|

시장보고서

상품코드

1911832

중동의 디지털 전환 시장 : 점유율 분석, 업계 동향, 통계, 성장 예측(2026-2031년)Middle East Digital Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

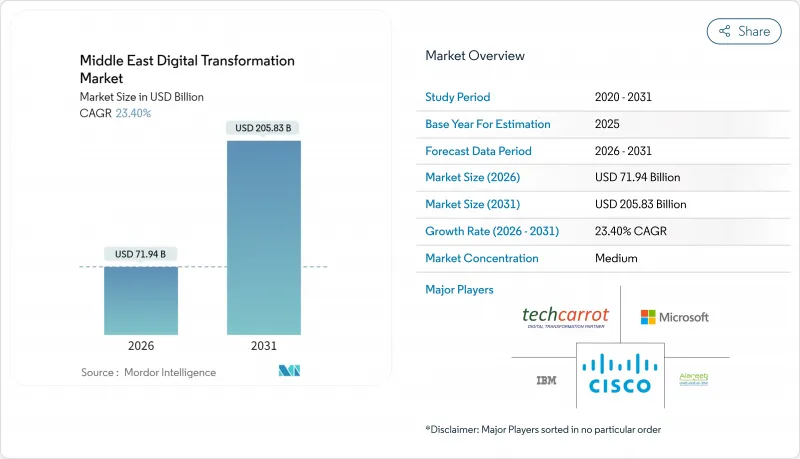

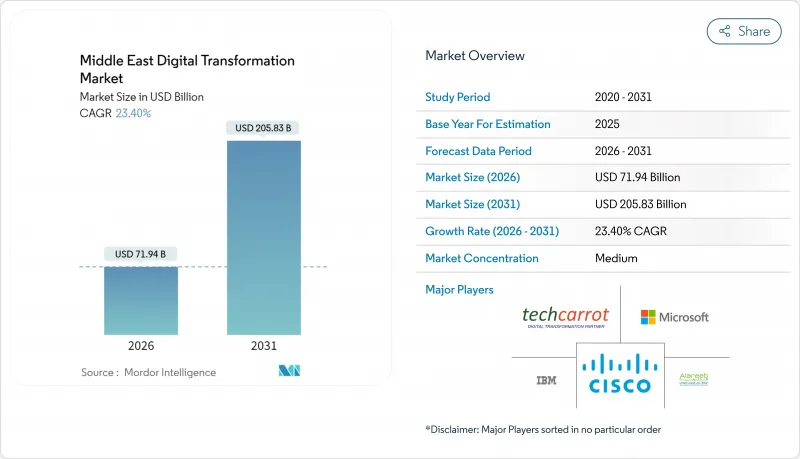

중동의 디지털 전환 시장은 2025년 583억 달러로 평가되었으며, 2026년 719억 4,000만 달러, 2031년까지 2,058억 3,000만 달러에 이를 것으로 예측됩니다. 예측기간(2026-2031년) CAGR은 23.4%를 나타낼 것으로 전망되고 있습니다.

이 급성장은 이 지역이 시책 주도로 석유 의존에서 기술 기반의 가치 창조로 축족을 옮기는 것을 반영하고 있습니다. 국가 펀드는 이미 1,000억 달러 이상을 인공지능 인프라(NEOM의 넷 제로 데이터 공장 포함)에 투자하고 있으며, 하이퍼스케일 클라우드 지역은 현재 걸프 국가 전역에 점재하고 있습니다. 정부 주도의 대형 이니셔티브는 디지털 전환을 경제적 보험으로 자리매김하고, 공공기관이나 국유기업에게 연간 기술예산의 최대 40%를 AI, 5G, 클라우드 프로그램에 배분하도록 요구하고 있습니다. 국제 하이퍼스케일러 기업이 직접 대결을 피하고 현지 유력 기업과 합작 투자를 형성하는 동안 경쟁 환경은 계속 협력하고 있습니다. 또한 5G의 고도화가 스마트 시티와 산업 프로젝트에서 IoT의 규모 확대를 지원함으로써 섹터 기회가 확대되고 있습니다.

중동의 디지털 전환 시장 동향과 인사이트

정부 주도의 대형 이니셔티브가 ICT 및 AI 지출을 가속

공공 섹터 프로그램은 기술 예산을 국가의 다양화 전략에 연결하여 중동의 디지털 전환 시장을 재정의합니다. 사우디아라비아의 '비전 2030', 아랍에미리트(UAE)의 '국가 AI 전략 2031', 카타르의 '국가 비전 2030', 쿠웨이트가 책정 예정인 'AI 로드맵'은 하이퍼스케일 인프라, 공공 서비스의 디지털화, 전국적인 기술 향상에 수십억 달러 규모의 지출 이러한 노력을 통해 지출은 원유 가격 변동의 영향을 받기 어려워지고 다년간 프로젝트 파이프라인이 보장되므로 국제 클라우드 제공업체와 디바이스 OEM은 제조, 연구 개발, 고객 성공 팀의 현지화를 추진하고 있습니다. 그 결과, 공공조달만으로도 이미 연간지역지출의 약 3분의 1을 차지하고 있어 민간섹터의 생태계에 안정적인 수요를 가져오고 있습니다.

하이퍼스케일 클라우드 지역 구축으로 변화 비용 절감

Microsoft, Amazon Web Services, Google 클라우드, Oracle 및 Tencent는 모두 국내 가용성 영역을 실행하기 시작했으며 하이브리드 On-Premise 환경에 비해 기업 운영 비용을 25-35% 절감하고 있습니다. Microsoft는 아부다비 기지 G42와 15억 달러 규모의 제휴를 통해 걸프 지역의 프라이버시법에 준거하면서 세계의 워크로드를 지원하는 주권형 Azure 리전을 전개하고 있습니다. 새로운 영역은 모바일 앱의 지연을 크게 줄이고 규정 준수 오버헤드를 줄이고 아랍어 지원 AI 모델의 대규모 운영을 가능하게 합니다. 이를 통해 은행, 소매 및 공공 안전 부문에서 클라우드 우선 배포를 가속화할 수 있습니다.

고급 디지털 인력과 AI 전문가의 만성 부족

걸프 지역의 고용주 중 80% 이상이 클라우드 아키텍처, 데이터 사이언스 및 사이버 운영 부문에서 즉각적인 인력 부족을 보고하고 있습니다. 고급 DevSecOps 엔지니어의 임금 상승률은 항상 20%를 넘어 프로젝트 기간의 장기화와 총 소유 비용(TCO) 모델의 팽창을 초래합니다. 정부는 STEM 커리큘럼의 가속화, 기술자용 골든 비자 제도, 벤더 주도의 인정 추진(예: Oracle이 2028년까지 지역 전문가 35만명을 육성할 계획)으로 대응하고 있습니다. 자동화 툴, 로우코드 플랫폼, 생성형 AI 코파일럿이 부족을 일부 보충하고 있지만, 복잡한 통합 작업은 여전히 희귀한 전문 인력에 의존하고 있습니다.

부문 분석

클라우드와 에지 플랫폼은 2025년 수익의 22.45%를 차지하며 중동의 디지털 전환 시장에서 모든 기능의 기반으로 필수적인 역할을 강조하고 있습니다. GPU 리치 인스턴스와 서버리스 런타임의 채택은 주류가 되고, 소블린 클라우드는 공공 부문과 규제 대상 워크로드의 컴플라이언스를 확보합니다. 대규모 언어 모델부터 컴퓨터 비전 검사에 이르기까지 인공지능 용도는 26.55%의 연평균 복합 성장률(CAGR)로 추이하여 고성능 네트워크와 오픈소스 MLOps 스택에 대한 수요를 이끌고 있습니다. AI의 성숙에 따라 석유 및 가스 정제소에서의 디지털 트윈의 파일럿 도입, 물류 허브에서의 산업용 로봇의 개수 설치, 블록체인 베이스 무역 금융 파일럿이 솔루션의 폭을 넓히고 있습니다. 증강현실(XR) 훈련 시뮬레이터는 항공 및 의료 부문에서 보급이 진행되고 몰입형 모듈에 의해 인정 시간이 최대 40% 단축됩니다. 5G와 프라이빗 LTE 슬라이스로 실현되는 IoT 센서 그리드는 자산 추적과 예지 보전의 실천을 변화시키고, 적층 조형 기술은 굴착 장치 부품의 현지 인쇄라는 틈새 부문에서 채택이 진행됩니다. 사이버 보안 플랫폼은 모든 스택을 포괄하고 매년 두 자리의 지속적인 지출 성장을 계속 견인합니다.

2차 기세는 유사한 패턴을 나타냅니다. 통신 중앙국에 집약된 에지 클라우드 노드가 공장 현장의 비전 시스템에서 밀리초 단위의 지연을 줄이고, AI-as-a-Service API가 중소기업에 의한 사내 모델 구축 없이 채팅봇 도입을 지원합니다. 정부는 아랍어 AI 조사를 지원하고 데이터 거주 기준을 설정하는 주권 모델 생태계를 육성합니다. 이 확장 모자이크 구조 중 양자 연구실, 뉴로모픽 칩 프로토타입, 포토닉 인터커넥트 기술 등의 다른 기술은 시드 자금을 얻고 있지만 여전히 장기 투자 대상입니다. 이러한 움직임이 결합되어 중동의 디지털 전환 시장은 차세대 엔터프라이즈 스택의 실험장으로 자리를 잡고 있습니다.

BFSI(은행, 금융 및 보험) 부문은 코어뱅킹 현대화, 즉시결제 플랫폼, 오픈뱅킹 API의 조기 도입으로 2025년 시점에서 중동의 디지털 전환 시장의 18.55%를 차지했습니다. 한편, 의료 부문은 원격 의료, AI 진단, 전자 건강 기록 의무화의 보급에 따라 25.95%의 연평균 복합 성장률(CAGR)로 급성장하고 있습니다. 두바이 헬스케어 시티 기관에 의한 의료청구의 자동심사 파일럿 사업은 AI가 처리시간을 35% 단축하는 실례를 보여줍니다. 제조업과 에너지 기업은 디지털 트윈을 고도의 공정 제어 시스템과 통합하여 예기치 못한 다운타임을 1자리수 후반의 비율로 줄였습니다. 소매업체는 옴니채널 앱, 점내 분석, AI 추천 엔진을 배포하여 전환율을 향상시키고 있습니다. 운송 및 물류사업자는 화물 가시화의 엔드 투 엔드 디지털화와 자율형 야드 관리 솔루션을 도입하고, 공공 부문은 전자 정부와 스마트 시티의 실현을 가속화하고 있습니다.

이러한 이니셔티브의 시너지 효과로 고객 기반의 확대가 실현되었습니다. 고급 이용 사례가 ROI를 입증함에 따라 산업 횡단 벤치마킹이 기술 전환을 가속화하고 있습니다. 병원에서는 은행 수준의 본인 확인 시스템이 도입되어 소매 산업에서는 석유 및 가스 산업의 예지보전 알고리즘이 활용되고 있습니다. 이러한 상호교류는 서비스 제공업체의 통합 기회를 심화시키고 중동의 디지털 전환 시장 내에 신속한 혁신 사이클을 확립하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 애널리스트에 의한 3개월간의 지원

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 발전 및 도입 로드맵

- 시장 성장 촉진요인

- 정부에 의한 대규모 시책이 ICT와 AI 지출을 가속

- 하이퍼스케일 클라우드 리전의 전개에 의한 변화 비용 절감

- 5G와 광섬유 네트워크의 고도화에 의한 IoT의 규모 확대

- 국부펀드 및 민간자본의 AI 인프라 투자 확대

- 소버린 AI 및 국가 차원의 LLM 프로젝트 등장

- 통신 인프라의 수익화에 의한 디지털 설비 투자의 촉진

- 시장 성장 억제요인

- 상급 디지털 인재와 AI 전문가의 만성적인 부족

- 사이버 보안 및 데이터 주권 준수 위험 증가

- GPU와 고성능 서버공급 병목

- 하이퍼스케일 데이터센터의 냉각에 있어서의 에너지 수자원의 제약

- 밸류체인 분석

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 거시경제 요인이 시장에 미치는 영향

제5장 시장 규모와 성장 예측

- 기술 유형별

- 인공지능(AI)과 머신러닝(ML)

- 증강현실(VR과 AR)

- 사물인터넷(IoT)

- 산업용 로봇

- 블록체인

- 디지털 트윈

- 적층 조형

- 사이버 보안

- 클라우드와 엣지 컴퓨팅

- 기타

- 최종 사용자 산업별

- 제조업

- 석유 및 가스 유틸리티

- 소매 및 전자상거래

- 운송 및 물류

- 헬스케어

- BFSI

- 통신 및 IT

- 정부 및 공공 부문

- 기타

- 전개 모드별

- On-Premise

- 클라우드

- 하이브리드

- 기업 규모별

- 대기업

- 중소기업(SME)

- 국가별

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 쿠웨이트

- 기타 중동 국가(이스라엘, 바레인, 이란, 오만, 요르단 등)

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Cisco Systems Inc.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Accenture PLC

- Siemens AG

- Amazon Web Services Inc.

- Google LLC

- Huawei Technologies Co. Ltd.

- Ericsson AB

- stc Group

- G42 Holding Ltd

- Etisalat by eand

- Ooredoo Group

- Techcarrot FZ LLC

- Alareeb ICT

- Baarez Technology Solutions

- Deloitte Touche Tohmatsu Ltd.

- Ernst and Young(E&Y) Global Limited

- PwC International Limited

- Capgemini SE

- Cognizant Technology Solutions

- Wipro Ltd.

제7장 시장 기회와 장래의 전망

SHW 26.02.05The Middle East Digital Transformation Market was valued at USD 58.30 billion in 2025 and estimated to grow from USD 71.94 billion in 2026 to reach USD 205.83 billion by 2031, at a CAGR of 23.4% during the forecast period (2026-2031).

This swift rise mirrors the region's policy-driven pivot from oil dependence toward technology-anchored value creation. Sovereign wealth funds have already committed more than USD 100 billion to artificial-intelligence infrastructure, including NEOM's net-zero data factories, while hyperscale cloud regions now dot every Gulf state . Government mega-initiatives treat digital transformation as economic insurance, compelling public agencies and state-owned enterprises to allocate up to 40% of their annual technology budgets to AI, 5G, and cloud programs. Competitive dynamics remain collaborative as international hyperscalers form joint ventures with local champions instead of entering head-to-head battles, and sector opportunities broaden as 5G densification underpins IoT scale-up across smart-city and industrial projects.

Middle East Digital Transformation Market Trends and Insights

Government mega-initiatives accelerating ICT and AI spend

Public-sector programs redefine the Middle East digital transformation market by anchoring technology budgets to national diversification strategies. Saudi Vision 2030, the UAE National AI Strategy 2031, Qatar National Vision 2030, and Kuwait's forthcoming AI Roadmap earmark multibillion-dollar outlays for hyperscale infrastructure, public-service digitization, and nationwide upskilling. These commitments insulate spending from oil-price cycles and guarantee multi-year project pipelines, prompting international cloud providers and device OEMs to localize manufacturing, R&D, and customer-success teams. As a result, public procurement alone already accounts for nearly one-third of annual regional outlays, funneling steady demand into private-sector ecosystems.

Hyperscale cloud-region rollouts cutting transformation costs

Microsoft, Amazon Web Services, Google Cloud, Oracle, and Tencent have all switched on in-country availability zones, driving enterprise operating-cost reductions of 25-35% compared with hybrid on-premises estates. Microsoft's USD 1.5 billion collaboration with Abu Dhabi-based G42 is rolling out sovereign Azure regions that comply with Gulf privacy laws while supporting global workloads. New zones slash latency for mobile apps, reduce compliance overhead, and enable Arabic-language AI models to run at scale, accelerating cloud-first adoption across banking, retail, and public safety.

Chronic shortage of senior digital talent and AI specialists

Eighty-plus percent of Gulf employers report immediate hiring gaps in cloud architecture, data science, and cyber-operations roles. Wage inflation regularly tops 20% for senior DevSecOps engineers, elongating project timelines and inflating total-cost-of-ownership models. Governments respond with accelerated STEM curricula, golden-visa schemes for tech workers, and vendor-led certification drives, such as Oracle's plan to upskill 350,000 regional professionals by 2028 . Automation tools, low-code platforms, and generative-AI copilots partially offset shortages, yet complex integration work still relies on scarce specialist talent.

Other drivers and restraints analyzed in the detailed report include:

- 5G and fiber network densification enabling IoT scale-up

- Sovereign-wealth and private-capital surge into AI infrastructure

- Heightened cybersecurity and data-sovereignty compliance risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud and edge platforms anchor 22.45% of 2025 revenue, underscoring their role as the indispensable substrate for every other capability in the Middle East digital transformation market. Adoption of GPU-rich instances and serverless runtimes is now mainstream, and sovereign clouds ensure compliance for public-sector and regulated workloads. Artificial-intelligence applications, from large language models to computer-vision inspection, are on track for a 26.55% CAGR, pulling through demand for high-performance networking and open-source MLOps stacks. As AI matures, digital-twin pilots in oil-gas refineries, industrial-robotics retrofits in logistics hubs, and blockchain-based trade-finance pilots widen the solution mix. Extended-reality training simulators gain traction in aviation and healthcare, where immersive modules cut certification time by up to 40%. IoT sensor grids, enabled by 5G and private-LTE slices, transform asset-tracking and predictive-maintenance practices, while additive manufacturing finds niche uptake in on-rig parts printing. Cybersecurity platforms wrap the entire stack, attracting sustained double-digit spend growth every year.

Second-order momentum follows the same pattern. Edge-cloud nodes clustered at telecom central offices trim millisecond latency for factory-floor vision systems, and AI-as-a-Service APIs help SMEs deploy chatbots without building in-house models. Governments back Arabic-language AI research, fostering sovereign-model ecosystems that set data-residency benchmarks. Within this growing mosaic, other technologies, quantum research labs, neuromorphic chip prototypes, and photonic interconnects receive seed funding but remain long-horizon bets. Collectively, these dynamics solidify the Middle East digital transformation market as a laboratory for next-generation enterprise stacks.

BFSI seized 18.55% of the Middle East digital transformation market share in 2025 owing to early adoption of core-bank modernization, instant-payments platforms, and open-banking APIs. Yet healthcare is racing ahead at a 25.95% CAGR as telehealth, AI-enabled diagnostics, and electronic health records mandates proliferate. Dubai Healthcare City Authority's pilot that auto-reviews medical claims demonstrates how AI slashes processing time by 35%. Manufacturing and energy players integrate digital twins with advanced process control systems, reducing unplanned downtime by high single-digit percentages. Retailers roll out omnichannel apps, in-store analytics, and AI recommendation engines that lift conversion rates. Transportation and logistics operators digitize end-to-end freight visibility and deploy autonomous yard-management solutions, while the public sector intensifies e-government and smart-city implementations.

The net effect is a broadening customer base. As frontier use cases prove ROI, cross-industry benchmarking accelerates technology migration. Hospitals adopt banking-style identity verification; retail borrows predictive-maintenance algorithms from oil and gas. That cross-pollination deepens integration opportunities for service providers and cements a fast-cycling innovation loop inside the Middle East digital transformation market.

The Middle East Digital Transformation Market Report is Segmented by Technology Type (AI and ML, Extended Reality, Iot, Industrial Robotics, Blockchain, and More), End-User Industry (Manufacturing, Oil and Gas Utilities, Retail and E-Commerce, and More), Deployment Mode (On-Premise, Cloud, Hybrid), Enterprise Size (Large Enterprises, Smes), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Cisco Systems Inc.

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Oracle Corporation

- Accenture PLC

- Siemens AG

- Amazon Web Services Inc.

- Google LLC

- Huawei Technologies Co. Ltd.

- Ericsson AB

- stc Group

- G42 Holding Ltd

- Etisalat by eand

- Ooredoo Group

- Techcarrot FZ LLC

- Alareeb ICT

- Baarez Technology Solutions

- Deloitte Touche Tohmatsu Ltd.

- Ernst and Young (E&Y) Global Limited

- PwC International Limited

- Capgemini SE

- Cognizant Technology Solutions

- Wipro Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Evolution and Adoption Roadmap

- 4.3 Market Drivers

- 4.3.1 Government mega-initiatives accelerating ICT and AI spend

- 4.3.2 Hyperscale cloud region rollouts cutting transformation costs

- 4.3.3 5G and fiber network densification enabling IoT scale-up

- 4.3.4 Sovereign wealth and private-capital surge into AI infrastructure

- 4.3.5 Emergence of sovereign AI and national LLM projects

- 4.3.6 Telecom-infrastructure monetization unlocking digital CAPEX

- 4.4 Market Restraints

- 4.4.1 Chronic shortage of senior digital talent and AI specialists

- 4.4.2 Heightened cybersecurity and data-sovereignty compliance risks

- 4.4.3 GPU and advanced-server supply bottlenecks

- 4.4.4 Energy-water constraints for hyperscale data center cooling

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology Type

- 5.1.1 Artificial Intelligence and Machine Learning

- 5.1.2 Extended Reality (VR and AR)

- 5.1.3 Internet of Things (IoT)

- 5.1.4 Industrial Robotics

- 5.1.5 Blockchain

- 5.1.6 Digital Twin

- 5.1.7 Additive Manufacturing

- 5.1.8 Cybersecurity

- 5.1.9 Cloud and Edge Computing

- 5.1.10 Other Technologies

- 5.2 By End-User Industry

- 5.2.1 Manufacturing

- 5.2.2 Oil and Gas Utilities

- 5.2.3 Retail and E-commerce

- 5.2.4 Transportation and Logistics

- 5.2.5 Healthcare

- 5.2.6 BFSI

- 5.2.7 Telecom and IT

- 5.2.8 Government and Public Sector

- 5.2.9 Other End-user Industries

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.3.3 Hybrid

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Country

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Qatar

- 5.5.4 Kuwait

- 5.5.5 Other Middle-East Countries (Israel, Bahrain, Iran, Oman, Jordan, etc.)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 SAP SE

- 6.4.5 Oracle Corporation

- 6.4.6 Accenture PLC

- 6.4.7 Siemens AG

- 6.4.8 Amazon Web Services Inc.

- 6.4.9 Google LLC

- 6.4.10 Huawei Technologies Co. Ltd.

- 6.4.11 Ericsson AB

- 6.4.12 stc Group

- 6.4.13 G42 Holding Ltd

- 6.4.14 Etisalat by eand

- 6.4.15 Ooredoo Group

- 6.4.16 Techcarrot FZ LLC

- 6.4.17 Alareeb ICT

- 6.4.18 Baarez Technology Solutions

- 6.4.19 Deloitte Touche Tohmatsu Ltd.

- 6.4.20 Ernst and Young (E&Y) Global Limited

- 6.4.21 PwC International Limited

- 6.4.22 Capgemini SE

- 6.4.23 Cognizant Technology Solutions

- 6.4.24 Wipro Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment