|

시장보고서

상품코드

1911830

유럽의 의약품 플라스틱 포장 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Europe Pharmaceutical Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

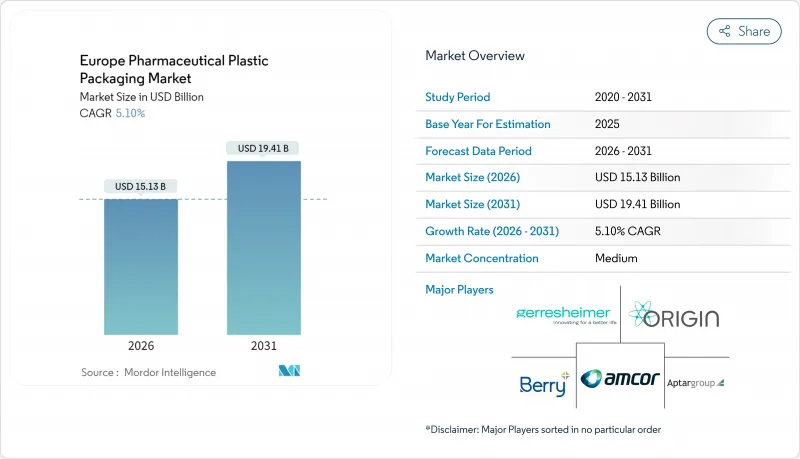

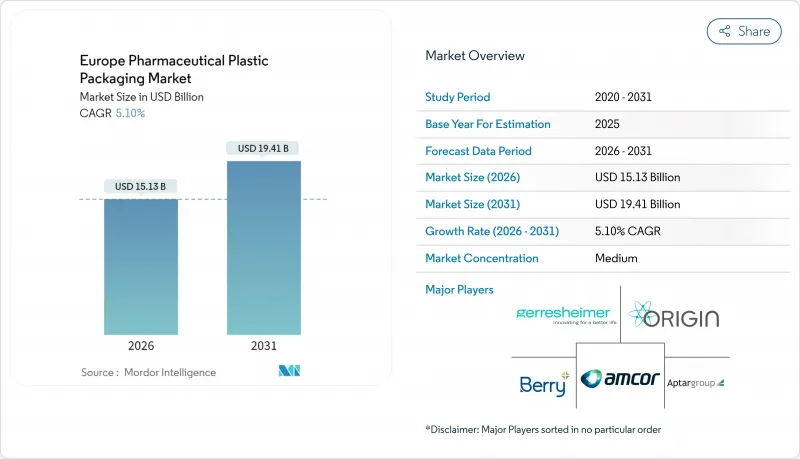

유럽의 의약품 플라스틱 포장 시장은 2025년 144억 달러로 평가되었고, 2026년 151억 3,000만 달러에서 2031년까지 194억 1,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년) CAGR은 5.10%로 성장이 예상됩니다.

성장의 열쇠는 지속가능성에 대한 요구, 바이오의약품의 보급, 재택 치료 확대에 있으며, 이들은 각각 장벽 특성, 재활용성, 사용자 중심 설계에 대한 성능 요건을 엄격화하고 있습니다. 주요 공급업체는 순환형 경제 목표 및 병원 자동화 프로그램을 충족하기 위해 재생재 사용 라인과 RFID 대응 형식의 확충을 추진하고 있습니다. 한편, 수지 비용의 변동 및 추출물 규제의 강화에 의해 이익률이 압박되고 있어 규모의 우위성을 유지하기 위해서 원재료의 헤징, 공급자의 다양화, 선택적인 합병이 진행되고 있습니다. 기존 기업이 수직 통합을 확대하는 한편, 전문 기업이 스마트 솔루션이나 바이오 솔루션의 틈새 시장을 획득하고 있기 때문에 경쟁의 격렬함은 적당합니다. 이로 인해 유럽의 의약품 플라스틱 포장 시장 전체에서 가격 설정과 협력 모델이 재구성되었습니다.

유럽의 의약품 플라스틱 포장 시장 동향 및 인사이트

어린이용 안전 캡 및 노인용 패키지 수요 증가

고령화와 소아 안전 규제의 강화로 포장 투자는 촉각적인 조작성과 인증된 어린이 저항을 겸비한 캡으로 이행하고 있습니다. 유럽의 컨버터 각사는 새로운 인체공학적 캡 플랫폼마다 200만-400만 유로를 투자하고 있어 이 대처에 의해 2024년에는 환자 중심 시스템의 도입이 18% 증가했습니다. 네메라사의 토크 저감식 캡은 ISO 8317 규격을 웃도는 성능을 유지하면서 개봉력을 30% 저감해, 사용의 용이성 및 안전성의 양립을 실증하고 있습니다. 유럽 의약품청(EMA)이 2024년에 발표한 만성 질환 치료제용 사용자 친화적인 포장을 추천하는 가이드라인에 의해 규제면에서의 뒷받침도 얻을 수 있었습니다. 조기 도입 기업에서는 특히 복잡한 락 기구를 지지하는 금형 정밀도가 요구되는 폴리프로필렌제 캡에 있어서, 초기 비용이 15-20% 상승하는 것, 프리미엄 가격 설정 및 브랜드 충성도의 향상에 의해 상쇄되고 있다고 하는 보고가 전해지고 있습니다.

고급 비경구 플라스틱이 필요한 생물학적 제형 급증

유럽에서 생물학적 제제의 생산량은 2024년에 23% 증가했으며, 독일과 스위스 공장에서는 단일클론항체의 생산이 확대되고 있습니다. 이러한 고가치 분자는 초저추출물성과 유리 미사용의 내파손성을 요구하기 때문에 폴리프로필렌의 3-4배 비용이면서 화학적 불활성성 및 투명성을 제공하는 환상 올레핀 공중합체 및 환상 올레핀 중합체 수요가 가속화되고 있습니다. 쇼트 파마의 1억 5,000만 유로 규모의 바이알 증산 계획은 특수 폴리머 제조 능력에 대한 공급업체의 노력을 뒷받침하고 있습니다. 바이오 의약품 대응 포장재의 성장률은 유럽의 의약품 플라스틱 포장 시장 전체의 거의 2배에 달하고, 재료 구성, 인증 스케줄, 공급업체 통합의 패턴을 재구축하고 있습니다.

변동하는 PP 및 PET 수지 가격

석유화학 원료 공급 장애 및 에너지 가격의 변동으로 2024년 폴리프로필렌과 PET는 15-20% 상승했습니다. BASF와 같은 생산자는 분기별 가격 제시로 전환하고 변동 위험을 컨버터 측으로 전가하고 있습니다. 컨버터는 제약기업과 다년간 공급계약을 맺는 경우가 많기 때문입니다. 헤지 능력이 부족한 중소기업은 압박에 직면하여 통합 파도를 일으키고 있습니다. 한편 주요 그룹은 공급원의 다양화 및 자사 재활용 투자로 가격 변동의 영향을 완화하고 있습니다. 많은 중견 컨버터에서는 원재료비의 30-40%가 분기별 조정 조항의 대상이 되고 있어 유럽의 의약품 플라스틱 포장 시장 전체의 예측 가능성이 손상되고 있습니다.

부문 분석

폴리프로필렌은 2025년에도 유럽의 의약품 플라스틱 포장 시장에서 비용 효율성, 내약품성, 규제 측면에서 광범위한 인지도를 바탕으로 35.20%의 점유율을 유지했습니다. 의약품용 PP의 연간 소비량은 18만 톤을 넘어, 캡, 물집 포장, 주사기 등을 커버하고 있습니다. 그러나 유럽 의약품 플라스틱 포장 시장 규모는 고밀도 폴리에틸렌(HDPE)으로 전환하고 있으며 5.74%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. HDPE는 뛰어난 방습 및 방산소 배리어성에 의해 생물학적 제제의 안정성 요건을 충족하는 동시에, PPWR(플라스틱 리사이클 규제) 하에서 보다 높은 리사이클 가능성을 제시하고 있기 때문입니다.

지속가능성으로의 전환은 의료용 등급 재생 PET(rPET)에 대한 수요를 증가시키고 바이오 등급의 시험 도입을 촉진합니다. 겔레스하이머는 의약품 순도 기준을 충족하는 재생 PET제 점적 병의 상업 생산을 시작했습니다. 틈새 폴리머(COC, COP, PLA 블렌드)는 300-400%의 프리미엄 가격이면서 초저 추출물이 필수인 비경구 제제 분야에서 채용이 진행되고 있습니다. 쇼트 파마의 COC 생산 확대는 이러한 특수 수지 수요 증가를 뒷받침하고 있습니다. 폴리프로필렌 공급업체는 사용한 플라스틱 원료의 흐름을 시험적으로 도입함으로써 대응하고 있지만, 유럽의 의약품 플라스틱 포장 시장에서 주도적 지위를 유지하기 위해서는 냄새, 색조, 추적성에 관한 기술적 과제를 극복할 필요가 있습니다.

유럽의 의약품 플라스틱 포장 시장은 원재료별(폴리프로필렌, 폴리에틸렌테레프탈레이트, 저밀도 폴리에틸렌, 고밀도 폴리에틸렌 등), 제품 유형별(고형 용기, 액체 및 점적용 병, 점비약 병, 구강 케어팩, 파우치 및 사쉐, 바이알 및 앰풀 등) 및 국가별로 구분되어 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 어린이용 안전 포장 및 노인용 포장 수요 증가

- 고급 비경구 플라스틱을 필요로 하는 생물학적 제제 급증

- EU 순환형 경제 규칙이 재활용 가능한 플라스틱 가속

- 전자상거래에 의한 의약품 유통의 확대가 2차 포장의 보호 기능 강화 촉진

- 재택 주사 요법이 소형 PP 프리필드 주사기 견인

- 병원 자동화용 로보틱스 대응 RFID 블리스터 포장

- 시장 성장 억제요인

- PP 및 PET 수지 가격의 변동성

- 추출물 및 용출물에 관한 보다 엄격한 규제 기준

- 주사제에 있어서 유리 및 알루미늄 대체

- 의료용 재생 수지 공급 부족

- 공급망 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

- 업계 밸류체인 분석

- 거시 경제 동향의 영향

제5장 시장 규모 및 성장 예측

- 원재료별

- 폴리프로필렌(PP)

- 폴리에틸렌테레프탈레이트(PET)

- 저밀도 폴리에틸렌(LDPE)

- 고밀도 폴리에틸렌(HDPE)

- 기타(COP, COC, PVC 프리 블렌드, 바이오폴리머)

- 제품 유형별

- 고형 용기

- 액체 및 스포이드 병

- 비강 스프레이 병

- 구강 케어 팩

- 파우치 및 사쉐

- 바이알 및 앰풀(폴리머)

- 카트리지

- 프리필드 주사기

- 뚜껑 및 마개

- 기타(단회 투여용 스트립, 흡입기용 캐니스터)

- 국가별

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 벨기에

- 스웨덴

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Gerresheimer AG

- Amcor PLC

- Berry Global Group Inc.

- AptarGroup Inc.

- Origin Pharma Packaging

- Pretium Packaging

- Klckner Pentaplast

- Comar

- Gil Plastic Products Ltd

- Drug Plastics Group

- West Pharmaceutical Services Inc.

- Nemera

- Bormioli Pharma

- Alpla Group

- Sanner GmbH

- Tekni-Plex

- Weener Plastics

- Jabil Healthcare(Nypro)

- Stevanato Group(EZ-fill polymer vials)

- Raumedic AG

제7장 시장 기회 및 장래 전망

AJY 26.01.30The Europe pharmaceutical plastic packaging market was valued at USD 14.40 billion in 2025 and estimated to grow from USD 15.13 billion in 2026 to reach USD 19.41 billion by 2031, at a CAGR of 5.10% during the forecast period (2026-2031).

Growth pivots on sustainability mandates, biologics proliferation, and home-based therapy expansion, each tightening performance requirements for barrier properties, recyclability, and user-centric design. Leading suppliers are scaling recycled-content lines and RFID-ready formats to satisfy circular-economy goals and hospital automation programs. Meanwhile resin cost swings and stricter extractables protocols are compressing margins, prompting raw-material hedging, supplier diversification, and selective mergers to preserve scale advantages. Competitive intensity remains moderate as incumbents extend vertical integration while specialists seize niches in smart and bio-based solutions, reshaping pricing and collaboration models across the Europe pharmaceutical plastic packaging market.

Europe Pharmaceutical Plastic Packaging Market Trends and Insights

Rising Demand for Child-Resistant and Senior-Friendly Packs

An ageing population and tighter pediatric-safety mandates are steering packaging investments toward closures that combine tactile ease with certified child resistance. European converters spend EUR 2-4 million on every new ergonomic closure platform, a commitment that lifted patient-centric system launches by 18% in 2024. Nemera's torque-reducing closure lowers opening force 30% while exceeding ISO 8317, illustrating how usability and safety can coexist.Regulatory endorsement came via the European Medicines Agency's 2024 guidelines stressing user-friendly packaging for chronic therapies. Early adopters report premium pricing and brand-loyalty gains that offset the initial 15-20% cost uplift, especially for polypropylene caps whose mold precision supports intricate locking mechanisms.

Surge in Biologics Needing Advanced Parenteral Plastics

Biologic drug output in Europe jumped 23% in 2024, with German and Swiss plants ramping monoclonal antibody runs. These high-value molecules require ultra-low extractables and glass-free break-resistance, accelerating demand for cyclic olefin copolymers and cyclic olefin polymers that cost 3-4 times polypropylene yet deliver chemical inertness and clarity. SCHOTT Pharma's EUR 150 million vial-expansion plan underscores supplier commitment to specialized polymer capacity. Biologics-ready packaging is growing nearly twice as fast as the overall Europe pharmaceutical plastic packaging market, reshaping material mix, qualification timelines, and supplier consolidation patterns.

Volatile PP and PET Resin Prices

Petrochemical feedstock disruptions and energy-price swings pushed polypropylene and PET up 15-20% during 2024. Producers such as BASF now quote quarterly, shifting volatility risk to converters who often lock in multi-year supply deals with drugmakers. Smaller firms lacking hedging capacity face squeezes that have triggered consolidation waves, while larger groups diversify supply and invest in in-house recycling to temper pricing shocks. Quarterly adjustment clauses already cover 30-40% of raw-material spend for many mid-tier converters, eroding predictability across the Europe pharmaceutical plastic packaging market.

Other drivers and restraints analyzed in the detailed report include:

- EU Circular-Economy Rules Accelerating Recyclable Plastics

- E-Commerce Pharma Boosting Protective Secondary Packaging

- Stricter Extractables / Leachables Limits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene retained 35.20% Europe pharmaceutical plastic packaging market share in 2025, supported by cost-efficiency, chemical resistance, and widespread regulatory familiarity. Annual pharmaceutical PP consumption exceeds 180,000 tons, covering closures, blisters, and syringes. However, the Europe pharmaceutical plastic packaging market size is tilting toward high-density polyethylene, advancing at a 5.74% CAGR as its superior moisture and oxygen barrier meets biologics stability requirements while presenting stronger recyclability credentials under PPWR.

Sustainability shifts also elevate medical-grade rPET and spur trials of bio-based grades. Gerresheimer has begun commercial runs of recycled PET dropper bottles that satisfy pharma purity thresholds. Niche polymers-COC, COP, PLA blends-command premiums of 300-400% but win specifications for parenterals where ultra-low extractables are mandatory. SCHOTT Pharma's COC expansion underscores rising demand for these specialty resins. Polypropylene suppliers are responding by piloting post-consumer content streams, yet must overcome technical hurdles in odor, color, and traceability to retain leadership within the Europe pharmaceutical plastic packaging market.

Europe Pharmaceutical Plastic Packaging Market is Segmented by Raw Material (Polypropylene, Polyethylene Terephthalate, Low-Density Polyethylene, High-Density Polyethylene, Others), Product Type (Solid Containers, Liquid and Dropper Bottles, Nasal Spray Bottles, Oral-Care Packs, Pouches/Sachets, Vials and Ampoules, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Gerresheimer AG

- Amcor PLC

- Berry Global Group Inc.

- AptarGroup Inc.

- Origin Pharma Packaging

- Pretium Packaging

- Klckner Pentaplast

- Comar

- Gil Plastic Products Ltd

- Drug Plastics Group

- West Pharmaceutical Services Inc.

- Nemera

- Bormioli Pharma

- Alpla Group

- Sanner GmbH

- Tekni-Plex

- Weener Plastics

- Jabil Healthcare (Nypro)

- Stevanato Group (EZ-fill polymer vials)

- Raumedic AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for child-resistant and senior-friendly packs

- 4.2.2 Surge in biologics needing advanced parenteral plastics

- 4.2.3 EU circular-economy rules accelerating recyclable plastics

- 4.2.4 E-commerce pharma boosting protective secondary packaging

- 4.2.5 Home-injection therapies driving small PP pre-filled syringes

- 4.2.6 Robotics-ready RFID blister packs for hospital automation

- 4.3 Market Restraints

- 4.3.1 Volatile PP and PET resin prices

- 4.3.2 Stricter extractables / leachables limits

- 4.3.3 Glass and aluminum substitution in injectables

- 4.3.4 Short supply of medical-grade recycled resin

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

- 4.8 Industry Value-Chain Analysis

- 4.9 Impact of Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Raw Material

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyethylene Terephthalate (PET)

- 5.1.3 Low-Density Polyethylene (LDPE)

- 5.1.4 High-Density Polyethylene (HDPE)

- 5.1.5 Others (COP, COC, PVC-free blends, bio-polymers)

- 5.2 By Product Type

- 5.2.1 Solid Containers

- 5.2.2 Liquid and Dropper Bottles

- 5.2.3 Nasal Spray Bottles

- 5.2.4 Oral-care Packs

- 5.2.5 Pouches / Sachets

- 5.2.6 Vials and Ampoules (polymer)

- 5.2.7 Cartridges

- 5.2.8 Prefilled Syringes

- 5.2.9 Caps and Closures

- 5.2.10 Others (unit-dose strips, inhaler canisters)

- 5.3 By Country

- 5.3.1 United Kingdom

- 5.3.2 Germany

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 Belgium

- 5.3.7 Sweden

- 5.3.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Gerresheimer AG

- 6.4.2 Amcor PLC

- 6.4.3 Berry Global Group Inc.

- 6.4.4 AptarGroup Inc.

- 6.4.5 Origin Pharma Packaging

- 6.4.6 Pretium Packaging

- 6.4.7 Klckner Pentaplast

- 6.4.8 Comar

- 6.4.9 Gil Plastic Products Ltd

- 6.4.10 Drug Plastics Group

- 6.4.11 West Pharmaceutical Services Inc.

- 6.4.12 Nemera

- 6.4.13 Bormioli Pharma

- 6.4.14 Alpla Group

- 6.4.15 Sanner GmbH

- 6.4.16 Tekni-Plex

- 6.4.17 Weener Plastics

- 6.4.18 Jabil Healthcare (Nypro)

- 6.4.19 Stevanato Group (EZ-fill polymer vials)

- 6.4.20 Raumedic AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment