|

시장보고서

상품코드

1911829

인도의 가구 하드웨어 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)India Furniture Hardware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

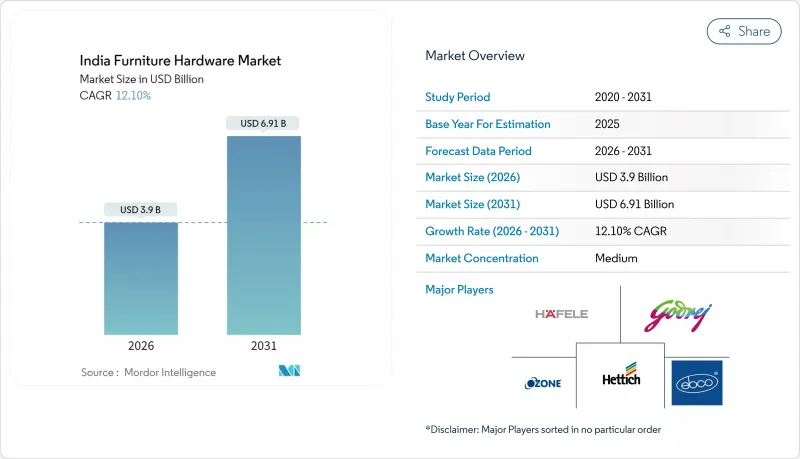

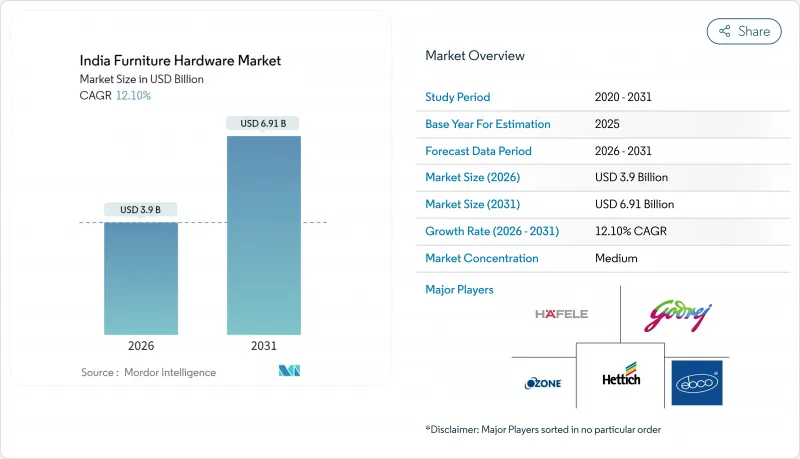

인도의 가구 하드웨어 시장 규모는 2026년 39억 달러로 추정되고, 2025년 34억 8,000만 달러에서 성장이 예상됩니다.

2031년까지 69억 1,000만 달러에 달할 것으로 예측되며, 2026-2031년 CAGR 12.1%로 확대될 전망입니다.

수요의 기세는 급속한 도시 주택 건설, 확대하는 조직 소매점포망, 디지털 채널의 보급에 지지되고 있어 인도의 가구 하드웨어 시장을 2자리 성장 궤도에 유지하고 있습니다. 가처분 소득 증가로 고급 브래킷 및 소프트 클로즈 시스템이 촉진되는 반면, 정부의 품질 기준은 인증 제품에 대한 구매를 유도하고 있습니다. 세계의 브랜드는 디자인 차별화로 점유율을 지키고 민첩한 지역 기업은 가격 경쟁으로 대항하고 분산된 경쟁 환경이 지속되고 있습니다. 단기 성장 요인으로는 견조한 주택 건설 파이프라인, 확대되는 상업 시설 내장 시장, 소비자 및 소규모 계약자의 구매 행동을 온라인화로 이끄는 인터넷 보급 등이 있습니다.

인도의 가구 하드웨어 시장 동향 및 인사이트

급속한 주택 건설 및 도시화

인도에서는 지난 10년간 약 1억호의 주택 증가가 요구되고 있으며, 뭄바이, 푸네, 첸나이 등의 대도시권이 그 수요의 대부분을 차지해, 힌지, 레일, 건축용 쇠장식 수요를 직접 밀어올리고 있습니다. 노후화된 주택 스톡의 현대화로 인해 레거시 힌지에서 부드러운 폐쇄식 및 내식성 힌지로의 교체 수요가 더욱 증가하고 있습니다. 해안 지역 개발자들은 습기에 견디는 스테인레스 스틸 등급을 지정하는 경향이 강해져 평균 판매 가격을 밀어 올리고 있습니다. 산업 거점 주변, 특히 마하라슈트라의 제조 지역에 집중하는 건설 프로젝트는 이웃 공급자에게 유리한 지역 수요 창출을 가져옵니다. 새로운 프로젝트와 교환 수요가 함께 인도의 가구 하드웨어 시장은 지리적으로 분산된 견조한 기반을 구축하고 있습니다.

모듈식 RTA 가구에서 전자상거래 가속화

조립식 옷장과 주방 모듈은 현재 나사, 캠, 레일 등의 부품이 포함된 플랫 팩으로 배송됩니다. 이러한 부품은 엄격한 공차를 충족해야 합니다. 온라인 구매자는 스스로 브래킷을 설치하기 때문에 각 브랜드는 직관적인 디자인, QR 코드가 있는 비디오 가이드, 완전한 체결 부품 키트에 중점을 둡니다. 주요 마켓플레이스의 신속한 제품 사이클로 인해 하드웨어 공급업체는 가구 제조업체의 업데이트 일정에 맞추어 SKU를 동기화해야 하며, 밸류체인 전반에 걸친 협력이 깊어지고 있습니다. 고객 리뷰 데이터에 따르면 힌지 결함이 반품 원인의 선두를 차지하고 있으며 품질 일관성이 중요한 차별화 요인이 되고 있습니다. 디지털 채널로 기록된 14.36%의 연평균 복합 성장률(CAGR)은 표준화 하드웨어의 매출 증가에 직결되는 동시에 인도의 가구 하드웨어 시장에 가격 투명성을 가져오고 있습니다.

비 조직 분야에 의한 가격 압력 및 물류 문제

대형 코트와 모라다바드에 집적된 수천 개의 소규모 공방은 인증 비용을 피하고 현지 목수에 직접 판매함으로써 브랜드 제조업체를 최대 30% 미만으로 가격을 실현하고 있습니다. 인기 SKU를 신속하게 모방하는 그들의 기동력은 인도의 가구 하드웨어 시장에서 엔트리 라인의 이익률을 압박하고 있습니다. 부피가 큰 금속 슬라이드 레일과 바구니는 중량 대 가치 비율이 불리하고 원격지로 운송할 때 운임 비용을 증가시킵니다. 북동부의 교통망 부족은 리드타임을 연장하고 유통업체에게 안전 재고의 증대를 강하게 하므로 운전 자금이 증가합니다. BIS(인도규격협회)의 규제는 기준 미달품의 배제를 목적으로 하고 있지만, 주요 항만 이외에서의 시행이 불충분하기 때문에 가격 경쟁이 계속되는 상황이 생기고 있습니다.

부문 분석

리프트 시스템은 2025년에 소량의 수익만 올릴 수 있었지만, 도시 부엌에서 공간 효율화를 위해 오픈 캐비닛이 요구되기 때문에 카테고리 중 가장 빠른 12.62%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다. 힌지는 인도의 가구 하드웨어 시장 점유율의 26.88%를 차지하는 주력 제품이었지만, 가치의 이행에 의해 가격 프리미엄이 붙는 숨겨진 식이나 소프트 클로즈 사양의 바리에이션이 선호되고 있습니다. 러너 시스템은 조용함과 풀 익스텐션 기능을 갖춘 서랍이 필요한 모듈 식 주방에서 계속 수요를 확대하고 있습니다. 핸들, 풀, 노브는 디자인 주도 수요에 힘입어 인테리어 테마에 조화를 이루는 컬러 매칭 컬렉션이 지지되고 있습니다. 패스너는 최대 볼륨의 SKU이지만, 비조직적인 기업에 의한 이익률의 저하에 직면하고 있습니다. 하지만 BIS 표준은 품질 중심의 구매층을 브랜드 제품으로 향하게 할 수 있습니다. 미닫이 문 시스템과 와이어 바스켓과 같은 전문적인 하위 카테고리는 기능성 옵션을 넓혀 인도의 가구 하드웨어 시장 전체에서 경쟁력으로 제품 폭 강화에 기여하고 있습니다.

2차 영향은 제품 분야를 가로지르는 경쟁 투자를 형성합니다. 리프트 어시스트 댐퍼 및 서보 구동 오프너는 정밀한 가스 스프링 조정이 필요하며 현지 공장에서 자동화를 촉진하고 있습니다. 숨겨진 힌지에는 마이크론 단위의 프레스 금형이 요구되고 소규모 공장에서는 유지가 곤란하기 때문에 조직화된 생산자 및 비조직적인 생산자의 능력 격차가 확대되고 있습니다. 럭셔리 박스 시스템의 성장은 옷장의 모듈화된 진전과 연동하며, 공급업체는 레일 브래킷 핸들을 통합 키트로 제공합니다. 바닥에서 천장까지의 유리 패널용 슬라이드 기구는 최소한의 프레임 두께가 중시되는 고급 주택 및 오피스 내장 시장을 개척합니다. 이러한 동향과 맞물려, 수익 구성은 엔지니어링 기구로 이행해 인도 가구 하드웨어 시장의 가치 기반을 확대하고 있습니다.

강재는 내구성과 저단가를 배경으로 2025년 시점에서 인도의 가구 하드웨어 시장 규모의 41.88%를 차지했습니다. 아연 합금은 내식성으로부터 해안부나 고습도 지역에서 채용되고, 알루미늄은 경량성을 살려 리프트 시스템 등의 고급 용도에 활용되고 있습니다. 한편, 플라스틱 및 기타 폴리머 계 금구는 제조업체가 사출 성형의 유연성을 활용하여 복잡한 형상의 창출과 감쇠 기능의 통합을 실현한 결과, 12.33%라는 가장 빠른 CAGR을 기록하고 있습니다. 황동은 푸른 푸른 미학이 높은 가격대를 정당화하는 고급 호텔 업계에서 틈새 장식 용도를 담당하고 있습니다.

현재는 재료 선정에 재활용성이 내장되어 있어 도시의 소비자는 구입 전에 환경 성능을 확인합니다. 고급 유리 섬유 강화 나일론 등급은 금속에 필적하는 강도를 경량으로 실현하여 EC 배송의 운송 비용을 절감합니다. 사출 성형에 대한 투자는 단위 사이클 시간도 단축하여 온라인 플래시 세일 급증에 대응하는 신속한 증산을 가능하게 합니다. 한편, SS-304와 SS-316과 같은 고급 스테인레스 스틸은 청소의 용이성과 긴 수명을 중시하는 고급 주방 시장에서 점유율을 확대하고 있습니다. 첨단 플라스틱과 스테인리스 합금의 동시 상승은 인도의 가구 하드웨어 시장에서 경량화에 의한 경제성과 하이 엔드 성능의 양방향으로의 분기를 나타내고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 서포트(3개월간)

자주 묻는 질문

목차

제1장 목차 : 인도 가구 하드웨어 시장

제2장 서문

- 조사의 전제조건 및 시장 정의

- 조사 범위

제3장 조사 방법

제4장 주요 요약

제5장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 주택 부동산의 급속한 성장 및 도시화

- 온라인으로 구입되는 모듈러 및 RTA 가구의 급증

- 프리미엄화 및 고품질 철물에 대한 디자인 주도 수요

- 조직화된 소매업 및 DIY 채널 확대

- BIS 품질 관리 지령에 의한 성능 기준의 향상

- 장애인(PwD)을 위한 접근성 기준이 인체공학에 근거한 하드웨어 추진

- 시장 성장 억제요인

- 분산된 비조직적 분야와 격렬한 경쟁

- 변동하는 철강, 아연 및 폴리머 비용

- 대형 및 중량 부품에 있어서 물류의 비효율성

- 새로운 지속가능성 및 접근성 기준에 대한 대응 비용

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 시장의 최신 동향 및 혁신에 관한 인사이트

- 시장의 최근 동향(신제품 발매, 전략적 이니셔티브, 투자, 제휴, 합작 사업, 사업 확대, M&A 등)에 관한 인사이트

- 하드웨어 산업에 있어서 규제 프레임워크 및 업계 기준에 관한 인사이트

제6장 시장 규모 및 성장 예측(금액 기준, 2020-2030년)

- 제품 유형별

- 힌지

- 러너 시스템

- 리프트 시스템

- 박스 시스템

- 와이어 바구니

- 미닫이 문 시스템

- 손잡이, 당김, 노브

- 패스너(나사, 볼트, 너트 등)

- 기타

- 재료별

- 강철

- 아연 합금

- 알루미늄

- 플라스틱 및 폴리머 기반

- 황동 및 기타 금속

- 최종 사용자별

- 주택용 가구

- 오피스 가구

- 호스피탈리티 및 소매 집기

- 유틸리티(의료, 교육)

- 유통 채널별

- 오프라인 : 딜러 및 소매점

- 온라인 : 전자상거래 및 브랜드 D2C

- 지역별(인도)

- 북인도

- 서인도

- 남 인도

- 동인도 및 동북인도

제7장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Hettich India Pvt. Ltd.

- Hafele India Pvt. Ltd.

- Godrej Locks & Architectural Fittings & Systems

- Ebco Pvt. Ltd.

- Ozone Overseas Pvt. Ltd.

- Dorset Industries Pvt. Ltd.

- Blum India

- Sugatsune Kogyo India

- H Hafele(Hafele brand stores)

- Hettich PODs & Studio Partners

- Kich Architectural Products

- PEGO Hardware

- Quba Group

- Vinay Wire & Polyproduct Pvt. Ltd.

- Dorset Smart Locks

- Ozone Securitas

- Evershine Appliances(Oliveworld)

- Italik Metalware Pvt. Ltd.

- DP Garg & Company(Garg Hinges)

- SIFON Hardware

제8장 시장 기회 및 장래 전망

- 조직화된 소매업의 확대가 브랜드 하드웨어 뒷받침

- 스마트 기구가 변혁하는 모듈 가구 시스템

India furniture hardware market size in 2026 is estimated at USD 3.90 billion, growing from 2025 value of USD 3.48 billion with 2031 projections showing USD 6.91 billion, growing at 12.1% CAGR over 2026-2031.

Demand momentum is anchored in rapid urban housing creation, swelling organized retail footprints, and digital channel adoption that keep the India furniture hardware market on a double-digit growth curve. Rising disposable incomes promote premium fittings and soft-close systems, while government quality mandates steer buyers toward certified products. Global brands safeguard share with design differentiation, whereas nimble regional firms battle on price, sustaining a fragmented competitive field. Near-term upside stems from a strong residential pipeline, expanding commercial interiors, and online penetration that moves both consumer and small-contractor purchases to click-based journeys.

India Furniture Hardware Market Trends and Insights

Rapid residential build-out and urbanization

India must add roughly 100 million homes this decade, and metros such as Mumbai, Pune and Chennai account for a large share of that pipeline, directly lifting demand for hinges, runners and architectural fittings. Modernization of aging housing stock further multiplies retrofit volumes as owners swap legacy hinges for soft-close or corrosion-resistant versions. Developers in coastal belts increasingly specify stainless-steel grades to withstand humidity, nudging average selling prices higher. Construction clusters around industrial nodes, especially Maharashtra's manufacturing belts, create localized demand pockets that favor nearby suppliers. Together, greenfield projects and replacements underpin a robust, geographically diversified base for the India furniture hardware market.

E-commerce acceleration in modular and RTA furniture

Ready-to-assemble wardrobes and kitchen modules now ship in flat-packs bundled with screws, cams and runners that must meet tight tolerances. Online buyers install fittings themselves, so brands emphasize intuitive designs, QR-code video guides and complete fastener kits. Rapid product cycles on leading marketplaces force hardware suppliers to synchronize SKUs with furniture makers' refresh calendars, deepening collaboration along the value chain. Customer-review data reveal hinge failures as a leading cause of returns, making quality consistency a vital differentiator. The 14.36% CAGR logged by digital channels thus converts directly into incremental standardized-hardware sales while injecting pricing transparency into the India furniture hardware market.

Price pressure from the unorganized sector plus logistics hurdles

Thousands of small workshops clustered in Rajkot and Moradabad undercut branded players by up to 30% because they sidestep certification costs and sell direct to local carpenters. Their agility in copying popular SKUs squeezes margins on entry-level lines within the India furniture hardware market. Bulky metal slides and baskets suffer unfavorable weight-to-value ratios, inflating freight costs when shipped to distant regions. Poor connectivity in the North-East lengthens lead times and forces distributors to hold larger safety stocks, raising working capital. Although BIS mandates aim to weed out sub-par goods, patchy enforcement outside major ports allows price-led competition to persist.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization, design focus and regulatory quality cues

- Rise of organized retail, DIY and accessibility needs

- Raw-material and compliance cost volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lift systems captured only modest revenue in 2025 but are forecast to grow at a 12.62% CAGR, the quickest pace among categories, as urban kitchens seek overhead cabinets that open upwards for space efficiency. Hinges remained the workhorse with 26.88% of the India furniture hardware market share, yet value migration favors concealed and soft-close variants that attract price premiums. Runner systems continue to gain traction in modular kitchens whose drawers require silent, full-extension slides. Handles, pulls and knobs benefit from design-led demand, supporting color-matched collections that complement interior themes. Fasteners are the highest-volume SKU yet face margin erosion from unorganized players; still, BIS standards could lift quality-conscious buyers toward branded options. Specialized sub-categories such as sliding-door systems and wire baskets broaden functionality choices, reinforcing product breadth as a competitive lever across the India furniture hardware market.

Second-order effects shape competitive investments across product verticals. Lift-assist dampers and servo-driven openers rely on precise gas-spring calibration, encouraging automation in local factories. Concealed hinges require micron-level stamping dies that smaller shops struggle to maintain, widening the capability gap between organized and informal producers. Growth in premium box systems aligns with rising wardrobe modularization, prompting suppliers to bundle runners, brackets and handles as integrated kits. Sliding mechanisms designed for floor-to-ceiling glass panels tap into premium residential and office interiors, where minimal frame thickness is prized. Together these trends shift revenue mix toward engineered mechanisms, expanding the value pool of the India furniture hardware market.

Steel delivered 41.88% of the India furniture hardware market size in 2025 thanks to its durability and low unit cost. Zinc alloy follows in coastal and high-humidity zones for its corrosion resistance, while aluminum's light weight attracts premium applications such as lift systems. Plastic and other polymer-based fittings, however, clock the fastest 12.33% CAGR as makers exploit injection-mold flexibility to create complex geometries and integrate damping functions. Brass serves niche decor roles in luxury hospitality where patina aesthetics justify higher price points.

Material selection now incorporates recyclability, with urban consumers querying environmental credentials before purchase. Advanced glass-fiber-reinforced nylon grades rival metal strength at lower weights, slashing freight costs for e-commerce shipments. Injection-molding investments also reduce per-unit cycle time, allowing rapid ramp-up to serve flash sale spikes online. Conversely, high-grade stainless variants such as SS-304 and SS-316 earn share in premium kitchens where ease of cleaning and long life matter. The simultaneous rise of advanced plastics and stainless alloys signals bifurcation toward both lightweight economy and high-end performance within the India furniture hardware market.

The India Furniture Hardware Market Report is Segmented by Product Type (Hinges, Runner Systems, Lift Systems, Box Systems, Wire Baskets, and More), Material (Steel, Zinc Alloy, Aluminium, and More), End-User (Residential, Office, Hospitality & Retail, Institutional), Distribution Channel (Offline, Online), and Geography (North, West, South, and More). Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Hettich India Pvt. Ltd.

- Hafele India Pvt. Ltd.

- Godrej Locks & Architectural Fittings & Systems

- Ebco Pvt. Ltd.

- Ozone Overseas Pvt. Ltd.

- Dorset Industries Pvt. Ltd.

- Blum India

- Sugatsune Kogyo India

- H Hafele (Hafele brand stores)

- Hettich PODs & Studio Partners

- Kich Architectural Products

- PEGO Hardware

- Quba Group

- Vinay Wire & Polyproduct Pvt. Ltd.

- Dorset Smart Locks

- Ozone Securitas

- Evershine Appliances (Oliveworld)

- Italik Metalware Pvt. Ltd.

- DP Garg & Company (Garg Hinges)

- SIFON Hardware

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Table of Contents - India Furniture Hardware Market

2 Introduction

- 2.1 Study Assumptions & Market Definition

- 2.2 Scope of the Study

3 Research Methodology

4 Executive Summary

5 Market Landscape

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Rapid growth in residential real-estate & urbanisation

- 5.2.2 Surge in modular/RTA furniture bought online

- 5.2.3 Premiumisation & design-driven demand for high-quality fittings

- 5.2.4 Expanding organised retail & DIY channels

- 5.2.5 BIS quality-control orders upgrading performance standards

- 5.2.6 Accessibility standards for PwD driving ergonomic hardware

- 5.3 Market Restraints

- 5.3.1 Fragmented unorganised sector & intense price competition

- 5.3.2 Volatile steel/zinc/polymer costs

- 5.3.3 Logistics inefficiencies for bulky, weighty fittings

- 5.3.4 Compliance costs for new sustainability & accessibility norms

- 5.4 Industry Value Chain Analysis

- 5.5 Porter's Five Forces Analysis

- 5.5.1 Threat of New Entrants

- 5.5.2 Bargaining Power of Suppliers

- 5.5.3 Bargaining Power of Buyers

- 5.5.4 Threat of Substitutes

- 5.5.5 Competitive Rivalry

- 5.6 Insights into the Latest Trends and Innovations in the Market

- 5.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

- 5.8 Insights on Regulatory Framework and Industry Standards for the Hardware Industry

6 Market Size & Growth Forecasts (Value, 2020-2030)

- 6.1 By Product Type

- 6.1.1 Hinges

- 6.1.2 Runner Systems

- 6.1.3 Lift Systems

- 6.1.4 Box Systems

- 6.1.5 Wire Baskets

- 6.1.6 Sliding Door Systems

- 6.1.7 Handles, Pulls, and Knobs

- 6.1.8 Fasteners (Screw, Bolts, Nuts, etc.)

- 6.1.9 Others

- 6.2 By Material

- 6.2.1 Steel

- 6.2.2 Zinc Alloy

- 6.2.3 Aluminium

- 6.2.4 Plastic & Polymer-based

- 6.2.5 Brass & Other Metals

- 6.3 By End-user

- 6.3.1 Residential Furniture

- 6.3.2 Office Furniture

- 6.3.3 Hospitality & Retail Fixtures

- 6.3.4 Institutional (Healthcare, Education)

- 6.4 By Distribution Channel

- 6.4.1 Offline - Dealer & Retail

- 6.4.2 Online - E-commerce & Brand D2C

- 6.5 By Region (India)

- 6.5.1 North India

- 6.5.2 West India

- 6.5.3 South India

- 6.5.4 East & North-East India

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.4.1 Hettich India Pvt. Ltd.

- 7.4.2 Hafele India Pvt. Ltd.

- 7.4.3 Godrej Locks & Architectural Fittings & Systems

- 7.4.4 Ebco Pvt. Ltd.

- 7.4.5 Ozone Overseas Pvt. Ltd.

- 7.4.6 Dorset Industries Pvt. Ltd.

- 7.4.7 Blum India

- 7.4.8 Sugatsune Kogyo India

- 7.4.9 H Hafele (Hafele brand stores)

- 7.4.10 Hettich PODs & Studio Partners

- 7.4.11 Kich Architectural Products

- 7.4.12 PEGO Hardware

- 7.4.13 Quba Group

- 7.4.14 Vinay Wire & Polyproduct Pvt. Ltd.

- 7.4.15 Dorset Smart Locks

- 7.4.16 Ozone Securitas

- 7.4.17 Evershine Appliances (Oliveworld)

- 7.4.18 Italik Metalware Pvt. Ltd.

- 7.4.19 DP Garg & Company (Garg Hinges)

- 7.4.20 SIFON Hardware

8 Market Opportunities & Future Outlook

- 8.1 Organized Retail Expansion Boosting Branded Hardware

- 8.2 Smart Mechanisms Transforming Modular Furniture Systems