|

시장보고서

상품코드

1931743

산업용 펌프 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Industrial Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

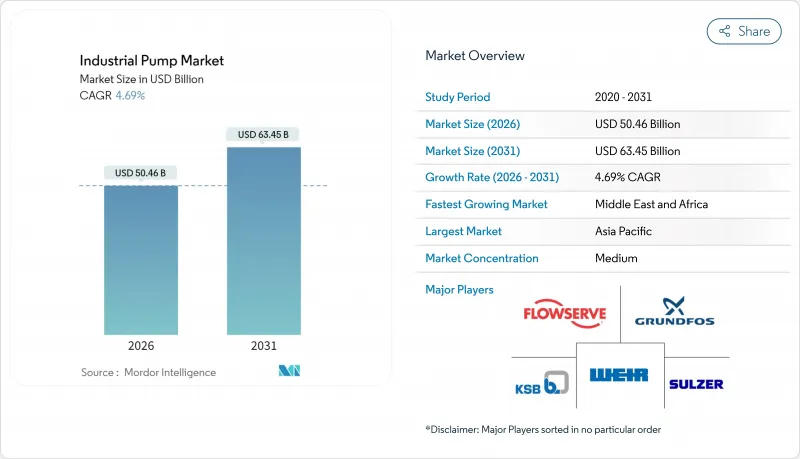

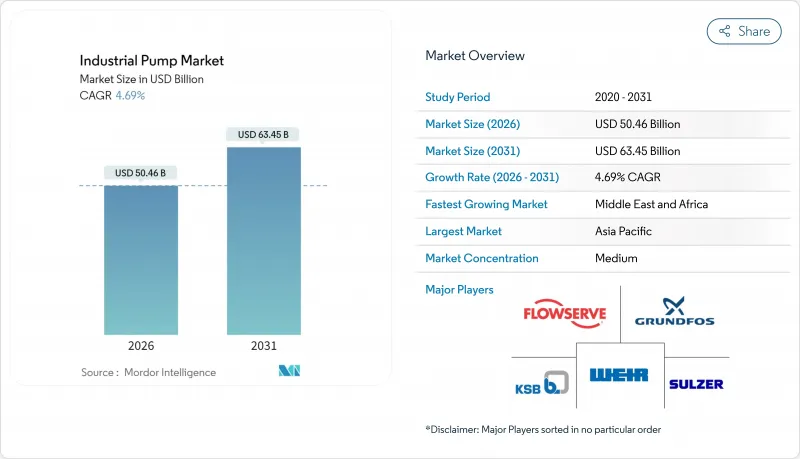

산업용 펌프 시장은 2025년에 482억 달러로 평가되며, 2026년 504억 6,000만 달러에서 2031년까지 634억 5,000만 달러에 달할 것으로 예측되고 있습니다.

예측 기간(2026-2031년)의 CAGR은 4.69%로 예상됩니다.

노후화된 도시 네트워크의 지속적인 갱신, 석유화학 플랜트 증설, 강화되는 효율성 규제는 장기적인 공급망 변동에도 불구하고 시장의 회복력을 지원했습니다. 수처리 분야에 대한 자본 지출은 여전히 가장 큰 수요 견인 요인으로, 미국에서만 2022-2026년까지 물 인프라 갱신에 500억 달러 이상을 지출할 것으로 예측됩니다. 카타르와 사우디의 메가 프로젝트는 에틸렌 크래커 및 가스 처리 플랜트에서 부식성 및 고온 매체를 처리할 수 있는 고사양 펌프의 수주를 지속적으로 증가시켰습니다. 아시아태평양은 중국, 인도, 동남아시아의 대규모 산업화를 배경으로 물량 기준 선두를 유지한 반면, 중동 및 아프리카은 석유화학 산업의 다변화가 가속화되면서 가장 빠른 성장세를 기록했습니다.

세계 산업용 펌프 시장 동향 및 전망

세계 상하수도 처리 투자 증가

2024년과 2025년 초에 발표된 기록적인 지자체 예산으로 인해 대용량 원심 펌프와 수중 하수 펌프의 입찰 수량이 증가했습니다. 미국 환경보호청(EPA)은 장기적인 개보수 수요를 7,440억 달러 이상으로 추정하고 있으며, 수시티의 4억 6,500만 달러 규모의 지역 시설과 케이프피어의 2억 3,900만 달러 규모의 사우스사이드 플랜트 등 여러 단계에 걸친 업그레이드가 추진되고 있습니다. 고도처리 의무화로 고압 역삼투압 장치에 대한 관심이 높아지면서 이집트의 알 마하사마 폐수 재생 프로젝트에서 슬러처의 수직 다단 시스템이 채택되었습니다. 수도사업자는 진동-온도 데이터를 클라우드 대시보드로 전송하는 무선 센서의 탑재를 확대하여 중요 설비의 평균 수리 시간을 단축하고 있습니다. 조달 프레임워크에서 총소유비용(TCO) 계산이 중시되기 시작했고, 에너지 효율 설계가 우대되면서 구매자는 EU의 MEI 기준을 여유 있게 충족하는 고효율 모터를 선택하는 경향이 강해지고 있습니다. 모니터링 의무 강화는 애프터마켓 수입원을 확대하고, OEM(Original Equipment Manufacturer)의 지속적인 서비스 계약의 기반이 되고 있습니다.

중동 및 아프리카의 석유화학 플랜트 증설

걸프 산유국들은 다운스트림 부문 다각화를 추진하며 크래커, 폴리머 유닛, 가스처리 플랜트 EPC 계약을 발주했습니다. 이를 위해서는 총 수천 대의 내식성 펌프가 필요합니다. 카타르의 라스 라판 폴리머 복합단지(예산 60억 달러)는 2027년 가동을 목표로 하루 2,080천 톤 규모의 에탄 크래커를 건설하고 있습니다. 사우디아라비아의 110억 달러 규모의 아밀랄 프로젝트는 SATORP 정유소와 통합된 165만 톤의 에틸렌 명목 생산 능력을 추가하여 400°F(약 204°C)의 토출 온도를 견딜 수 있는 API 610 규격 펌프에 대한 수요가 크게 증가했습니다. 조달 입찰의 현지 조달 조항은 국제 OEM(Original Equipment Manufacturer)가 케이싱 가공 및 최종 조립을 현지화할 수 있는 인센티브를 강화했습니다. 최종사용자는 전력 소비 억제를 위해 가변 주파수 드라이브를 우선시하고, 지역 에너지 절약 목표에 따라 스마트 모터 제어의 채택이 촉진되었습니다.

철강 및 구리 가격 변동으로 총 소유 비용 증가

2024년, 구리 가격은 공급 부족 우려로 톤당 1만 달러를 돌파하고 1만 1,000달러에 근접하는 수준까지 상승. 구리를 많이 사용하는 고정자 및 권선 부품의 생산 비용을 3.5-4.2% 상승시켰습니다. 탄소중립 철강재 구상은 제철소가 수소 기반 생산에 연동된 그린프리미엄 추가 요금을 제철소에 전가하면서 불확실성이 더욱 커졌습니다. 제조업체는 헤지 프로그램 강화, 자재 절감을 위한 케이싱 재설계, 공급 계약에 변동가격 조항 도입에 대응. 한편 최종사용자는 임의 교체를 연기하여 설비의 평균 수명을 연장하는 한편, 산업용 펌프 시장의 단기 출하량을 억제했습니다.

부문 분석

원심 펌프 유닛은 2025년 매출의 61.85%를 차지했으며, 급수, 화학물질 이송 및 공조 루프에서 입증된 비용 대비 성능의 균형이 산업용 펌프 시장을 지원했습니다. 지자체용 사이클의 평균 오버홀 주기가 3년이기 때문에 이 부문은 안정적인 애프터마켓 수요를 창출하고 있습니다. 그러나 고점도 슬러리 처리의 특수한 수요로 인해 증분 점유율은 2031년까지 연평균 복합 성장률(CAGR) 7.45%로 확대될 것으로 예상되는 프로그레시브 케이브 설계로 전환될 것으로 예측됩니다. 저전단 이송을 중시하는 석유화학 및 광업 고객층에서 프로그레시브 케이브 펌프는 산업용 펌프 시장 점유율을 확대해 나가고 있습니다. 한편, 왕복동 펌프와 다이어프램 펌프는 각각 고압 주입과 위생 생산에서 중요한 역할을 유지했으나, 틈새 시장으로 발전했습니다. IoT 개조는 기존 원심 펌프 세트에도 적용되어 예지보전을 위한 진동 분석을 가능하게 함으로써 예기치 못한 다운타임을 최대 30%까지 줄일 수 있습니다.

일축 편심 스크류 펌프 제조업체는 내마모성 로터 코팅에 많은 투자를 하여 연마 하중 하에서 8,000시간 이상의 서비스 간격을 연장했습니다. 로터리 기어 펌프와 페리스탈틱 펌프는 배터리 재료 생산 라인의 새로운 미량 투여 작업에 대응하여 최종 용도에 대한 혁신의 확산을 보여주었습니다. 센서 텔레메트리로 구축된 디지털 트윈을 통해 작업자는 전체 유압 엔벨로프에서 캐비테이션 위험을 시뮬레이션하여 임펠러를 보호하는 공정 제어를 개선할 수 있게 되었습니다. 공급업체는 유지보수를 간소화하고 예비 재고를 줄이는 모듈식 카트리지 실의 중요성을 지속적으로 강조했습니다. 에너지 강도에 대한 규제적 관심이 높아짐에 따라 케이싱 소용돌이 및 디퓨저 베인의 효율 향상은 광범위한 산업용 펌프 시장에서 모든 펌프 유형에 대한 경쟁적 요구사항이 되었습니다.

전기 구동 장치는 2025년 77.95%로 압도적인 점유율을 차지할 것으로 예상되며, 선진국의 거의 보편적인 전력망 접근과 가변 주파수 드라이브로 인한 효율성 향상에 따른 수혜를 입게 될 것입니다. Graco의 QUANTM 플랫폼이 기록한 현장 데이터에 따르면 횡방향 자속 토폴로지를 통해 최대 85%의 모터 효율을 달성하여 전력 기반의 수명주기 비용 우위를 입증했습니다. 그러나 태양광발전 솔루션은 아프리카와 남아시아의 농촌 관개 프로젝트를 배경으로 CAGR 11.1%로 확대되어 산업용 펌프 업계에서 가장 빠르게 성장하는 분야로 부상했습니다. 설치 비용은 76.23유로(89.13달러)에서 1,219.59유로(1,425.95달러)로, 특히 디젤 발전기의 연료 물류 비용을 고려하면 경쟁력 있는 균등화 비용을 실현했습니다.

디젤 엔진 패키지는 전력망의 신뢰성이 여전히 의문시되고 있는 유전 파쇄 및 긴급 빗물 배수에서 전략적 중요성을 유지했습니다. 유압 구동 및 공압 구동은 출력 밀도와 점화 안전성을 중시하는 위험 지역 설치 및 이동식 플랜트 설비용으로 계속 채택되었습니다. 태양광발전 어레이와 리튬이온 축전지를 결합한 하이브리드 마이크로그리드 솔루션은 인도네시아의 여러 광산에서 시험 도입 단계에 접어들었으며, 디젤 보조 없이 24시간 가동할 수 있게 되었습니다. 기존 전기설비에 가변속 구동장치(VFD)를 개조하여 연속운전 해수담수화 플랜트에서 최대 20%의 에너지 비용 절감을 달성했습니다. 전반적으로 전원 구성은 최종사용자의 현실적인 선택을 보여주지만, 산업용 펌프 시장에서 전기 드라이브의 우위는 예측 기간 중 지속될 것으로 예측됩니다.

산업용 펌프 시장은 펌프 유형(원심식, 왕복동식, 회전식 등), 동력원(전기, 디젤, 태양광 등), 최종사용자 산업(석유/가스, 상하수도, 화학/석유화학, 발전, 광업, 식품 및 음료 등), 펌프 설치 형태(수중형, 지상형), 지역(북미, 남미, 유럽, 아시아태평양, 중동, 아프리카)으로 구분됩니다. 아시아태평양, 중동 및 아프리카)로 구분됩니다.

지역별 분석

아시아태평양은 수십년에 걸친 산업 기반 구축, 대규모 도시 인프라 정비, 정책 주도의 제조 거점 현지화를 통해 2025년 44.85%의 매출 점유율로 시장을 주도할 것으로 예측됩니다. 복건성의 새로운 에틸렌 크래커 단지와 호주의 대규모 해수 담수화 계획은 고효율 다단 펌프의 조달을 촉진했습니다. 중국의 폐수 재이용 촉진책과 인도의 화학제품 생산 연동형 장려 프로그램(PLI)은 국내외 펌프 제조업체들에게 지속적인 수주를 이끌었습니다. 전력 소비 강도 및 탄소발자국에 대한 규제가 강화됨에 따라 산업용 펌프 시장에서 가변 속도 구동 장치(VFD)로의 전환을 촉진하고, 고효율 제품군으로 시장 규모를 확대하는 계기가 되었습니다.

중동 및 아프리카은 6.05%의 가장 빠른 CAGR을 기록했으며, 사우디아라비아, 카타르, 아랍에미레이트의 총 170억 달러 규모의 석유화학 투자가 주도했습니다. NEOM의 100만m3/일 해수처리 프로젝트와 같은 해수담수화 사업에서는 염화물 응력 부식에 강한 고압 듀플렉스강 펌프가 요구되었습니다. 잠비아와 콩고민주공화국의 아프리카 광업의 확장으로 내마모성 슬러리 유닛의 주문이 증가했습니다. 현지 조달 프레임워크를 통해 OEM(Original Equipment Manufacturer)는 오만과 남아공에 서비스 거점을 설치하여 오버홀 처리 시간을 단축하고 브랜드 충성도를 강화할 수 있게 되었습니다. 북미에서는 상수도 인프라 법안을 배경으로 안정적인 갱신 주기가 이어졌으며, 캘리포니아, 텍사스, 플로리다 주에서 원심 펌프와 수직 터빈 펌프의 갱신 입찰이 집중되었습니다. 에너지 정책의 특혜로 수소전기자동차의 조기 도입이 진행되어 내식성 순환펌프의 틈새 주문이 발생함. 유럽의 엄격한 MEI 규제는 초 고효율 설계에 대한 수요를 불러일으켰고, 플랜트 소유주들은 총소유비용 지표를 재평가하게 되었습니다. 라틴아메리카는 규모는 작지만 농업용 관개 펌프의 꾸준한 보급과 칠레, 페루의 광업 관련 수요가 확인되었습니다. 모든 지역에서 예지보전을 특징으로 하는 디지털 서비스 제안이 입찰 평가의 결정적인 요소로 작용하여 산업용 펌프 시장의 경쟁 환경을 더욱 형성했습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.02.25The industrial pump market was valued at USD 48.2 billion in 2025 and estimated to grow from USD 50.46 billion in 2026 to reach USD 63.45 billion by 2031, at a CAGR of 4.69% during the forecast period (2026-2031).

Sustained replacement of aging municipal networks, petrochemical capacity additions, and tighter efficiency rules underpinned the market's resilience through prolonged supply-chain volatility. Capital spending on water treatment remained the single largest pull-forward of demand, with the United States alone earmarking more than USD 50 billion for water infrastructure upgrades between 2022 and 2026. Mega-projects in Qatar and Saudi Arabia continued to lift orders for high-specification pumps capable of handling corrosive, high-temperature media in ethylene crackers and gas-processing trains. Asia-Pacific retained volumetric leadership on the back of large-scale industrialization across China, India, and Southeast Asia, while the Middle East and Africa posted the fastest growth trajectory as petrochemical diversification accelerated.

Global Industrial Pump Market Trends and Insights

Rising Water and Wastewater Treatment Spending Globally

Record municipal budgets released in 2024 and early 2025 translated into larger tender volumes for high-capacity centrifugal and submersible sewage pumps. The US Environmental Protection Agency estimated long-term rehabilitation needs above USD 744 billion, prompting multi-phase upgrades such as Sioux City's USD 465 million regional facility and Cape Fear's USD 239 million Southside plant. Advanced treatment mandates drove interest in high-pressure reverse-osmosis trains, with Sulzer's vertical multistage systems underpinning Egypt's Al Mahsama drainage reclamation project. Utilities are increasingly embedding wireless sensors that stream vibration and temperature data into cloud dashboards, shortening mean-time-to-repair on critical units. Procurement frameworks began weighting total-cost-of-ownership calculations that favor energy-efficient designs, nudging buyers toward premium efficiency motors that comfortably clear EU MEI thresholds. Heightened monitoring obligations also expanded aftermarket revenue pools, anchoring recurring service contracts for OEMs.

Expansion of Petrochemical Capacity in MEA

Gulf producers pushed downstream diversification agendas, awarding EPC contracts for crackers, polymer units, and gas-processing trains that collectively require thousands of corrosion-resistant pumps. Qatar's Ras Laffan polymers complex, budgeted at USD 6 billion, incorporated a 2,080 KTA ethane cracker slated for 2027 on-stream dates. Saudi Arabia's USD 11 billion Amiral project added 1.65 million tons of ethylene nameplate capacity integrated with SATORP's refinery, multiplying demand for API 610 compliant pumps that withstand 400°F discharge temperatures. Local-content clauses inside procurement tenders intensified incentives for international OEMs to localize casing machining and final assembly. End-users prioritized variable-frequency drives to curb power draw, reinforcing adoption of smart motor controls that align with regional energy-efficiency ambitions.

Volatility in Steel and Copper Prices Inflating TCO

Copper cleared USD 10,000 per metric ton in 2024 and flirted with USD 11,000 amid looming supply deficits, hiking producer input costs by 3.5%-4.2% on copper-intensive stators and windings. Carbon-neutral steel initiatives added further unpredictability as mills passed on green-premium surcharges linked to hydrogen-based production. Manufacturers responded by tightening hedging programs, redesigning casings for material thrift, and introducing dynamic price clauses into supply contracts. End-users, meanwhile, deferred discretionary replacements, stretching the mean equipment life and tempering near-term shipment volumes in the industrial pump market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Industrial Infrastructure Build-out Across Asia-Pacific

- Demand for Corrosion-Resistant Pumps in Green-Hydrogen Electrolyzers

- Stricter Pump-Efficiency Directives Delaying Cap-ex Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Centrifugal units retained 61.85% of 2025 revenue, anchoring the industrial pump market through their proven cost-performance balance in water supply, chemical transfer, and HVAC loops. The segment generated steady aftermarket volumes, given typical mean-time-between-overhauls of three years in municipal duty cycles. However, specialty demands in viscous slurry handling shifted incremental share toward progressing cavity designs, which are projected to clock 7.45% CAGR through 2031. The progressing cavity cohort captured a rising slice of the industrial pump market size for petrochemical and mining customers that prize low-shear conveyance. Meanwhile, reciprocating and diaphragm pumps preserved critical roles in high-pressure injection and sanitary production, respectively, albeit with niche footprints. IoT retrofits became common even on legacy centrifugal sets, enabling predictive vibration analytics that cut unscheduled downtime by up to 30%.

Progressing cavity manufacturers invested heavily in wear-resistant rotor coatings to extend service intervals beyond 8,000 hours under abrasive duty. Rotary gear and peristaltic pumps addressed emerging micro-dosing tasks within battery-materials manufacturing lines, underscoring the breadth of end-use innovation. Digital twins built from sensor telemetry allowed operators to simulate cavitation risk across the hydraulic envelope, driving process-control refinements that protect impellers. Suppliers continued to emphasize modular cartridge seals that simplify maintenance and shrink spare inventory. With regulatory spotlight fixed on energy intensity, efficiency upgrades in casing volutes and diffuser vanes became a competitive must-have across all pump types in the broader industrial pump market.

Electric-driven assemblies held a commanding 77.95% share in 2025, benefitting from near-universal grid access in industrialized economies and the incremental efficiency yields of variable-frequency drives. Field data logged by Graco's QUANTM platform demonstrated up to 85% motor efficiency thanks to transverse-flux topology, reinforcing the narrative of electricity-based lifecycle cost advantage. Solar-powered solutions, however, emerged as the fastest expanding slice of the industrial pump industry, advancing at an 11.1% CAGR on the back of rural irrigation projects in Africa and South Asia. Installation costs ranging from EUR 76.23 (USD 89.13) to EUR 1,219.59 (USD 1,425.95) translated to competitive levelized costs, particularly once fuel-logistics premiums on diesel sets were factored in.

Diesel-engine packages retained strategic relevance for oilfield fracturing and emergency stormwater evacuation, where grid resilience remained questionable. Hydraulic and pneumatic drives continued to serve hazardous-area placements and mobile plant equipment that prized power density and ignition safety. Hybrid microgrid solutions that pair PV arrays with lithium-ion storage entered the pilot stage at several Indonesian mines, offering 24/7 uptime without diesel supplementation. VFD retrofits on existing electric fleets shaved energy bills by up to 20% in continuous-duty desalination applications. Altogether, the power-source mix illustrated end-user pragmatism, but electric leadership in the industrial pump market is expected to persist through the forecast horizon.

Industrial Pump Market is Segmented by Pump Type (Centrifugal, Reciprocating, Rotary, and More), Power Source (Electric, Diesel, Solar, and More), End-User Industry (Oil and Gas, Water and Waste-Water, Chemicals and Petrochemicals, Power Generation, Mining, Food and Beverage, and More), Pump Orientation (Submersible, and Surface), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific dominated with 44.85% revenue in 2025 after decades of industrial build-out, extensive municipal upgrades, and policy-driven manufacturing localization. New ethylene cracker complexes in Fujian and large-scale desalination schemes in Australia magnified the procurement of high-efficiency multistage pumps. China's stimulus for wastewater reuse and India's Production Linked Incentive program for chemicals continued to channel orders toward both global and domestic pump manufacturers. Regulatory pushes around electricity intensity and carbon footprints incentivized operators to retrofit VFDs, nudging market volume toward premium-efficiency product lines within the industrial pump market.

The Middle East and Africa posted the fastest 6.05% CAGR, propelled by USD 17 billion in combined petrochemical investments across Saudi Arabia, Qatar, and the United Arab Emirates. Desalination, such as NEOM's 1 million m3/day seawater project, demanded high-pressure duplex-steel pumps tolerant to chloride stress-corrosion. African mining expansions in Zambia and the Democratic Republic of Congo increased orders for abrasion-resistant slurry units. Local content frameworks pushed OEMs to open service hubs in Oman and South Africa, shortening turnaround times on overhauls and reinforcing brand loyalty. North America experienced a steady replacement cycle driven by water infrastructure bills, with California, Texas, and Florida aggregating the bulk of tenders for replacement centrifugal and vertical turbine pumps. Energy policy incentives supported early adoption of hydrogen electrolysis, sparking niche orders for corrosion-resistant circulation pumps. Europe's stringent MEI regulations stimulated demand for ultra-high-efficiency designs and encouraged plant owners to reassess total-cost-of-ownership metrics. Latin America, though smaller, witnessed steady uptake in agricultural irrigation pumps and mining-related demand in Chile and Peru. Across all regions, digital service propositions featuring predictive maintenance became a decisive factor in bid evaluations, further shaping competitive standings in the industrial pump market.

- Flowserve Corporation

- Grundfos Holding A/S

- Xylem Inc.

- Sulzer Ltd.

- KSB SE & Co. KGaA

- ITT Inc.

- Ebara Corporation

- The Weir Group PLC

- Schlumberger NV (REDA Pump)

- Baker Hughes Company

- SPX FLOW Inc.

- Wilo SE

- Dover Corporation

- Pentair plc

- Franklin Electric Co. Inc.

- Tsurumi Manufacturing Co. Ltd.

- Kirloskar Brothers Ltd.

- Atlas Copco AB

- Ruhrpumpen Group

- Zoeller Company

- Roto Pumps Ltd.

- Gardner Denver LLC (Ingersoll Rand)

- ClydeUnion Pumps (Celeros Flow Tech)

- LEWA GmbH

- Graco Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising water and waste-water treatment spending globally

- 4.2.2 Expansion of petrochemical capacity in MEA

- 4.2.3 Rapid industrial infrastructure build-out across Asia-Pacific

- 4.2.4 Demand for corrosion-resistant pumps in green-hydrogen electrolyzers

- 4.2.5 Predictive-maintenance IoT service models unlocking aftermarket revenue

- 4.3 Market Restraints

- 4.3.1 Volatility in steel and copper prices inflating TCO

- 4.3.2 Stricter pump-efficiency directives delaying cap-ex cycles

- 4.3.3 Shift to motor-less gravity micro-irrigation systems in arid economies

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Pump Type

- 5.1.1 Centrifugal

- 5.1.2 Reciprocating

- 5.1.3 Rotary

- 5.1.4 Diaphragm

- 5.1.5 Progressing Cavity

- 5.1.6 Others

- 5.2 By Power Source

- 5.2.1 Electric

- 5.2.2 Diesel

- 5.2.3 Solar

- 5.2.4 Hydraulic

- 5.2.5 Pneumatic

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Water and Waste-water

- 5.3.3 Chemicals and Petrochemicals

- 5.3.4 Power Generation

- 5.3.5 Mining

- 5.3.6 Food and Beverage

- 5.3.7 Pharmaceuticals

- 5.3.8 Pulp and Paper

- 5.3.9 Others

- 5.4 By Pump Orientation

- 5.4.1 Submersible

- 5.4.2 Surface

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Taiwan

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Turkey

- 5.5.5.1.2 Israel

- 5.5.5.1.3 GCC Countries

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Flowserve Corporation

- 6.4.2 Grundfos Holding A/S

- 6.4.3 Xylem Inc.

- 6.4.4 Sulzer Ltd.

- 6.4.5 KSB SE & Co. KGaA

- 6.4.6 ITT Inc.

- 6.4.7 Ebara Corporation

- 6.4.8 The Weir Group PLC

- 6.4.9 Schlumberger NV (REDA Pump)

- 6.4.10 Baker Hughes Company

- 6.4.11 SPX FLOW Inc.

- 6.4.12 Wilo SE

- 6.4.13 Dover Corporation

- 6.4.14 Pentair plc

- 6.4.15 Franklin Electric Co. Inc.

- 6.4.16 Tsurumi Manufacturing Co. Ltd.

- 6.4.17 Kirloskar Brothers Ltd.

- 6.4.18 Atlas Copco AB

- 6.4.19 Ruhrpumpen Group

- 6.4.20 Zoeller Company

- 6.4.21 Roto Pumps Ltd.

- 6.4.22 Gardner Denver LLC (Ingersoll Rand)

- 6.4.23 ClydeUnion Pumps (Celeros Flow Tech)

- 6.4.24 LEWA GmbH

- 6.4.25 Graco Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment