashon Aircraft

- ICON Aircraft, Inc.

- Glasair Aviation USA, LLC (Hanxing Group)

- Van's Aircraft, Inc.

- Sonex, LLC

- Zenith Aircraft Co.

- BRM AERO, s.r.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for training aircraft due to pilot shortage

- 4.2.2 Rising adoption of piston-diesel engines for fuel efficiency

- 4.2.3 Expanding general aviation infrastructure in emerging markets

- 4.2.4 Recreational flying boom among high-net-worth individuals (HNWIs)

- 4.2.5 Light sport aircraft regulatory relaxation

- 4.2.6 Electronic ignition and FADEC innovations reducing maintenance costs

- 4.3 Market Restraints

- 4.3.1 Stringent emission regulations on leaded Avgas

- 4.3.2 Supply chain disruptions for critical engine components

- 4.3.3 High insurance premiums for general aviation operators

- 4.3.4 Competition from advanced eVTOL and turboprop options

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Engine Type

- 5.1.1 Single Engine

- 5.1.2 Twin Engine

- 5.2 By End-User Service

- 5.2.1 Civil/Commercial

- 5.2.2 Government and Military

- 5.3 By Application

- 5.3.1 Sports

- 5.3.2 Pilot Training

- 5.3.3 Aerial Surveying

- 5.3.4 Agriculture and Forestry

- 5.3.5 Air Taxi and Charter

- 5.3.6 Special Mission

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Indonesia

- 5.4.3.6 Australia

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Qatar

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 American Champion Aircraft Corporation

- 6.4.2 Cirrus Design Corporation (Aviation Industry Corporation of China)

- 6.4.3 Cub Crafters, Inc.

- 6.4.4 Diamond Aircraft Industries GmbH

- 6.4.5 Extra Flugzeugproduktions- und Vertriebs- GmbH

- 6.4.6 Flight Design general aviation GmbH

- 6.4.7 Piper Aircraft, Inc.

- 6.4.8 Costruzioni Aeronautiche TECNAM S.p.A.

- 6.4.9 Textron Inc.

- 6.4.10 Mooney International Corporation

- 6.4.11 COMPAGNIE DAHER SA

- 6.4.12 Vulcanair S.p.A.

- 6.4.13 Vashon Aircraft

- 6.4.14 ICON Aircraft, Inc.

- 6.4.15 Glasair Aviation USA, LLC (Hanxing Group)

- 6.4.16 Van's Aircraft, Inc.

- 6.4.17 Sonex, LLC

- 6.4.18 Zenith Aircraft Co.

- 6.4.19 BRM AERO, s.r.o.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment