|

시장보고서

상품코드

1911825

인도네시아의 디지털 광고 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Indonesia Digital Advertising - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

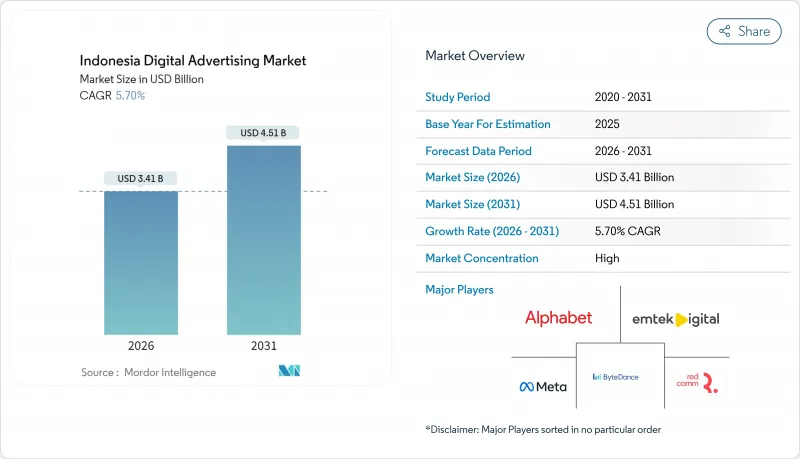

인도네시아의 디지털 광고 시장은 2025년 32억 3,000만 달러로 평가되었고, 2026년에는 34억 1,000만 달러, 2031년까지 45억 1,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년에 걸쳐 CAGR은 5.70%를 나타낼 전망입니다.

브로드밴드 대응 스마트폰의 보급 확대, 소셜 커머스와의 통합, 동영상 중심의 소비 패턴이 미디어 예산의 재정의를 계속하는 한편, 브랜드가 측정 가능한 성과를 요구하는 가운데, 퍼포먼스 중시의 모델이 기세를 늘리고 있습니다. 슈퍼앱 간 통합협상 활성화, 크리에이티브를 대규모로 현지화하는 국가 주도의 AI 투자, 데이터 프라이버시 규제의 강화가 함께 플랫폼의 경제성과 경쟁 전략을 재구성하고 있습니다. 한편, 커넥티드 TV의 확대와 라이브 커머스의 수익화에 의해 새로운 광고 인벤토리가 창출되어, 디바이스를 횡단한 인지로부터 전환으로의 제휴를 도모하는 옴니 채널 전략이 촉진되고 있습니다. 병행하여 브랜드 안전 기준을 강화하고 컨텍스트 검증 도구를 도입하면 도달범위를 손상시키지 않고 브랜드 평가가 보호됩니다.

인도네시아 디지털 광고 시장 동향과 인사이트

스마트폰 보급과 모바일 인터넷의 급성장

인도네시아에서 모바일 우선으로 전환하면 광고 예산 전환이 가속화되고 있습니다. 스마트폰 소유율은 2025년 86%에서 2028년까지 91.3%로 상승할 것으로 예측됩니다. 하루에 앱 이용 시간은 현재 5시간을 넘어, 4G 커버리지는 인구밀집지역의 96.48%를 커버하고 있어 도시 주변부에서도 신뢰성 높은 프로그래매틱 리치를 가능하게 하고 있습니다. Telkomsel, Indosat, XL Axiata를 중심으로 한 통신 사업자의 중앙 집중화는 대규모 광고 인벤토리와 확정적인 잠재고객 데이터를 제공합니다. 또한 Telkomsel의 TADEX 플랫폼은 수천 개의 게시자에 걸쳐 프리미엄 노출을 패키징합니다. 2024년에는 전년 대비 17.99% 증가하고 증가하는 모바일 트래픽으로 인도네시아의 디지털 광고 시장이 당분간 휴대기기의 화면에 계속 의존할 것이 확실합니다.

전통 미디어에서 디지털 미디어로의 예산 이동

선형 TV 시청률의 저하와 옥외 광고의 분산화에 의한 효과 감퇴를 받고, 마케터는 총 지출에서 차지하는 온라인 광고의 비율을 점차 증가시키고 있습니다. 전국적인 광고주는 2023년부터 2025년에 걸쳐 기존의 매체에서는 실현 불가능한 ROI의 명확한 증거와 상세한 타겟팅을 배경으로 예산의 7%를 아날로그에서 디지털로 전환시켰습니다. 이 전환은 자카르타 거점의 다국적 기업이 주도하고 있지만, 지역 브랜드도 퍼포먼스 마케팅 연수를 통해 모범 사례를 신속하게 도입하고 있습니다. 그 결과 인도네시아의 디지털 광고 시장은 멀티포맷 실험의 혜택을 누리고 있으며, 동적 크리에이티브 최적화와 연속 스토리텔링 캠페인이 정적 매스리치 광고를 대체하고 있습니다.

광고 사기 및 브랜드 안전에 대한 우려

선거 연도의 가짜 정보가 급증하고 소비자의 대부분이 가짜 뉴스를 심각한 문제로 인식하고 있습니다. 브랜드는 대책 강화를 위해 키워드 블록과 같은 대규모 기술이 아니라 페이지별로 컨텐츠를 분류하는 검증 파트너를 선택합니다. 노출 수준의 투명성에 대한 수요가 높아지는 반면 게시자의 품질 편차와 실시간 게재의 복잡성은 모니터링 비용을 늘리고 있습니다. 검증 기준이 성숙할 때까지 인도네시아의 디지털 광고 시장의 일부에서 공급측의 가격 압력에 직면할 수 있습니다.

부문 분석

2025년 동영상 광고는 지출의 34.02%를 차지했고 OTT 시청 시간이 월간 35억 시간을 넘어 인도네시아 디지털 광고 시장 규모의 최대 점유율을 획득했습니다. 높은 완료율과 측정 툴의 개선이 FMCG, 자동차, 통신 업계의 예산을 불러일으켰으며, 6초 범퍼 광고는 대역폭이 제한된 접속 환경에서도 사용자 경험을 보호했습니다. 한편 소셜미디어는 CAGR 6.11%로 가장 빠르게 성장할 것으로 전망됩니다. TikTok의 1억 5,760만 명의 사용자 기반과 Tokopedia와의 통합 후 구축된 마찰이 없는 상거래 결제 프로세스가 이를 뒷받침하고 있습니다. 소셜 커머스 규제 강화에도 불구하고 브랜드 컨텐츠의 명시적 표시 및 퍼스트 파티 데이터에 대한 액세스는 성능 안정성을 지원하고 점유율 확대를 지속적으로 보장합니다.

디스플레이 광고와 배너 형식은 수직 동영상 피드에 최적화된 반응형 디자인으로 진화하는 반면 검색 광고는 여행 및 금융 서비스 분야를 중심으로 고구매 의욕 전환에 필수적입니다. 오디오 광고는 주간 팟캐스트 도달률 42.6%를 배경으로 브랜드 안전한 스토리텔링 환경을 제공. 네이티브 광고 및 메일 육성 흐름은 빈도 접촉을 보완합니다. 이와 같은 시너지 효과로 인해 광고주가 소비자의 미묘한 행동 변화에 맞춘 크리에이티브를 다양화하는 가운데 인도네시아의 디지털 광고 시장은 계속 확대되고 있습니다.

2025년에는 모바일 단말이 광고 지출의 68.10%를 차지하고, SIM 보급률이 인구를 상회하고, 전자상거래 결제의 67%가 휴대 단말에서 이루어지는 인도네시아에서 스마트폰이 디지털 광고 시장 점유율을 견인하고 있음을 보여주고 있습니다. 저대역 지역을 위해 광고 소재를 압축하는 경량 SDK는 지연을 희생하지 않고 도달범위 확대를 추진합니다. 동시에 커넥티드 TV에 대한 지출은 CAGR 6.72%로 확대가 전망되고 거실의 스크린이 주소 지정 가능한 인벤토리로 변모하고 있습니다. 구독형 동영상 서비스 가입 가구가 유료 TV를 능가함으로써 동적 광고 삽입이나 가구 단위의 빈도 제한이 가능해져, 종래는 패널 조사에 의존하고 있던 브랜드 리프트 조사에 있어서 큰 진전이 되고 있습니다.

지속적인 데스크톱 캠페인은 B2B의 의도 수집 및 긴 조사 용도로 지속되며, 태블릿 기기는 교육 및 어린이 컨텐츠 분야에서 노출을 증가시킵니다. 수라바야와 메단에서 차세대 5G의 전개에 의해 버퍼링이 더욱 경감되어, QR코드와 방송 영상을 융합한 인터랙티브한 쇼핑 가능한 광고가 가능해집니다. 가정용 광섬유 커버율은 지구의 97.86%에 이르며 피크 시의 품질을 안정시킵니다. 이러한 인프라의 강화는 인도네시아의 디지털 광고 시장이 성숙함에 따라 옴니 디바이스 계획을 뒷받침합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 스마트폰의 보급과 모바일 인터넷의 급성장

- 기존 미디어에서 디지털 미디어로 예산 이동

- 전자상거래(E커머스)와 소셜커머스의 급성장

- OTT/쇼트 동영상 소비의 급증

- 정부 'Making Indonesia 4.0' 중소기업 디지털화 촉진 시책

- 라이드 셰어링 및 POS 데이터를 활용한 AI 구동형 하이퍼로컬 타겟팅

- 시장 성장 억제요인

- 광고 사기와 브랜드 세이프티에 대한 우려

- 측정 및 기여도(Attribution) 체계의 파편화

- 개인정보보호법(PDP) 준수 부담

- 지방도시에서의 광대역 환경의 불균일성

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 광고 형식별

- 디스플레이 광고 / 배너 광고

- 동영상

- 소셜 미디어

- 검색

- 오디오 / 팟캐스트

- 네이티브 광고

- 메일

- 기기별

- 모바일 단말기

- 데스크톱 / 노트북

- 커넥티드 TV

- 태블릿 및 기타

- 업계별

- FMCG(일용품)

- 통신

- 의료 및 의약품

- 미디어 및 엔터테인먼트

- 금융 서비스

- 여행 및 관광

- 전자상거래 및 마켓플레이스

- 기타 산업 분야

- 구매(과금) 방식별

- 클릭당 비용(CPC)

- 노출당 비용(CPM)

- 전환당 비용(CPA)

- 조회당 비용(CPV)

- 혼합형 / 기타 과금 모델

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- PT Google Indonesia(Alphabet Inc.)

- Meta Platforms Inc.

- ByteDance Ltd.(TikTok Indonesia)

- PT GoTo Gojek Tokopedia Tbk(GoTo Ads)

- PT Shopee Internasional Indonesia(Sea Ltd.)

- PT Telekomunikasi Indonesia Tbk(IndiHome Ads)

- PT Bukalapak.com Tbk

- PT Traveloka Digital Indonesia

- Dentsu Group Inc.(PT Dentsu Indonesia)

- WPP plc(GroupM Indonesia)

- Omnicom Group Inc.(OMD/PHD Indonesia)

- Publicis Groupe SA(Publicis Indonesia)

- Havas Group SA(Havas Indonesia)

- PT Emtek Digital

- PT ADA Asia(ADA Indonesia)

- PT RedComm Indonesia

- PT HeartMedia Digital(IDN Media)

- PT Verizon Media Indonesia(Yahoo Ads)

- PT InMobi Indonesia

- PT Revindo Jakarta(Reevo)

- PT Kantar Indonesia

- PT Comscore Indonesia

- PT MOLOCO Indonesia

- PT Samsung Ads Indonesia

제7장 시장 기회와 장래의 전망

SHW 26.01.28The Indonesia digital advertising market is expected to grow from USD 3.23 billion in 2025 to USD 3.41 billion in 2026 and is forecast to reach USD 4.51 billion by 2031 at 5.70% CAGR over 2026-2031.

Rising broadband smartphone adoption, social-commerce integration, and video-first consumption patterns continue to redefine media budgets, while performance-oriented models gain traction as brands demand measurable outcomes. Intensifying consolidation talks among super-apps, sovereign AI investments that localize creative at scale, and stricter data-privacy enforcement collectively reshape platform economics and competitive tactics. Meanwhile, connected-TV expansion and live-commerce monetization unlock fresh inventory, encouraging omnichannel strategies that link awareness to conversion across devices. In parallel, higher brand-safety standards and contextual verification tools protect reputation without eroding reach.

Indonesia Digital Advertising Market Trends and Insights

Smartphone penetration and mobile internet boom

Indonesia's mobile-first transition accelerates advertising-budget shifts as smartphone ownership is forecast to climb from 86% in 2025 to 91.3% by 2028. Daily app usage now exceeds 5 hours, and 4G coverage blankets 96.48% of populated areas, enabling reliable programmatic reach even in peri-urban zones. Operator concentration around Telkomsel, Indosat, and XL Axiata provides scaled inventory and deterministic audience data, while Telkomsel's TADEX platform packages premium impressions across thousands of publishers. Rising mobile traffic, up 17.99% YoY in 2024, ensures that the Indonesia digital advertising market remains anchored to handheld screens for the foreseeable future.

Budget shift from traditional to digital media

Marketers allocate progressively larger shares of total spend online as linear-TV ratings wane and OOH fragmentation dilutes impact. National advertisers moved 7 percentage-points of budget from analog to digital between 2023-2025, spurred by compelling ROI evidence and granular targeting unavailable on legacy channels. The shift is led by Jakarta-based multinationals, yet regional brands quickly replicate best practices through performance-marketing workshops. The Indonesia digital advertising market consequently benefits from multi-format experimentation, with dynamic creative optimization and sequential-storytelling campaigns replacing static mass-reach placements.

Ad-fraud and brand-safety concerns

Election-year misinformation surged, with most of consumers perceiving fake news as severe. Brands thus tighten controls, opting for verification partners that classify content at page level rather than blunt keyword blocks. Demand for impression-level transparency grows, yet fragmented publisher quality and livestream complexity raise monitoring costs. Until verification standards mature, pockets of the Indonesia digital advertising market may face supply-side pricing pressure.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce and social-commerce surge

- OTT / short-form video consumption spike

- Personal-Data Protection Law compliance burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Video ads represented 34.02% of spend in 2025, capturing the largest slice of the Indonesia digital advertising market size as OTT viewership soared beyond 3.5 billion monthly hours. High completion rates and improved measurement tools attracted FMCG, automotive, and telco budgets, while six-second bumper ads safeguarded user experience on constrained bandwidth connections. Social media, however, is poised for the quickest ascent at a 6.11% CAGR, buoyed by TikTok's 157.6 million users and frictionless commerce checkout journeys forged after its Tokopedia merger. Even with stricter social-commerce rules, branded-content labeling and first-party data access underpin performance consistency, ensuring continued share gains.

Display and banner formats evolve with responsive designs optimized for vertical video feeds, whereas search remains indispensable for high-intent conversions, especially within travel and financial-services categories. Audio ads benefit from a weekly podcast reach of 42.6%, providing brand-safe storytelling environments. Native integrations and email nurture flows add complementary frequency touches. Collectively, these dynamics keep the Indonesia digital advertising market expanding as advertisers diversify creative to match nuanced consumer moments.

Mobile handsets absorbed 68.10% of expenditure in 2025, underlining the Indonesia digital advertising market share leadership of smartphones in a country where SIM penetration exceeds population and 67% of e-commerce checkouts occur on handhelds. Lightweight SDKs that compress creatives for low-bandwidth regions drive incremental reach without compromising latency. Simultaneously, connected-TV spending is forecast to grow at 6.72% CAGR, turning living-room screens into addressable inventory. Subscription-video households surpass pay-TV, enabling dynamic ad insertion and household-level frequency capping, a boon for brand-lift studies that previously relied on panel-based measurement.

Desktop campaigns persist for B2B intent harvesting and long-form research journeys, while tablets furnish incremental impressions across education and children's content. Next-generation 5G rollouts across Surabaya and Medan further reduce buffering, allowing interactive shoppable ads that merge QR codes with broadcast visuals. Fiber-to-home coverage reaching 97.86% of districts cushions peak-time quality. These infrastructure upgrades reinforce omni-device planning as the Indonesia digital advertising market matures.

The Indonesia Digital Advertising Market Report is Segmented by Advertising Format (Display/Banner, Video, and More), Device (Mobile Handset, Desktop/Laptop, and More), Industry Vertical (FMCG, Telecom, Healthcare and Pharma, and More), Buying Model (Cost-Per-Click, Cost-Per-Mille, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- PT Google Indonesia (Alphabet Inc.)

- Meta Platforms Inc.

- ByteDance Ltd. (TikTok Indonesia)

- PT GoTo Gojek Tokopedia Tbk (GoTo Ads)

- PT Shopee Internasional Indonesia (Sea Ltd.)

- PT Telekomunikasi Indonesia Tbk (IndiHome Ads)

- PT Bukalapak.com Tbk

- PT Traveloka Digital Indonesia

- Dentsu Group Inc. (PT Dentsu Indonesia)

- WPP plc (GroupM Indonesia)

- Omnicom Group Inc. (OMD/PHD Indonesia)

- Publicis Groupe SA (Publicis Indonesia)

- Havas Group SA (Havas Indonesia)

- PT Emtek Digital

- PT ADA Asia (ADA Indonesia)

- PT RedComm Indonesia

- PT HeartMedia Digital (IDN Media)

- PT Verizon Media Indonesia (Yahoo Ads)

- PT InMobi Indonesia

- PT Revindo Jakarta (Reevo)

- PT Kantar Indonesia

- PT Comscore Indonesia

- PT MOLOCO Indonesia

- PT Samsung Ads Indonesia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smartphone penetration and mobile internet boom

- 4.2.2 Budget shift from traditional to digital media

- 4.2.3 E-commerce and social-commerce surge

- 4.2.4 OTT / short-form video consumption spike

- 4.2.5 Govt "Making Indonesia 4.0" SME digitization incentives

- 4.2.6 AI-driven hyper-local targeting via ride-hailing and POS data

- 4.3 Market Restraints

- 4.3.1 Ad-fraud and brand-safety concerns

- 4.3.2 Measurement and attribution fragmentation

- 4.3.3 Personal-Data Protection Law (PDP) compliance burden

- 4.3.4 Uneven broadband outside tier-1 cities

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Advertising Format

- 5.1.1 Display/Banner

- 5.1.2 Video

- 5.1.3 Social Media

- 5.1.4 Search

- 5.1.5 Audio/Podcast

- 5.1.6 Native

- 5.1.7 Email

- 5.2 By Device

- 5.2.1 Mobile Handset

- 5.2.2 Desktop / Laptop

- 5.2.3 Connected TV

- 5.2.4 Tablet and Others

- 5.3 By Industry Vertical

- 5.3.1 FMCG

- 5.3.2 Telecom

- 5.3.3 Healthcare and Pharma

- 5.3.4 Media and Entertainment

- 5.3.5 Financial Services

- 5.3.6 Travel and Tourism

- 5.3.7 E-commerce and Marketplaces

- 5.3.8 Others Industry Verticals

- 5.4 By Buying Model

- 5.4.1 Cost-Per-Click (CPC)

- 5.4.2 Cost-Per-Mille (CPM)

- 5.4.3 Cost-Per-Acquisition (CPA)

- 5.4.4 Cost-Per-View (CPV)

- 5.4.5 Hybrid / Other Buying Models

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 PT Google Indonesia (Alphabet Inc.)

- 6.4.2 Meta Platforms Inc.

- 6.4.3 ByteDance Ltd. (TikTok Indonesia)

- 6.4.4 PT GoTo Gojek Tokopedia Tbk (GoTo Ads)

- 6.4.5 PT Shopee Internasional Indonesia (Sea Ltd.)

- 6.4.6 PT Telekomunikasi Indonesia Tbk (IndiHome Ads)

- 6.4.7 PT Bukalapak.com Tbk

- 6.4.8 PT Traveloka Digital Indonesia

- 6.4.9 Dentsu Group Inc. (PT Dentsu Indonesia)

- 6.4.10 WPP plc (GroupM Indonesia)

- 6.4.11 Omnicom Group Inc. (OMD/PHD Indonesia)

- 6.4.12 Publicis Groupe SA (Publicis Indonesia)

- 6.4.13 Havas Group SA (Havas Indonesia)

- 6.4.14 PT Emtek Digital

- 6.4.15 PT ADA Asia (ADA Indonesia)

- 6.4.16 PT RedComm Indonesia

- 6.4.17 PT HeartMedia Digital (IDN Media)

- 6.4.18 PT Verizon Media Indonesia (Yahoo Ads)

- 6.4.19 PT InMobi Indonesia

- 6.4.20 PT Revindo Jakarta (Reevo)

- 6.4.21 PT Kantar Indonesia

- 6.4.22 PT Comscore Indonesia

- 6.4.23 PT MOLOCO Indonesia

- 6.4.24 PT Samsung Ads Indonesia

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment