|

시장보고서

상품코드

1934639

클라우드 마이그레이션 서비스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cloud Migration Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

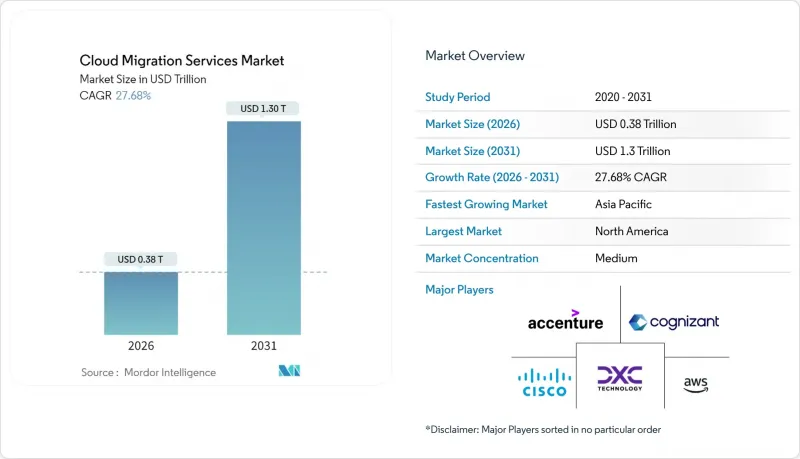

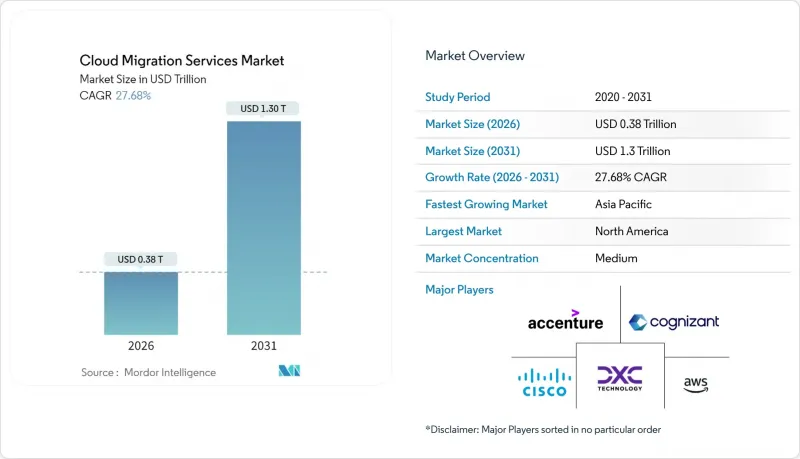

클라우드 마이그레이션 서비스 시장은 2025년에 3,000억 달러로 평가되었고, 2026년 3,830억 4,000만 달러에서 2031년까지 1조 2,994억 8,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 27.68%로 예상됩니다.

이러한 빠른 성장은 기업들이 자본 집약적인 On-Premise 자산에서 빠른 혁신 주기와 우수한 비용 관리를 가능하게 하는 확장 가능한 클라우드 환경으로 전환하고 있는 현실을 반영합니다. 이러한 모멘텀은 생성형 AI 워크로드의 가속화, 하이브리드 전략의 확대, 클라우드 네이티브 아키텍처에 유리한 Scope 3 탄소 보고 의무 증가로 인해 더욱 가속화되고 있습니다. 퍼블릭 클라우드는 여전히 선도적인 위치를 유지하고 있지만, 기업이 성능과 컴플라이언스, 비용 최적화라는 목표의 균형을 맞추기 위해 하이브리드 패턴이 부상하고 있습니다. 대기업이 가장 큰 지출 주체이지만, 자동화된 마이그레이션 툴체인을 통한 기술 장벽의 감소로 중소기업(SME)의 지출 규모도 점차 줄어들고 있습니다. 산업별로는 은행, 금융 서비스 및 보험(BFSI), 의료 분야가 도입을 주도하고 있으며, 벤더 종속성 및 데이터 전송 수수료에 대한 우려가 지속되는 가운데, 하이퍼스케일 제공업체와 틈새 전문 업체들이 서비스 포트폴리오를 계속 확장하고 있습니다.

세계 클라우드 마이그레이션 서비스 시장 동향과 인사이트

클라우드 도입으로 인한 비용 효율성과 확장성의 이점

클라우드로 워크로드를 이전한 기업들은 자본 집약적인 하드웨어 업데이트 주기를 없애고 온디맨드 리소스를 적절히 활용함으로써 운영 비용을 20-30% 절감하고 있습니다. 인포마트의 B2B 플랫폼을 Oracle 클라우드 인프라로 전환한 사례에서는 데이터센터 비용을 38% 절감하고, 성능 유연성을 향상시켰습니다. 탄력적인 리소스 프로비저닝을 통해 조직은 물리적 데이터센터 환경에서 흔히 발생하는 6-12개월의 조달 지연 없이 예상치 못한 수요 급증에 대응할 수 있습니다. 인프라 유지관리에서 해방된 예산은 경쟁적 차별화를 강화하는 혁신 시책에 점점 더 많이 투입되고 있습니다. 이러한 누적된 이점으로 인해 비용 합리화 전략은 예측 CAGR에 가장 큰 긍정적인 영향을 미치고 있습니다.

원격근무와 BYOD 확산

하이브리드 업무 모델이 정착됨에 따라 조직은 협업 스위트, ID 서비스, 보안 제어를 클라우드로 이전하여 장소와 디바이스에 관계없이 일관된 사용자 경험을 보장해야 하는 상황에 직면해 있습니다. 최근 조사에 따르면, IT 리더의 89%가 분산된 팀을 지원하기 위해 2025년에 클라우드 지출을 늘릴 의향이 있다고 답했습니다. BYOD는 경계 보안을 복잡하게 만들고, 클라우드 네이티브 형태로 도입이 용이한 제로 트러스트 아키텍처로 전환을 유도하고 있습니다. 그 결과, 보안 액세스 서비스 엣지, 엔드포인트 관리, 실시간 분석 레이어가 점점 더 많이 포함되고 있으며, 모든 위치에서 직원의 생산성을 유지할 수 있도록 지원합니다. 이러한 추세는 특히 북미와 유럽에서 프로젝트 파이프라인에 단기적으로 강한 견인력을 발휘하고 있습니다.

데이터 보안 및 규제 준수 리스크

유럽 기업들은 일반개인정보보호규정(GDPR(EU 개인정보보호규정))의 규정과 퍼블릭 클라우드 서비스 모델과의 정합성에 대해 고민하고 있습니다. 한편, 전 세계 금융기관은 클라우드 데이터 흐름을 명시적으로 규정하지 않는 중복된 관할권의 규정에 대응해야 합니다. 책임 분담 모델에서는 암호화, 로그 기록, 사고 대응에 대한 책임 소재가 불분명한 경우가 많습니다. 경우에 따라 소버린 클라우드 요구 사항으로 인해 조직은 현지화된 용량에 대한 추가 비용을 지불하거나 On-Premise 인프라를 유지해야 하며, 마이그레이션 일정이 연장될 수 있습니다. 이러한 요인들은 거의 모든 산업, 특히 의료, 은행, 정부 기관에서 성장을 억제하고 있습니다.

부문 분석

하이브리드 구축이 가장 빠르게 성장하고 있으며, 기업들이 저지연 On-Premise 수요와 퍼블릭 클라우드의 확장성을 동시에 충족시키면서 18.35%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 퍼블릭 클라우드는 하이퍼스케일 사업자의 성숙한 보안 체계로 인해 여전히 클라우드 마이그레이션 서비스 시장의 54.82%를 차지하고 있습니다. 엣지 클라우드 통합을 통해 탄력적인 백엔드 분석 연결성을 유지하면서 컴퓨팅을 사용자에게 더 가까이 가져가는 움직임이 진행되고 있으며, 향후 아키텍처는 단일 워크플로우 내에서 여러 실행 환경을 통합하는 방향으로 나아가고 있습니다. 이러한 노드 간 워크로드 배치를 조정할 수 있는 마이그레이션 전문가에 대한 수요는 여전히 높은 수준입니다.

기업들은 더 이상 배포를 양자택일의 문제로 보지 않습니다. 금융기관들은 밀리초 미만의 대기시간을 위해 거래 엔진을 프라이빗 클러스터에 배치하고, 규제 보고 업무는 비용 효율적인 퍼블릭 버킷에 오프로드하여 처리하고 있습니다. 의료기관은 영상 데이터를 로컬에서 처리한 후, 익명화된 데이터를 클라우드의 AI 파이프라인으로 라우팅합니다. 이러한 미묘한 설계도 덕분에 하이브리드 옵션이 클라우드 마이그레이션 서비스 시장에서 지속적으로 입지를 넓혀가고 있는 이유를 알 수 있습니다.

2025년 기준 클라우드 마이그레이션 서비스 시장 규모에서 대기업이 61.20%를 차지하고 있습니다. 이는 다년간의 혁신 예산과 전 세계 전개가 반영된 결과입니다. 반면, 중소기업은 17.65%의 연평균 복합 성장률(CAGR)을 보이고 있으며, 설정 시간을 단축하고 전문 지식의 장벽을 낮추는 패키지화된 마이그레이션 툴체인이 이를 주도하고 있습니다. 클라우드 제공업체들은 현재 포춘지 선정 500대 기업 대상의 풍부한 컨설팅과 중소기업 대상의 절차서 템플릿으로 제공 내용을 구분하여, 수익률 저하 없이 대응 가능한 수요를 확대하고 있습니다.

중소기업은 고비용의 사내 운영팀을 피하기 위해 SaaS 대체 솔루션이나 매니지드 서비스를 선택하는 경향이 있습니다. 반면, 대기업은 수십 개의 사업부문에 걸쳐 단계적으로 재구축을 추진하고, 거버넌스 및 보안 청사진을 체계화하는 전문 팀(Center of Excellence)을 기반으로 하는 경우가 많습니다. 이러한 양극화로 인해 벤더는 각 고객층의 예산 주기 및 컴플라이언스 요구사항에 따라 차별화된 영업 전략을 유지해야 합니다.

지역별 분석

북미는 2025년 지출의 37.10%를 차지할 것으로 예상되며, 현재 AI 최적화 및 멀티 클라우드 비용 거버넌스에 집중하는 초기 도입 기업이 주도하고 있습니다. 미국은 83억 달러의 현대화 예산 등 연방정부 클라우드 프로그램을 주도하고 있으며, 캐나다와 멕시코는 강화된 네트워크 인프라를 활용해 도입을 가속화하고 있습니다. 지역 전체적으로 예측형 워크로드 배치 엔진의 통합으로 소비 모델 정교화 및 데이터 전송 비용 절감이 진행되면서 북미가 클라우드 마이그레이션 서비스 시장의 핵심으로 자리매김하고 있습니다.

아시아태평양은 국가 차원의 디지털 혁신 기금과 하이퍼스케일러 투자에 힘입어 2031년까지 18.15%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 마이크로소프트는 일본 데이터센터 확장에 29억 달러를 배정하여 일본의 클라우드 발전 궤도에 대한 확신을 보여주었습니다. 인도는 BFSI(은행, 금융, 보험), 소매, 정부 부문의 광범위한 현대화를 배경으로 2028년까지 255억 달러 규모의 클라우드 시장이 형성될 것으로 예측됩니다. 중국에서는 데이터 현지화 규제에 힘입어 국내 업체들이 맞춤형 주권형 서비스를 통해 시장 점유율을 지속적으로 확대하고 있습니다. 이 지역의 다양한 규제 환경은 하이브리드 클라우드와 멀티 클라우드 설계에 대한 다양한 규제 환경을 형성하고 있으며, 이에 대응해야 하는 기업들은 하이브리드 클라우드와 멀티 클라우드 설계의 패치워크를 형성하고 있습니다.

유럽에서는 꾸준한 성장과 엄격한 데이터 주권 관리가 병행되고 있습니다. 독일과 영국이 가장 큰 도입 국가인 반면, 프랑스와 스페인은 국내 벤더를 강화하는 주권적 클라우드 프레임워크를 추진하고 있습니다. GDPR(EU 개인정보보호규정) 시행으로 모든 프로젝트에서 세심한 데이터 거주지 매핑과 암호화 거버넌스가 요구되고 있습니다. 그 결과, 기밀성이 높은 워크로드는 국내에 두고, 분석 및 AI 작업은 확장성이 높은 리전 노드를 활용하는 하이브리드 전략이 주류를 이루고 있습니다. 이러한 추세로 인해, 예측 기간 동안 유럽의 마이그레이션 프로파일은 컴플라이언스 우선 아키텍처와 밀접하게 연관된 상태로 유지될 것입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The cloud migration services market was valued at USD 300 billion in 2025 and estimated to grow from USD 383.04 billion in 2026 to reach USD 1299.48 billion by 2031, at a CAGR of 27.68% during the forecast period (2026-2031).

This rapid upside reflects how enterprises are shifting from capital-intensive on-premises assets toward scalable cloud environments that permit faster innovation cycles and superior cost control. Momentum is fueled by generative-AI workload acceleration, expanding hybrid strategies, and mounting Scope-3 carbon-reporting obligations that favor cloud-native architectures. Public cloud keeps its leadership position, yet hybrid patterns are gaining ground as firms work to balance performance with compliance and cost-optimization goals. Large enterprises remain the biggest spenders, but small and medium enterprises (SMEs) are closing the gap as automated migration toolchains lower technical barriers. Across industries, Banking, Financial Services and Insurance (BFSI) and Healthcare are pacing adoption, while hyperscale providers and niche specialists continue to broaden service portfolios amid vendor-lock-in and egress-fee concerns.

Global Cloud Migration Services Market Trends and Insights

Cost-efficiency and Scalability Advantages of Cloud Adoption

Enterprises continue to realize 20-30% operational-expenditure savings after moving workloads to the cloud, primarily by eliminating capital-intensive hardware refresh cycles and right-sizing resources on demand. Infomart's business-to-business platform migration to Oracle Cloud Infrastructure cut data-center costs by 38% while boosting performance flexibility. Elastic resource provisioning now allows organizations to handle unexpected demand spikes without the six-to-twelve-month procurement delays common in physical data-center environments. Budget freed from infrastructure upkeep is increasingly redirected toward innovation initiatives that sharpen competitive differentiation. These cumulative benefits give cost-rationalization strategies the highest positive impact on the forecast CAGR.

Rising Remote-work and BYOD Penetration

Hybrid work models have solidified, prompting organizations to migrate collaboration suites, identity services and security controls to the cloud to guarantee consistent user experiences across locations and devices. A recent survey shows 89% of IT leaders intend to raise cloud spending in 2025 to support distributed teams. BYOD complicates perimeter security, steering enterprises toward zero-trust architectures that are easier to enforce in cloud-native form. Consequently, migrations increasingly encompass secure access service edge, endpoint management and real-time analytics layers that maintain workforce productivity from any location. This trend exerts a strong, near-term pull on project pipelines, particularly in North America and Europe.

Data-security and Regulatory-compliance Risks

European firms struggle to reconcile General Data Protection Regulation (GDPR) stipulations with public-cloud service models, while global financial institutions juggle overlapping jurisdictional rules that rarely address cloud data flows explicitly. The shared-responsibility model often blurs accountability for encryption, logging and incident response. In some cases, sovereign-cloud requirements force organizations to pay premiums for localized capacity or retain on-premises infrastructure, extending migration timelines. These factors temper growth across nearly every industry, especially healthcare, banking and government.

Other drivers and restraints analyzed in the detailed report include:

- Government Digital-transformation Funding

- Proliferation of Hybrid / Multi-cloud Strategies

- Legacy-application Complexity and Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments are the fastest riser, advancing at an 18.35% CAGR as enterprises balance low-latency on-premises demands with public-cloud scale. Public cloud still holds 54.82% cloud migration services market share due to the mature security posture of hyperscale providers. Edge-cloud integrations now push compute closer to the user while maintaining elastic backend analytics connectivity, signaling that future architectures will combine multiple execution venues within a single workflow. Migration specialists able to orchestrate workload placement across these nodes remain in high demand.

Enterprises no longer view deployment as a binary choice. Financial institutions position trading engines on private clusters for sub-millisecond latency while offloading regulatory reporting to cost-efficient public buckets. Healthcare groups process imaging data on-site, then route anonymized sets to AI pipelines in the cloud. These nuanced blueprints underline why hybrid options will keep expanding their footprint within the cloud migration services market.

Large enterprises accounted for 61.20% of cloud migration services market size in 2025, reflecting multi-year transformation budgets and global rollouts. Yet SMEs exhibit an 17.65% CAGR, propelled by packaged migration toolchains that cut setup time and lower expertise thresholds. Cloud providers now segment offerings-white-glove consulting for Fortune 500 clients versus prescriptive templates for smaller firms-thereby widening addressable demand without eroding margins.

SMEs gravitate toward SaaS replacements and managed services to avoid staffing expensive in-house operations teams. Conversely, large entities pursue phased re-architecting across dozens of business units, often underpinned by center-of-excellence teams that codify governance and security blueprints. This bifurcation requires service vendors to maintain differentiated go-to-market motions tailored to each cohort's budget cycles and compliance obligations.

The Cloud Migration Services Market Report is Segmented by Deployment Type (Public Cloud, and More), Enterprise Size (Small and Medium Enterprises, and More), Service Type (IaaS, Paas, Saas), Migration Approach (Lift-And-Shift, Re-Platform, Refactor/Re-architect, Replace), End-User Vertical (BFSI, Healthcare, Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 37.10% of 2025 spend, anchored by early adopters that now focus on AI optimization and multi-cloud cost governance. The United States leads through federal cloud programs such as the USD 8.3 billion modernization budget, while Canada and Mexico leverage improved network backbones to accelerate adoption. Across the region, organizations are integrating predictive workload placement engines to refine consumption models and curb egress charges, reinforcing North America's position at the core of the cloud migration services market.

Asia-Pacific is projected to post an 18.15% CAGR to 2031, propelled by state-level digital-transformation funds and hyperscaler investments. Microsoft earmarked USD 2.9 billion for data-center expansion in Japan, demonstrating confidence in Japan's cloud trajectory. India is on course for a USD 25.5 billion cloud sector by 2028, reflecting widespread modernization across BFSI, retail and government. China's domestic providers, supported by data-localization rules, continue to grow market share via tailored sovereign offerings. The region's diverse regulatory landscape shapes a patchwork of hybrid and multi-cloud designs that migration firms must navigate.

Europe pairs steady growth with stringent data-sovereignty controls. Germany and the United Kingdom remain the largest adopters, yet France and Spain are championing sovereign-cloud frameworks that bolster domestic vendors. GDPR enforcement compels meticulous residency mapping and encryption governance across every project. Consequently, hybrid strategies dominate, allowing sensitive workloads to stay on national soil while analytics and AI tasks harness scalable regional nodes. This dynamic will keep Europe's migration profile firmly tied to compliance-first architectures throughout the forecast period.

- Accenture plc

- Amazon Web Services Inc.

- Cisco Systems Inc.

- Cognizant Technology Solutions Corporation

- DXC Technology Company

- Evolve IP LLC

- Google LLC

- International Business Machines Corporation (IBM)

- Microsoft Corporation

- Oracle Corporation

- Rackspace Technology Inc.

- Flexera Software LLC (RightScale)

- Tech Mahindra Limited

- VMware Inc.

- WSM International LLC

- Infosys Limited

- HCL Technologies Limited

- Capgemini SE

- Atos SE

- Fujitsu Limited

- Alibaba Cloud (Alibaba Group Holding Limited)

- Kyndryl Holdings Inc.

- Tata Consultancy Services Limited

- NTT Data Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-efficiency and scalability advantages of cloud adoption

- 4.2.2 Rising remote-work and BYOD penetration

- 4.2.3 Government digital-transformation funding

- 4.2.4 Proliferation of hybrid / multi-cloud strategies

- 4.2.5 Generative-AI workload acceleration of refactoring

- 4.2.6 Scope-3 reporting pushes carbon-aware migrations

- 4.3 Market Restraints

- 4.3.1 Data-security and regulatory-compliance risks

- 4.3.2 Legacy-application complexity and interoperability

- 4.3.3 Escalating cloud-egress fees impact TCO

- 4.3.4 Vendor lock-in fears amid sovereign-cloud mandates

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macro-Economic Factors

- 4.8 Investment Analysis

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.1.4 Multi-Cloud

- 5.2 By Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Service Type

- 5.3.1 Infrastructure-as-a-Service (IaaS)

- 5.3.2 Platform-as-a-Service (PaaS)

- 5.3.3 Software-as-a-Service (SaaS)

- 5.4 By Migration Approach

- 5.4.1 Lift-and-Shift (Re-hosting)

- 5.4.2 Re-platform

- 5.4.3 Refactor / Re-architect

- 5.4.4 Replace (SaaS Substitution)

- 5.5 By End-user Vertical

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Retail and E-commerce

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecommunication

- 5.5.6 Manufacturing

- 5.5.7 Energy and Utilities

- 5.5.8 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 UAE

- 5.6.5.1.3 Turkey

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Amazon Web Services Inc.

- 6.4.3 Cisco Systems Inc.

- 6.4.4 Cognizant Technology Solutions Corporation

- 6.4.5 DXC Technology Company

- 6.4.6 Evolve IP LLC

- 6.4.7 Google LLC

- 6.4.8 International Business Machines Corporation (IBM)

- 6.4.9 Microsoft Corporation

- 6.4.10 Oracle Corporation

- 6.4.11 Rackspace Technology Inc.

- 6.4.12 Flexera Software LLC (RightScale)

- 6.4.13 Tech Mahindra Limited

- 6.4.14 VMware Inc.

- 6.4.15 WSM International LLC

- 6.4.16 Infosys Limited

- 6.4.17 HCL Technologies Limited

- 6.4.18 Capgemini SE

- 6.4.19 Atos SE

- 6.4.20 Fujitsu Limited

- 6.4.21 Alibaba Cloud (Alibaba Group Holding Limited)

- 6.4.22 Kyndryl Holdings Inc.

- 6.4.23 Tata Consultancy Services Limited

- 6.4.24 NTT Data Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment