|

시장보고서

상품코드

1934661

CMOS 이미지 센서 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)CMOS Image Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

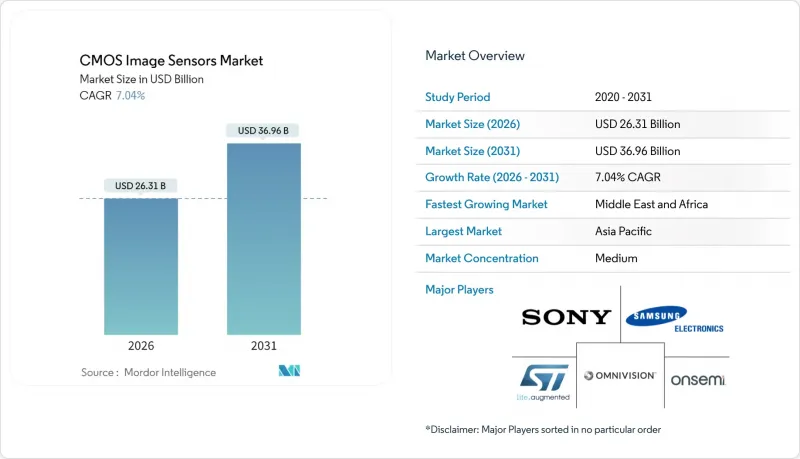

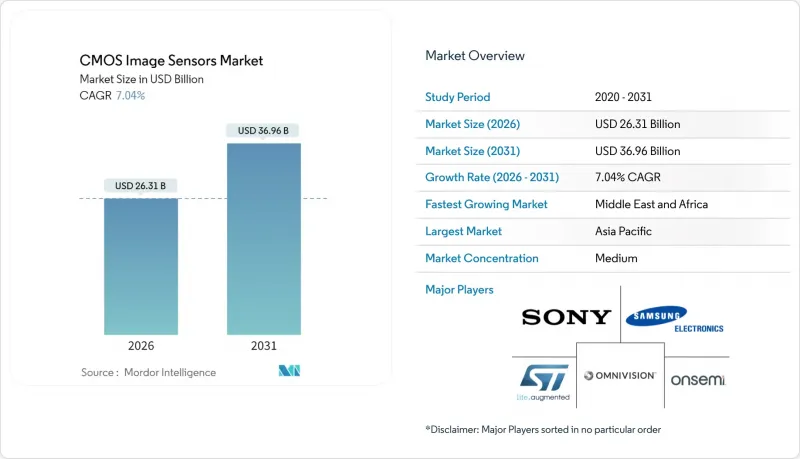

CMOS 이미지 센서 시장은 2025년 245억 8,000만 달러에서 2026년에는 263억 1,000만 달러로 성장하고, 2026-2031년 CAGR 7.04%로 성장을 지속하여, 2031년에는 369억 6,000만 달러에 이를 것으로 예측됩니다.

수요는 스마트폰 카메라에서 자동차 안전, 산업 자동화, 의료 진단으로 확대되고 있으며, 이는 CCD 설계에 대한 본 기술의 기능적 우위를 반영하고 있습니다. 온다이 AI 로직을 내장한 적층형 후면조사형(BSI) 아키텍처는 전력 소비를 줄이면서 성능을 향상시켜 대량 생산 전자기기에서 CMOS 이미지 센서 시장의 비용 우위를 강화하고 있습니다. 지역별로는 아시아태평양이 대만의 파운더리를 기반으로 생산을 뒷받침하는 가운데, 중동 및 아프리카이 스마트시티 모니터링 시스템 도입 확대로 두 자릿수 성장률을 기록하며 추월하고 있습니다. 미국-중국 수출 규제와 300mm 웨이퍼 부족으로 인한 공급망 리스크에도 불구하고, 기존 업체들의 생산능력 매각과 전문업체 인수가 가속화되면서 업계 재편이 진행되고 있습니다.

세계 CMOS 이미지 센서 시장 동향 및 인사이트

아시아태평양 OEM 업체들의 스마트폰 멀티 카메라 탑재 현황과 전망

아시아태평양의 휴대폰 제조업체들은 플래그십 모델에서 미드레인지 라인까지 멀티 카메라 어레이를 확대 적용하고 있으며, 이는 하이 다이내믹 레인지 이미지 센서의 지속적인 유닛 성장을 견인하고 있습니다. 삼성이 2024년에 발표한 2억 화소와 5,000만 화소의 ISOCELL 디바이스는 계산 사진 기술과 고프레임 레이트 동영상으로의 전환을 명확히 보여줍니다. 옴니비전의 OV50X(110dB 단노출 HDR 지원)는 프리미엄 스마트폰이 화소수뿐만 아니라 센서 성능으로 차별화를 꾀하고 있는 현 상황을 잘 보여주고 있습니다. 소니 LYT-828은 2025년 양산 개시 예정으로, 하이브리드 프레임 HDR 로직을 내장하여 외부 ISP 사이클이 필요 없는 AI 지원 저조도 처리를 실현합니다. 고화소 밀도와 온센서 연산의 조합은 기능 확장을 지원하고, 동시에 첨단 부품의 평균 판매 가격을 높여 CMOS 이미지 센서 시장의 수익 성장을 강화할 것입니다.

미국 및 유럽의 ADAS 카메라 규제 요건

미국 도로교통안전국(NHTSA)이 2024년 12월에 시행하는 신차 평가 프로그램(NCAP) 개정으로 경차 전 차종에 카메라 기반 사각지대 감지 시스템, 차선 유지 지원 시스템, 자동 긴급 제동 시스템 탑재가 의무화되어 센서의 장기적인 수요를 뒷받침할 것입니다. 전 세계 셔터 구조는 안전성이 매우 중요한 영상 촬영에서 필수적인 모션 아티팩트를 줄여줍니다. 이는 ASIL C 안전 기준을 충족하는 온세미의 Hyperlux AR0823AT 센서를 채택한 스바루의 차세대 EyeSight 시스템에서 두드러지게 나타납니다. EU의 일반 안전 규정은 미국의 요구 사항을 반영하고 있으며, 규격이 동기화됨에 따라 CMOS 파운드리 업체들은 향후 10년간 자동차 등급 생산 능력 투자에 대한 전망을 얻게 되었습니다.

대만과 한국의 첨단 300mm CIS 웨이퍼 생산 능력의 한계

AI 칩 주문이 급증하면서 대만과 한국 파운드리의 첨단 300mm 라인의 이미지센서 생산능력이 부족하여 리드타임이 12-16주에서 20-24주로 연장되고 있습니다. TSMC의 애리조나 확장 계획은 1,650억 달러의 자본을 투자할 예정이지만, 2027년 이전에는 CIS의 병목현상을 크게 완화하지 못할 것입니다. 적층 BSI 제조의 지리적 집중은 지정학적 리스크를 증가시켜 CMOS 이미지 센서 시장의 단기 공급 탄력성을 크게 억제하고 있습니다.

부문 분석

2025년, 후면조사형 센서는 우수한 감도와 높은 S/N비를 반영하여 CMOS 이미지 센서 시장 점유율의 64.40%를 차지하였습니다. 이 부문의 부상으로 프리미엄 스마트폰 및 차량용 카메라용 BSI 기반 CMOS 이미지 센서 시장 규모가 확대되었습니다. 적층형 BSI/3D 센서는 CAGR 9.52%로 발전하고 있으며, AI 추론을 온칩으로 실행하는 로직 레이어를 통합하여 평방 mm당 가치를 더욱 확장하고 있습니다.

전면 조명 방식의 디바이스는 보급형 IoT 카메라 등 비용 제약이 있는 SKU에서 여전히 중요성이 유지되고 있습니다. 전 세계적으로 셔터 아키텍처(대부분 FSI 기반)는 모션 아티팩트를 방지하기 위해 산업 자동화 분야에서 채택이 증가하고 있습니다. 2026년부터 2031년까지 도입이 예상되는 신기술인 유리 기판 3D 적층은 보다 엄격한 열 프로파일과 높은 상호 연결 밀도를 실현하여 하이엔드 제품의 차별화를 확대할 것으로 예측됩니다.

2025년 기준 12-24MP 대역은 CMOS 이미지 센서 시장의 24.60%를 차지하며, 주류 스마트폰의 스토리지와 연산 부하의 균형을 이루고 있습니다. 49MP 이상 기기는 틈새 시장이지만, 감시, 의료, 전문 사진 분야의 극한의 디지털 줌 수요를 바탕으로 연평균 9.23% 성장하고 있습니다. 캐논의 410MP 프로토타입은 풀프레임 초 고밀도 센서의 기술적 실현 가능성을 입증하고 새로운 진단 영상 양식의 창출을 촉진할 수 있습니다.

1,200만 화소 미만의 제품은 프레임 속도가 해상도보다 우선시되는 바코드 스캔 및 드라이브 레코더 분야에서 수요가 지속되고 있습니다. 중간층인 2,500만-4,800만 화소 센서는 멀티 프레임 연산처리를 활용한 미러리스 카메라에 공급되고 있습니다. 화소수 양극화로 인해 CMOS 이미지 센서 시장 전체에서 가격대별 세분화가 진행되어 수익률의 계층화가 유지되고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 33.70%를 차지할 것으로 예상되며, 파운드리 실리콘에서 최종 휴대폰 조립에 이르는 수직적 통합 생태계의 혜택을 누리고 있습니다. 대만 팹이 적층형 BSI 웨이퍼의 대부분을 공급하고 있는 반면, 중국 본토는 세계 최대의 스마트폰 수출 거점입니다. 삼성의 ISOCELL 로드맵을 필두로 한 한국의 기술 혁신은 CMOS 이미지 센서 시장에서 기술 리더십을 유지하고 있습니다. 공급망의 중앙집중화는 규모의 경제를 가져오는 반면, 지진과 지정학적 위험에 대한 노출을 증가시키고 있습니다.

중동 및 아프리카은 2031년까지 연평균 복합 성장률(CAGR) 9.55%로 가장 빠르게 성장할 것으로 예측됩니다. 걸프 국가들의 스마트시티 구상은 네트워크 모니터링 카메라와 교통 분석 카메라가 필요하기 때문입니다. ADAS 장착 차량의 수입 증가는 애프터마켓의 교체 주기를 촉진하고, 아프리카의 모바일 퍼스트 전자상거래 붐은 저조도 셀카 카메라 수요를 견인할 것입니다. 민관 협력의 자금 지원책은 현지 시스템 통합을 가속화하고, CMOS 이미지 센서 시장 확대의 새로운 통로를 형성하고 있습니다.

북미는 소셜 미디어 플랫폼 수요와 엄격한 자동차 안전 규제를 통해 전 세계 디자인에 영향을 미칩니다. 컨텐츠 제작자 생태계에서는 고화질의 8K 촬영에 최적화된 센서가 선호되고 있으며, 국내 팹리스 업체를 프리미엄 틈새 시장으로 이끌고 있습니다. 유럽에서는 독일의 인더스트리 4.0 투자를 기반으로 고신뢰성 산업 및 의료분야에 대한 포토닉스 연구개발이 집중되고 있습니다. 남미와 남아시아는 미개척 시장 규모이지만 가격 민감도가 높아 첨단 센서보다 중급형 센서의 조달이 더 많이 이루어지고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The CMOS image sensor market is expected to grow from USD 24.58 billion in 2025 to USD 26.31 billion in 2026 and is forecast to reach USD 36.96 billion by 2031 at 7.04% CAGR over 2026-2031.

Demand spreads from smartphone cameras to automotive safety, industrial automation and medical diagnostics, reflecting the technology's growing functionality advantages over CCD designs. Stacked backside-illuminated (BSI) architectures incorporating on-die AI logic raise performance while trimming power budgets, reinforcing the CMOS image sensor market's cost-leadership in mass-volume electronics. Regionally, Asia-Pacific anchors production through Taiwan's foundries, while Middle East and Africa outpace with double-digit expansion on smart-city surveillance deployments. Consolidation continues as legacy producers divest capacity and specialist acquisitions accelerate, even as U.S.-China export controls and 300 mm wafer shortages inject supply-chain risk.

Global CMOS Image Sensors Market Trends and Insights

Smartphone Multi-Camera Adoption by APAC OEMs

APAC handset makers are extending multi-camera arrays from flagships into mid-range lines, driving sustained unit growth for high-dynamic-range image sensors. Samsung's 2024 release of 200 MP and 50 MP ISOCELL devices underscored the pivot toward computational photography and higher frame-rate video. OmniVision's OV50X, offering 110 dB single-exposure HDR, illustrates how premium smartphones now differentiate on sensor capability rather than megapixel count alone. Sony's LYT-828, entering mass production in 2025, embeds Hybrid Frame-HDR logic on-die, allowing AI-assisted low-light processing without external ISP cycles. The combination of higher pixel densities and on-sensor compute supports feature expansion while raising average selling prices for advanced parts, reinforcing revenue growth for the CMOS image sensor market.

Regulatory Mandates for ADAS Cameras in US & EU

NHTSA's December 2024 New Car Assessment Program upgrade mandates camera-based blind-spot, lane-keeping and automatic emergency-braking systems across light vehicles, anchoring long-term sensor demand. Global-shutter architectures mitigate motion artifacts essential for safety-critical imaging, evident in Subaru's next-generation EyeSight system that selects onsemi's Hyperlux AR0823AT sensor meeting ASIL C safety standards. The EU's General Safety Regulation mirrors U.S. requirements, synchronizing specifications and giving CMOS foundry operators visibility for a decade of automotive-grade capacity investments.

Advanced 300 mm CIS Wafer Capacity Constraints in Taiwan & Korea

Surging AI-chip orders compete with image-sensor output for advanced 300 mm lines at Taiwanese and Korean foundries, extending lead times from 12-16 weeks to 20-24 weeks. TSMC's Arizona expansion, though capitalized at USD 165 billion, will not meaningfully relieve CIS bottlenecks before 2027. The geographic clustering of stacked BSI manufacturing heightens geopolitical exposure, significantly tempering near-term supply elasticity for the CMOS image sensor market.

Other drivers and restraints analyzed in the detailed report include:

- Video-Centric Social-Media Demand for 4K/8K Sensors in North America

- Miniaturized Sensors for Wearable Medical Imaging in Japan & EU

- ASP Erosion in Entry-Level Smartphones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Backside-illuminated sensors captured 64.40% CMOS image sensor market share in 2025, reflecting superior sensitivity and higher signal-to-noise ratios. The segment's ascendancy lifted the BSI-based CMOS image sensor market size for premium smartphones and automotive cameras. Stacked BSI/3D sensors are advancing at 9.52% CAGR, integrating logic layers that execute AI inference in situ and further enlarge value per square millimeter.

Front-side-illuminated devices maintain relevance in cost-constrained SKUs such as entry-level IoT cameras. Global-shutter architectures, often FSI-based, gain adoption in industrial automation to thwart motion artefacts. Emerging glass-substrate 3D stacking, projected between 2026 and 2031, promises tighter thermal profiles and higher interconnect densities, widening high-end differentiation.

The 12-24 MP band accounted for 24.60% CMOS image sensor market share in 2025, balancing storage and compute overhead in mainstream handsets. >=49 MP devices, though niche, are growing 9.23% annually as surveillance, medical and professional photography favor extreme digital zoom. Canon's 410 MP prototype highlights technical viability of full-frame ultra-high-density sensors, potentially catalyzing new diagnostic imaging modalities.

Sub-12 MP parts endure in barcode scanning and dashcams where frame rate trumps definition. Mid-tier 25-48 MP sensors serve mirrorless cameras leveraging multi-frame computational overlays. The pixel-count bifurcation sharpens price segmentation across the CMOS image sensor market, preserving margin tiers.

The CMOS Image Sensor Market Report is Segmented by Technology (Front Side Illuminated, Backside-Illuminated, and More), Resolution ( Less Than 12 Megapixels, 12-24 Megapixels, and More ), Spectrum (Visible, Non-Visible), Communication Type (Wired, Wireless), End-User Industry (Consumer Electronics, Automotive, Industrial, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific holds 33.70% of 2025 revenue, benefiting from vertically integrated ecosystems spanning foundry silicon to final handset assembly. Taiwanese fabs supply the bulk of stacked-BSI wafers, while mainland China remains the world's largest smartphone export base. Korean innovation, led by Samsung's ISOCELL roadmap, sustains technology leadership inside the CMOS image sensor market. Supply-chain concentration confers scale economics yet elevates earthquake and geopolitical exposure.

Middle East and Africa present the fastest growth at 9.55% CAGR to 2031 as Gulf smart-city blueprints demand networked surveillance and traffic-analytics cameras. ADAS-equipped vehicle imports lift aftermarket replacement cycles, while Africa's mobile-first e-commerce boom drives low-light selfie camera volumes. Public-private funding incentives accelerate local system integration, creating an emerging corridor for CMOS image sensor market expansion.

North America influences global design through social-media platform demands and stringent automotive safety rules. Content-creator ecosystems prioritize sensors optimized for high-frame-rate 8K capture, pushing domestic fabless vendors toward premium niches. Europe, anchored by Germany's Industry 4.0 investments, channels photonics R&D into high-reliability industrial and medical segments. South America and South Asia represent untapped volume, though price sensitivity steers procurement toward established mid-tier designs rather than bleeding-edge sensors.

- Sony Group Corporation

- Samsung Electronics Co., Ltd.

- OmniVision Technologies, Inc.

- onsemi Corporation

- STMicroelectronics N.V.

- Canon Inc.

- Panasonic Holdings Corporation

- SK Hynix Inc.

- Hamamatsu Photonics K.K.

- Teledyne Technologies Incorporated

- GalaxyCore Shanghai Limited Corporation

- SmartSens Technology Co., Ltd.

- PixArt Imaging Inc.

- Tower Semiconductor Ltd.

- ams-OSRAM AG

- Teledyne e2v (UK) Ltd.

- Himax Technologies, Inc.

- Siliconfile Technologies Inc.

- Sharp Corporation

- Caeleste CVBA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smartphone Multi-Camera Adoption by APAC OEMs

- 4.2.2 Regulatory Mandates for ADAS Cameras in US and EU

- 4.2.3 Video-Centric Social Media Demand for 4K/8K Sensors in North America

- 4.2.4 Miniaturized Sensors for Wearable Medical Imaging in Japan and EU

- 4.2.5 Smart-City Surveillance Roll-outs in Middle East

- 4.2.6 Global-Shutter Demand for Industrial Automation in Germany's Industry 4.0

- 4.3 Market Restraints

- 4.3.1 Advanced 300-mm CIS Wafer Capacity Constraints in Taiwan and Korea

- 4.3.2 ASP Erosion in Entry-Level Smartphones

- 4.3.3 Thermal Noise and Rolling-Shutter Limits in High-Speed Cinematography

- 4.3.4 US-China Export Controls on Leading-Edge CIS

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Technology Snapshot (By Communication Type)

- 4.7.1 Wired

- 4.7.2 Wireless

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Front-Side Illuminated (FSI)

- 5.1.2 Backside-Illuminated (BSI)

- 5.1.3 Stacked BSI / 3-D

- 5.1.4 Global-Shutter CMOS

- 5.2 By Resolution

- 5.2.1 Less than 12 Megapixels

- 5.2.2 12-24 Megapixels

- 5.2.3 25-48 Megapixels

- 5.2.4 Greater than 49 Megapixels

- 5.3 By Spectrum

- 5.3.1 Visible Spectrum

- 5.3.2 Non-Visible (NIR, UV, SWIR) Spectrum

- 5.4 By Communication Type

- 5.4.1 Wired

- 5.4.2 Wireless

- 5.5 By End-user Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Automotive and Transportation

- 5.5.3 Industrial and Machine Vision

- 5.5.4 Security and Surveillance

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Computing and Data-center

- 5.5.7 Aerospace and Defense

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Israel

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 United Arab Emirates

- 5.6.4.4 Turkey

- 5.6.4.5 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Sony Group Corporation

- 6.3.2 Samsung Electronics Co., Ltd.

- 6.3.3 OmniVision Technologies, Inc.

- 6.3.4 onsemi Corporation

- 6.3.5 STMicroelectronics N.V.

- 6.3.6 Canon Inc.

- 6.3.7 Panasonic Holdings Corporation

- 6.3.8 SK Hynix Inc.

- 6.3.9 Hamamatsu Photonics K.K.

- 6.3.10 Teledyne Technologies Incorporated

- 6.3.11 GalaxyCore Shanghai Limited Corporation

- 6.3.12 SmartSens Technology Co., Ltd.

- 6.3.13 PixArt Imaging Inc.

- 6.3.14 Tower Semiconductor Ltd.

- 6.3.15 ams-OSRAM AG

- 6.3.16 Teledyne e2v (UK) Ltd.

- 6.3.17 Himax Technologies, Inc.

- 6.3.18 Siliconfile Technologies Inc.

- 6.3.19 Sharp Corporation

- 6.3.20 Caeleste CVBA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment