|

시장보고서

상품코드

1934739

일회용 페이스 마스크 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Disposable Face Mask - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

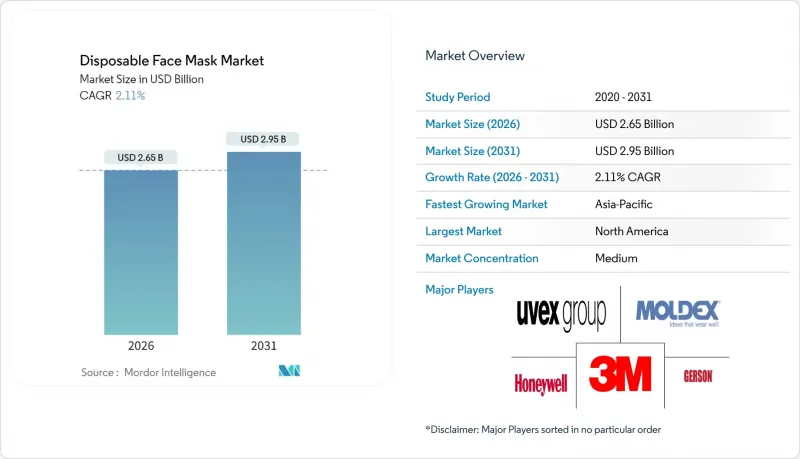

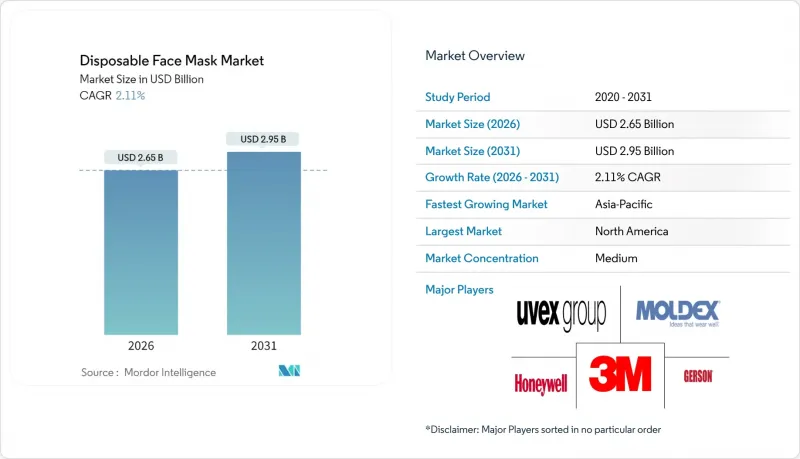

일회용 페이스 마스크 시장은 2025년 26억 달러에서 2026년에는 26억 5,000만 달러로 성장하며, 2026-2031년에 CAGR 2.11%로 추이하며, 2031년까지 29억 5,000만 달러에 달할 것으로 예측됩니다.

이러한 전망은 일회용 페이스 마스크 시장이 성숙기에 접어들었음을 의미하며, 전염병으로 인한 수요 급증보다는 여과 성능, 항균 코팅, 지속가능한 소재의 기술 혁신이 더 중요하게 여겨지는 상황입니다. 산업용 구매자가 지속적으로 판매량을 견인하고 있지만, 소비자의 고성능성 마스크와 친환경 제품에 대한 수용도도 높아지고 있습니다. 주요 원자재 가격 안정화에 따라 가격 책정 규율이 개선되는 한편, 유통 경로의 다변화로 지역별 수요 변동이 완화되고 있습니다. 주요 PPE 공급업체들 간의 통합이 진행되면서 프리미엄 제품이나 친환경 제품에 특화된 틈새 기업에게 기회가 생기고 있습니다.

세계 일회용 페이스 마스크 시장 동향과 인사이트

주요 대도시권의 대기오염 심화

대기질 악화로 인해 전 세계 인구의 99%가 WHO 기준치를 초과하는 공기를 마시고 있습니다. 이에 따라 아시아 메가시티에서는 소비자들이 연중 내내 고여과율 마스크를 착용하는 움직임이 확산되고 있습니다. 0.3 마이크론 입자를 99% 걸러내는 FFP3 방진 마스크는 2025년에 인기를 얻었으며, 특히 건설업에서 널리 채택되었습니다. 중공업 지역의 조달 책임자는 현재 실시간 오염 지수와 보호구 재고를 연동하여 고품질 마스크를 지정하고 있습니다. 직장 수요와 소매 수요가 결합하여 일회용 마스크 시장에는 환경 위생에 기인하는 팬데믹 이외의 성장 요인이 생겨나고 있습니다. 오염 급증과 판매의 연동성을 활용하는 제조업체는 평균 판매 가격 상승을 누리고 있습니다.

직장에서의 PPE(개인보호장비) 준수 의무

2025년 1월 13일 시행되는 OSHA 개정 건설업 규정은 적합성 테스트 및 문서화 요건을 명문화하고, 기존에 허용되었던 기준 미달 보호구 사용을 배제했습니다. 비준수 여부를 실시간으로 감지하는 시각적 AI 시스템이 단속을 강화하고, 인증된 일회용 마스크는 사업 운영의 기본 비용으로 자리 잡았습니다. 이러한 규제 강화는 제조업, 의료, 서비스업에 영향을 미쳐 경기 순환으로부터 수요를 보호하고 있습니다. 대규모 산업 바이어는 다년 계약을 체결하여 일회용 마스크 시장에서 인증 공급업체의 안정적인 공급량을 확보합니다. 중소기업은 더 무거운 처벌에 직면하고 있으며, 적합 제품으로의 전환을 가속화하고 있습니다.

폴리프로필렌 원료 가격 변동성

2025년 1월부터 4월까지 현물 가격(파운드당 0.11달러)의 급등은 특히 중소형 컨버터 기업의 이익률을 압박하고 있습니다. 북미의 수지 가격 상승이 아시아 시장을 앞지르면서 세계 조달 전략이 복잡해지고 있습니다. 일부 공급망 리더는 물류비용이 매출의 20%에 달하고, 경쟁력을 떨어뜨리고 있다고 보고하고 있습니다. 지정학적 불확실성을 고려할 때, 선물 매수나 헤지를 통한 완화 효과는 제한적일 것입니다. 대부분의 일회용 마스크는 수지가 주원료이기 때문에 비용 전가는 가격에 민감한 일회용 마스크 시장 부문의 판매량 감소 위험을 수반합니다.

부문 분석

2025년 기준, 이 부문은 일회용 마스크 시장 규모에서 가장 큰 단독 점유율을 차지했으며, 수술용 마스크는 병원 및 클리닉에서 광범위하게 채택되면서 38.74%의 점유율을 유지했습니다. 그러나 산업 고용주들이 여과 성능 요건을 FFP3 및 ASTM 레벨 3 표준으로 상향 조정함에 따라 보호 마스크는 2031년까지 2.51%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 기술의 상호 침투가 두드러지고, 한때 고급 보호 장비의 영역이었던 항균 코팅이 수술용 마스크에도 적용되어 기능적 차이가 줄어들고 있습니다. 부직포 유형은 대량 생산에서 비용 효율성을 유지하는 한편, ESG 지표가 입찰에 영향을 미치는 가운데, 새로운 생분해성 제품 라인이 미래 성장의 씨앗이 되고 있습니다. FDA의 미승인 제품 변경에 대한 경고는 안전성 재분류가 시장 진입을 제한할 수 있다는 점을 강조하며, 명확한 시험 데이터의 중요성을 다시 한 번 강조하고 있습니다.

지속적인 혁신을 통해 상품화 위험에도 불구하고 이익률은 유지되고 있습니다. 완전 자동화된 조립 라인은 약간의 공구 변경으로 제품 유형을 전환할 수 있으며, 공급업체는 생산 능력을 희생하지 않고도 수요 급증에 대응할 수 있습니다. 동시에, 특수 방진 마스크에 부수되는 일회용 페이스 마스크 시장 점유율은 대기질 규제와 근로자 건강 소송이라는 이중적 요인에 대응하는 건설 분야에서 확대되고 있습니다. 기능성, 편안함, 지속가능성을 융합한 공급업체는 프리미엄 가격대와 고객 충성도를 확보할 수 있습니다.

지역별 분석

북미는 엄격한 노동 안전 정책과 대규모 비축을 유지할 수 있는 재정적 자원으로 인해 2025년 일회용 마스크 시장의 36.80%를 차지했습니다. '미국산 PPE법'은 조달을 국내 생산품으로 전환하여 국내 제조업체를 수입 변동의 영향으로부터 보호하고 있습니다. 성장세는 완만하지만 안정적이며, 항균 및 생분해성 제품을 권장하는 규제 강화와 병원 관행의 변화가 그 중심을 이루고 있습니다. 미국 소재 공급업체는 생산 능력 및 인력 개발 관련 연방 정부 보조금도 활용할 수 있습니다.

아시아태평양은 제조업의 확대, 도시 지역의 심각한 대기 오염, 안전 기준 강화 등을 배경으로 2031년까지 연평균 복합 성장률(CAGR) 2.57%를 보일 것으로 예측됩니다. 중국 마스크 소매 시장 규모는 6,000억 위안이 넘고, 습관적인 주간 사용이 기초 수요를 지탱하고 있습니다. 인도에서는 수술 건수 증가와 감염 예방 의무화로 병원 수요가 증가하고 있지만, 정보 출처의 신뢰성 유지를 위해 시장 조사에 기반한 예측은 제외했습니다. 지역 제조업체들은 비용 우위를 활용하여 잉여 생산능력을 수출하기 전에 국내 가치를 확보하기 위해 자체 브랜드에 대한 투자를 확대하고 있습니다.

유럽에서는 CE 마킹 요건과 지속가능성 관련 법규로 인해 균형 잡힌 발전이 이루어지고 있습니다. 인증의 강화는 고품질 공급업체에게는 기회를 가져다주는 반면, 신규 시장 진출기업에게는 진입장벽을 높이고 있습니다. 유럽연합 집행위원회의 순환경제 로드맵은 생분해성 마스크를 권장하고, 재료과학 분야의 협력을 촉진하고 있습니다. 지속적인 경제 회복과 공중 보건에 대한 인식이 높아지면서 기준 수요가 안정화되는 가운데, 기관 구매자들은 ESG 태스크포스의 권고에 따라 전체 수명주기 비용에 대한 평가를 진행하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

The disposable face mask market is expected to grow from USD 2.60 billion in 2025 to USD 2.65 billion in 2026 and is forecast to reach USD 2.95 billion by 2031 at 2.11% CAGR over 2026-2031.

This outlook positions the disposable face mask market as a maturing field where innovation in filtration performance, antimicrobial coatings, and sustainable materials now matter more than pandemic-driven spikes in demand. Industrial buyers continue to underpin volume, but consumer acceptance of higher-specification masks and environmentally friendly variants is rising. Pricing discipline has improved as major raw-material costs stabilize, while channel diversification mitigates regional demand swings. Consolidation among large PPE suppliers creates opportunities for niche players focusing on premium and eco-conscious offerings.

Global Disposable Face Mask Market Trends and Insights

Rising Pollution Levels in Major Urban Clusters

Air-quality deterioration means that 99% of the world's population breathes air exceeding WHO guidelines, prompting consumers in Asian megacities to adopt high-filtration masks year-round . FFP3 dust masks offering 99% filtration for 0.3-micron particles gained popularity in 2025, especially among construction trades. Procurement managers in heavily industrialized regions now specify premium masks, linking real-time pollution indices to protective-equipment inventories. Workplace demand combines with retail uptake, giving the disposable face mask market a non-pandemic growth lever tied to environmental health. Manufacturers capitalizing on this link between pollution spikes and sales enjoy higher average selling prices.

Mandates For Workplace PPE Compliance

OSHA's revised construction-sector rule effective 13 January 2025 codifies fit-testing and documentation requirements, removing ambiguity that once allowed sub-standard protection . Vision AI systems that flag non-compliance in real time strengthen enforcement, making certified disposable masks a baseline cost of doing business. This regulatory tightening affects manufacturing, healthcare, and services, shielding demand from economic cycles. Large industrial buyers negotiate multi-year contracts, ensuring stable throughput for certified suppliers in the disposable face mask market. Smaller firms confront heavier penalties, accelerating the shift toward compliant products.

Volatility In Polypropylene Feedstock Prices

Spot-price spikes of USD 0.11 per pound between January and April 2025 squeeze margins, particularly for small and mid-tier converters. North American resin hikes outpaced Asian markets, complicating global sourcing strategies. Some supply-chain leaders report logistics costs hitting 20% of revenue, eroding competitiveness. Forward-buying and hedging offer limited relief given geopolitical uncertainties. As resin remains the primary input for most disposable masks, cost pass-throughs risk volume losses in price-sensitive segments of the disposable face mask market.

Other drivers and restraints analyzed in the detailed report include:

- Pandemic-Preparedness Stockpiling by Governments

- Antimicrobial Coating Innovations Accelerating Premiumisation

- Shift Toward Reusable Respirators For Sustainability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment generated the largest singular slice of the disposable face mask market size in 2025, with surgical masks holding 38.74% share alongside broad adoption in hospitals and clinics. Protective masks, however, post the briskest 2.51% CAGR through 2031 as industrial employers upgrade filtration requirements to FFP3 and ASTM Level 3 thresholds. Cross-pollination of technology is evident: antimicrobial coatings, once the domain of high-end protective gear, now appear on surgical offerings, narrowing functional distinctions. Non-woven variants remain cost-efficient for scale production, while novel biodegradable lines seed future growth as ESG metrics influence tenders. The FDA's warning to Baylab USA for unapproved product changes underscores how safety re-classification can restrict market access, reinforcing the importance of unambiguous test data.

Persistent innovation keeps margins defensible despite commoditization risks. Fully automated assembly lines now switch among product types with minor tooling shifts, enabling suppliers to chase demand spikes without capacity penalties. At the same time, the disposable face mask market share attached to specialty dust masks grows within construction verticals responding to dual drivers of air-quality regulation and worker-health litigation. Suppliers that blend function, comfort, and sustainability command premium price bands and customer loyalty.

The Disposable Face Mask Market Report is Segmented by Product Type (Non-Woven, Protective, Surgical, Dust, Others), Application (Industrial Use, Personal Use), Distribution Channel (Offline, Online), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 36.80% of the disposable face mask market in 2025 due to stringent occupational-safety policies and the financial resources to maintain sizeable stockpiles. The Make PPE in America Act shifts procurement toward domestically produced units, sheltering local manufacturers from import volatility. Growth is modest but reliable, pivoting on regulatory upgrades and hospital practice changes that favor antimicrobial and biodegradable variants. Suppliers located in the United States also benefit from federal grants tied to capacity and workforce development.

Asia-Pacific is the momentum engine, expanding at a 2.57% CAGR through 2031 on the back of manufacturing growth, dense urban pollution, and tightening safety standards. China's retail market for masks exceeds CNY 600 billion, with habitual weekly use supporting baseline demand. India's rising surgical volumes and infection-prevention mandates add hospital demand, although market-research-derived forecasts have been excluded to maintain source integrity. Regional producers leverage cost advantages and are increasingly investing in proprietary brands to capture domestic value before exporting excess capacity.

Europe shows balanced development shaped by CE-marking requirements and sustainability legislation. Certification stringency opens doors for high-quality suppliers yet raises entry costs for new players. The European Commission's circular-economy roadmap encourages biodegradable masks, spurring material-science collaborations. Ongoing economic recovery and renewed public-health awareness keep baseline volumes stable, while institutional buyers assess total-lifecycle costs to align with ESG task-force recommendations.

- Solventum

- Honeywell International

- Kimberly-Clark Worldwide

- Cardinal Health

- Moldex-Metric

- Uvex Group

- Ansell

- DuPont

- Kowa

- The Gerson Company

- SAS Safety

- Prestige Ameritech

- Alpha Pro Tech

- Cambridge Mask

- Owens & Minor Inc.

- Medicom Group

- Shanghai Dasheng Health Products Manufacture Co.

- Winner Medical Co., Ltd.

- Lakeland Industries

- Louis M. Gerson Co.

- BYD Company Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Pollution Levels in Major Urban Clusters

- 4.2.2 Mandates For Workplace PPE Compliance

- 4.2.3 Pandemic-Preparedness Stockpiling by Governments

- 4.2.4 Antimicrobial Coating Innovations Accelerating Premiumisation

- 4.2.5 D2C Micro-Brands Growing Via E-Commerce

- 4.2.6 ESG-Driven Demand for Biodegradable Mask Options

- 4.3 Market Restraints

- 4.3.1 Volatility In Polypropylene Feedstock Prices

- 4.3.2 Shift Toward Reusable Respirators for Sustainability

- 4.3.3 Phase-Out Of Temporary PPE Subsidies

- 4.3.4 Counterfeit Certification Undermining Consumer Trust

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product type

- 5.1.1 Non-woven

- 5.1.2 Protective

- 5.1.3 Surgical

- 5.1.4 Dust

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Industrial Use

- 5.2.2 Personal Use

- 5.3 By Distribution Channel

- 5.3.1 Offline

- 5.3.2 Online

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Solventum

- 6.3.2 Honeywell International Inc.

- 6.3.3 Kimberly-Clark Corporation

- 6.3.4 Cardinal Health Inc.

- 6.3.5 Moldex-Metric Inc.

- 6.3.6 Uvex Group

- 6.3.7 Ansell Limited

- 6.3.8 DuPont de Nemours Inc.

- 6.3.9 Kowa Company Ltd.

- 6.3.10 The Gerson Company

- 6.3.11 SAS Safety Corp.

- 6.3.12 Prestige Ameritech

- 6.3.13 Alpha ProTech

- 6.3.14 Cambridge Mask Co.

- 6.3.15 Owens & Minor Inc.

- 6.3.16 Medicom Group

- 6.3.17 Shanghai Dasheng Health Products Manufacture Co.

- 6.3.18 Winner Medical Co., Ltd.

- 6.3.19 Lakeland Industries

- 6.3.20 Louis M. Gerson Co.

- 6.3.21 BYD Company Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment