|

시장보고서

상품코드

1911812

인도네시아의 클라우드 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Indonesia Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

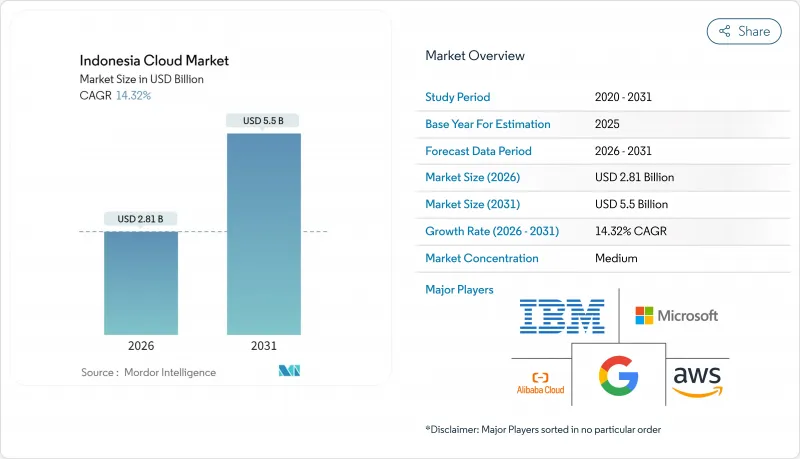

인도네시아의 클라우드 시장은 2025년 24억 6,000만 달러로 평가되었고, 2026년 28억 1,000만 달러로 성장하고, 2031년까지 55억 달러에 이를 것으로 예상됩니다. 2026년에서 2031년까지 연평균 복합 성장률(CAGR)은 14.32%를 나타낼 전망입니다.

이 확대는 지속적인 기업의 디지털 변혁에 대한 지출, 대규모 하이퍼스케일러의 설비 투자, '디지털 인도네시아 2025' 틀에 근거한 정부의 지령에 의해 추진되고 있습니다. 퍼블릭 클라우드는 자바 섬을 중심으로 한 인프라 밀도를 배경으로 주도권을 유지하고 있지만, 규제 당국이 데이터 주권에 관한 규칙을 강화함에 따라 하이브리드 아키텍처가 기세를 늘리고 있습니다. AI와 컴플라이언스 기능을 결합한 업계 특화형 클라우드 플랫폼이 공급자 간의 차별화 요인이 되고 있으며, 증가하는 ESG 목표가 재생에너지를 이용한 데이터센터 수요를 끌어 올리고 있습니다. 인재 부족과 사이버 공격 피해의 확대가 도입 속도를 억제하는 것, 프로바이더가 보안 바이 디자인이나 연수 이니셔티브를 서비스 포트폴리오에 임베디드하는 것으로, 전체적인 성장 전망은 유지되고 있습니다.

인도네시아의 클라우드 시장 동향과 인사이트력

기업의 디지털 변환에 대한 급속한 투자

대기업은 디지털 네이티브 기업과의 경쟁으로 시장 점유율을 보호하기 위해 기간 시스템의 현대화를 추진하고 있습니다. Microsoft의 17억 달러 규모의 지역 클라우드 계획과 Oracle의 65억 달러 규모의 바탐 캠퍼스 계획은 장기적인 수요를 뒷받침합니다. 멀티클라우드 배포가 가속화되는 가운데 GoTo는 알리바바 클라우드와 텐센트 클라우드와 동시 제휴하여 가격과 내결함성의 균형을 맞추고 있습니다. 텔콤 인도네시아와 레카 AI의 제휴는 기존 기업이 PaaS(Platform as a Service)를 통해 언어 인식 AI를 통합하여 고객 대응을 개선하고 있음을 보여줍니다. 지속적인 혁신 주기는 단발 전환을 넘어 지출을 증가시키고 고수익 클라우드 서비스 채택을 지속하고 있습니다. 이 움직임은 SaaS의 주도적 지위를 확고하게 하고 동시에 DevOps 대응의 PaaS 스택에 대한 수요를 환기하고 있습니다.

인도네시아 데이터센터 지역의 하이퍼스케일러 설비 투자

아마존의 50억 달러 규모의 AI 클라우드 투자 계획과 디지털 리얼티에 의한 4억 9,900만 달러의 자카르타 합작 사업은 다년간의 워크로드 성장에 대한 확신을 뒷받침하고 있습니다. 투자는 자카르타 대도시권과 바탐 섬의 저지연 회랑 주변에 집중되고, 재생가능 에너지 조달은 ESG 목표와 일치합니다. Google Cloud의 BerdAIa 프로그램은 지역 용량이 업계 특화형 AI 생태계 구축을 지원하는 예를 보여줍니다. 하이퍼스케일러 각 회사는 10년 규모의 투자 회수 기간을 받아들이고 있으며 인도네시아의 거시 경제 안정성과 규제의 명확성에 대한 확신을 보여줍니다. 현지 공동 위치 제공업체는 주요 테넌트 수요의 혜택을 받고 지방 도시에서 2차 시장의 발전을 촉진하고 있습니다.

사이버 보안 침해 비용 증가

국가 데이터센터에 대한 800만 달러의 랜섬웨어 요구는 기업의 신뢰를 뒤흔들고 위험 회피적인 섹터의 전환 지연을 초래했습니다. 새로운 아동 온라인 보호 규칙은 추가 보안 계층을 부과하고 공급자의 부담을 증가시킵니다. 금융기관은 징벌적 벌금과 평판 훼손에 직면하여 입증된 제로 트러스트 프레임워크를 가진 공급업체로 시장 이동을 촉진하고 있습니다. 엄격한 모니터링 강화로 인해 공급업체가 인증된 탄력성 프로그램을 제시할 때까지 도입이 지연된 기업에서 인도네시아의 클라우드 시장 침투가 단기적으로 억제될 수 있습니다.

부문 분석

2025년 인도네시아 클라우드 시장에서 SaaS(Software as a Service)는 44.62%를 차지했습니다. 이는 기업이 예측 가능한 운영 비용(OPEX)으로 즉시 운영할 수 있는 비즈니스 용도를 선택했기 때문입니다. PaaS(Platform as a Service)는 15.42%라는 가장 빠른 CAGR로 이어져 개발자의 마이크로서비스 및 컨테이너 오케스트레이션에 대한 수요를 반영하고 있습니다. IaaS(Infrastructure as a Service)는 이 두 가지를 모두 지원하며 소규모 SaaS 사업자가 소유하지 않고 임대하는 탄력적인 컴퓨팅 리소스를 제공합니다. 재해 복구 서비스(DRaaS)의 도입은 대규모 서비스 중단 사고 이후 급증하고 이사회 수준의 리스크 대책에 탄력성이 내장되어 있습니다.

SaaS 분야의 인도네시아 클라우드 시장 규모는 BFSI(은행, 금융 및 보험) 및 의료 분야에서 컴플라이언스 대응 솔루션이 보급됨에 따라 확대되고 있습니다. PaaS 공급업체는 Telkom DWS의 멀티미디어 CPaaS 제품군과 같은 도메인 특화형 API로 차별화를 도모하고 있습니다. 현지 제공업체인 Lintasarta는 OpenShift 기반 PaaS와 백업 저장소를 번들하여 엄격한 현지화 규정을 준수합니다. 이러한 통합 스택은 하이퍼스케일 기업의 가격 인하에 대한 마진을 보호하고 경쟁 균형을 안정화시킵니다.

2025년 현재 퍼블릭 클라우드는 즉각적인 확장성과 비용 가시성으로 인도네시아 시장 점유율의 66.05%를 차지했습니다. 한편, 하이브리드 아키텍처는 15.21%의 연평균 복합 성장률(CAGR)을 보여주며, 기업은 대기 시간에 민감한 워크로드와 규제 대상 워크로드에 대해 On-Premise/코로케이션 노드를 결합합니다. 프라이빗 클라우드는 방어 및 중요 인프라 등 엄격한 규제 환경을 위한 틈새 시장으로 존속합니다.

하이브리드 성장은 GoTo의 듀얼 프로바이더 전략과 Singtel-GMI의 국경을 넘어선 용량 공유형 GPU 풀 프로젝트에 기인합니다. Wi-Fi 6E/7의 도입으로 사이트 간 클라우드 간 처리량이 최대 46Gbps에 도달하여 분산 아키텍처를 지원합니다. 규제 당국이 국내 데이터 복사를 의무화하는 한편, 경영진이 멀티클라우드 내장해성을 요구하는 가운데 인도네시아의 하이브리드 솔루션 시장 규모는 복합적으로 확대될 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 기업에 의한 급속한 디지털 변혁 투자

- 인도네시아 데이터센터 지역의 하이퍼스케일러 설비투자(CAPEX)

- 정부의 「디지털 인도네시아 2025」구상과 전자 정부 추진

- 전자상거래 급증 / 핀테크 분야에서 클라우드 워크로드 증가

- 국가 데이터센터(PDN)에 의한 소버린 클라우드 기반 구축

- ESG 중시 기업을 중심으로 한 재생에너지 기반 '그린 클라우드' 수요 확대

- 시장 성장 억제요인

- 사이버 보안 침해 비용 급증

- 복잡한 데이터 현지화 및 산업별 컴플라이언스

- 클라우드 기술자 부족과 임금 상승

- 도서 지역 간 전력 및 광섬유 인프라 안정성 격차

- 업계 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 주요 이용 사례

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 서비스 모델별

- 소프트웨어 서비스(SaaS)

- 플랫폼 서비스(PaaS)

- 인프라 서비스(IaaS)

- 재해 복구 서비스(DRaaS)

- 전개 모델별

- 퍼블릭 클라우드

- 프라이빗 클라우드

- 하이브리드 클라우드

- 기업 규모별

- 중소기업(SME)

- 대기업

- 최종 이용 산업별

- IT 및 통신

- BFSI

- 소매 및 소비재

- 제조업

- 헬스케어 및 생명과학

- 정부 및 공공 부문

- 운송 및 물류

- 에너지 및 유틸리티

- 기타 최종 사용자 산업

- 지역별

- 자바

- 수마트라

- 칼리만탄

- 술라웨시

- 발리 및 누사?가라

- 파푸아 및 말루쿠

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Alibaba Cloud(Alibaba Group Holding Limited)

- IBM Corporation

- Tencent Cloud Computing(Beijing) Co., Ltd.

- Oracle Corporation

- Huawei Technologies Co., Ltd.

- Salesforce, Inc.

- OVH Groupe SAS

- DigitalOcean Holdings, Inc.

- Rackspace Technology, Inc.

- Linode LLC(Akamai Technologies Inc.)

- Vultr Holdings Corporation, LLC

- Hetzner Online GmbH

- PT DCI Indonesia Tbk

- PT Telekomunikasi Indonesia(Persero) Tbk

- PT Indosat Tbk(Indosat Ooredoo Hutchison)

- PT XL Axiata Tbk

- PT Biznet Gio Nusantara

- PT Indonesian Cloud

- Princeton Digital Group Pte. Ltd.

제7장 시장 기회와 장래의 전망

SHW 26.01.28The Indonesia cloud market is expected to grow from USD 2.46 billion in 2025 to USD 2.81 billion in 2026 and is forecast to reach USD 5.5 billion by 2031 at 14.32% CAGR over 2026-2031.

This expansion is propelled by sustained enterprise digital-transformation spending, large-scale hyperscaler capital expenditure, and government mandates under the Digital Indonesia 2025 framework. Public cloud retains leadership on the back of Java-centric infrastructure density, while hybrid architectures gain momentum as regulators tighten data-sovereignty rules. Sector-specific cloud platforms that combine AI and compliance functionality differentiate providers, and rising ESG targets push demand for renewable-powered data centers. Talent scarcity and escalating cyber-attack losses temper adoption velocity, but overall growth prospects remain intact as providers embed security-by-design and training initiatives into service portfolios.

Indonesia Cloud Market Trends and Insights

Rapid digital-transformation spend by enterprises

Large corporations modernize core systems to defend market share against digital-native rivals. Microsoft's USD 1.7 billion regional cloud plan and Oracle's USD 6.5 billion Batam campus validate long-term demand. Multi-cloud adoption accelerates as GoTo partners concurrently with Alibaba Cloud and Tencent Cloud to balance pricing and resilience. Telkom Indonesia's alliance with Reka AI shows traditional firms embedding language-aware AI through Platform as a Service to improve customer interactions. Continuous innovation cycles elevate spend beyond one-off migrations, sustaining uptake of higher-margin cloud offerings. This dynamic cements SaaS leadership while igniting demand for DevOps-ready PaaS stacks.

Hyperscaler CAPEX on Indonesian data-center regions

Amazon's USD 5 billion AI-cloud pledge, alongside Digital Realty's USD 499 million Jakarta JV, reinforces confidence in multiyear workload growth. Investment clusters around low-latency corridors in Greater Jakarta and Batam, with renewable power procurement aligning ESG goals. Google Cloud's BerdAIa program illustrates how regional capacity underpins ecosystem building for industry-specific AI. Hyperscalers accept decade-long payback profiles, signaling belief in Indonesia's macro stability and regulatory clarity. Local colocation providers benefit via anchor-tenant demand, catalyzing secondary market development in second-tier cities.

Escalating cybersecurity-breach costs

A USD 8 million ransomware demand on the National Data Center shook enterprise confidence, pushing risk-averse sectors to delay migrations. New child online protection rules add additional security layers, increasing provider overhead. Financial institutions face punitive fines and reputational harm, tilting the market toward vendors with proven zero-trust frameworks. Heightened scrutiny may short-term curb Indonesia's cloud market uptake among late-adopting firms until providers showcase certified resilience programs.

Other drivers and restraints analyzed in the detailed report include:

- Government Digital Indonesia 2025 and e-Gov push

- Surge in e-commerce/fintech cloud workloads

- Complex data-localization and sectoral compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software as a Service accounted for 44.62% of the Indonesian cloud market in 2025 as firms opted for ready-to-run business applications with predictable OPEX. PaaS follows with the fastest 15.42% CAGR, reflecting developer demand for micro-services and container orchestration. Infrastructure as a Service underpins both, supplying elastic compute that smaller SaaS players lease rather than own. Disaster Recovery as a Service uptake spikes after high-profile outages, embedding resiliency into board-level risk agendas.

The Indonesian cloud market size for SaaS will widen as compliance-ready solutions gain traction in BFSI and healthcare. PaaS vendors differentiate on domain-specific APIs, such as Telkom DWS's multimedia CPaaS suite. Local provider Lintasarta bundles OpenShift-based PaaS with backup vaults, meeting stringent localization rules. These integrated stacks protect margins against hyperscale price cuts, stabilizing competitive equilibrium.

Public deployments captured 66.05% Indonesia cloud market share in 2025 due to immediate scalability and cost visibility. Hybrid architectures, however, post a 15.21% CAGR as firms blend on-premise or colocation nodes for latency-sensitive or regulated workloads. Private clouds remain niche, reserved for ultra-regulated setups in defense or critical infrastructure.

Hybrid growth stems from GoTo's dual-provider play and Singtel-GMI's pooled GPU project that share capacity across borders. Rollout of Wi-Fi 6E/7 enables site-to-cloud throughput up to 46 Gbps, supporting distributed architectures. The Indonesian cloud market size for hybrid solutions is forecast to compound as regulators mandate in-country data copies while boards demand multicloud resilience.

The Indonesia Cloud Market Report is Segmented by Service Model (Software As A Service, Platform As A Service, and More), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Organization Size (Small and Medium Enterprises and Large Enterprises), and End-Use Industry (IT and Telecom, BFSI, Retail and Consumer Goods, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Alibaba Cloud (Alibaba Group Holding Limited)

- IBM Corporation

- Tencent Cloud Computing (Beijing) Co., Ltd.

- Oracle Corporation

- Huawei Technologies Co., Ltd.

- Salesforce, Inc.

- OVH Groupe SAS

- DigitalOcean Holdings, Inc.

- Rackspace Technology, Inc.

- Linode LLC (Akamai Technologies Inc.)

- Vultr Holdings Corporation, LLC

- Hetzner Online GmbH

- PT DCI Indonesia Tbk

- PT Telekomunikasi Indonesia (Persero) Tbk

- PT Indosat Tbk (Indosat Ooredoo Hutchison)

- PT XL Axiata Tbk

- PT Biznet Gio Nusantara

- PT Indonesian Cloud

- Princeton Digital Group Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid digital-transformation spend by enterprises

- 4.2.2 Hyperscaler CAPEX on Indonesian data-centre regions

- 4.2.3 Government "Digital Indonesia 2025" and e-Gov push

- 4.2.4 Surge in e-commerce / fintech cloud workloads

- 4.2.5 National Data Centre (PDN) enabling sovereign cloud

- 4.2.6 Renewable-powered 'green-cloud' demand from ESG-focused firms

- 4.3 Market Restraints

- 4.3.1 Escalating cybersecurity-breach costs

- 4.3.2 Complex data-localisation and sectoral compliance

- 4.3.3 Shortage of cloud-skilled talent and high wage inflation

- 4.3.4 Inter-island power and fibre reliability gaps

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Use Cases

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Model

- 5.1.1 Software as a Service (SaaS)

- 5.1.2 Platform as a Service (PaaS)

- 5.1.3 Infrastructure as a Service (IaaS)

- 5.1.4 Disaster-Recovery as a Service (DRaaS)

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Organisation Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-Use Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Retail and Consumer Goods

- 5.4.4 Manufacturing

- 5.4.5 Healthcare and Life Sciences

- 5.4.6 Government and Public Sector

- 5.4.7 Transportation and Logistics

- 5.4.8 Energy and Utilities

- 5.4.9 Other End-Use Industries

- 5.5 By Region

- 5.5.1 Java

- 5.5.2 Sumatra

- 5.5.3 Kalimantan

- 5.5.4 Sulawesi

- 5.5.5 Bali and Nusa Tenggara

- 5.5.6 Papua and Maluku

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC

- 6.4.4 Alibaba Cloud (Alibaba Group Holding Limited)

- 6.4.5 IBM Corporation

- 6.4.6 Tencent Cloud Computing (Beijing) Co., Ltd.

- 6.4.7 Oracle Corporation

- 6.4.8 Huawei Technologies Co., Ltd.

- 6.4.9 Salesforce, Inc.

- 6.4.10 OVH Groupe SAS

- 6.4.11 DigitalOcean Holdings, Inc.

- 6.4.12 Rackspace Technology, Inc.

- 6.4.13 Linode LLC (Akamai Technologies Inc.)

- 6.4.14 Vultr Holdings Corporation, LLC

- 6.4.15 Hetzner Online GmbH

- 6.4.16 PT DCI Indonesia Tbk

- 6.4.17 PT Telekomunikasi Indonesia (Persero) Tbk

- 6.4.18 PT Indosat Tbk (Indosat Ooredoo Hutchison)

- 6.4.19 PT XL Axiata Tbk

- 6.4.20 PT Biznet Gio Nusantara

- 6.4.21 PT Indonesian Cloud

- 6.4.22 Princeton Digital Group Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment