|

시장보고서

상품코드

1934630

특수 흑연 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Special Graphite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

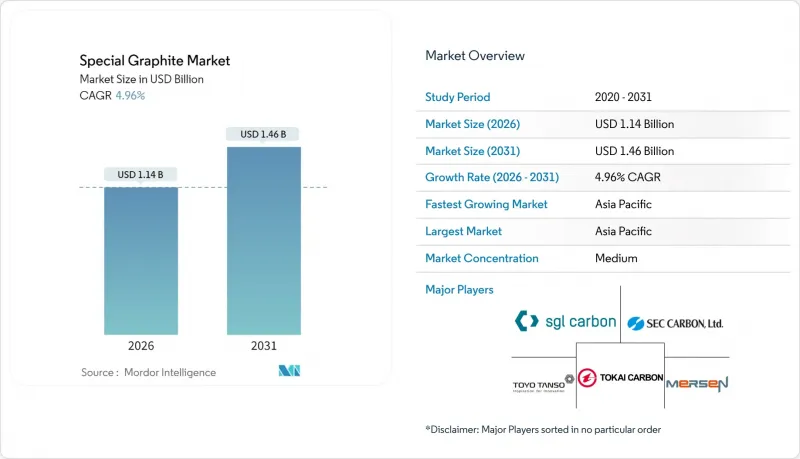

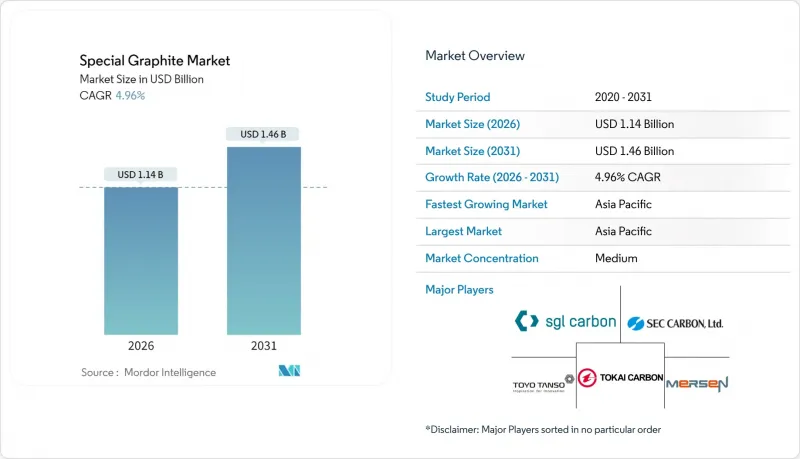

특수 흑연 시장은 2025년에 10억 9,000만 달러로 평가되었고, 2026년 11억 4,000만 달러에서 2031년까지 14억 6,000만 달러에 이를 것으로 예측되고 있습니다.

예측 기간(2026-2031년)의 CAGR은 4.96%로 예상됩니다.

탈탄소화 정책, 태양전지용 웨이퍼 생산량 증가 및 유럽과 미국의 배터리 음극재 국산화가 진행되면서 고순도 등방성 흑연 및 성형품 등급 수요가 기존 강재 전극을 넘어 확대되고 있습니다. 중국이 2024년 천연 플레이크 흑연 수출 허가제를 도입하고, 미국이 2026년 25%의 관세를 부과하기로 한 것은 중국산 이외의 원료에 대한 적격성 평가를 가속화하고, 유럽과 미국의 휴면 상태였던 생산 능력을 재가동하도록 유도하고 있습니다. 복잡한 합금 주조에서 금속 주형에서 흑연 주형으로의 주조소 전환, 반도체 도가니 수요, 태양광 발전의 핫존 소비가 견고한 최종 시장의 다양성을 뒷받침하고 있습니다. 한편, 나트륨 이온화학에 의한 대체 리스크가 장기적인 물량 전망을 억제하고 있습니다. 경쟁 환경에서는 10ppm 미만의 불순물 수준을 보장하고 ISO 9001 및 ISO 14001에 대한 적합성을 제공할 수 있는 공급업체가 우위를 점합니다. 이는 바이어들이 최저 가격보다 원산지를 중시하는 경향이 강해졌기 때문입니다. 전반적으로 특수 흑연 시장은 적당히 통합되어 있지만 기술적으로 차별화되어 있어 유럽, 미국 및 일본의 기존 기업들이 수익성이 높은 틈새 시장을 보호할 수 있는 여지를 남겨두고 있습니다.

세계 특수 흑연 시장 동향 및 인사이트

정부의 탈탄소화 정책으로 태양전지 웨이퍼 수요 증가 견인

넷 제로 달성을 위한 로드맵은 기가 와트 규모의 태양광 발전 확대로 이어지고 있으며, 설치 기가 와트당 180-220톤의 고순도 흑연 도가니 및 핫존 부품을 소비하고 있습니다. 유럽연합(EU)은 2030년까지 750기가와트를 목표로 하고 있으며, 연간 3만톤 이상의 흑연이 추가 수요로 발생합니다. 한편, 중국의 '14차 5개년 계획'은 같은 해까지 풍력과 태양광을 합해 1,200기가와트의 설비용량을 의무화하고 있습니다. 인도의 2024년 태양광 모듈 생산 연동형 인센티브(PLI)는 지역 내 소모품 수요를 더욱 확대할 것입니다. 정책적으로 뒷받침되는 조달주기를 통해 공급업체는 다년간 수요량을 예측할 수 있고, 설비투자의 정당성을 확보할 수 있기 때문에 이 수요 요인은 철강 사이클 특유의 변동에 영향을 덜 받는 특성을 가지고 있습니다.

미국 및 유럽 연합의 전기차 배터리 현지화가 특수 흑연 수요 증가를 주도하고 있습니다.

인플레이션 억제법에 따라 2027년까지 중국산 배터리 재료의 보조금 대상 제외가 규정됨에 따라 비 중국산 흑연 프로젝트가 속속 등장하고 있습니다. 누보몬드 그라파이트는 제너럴 모터스와 파나소닉 에너지로부터 5,000만 달러의 자금 조달에 성공했으며, 퀘벡 주에서 연간 36,000톤의 플레이크 흑연을 공급하고 있습니다. 또한, 파나소닉은 노보닉스 테네시 공장에서 연간 1만 톤의 합성 흑연을 계약했습니다. 유럽의 중요원료법(2023년 시행)은 2030년까지 40%의 국내 가공을 의무화하고 있으며, 이에 따라 메르센은 미국 내 등방성 흑연 생산능력을 연간 16,000톤으로 확대했습니다. 현재 유럽과 미국의 배터리 제조업체들은 추적 가능한 원재료에 대해 20-30%의 가격 프리미엄을 감수하고 있으며, 수익률은 인증된 공급업체로 이동하고 있습니다.

중국 중심의 원료 플레이크 공급 집중으로 조달 리스크 증가

2024년 중국의 천연흑연 채굴량은 전 세계 77%를 차지했고, 음극용 정련량은 90% 이상을 차지했습니다. 2023년 12월 수출 허가 규제로 인해 일시적으로 출하가 제한되어 공급망의 취약성이 드러났습니다. 모잠비크의 바라마에서 캐나다의 락 데 일까지 비 중국 프로젝트는 자금 조달 문제와 12-18개월의 고객 인증 주기에 직면하고 있으며, 이는 유럽과 미국 가격에 15-20%의 위험 프리미엄을 포함시켜 재고를 쌓아두게 하고 있습니다.

부문 분석

등방성 흑연은 2025년 특수 흑연 시장의 47.90%를 차지하며 반도체 도가니, 방전 가공 전극, 그린 수소 플레이트 수요에 힘입어 CAGR 5.44%로 성장하고 있습니다. 메르센은 웨이퍼 공장용 미국 생산능력을 16,000톤으로 늘리고, 프라운호퍼 연구소의 바이폴라 플레이트 기술 혁신으로 연간 3만톤 수요 증가가 예상됩니다. 전극과 연속 주조용 금형에 사용되는 압출 흑연은 토카이카본이 2025년 7월까지 일본 전극 생산량을 50%, 유럽을 30% 줄임에 따라 구조적인 과잉 생산 능력에 직면해 있습니다. 성형 흑연은 중동의 알루미늄 제련 확대에 따라 성장하고 있으며, 플렉서블 호일 제품은 EV용 열관리 개스킷 수요에 대응하고 있습니다. 불순물 함량 10ppm 이하를 달성한 공급업체는 다년간의 판매 계약을 체결하여 철강 수요의 주기적 변동으로부터 수익을 보호할 수 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 45.70%를 차지할 것으로 예상되며, 예측 기간(2026-2031년) 동안 6.42%의 성장률을 나타낼 것으로 예측됩니다. 중국은 업스트림 채굴 및 정제를 주도하고 있지만, 일본은 국내 전극 수요 감소에 따라 미세 탄소 부품으로 주력 분야를 전환했습니다. 한편, 한국은 포스코퓨처엠을 통해 모잠비크산 플레이크 확보를 추진하고 있습니다. 인도의 태양광 모듈 생산 연동형 보조금 제도(PLI)가 태양광 모듈에 대한 수요를 자극하여 국내 가공업체에 기회를 창출하고 있습니다.

북미는 특수 흑연 시장에서 큰 비중을 차지하고 있습니다. 비달리아의 1만 1,300톤 규모의 구형 흑연 공장과 빌라 카본의 10억 달러 규모의 사우스캐롤라이나주 프로젝트는 인플레이션 억제법에 따른 후폭풍을 보여주고 있습니다. 2026년 중국산 흑연에 대한 관세가 25%로 인상되는 점과 기가팩토리 건설의 물결이 지역 성장을 뒷받침하고 있지만, 12-18개월의 인증 기간이 장벽으로 작용하고 있습니다.

유럽의 점유율은 반도체, 자동차, 재생에너지 설비가 주도하고 있습니다. SGL 카본의 반도체 매출 30% 증가는 중국의 비용 압박으로 인한 음극재 연구개발에서 철수한 것과는 대조적입니다. REACH 분진 규제는 컴플라이언스 비용을 증가시키지만, 중요원료법은 국내 가공을 촉진하고 있습니다.

남미와 중동 및 아프리카은 원료 플레이크와 알루미늄 제련용 음극을 공급하고 있지만, 인프라 부족으로 인해 단기적인 확장을 억제하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The Special Graphite Market was valued at USD 1.09 billion in 2025 and estimated to grow from USD 1.14 billion in 2026 to reach USD 1.46 billion by 2031, at a CAGR of 4.96% during the forecast period (2026-2031).

Decarbonization policies, solar-wafer build-outs, and Western battery-anode localization are expanding high-purity isotropic and molded grades beyond traditional steel electrodes. China's 2024 export-license regime for natural flake and the 25% United States tariff set for 2026 are accelerating the qualification of non-Chinese feedstocks and the restarts of dormant Western capacity. Foundry migration from metal to graphite molds in complex-alloy casting, semiconductor crucible demand, and photovoltaic hot-zone consumption underpin resilient end-market diversity, while substitution risks from sodium-ion chemistries temper longer-range volume expectations. Competitive dynamics favor suppliers who can certify sub-10-ppm impurity levels and offer ISO 9001 and ISO 14001 compliance, as buyers increasingly emphasize provenance over the lowest cost. Overall, the special graphite market remains moderately consolidated yet technically differentiated, giving Western and Japanese incumbents scope to defend high-margin niches.

Global Special Graphite Market Trends and Insights

Government Decarbonization Policies Boosting Solar Wafer Demand

Net-zero roadmaps are translating into gigawatt-scale photovoltaic expansions that consume high-purity graphite crucibles and hot-zone parts at 180-220 t per installed gigawatt. The European Union targets 750 GW by 2030, adding more than 30,000 t of graphite annually, while China's 14th Five-Year Plan mandates 1,200 GW of combined wind and solar capacity by the same year. India's 2024 production-linked incentive for solar modules further amplifies localized consumable demand. Policy-locked procurement cycles give suppliers multi-year volume visibility and justify capacity investments, insulating this driver from typical steel-cycle volatility.

EV Battery Localization in United States and European Union Sparking Specialty Graphite Offtake

Inflation Reduction Act rules phasing out Chinese battery materials from subsidies by 2027 have triggered non-Chinese graphite projects. Nouveau Monde Graphite secured USD 50 million from General Motors and Panasonic Energy to supply 36,000 t/yr of flake from Quebec, and Panasonic additionally contracted 10,000 t/yr of synthetic graphite from Novonix's Tennessee plant. Europe's Critical Raw Materials Act, effective 2023, compels 40% domestic processing by 2030, prompting Mersen to raise US isotropic capacity to 16,000 t/yr. Western cell makers now accept 20-30% price premiums for traceable feedstocks, shifting margin to certified suppliers.

Sino-Centric Raw-Flake Supply Concentration Raising Procurement Risk

China mined 77% of global natural graphite and refined over 90% of anode-grade output in 2024. December 2023 export license controls briefly curbed shipments, revealing supply chain fragility. Non-Chinese projects-from Mozambique's Balama to Canada's Lac des Iles-face financing challenges and 12-18-month customer-qualification cycles, which embed a 15-20% risk premium into Western pricing and incentivize inventory stockpiling.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Large-Format Si-Rich Anodes Requiring Higher-Purity Graphite

- Foundry Migration from Metal Molds to Graphite Molds for Complex Alloys

- Breakthroughs in Lithium Titanium Oxide and Sodium-Ion Chemistries Reducing Graphite Intensity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Isotropic graphite held 47.90% of the special graphite market share in 2025 and is growing at a 5.44% CAGR, fueled by semiconductor crucibles, EDM electrodes, and green-hydrogen plates. Mersen lifted US capacity to 16,000 t to serve wafer fabs, and Fraunhofer's bipolar-plate breakthrough could add 30,000 t annual demand. Extruded graphite, used in electrodes and continuous-casting molds, faces structural overcapacity after Tokai Carbon's 50% Japanese and 30% European electrode cuts by July 2025. Molded graphite grows alongside Middle East aluminum smelting, while flexible foils address thermal management gaskets in EVs. Suppliers achieving sub-10-ppm impurity win multiyear offtakes, insulating revenue from cyclical steel swings.

The Special Graphite Market Report is Segmented by Product Type (Extruded Graphite, Isotropic Graphite, Molded Graphite, and Other Types), End-User Industry (Electronics, Photovoltaic, Foundry and Metallurgy, and Other End-Users), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region dominated 45.70% of 2025 revenue and is expected to grow at a rate of 6.42% during the forecast period (2026-2031). China anchors upstream mining and refining, yet Japan shifts focus to fine-carbon parts after domestic electrode cuts, while South Korea secures Mozambican flake via Posco Future M. India's PLI scheme for solar modules stimulates crucible demand and domestic fabricator opportunities.

North America captures a substantial share of the special graphite market. Vidalia's 11,300 t spherical plant and Birla Carbon's USD 1 billion South Carolina project illustrate Inflation Reduction Act tailwinds. Tariffs rising to 25% on Chinese graphite in 2026 and a wave of gigafactory construction underpin regional growth, though 12-18-month qualification timelines remain a hurdle.

Europe's share, driven by semiconductor, automotive, and renewable installations. SGL Carbon's 30% jump in semiconductor sales contrasts with its exit from anode R&D due to Chinese cost pressure. REACH dust rules raise compliance costs, yet the Critical Raw Materials Act pushes domestic processing.

South America and the Middle East & Africa supply raw flake and aluminum-smelting cathodes but face infrastructure gaps that temper near-term expansion.

- Entegris, Inc.

- Fangda Carbon New Material Co. Ltd

- GrafTech International

- Graphite India Limited

- MERSEN PROPERTY

- Morgan Advanced Materials Plc

- Nippon Carbon Co. Ltd

- Pingdingshan City Kaiyuan Specialty Graphite Ltd

- Schunk Carbon Technology

- SEC CARBON, Limited

- SGL Carbon

- Tokai Carbon Co., Ltd.

- Toyo Tanso Co., Ltd.

- Yichang Xincheng Graphite Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government decarbonisation policies boosting solar wafer demand

- 4.2.2 EV-battery supply-chain localisation in United States and European Union sparking specialty graphite offtake

- 4.2.3 Shift to large-format Si-rich anodes that require higher-purity graphite

- 4.2.4 Foundry migration from metal molds to graphite molds for complex alloys

- 4.2.5 Rapid expansion of green-hydrogen electrolyser plates using isostatic graphite

- 4.3 Market Restraints

- 4.3.1 Sino-centric raw-flake supply concentration raises procurement risk

- 4.3.2 Breakthroughs in Lithium Titanium Oxide (LTO ) and sodium-ion chemistries reducing graphite intensity

- 4.3.3 Stricter EU REACH limits on graphite dust emissions increase CAPEX

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Extruded Graphite

- 5.1.2 Isotropic Graphite

- 5.1.3 Molded Graphite

- 5.1.4 Other Types

- 5.2 By End-user Industry

- 5.2.1 Electronics Industry

- 5.2.2 Photovoltaic Industry

- 5.2.3 Foundry and Metallurgy Industry

- 5.2.4 Other End-Users

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 South Korea

- 5.3.1.4 India

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Entegris, Inc.

- 6.4.2 Fangda Carbon New Material Co. Ltd

- 6.4.3 GrafTech International

- 6.4.4 Graphite India Limited

- 6.4.5 MERSEN PROPERTY

- 6.4.6 Morgan Advanced Materials Plc

- 6.4.7 Nippon Carbon Co. Ltd

- 6.4.8 Pingdingshan City Kaiyuan Specialty Graphite Ltd

- 6.4.9 Schunk Carbon Technology

- 6.4.10 SEC CARBON, Limited

- 6.4.11 SGL Carbon

- 6.4.12 Tokai Carbon Co., Ltd.

- 6.4.13 Toyo Tanso Co., Ltd.

- 6.4.14 Yichang Xincheng Graphite Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment