|

시장보고서

상품코드

1934742

수근관 개방 시스템 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Carpal Tunnel Release Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

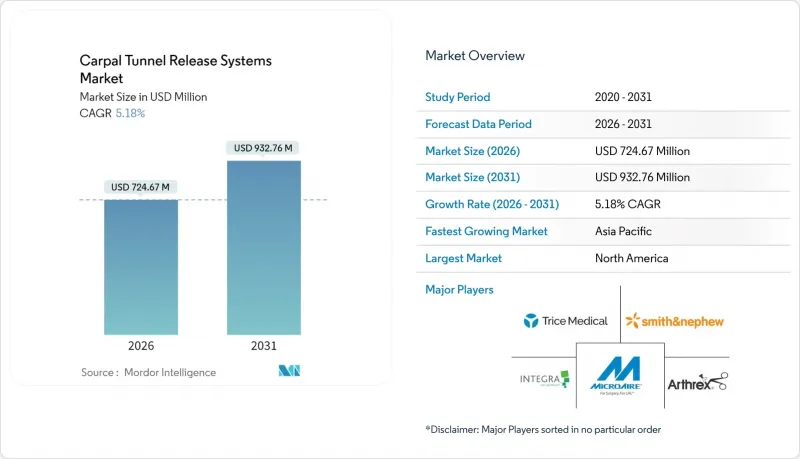

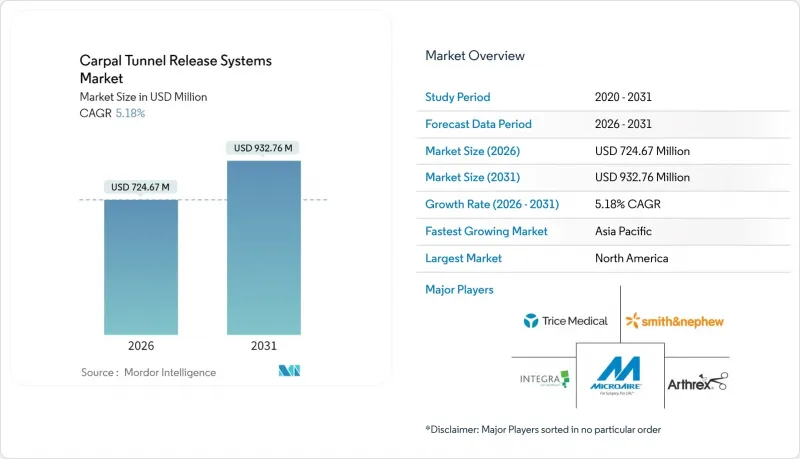

수근관 개방 시스템 시장 규모는 2026년에는 7억 2,467만 달러로 추정되며, 2025년 6억 8,898만 달러에서 성장이 전망됩니다.

2031년에는 9억 3,276만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 연평균 5.18%의 성장률을 나타낼 것으로 전망됩니다.

고령화에 따른 중추신경감압술에 대한 수요 증가, 저침습적 기술에 대한 외과 의사들의 선호도 증가, 초음파 유도하 접근법에 대한 지불자의 지원 등이 주요 성장 요인으로 작용하고 있습니다. 내시경 솔루션은 회복기간 단축을 위해 채택이 확대되고 있으며, 클리닉 기반 각성하 수술 모델은 미국에서만 연간 약 7억 5,000만 달러의 시설 사용료와 마취 비용을 절감하고 있습니다. AI를 활용한 신경 매핑, 일회용 광학기기, 일회용 기구 등의 혁신은 외래 진료 환경에서의 가치 제안을 더욱 강화할 것입니다. 지역별로 보면, 북미가 보험급여제도와 전문의 밀집도가 높아 선두를 달리고 있지만, 아시아태평양은 의료 접근성 확대와 저침습적 치료법에 대한 인식이 높아지면서 다른 모든 지역을 능가하는 성장이 예상되고 있습니다.

세계 수근관 개방 시스템 시장 동향 및 인사이트

노동력 고령화로 인한 CTS 발생률 증가

45-60세 근로자의 손목터널증후군 발병률이 가장 높으며, 이는 정년연령 증가 및 반복적인 작업에 장기간 노출되는 것과 밀접한 관련이 있습니다. 조직의 노화로 인해 힘줄의 탄력이 감소하고 중추신경 압박의 위험이 증가하기 때문에 많은 환자들에게 인체공학적 조치만으로는 충분하지 않습니다. 전 세계 인구의 3.8%가 앓고 있어 지속적인 환자 유입이 수술 건수의 견조한 추세를 뒷받침하고 있으며, 이는 수근관개방시스템 시장에 대한 지속적인 수요로 이어지고 있습니다. 선진국은 여전히 고령화된 노동력 때문에 여전히 중심이지만, 산업화가 빠르게 진행되고 있는 아시아 국가들도 빠르게 따라잡고 있습니다. 고용주들이 생산성 감소의 위험을 인식하고 있기 때문에 기업은 조기 개입 경로의 도입을 촉진하고 있으며, 예방 조치를 취하더라도 수술 수요가 지속될 수 있도록 보장하고 있습니다.

외래 및 클리닉 기반 수술로의 전환

내시경 수술은 당일 퇴원이 가능하며, 환자는 수일 내에 가벼운 활동을 재개할 수 있습니다. 반면, 개복 수술은 몇 주가 소요됩니다. 전신마취가 필요 없는 국소마취 프로토콜은 전체 수술 시간을 더욱 단축하고, 하루 수술 건수를 증가시켜 의료기관의 비용 절감으로 이어집니다. 이 형태는 동등한 임상적 성과와 편리함을 동시에 내세울 수 있는 외래수술센터(ASC)나 진료소에게 수익 창출의 기회를 열어줄 수 있습니다. 이러한 환경에서는 재처리가 필요 없는 일회용 키트의 도입이 촉진되어 감염관리 컴플라이언스 강화와 물류 효율화를 동시에 도모할 수 있습니다.

수술 후 주상부 통증과 소송 리스크

주상부 통증은 해방술의 7-48%에서 발생하며, 최대 1년까지 지속될 수 있고, 특히 소송이 많은 지역에서는 환자의 불만과 의료 과실 위험을 높입니다. 내시경적 접근은 발생률이 다소 낮지만, 이 증후군을 완전히 배제할 수 있는 것은 아닙니다. 수술 전 감각 프로파일 평가를 통해 위험도 계층화가 가능하지만, 시간과 비용이 증가합니다. 외과의사는 새로운 의료기기의 추가적 이점이 법적 리스크를 상회하지 않는다고 판단할 경우, 도입을 주저할 수 있으며, 일시적으로 보급이 둔화될 수 있습니다.

부문 분석

내시경 솔루션은 2025년 수근관 개방 시스템 시장 점유율의 55.64%를 차지할 것으로 예상되며, 이는 15mm 미만의 절개를 통한 최소침습적 시각화에 대한 외과 의사의 지속적인 선호를 뒷받침합니다. 내시경 기기 시장 규모는 멸균 비용을 절감할 수 있는 일회용 키트의 출시로 복합적으로 확대될 것으로 예측됩니다. 단일 포트형은 학습 곡선을 줄이고, 듀얼 포트 시스템은 복잡한 인대 해부학에 대응하는 넓은 시야를 제공합니다. 초음파 가이드 플랫폼은 절대적인 시장 규모는 작지만 전신마취가 필요 없는 진정한 진료실 수술이 가능하기 때문에 5.63%의 가장 빠른 CAGR을 기록하고 있습니다. AI 지원 이미지 오버레이는 인대절단 경로 계획을 효율화하여 조기 도입자의 기술 격차 장벽을 줄입니다. 개방형 시스템은 여전히 유착을 동반한 복잡한 재수술 사례에 사용되고 있으며, 저침습적 나이프 라이트 키트는 촉각 피드백과 LED 조명을 결합한 하이브리드형 비용 절감 옵션을 제공합니다.

이와 함께, 제조업체들이 대량 사용 시설용 재사용 스코프부터 원격 진료 시설용 일회용 블레이드까지 계층화된 구성을 도입함에 따라 가격 경쟁이 치열해지고 있습니다. 미국은 보험사의 시설요금 우대정책의 혜택을 받아 주요 수익원이 되고 있지만, 성장의 초점이 인도, 중국 등 인구 대국으로 이동하고 있습니다. 이들 국가에서는 산업 분야의 고용 확대로 인해 CTS(손목터널증후군)의 발생률이 가속화되고 있습니다. 제품 차별화는 현재 하드웨어 개선과 더불어 소프트웨어 업그레이드에 중점을 두고 있으며, 진단, 수술 안내, 수술 후 분석을 통합된 워크플로우로 연결하는 에코시스템 관점을 강조하고 있습니다.

본 보고서는 제품 유형별(개방형 수근관 개방 시스템, 내시경적 수근관 개방 시스템, 초음파 유도하 CTR 시스템, 최소침습 키트 기반 CTR 시스템), 최종사용자별(병원, 외래수술센터, 전문 클리닉), 지역별(북미, 유럽, 아시아, 아시아태평양, 남미, 기타)로 분류되어 있습니다. 태평양, 남미, 기타)로 분류되어 있습니다. 시장 예측은 금액(USD)으로 제공됩니다.

지역별 분석

북미는 종합적인 보험 적용 범위와 펠로우십 교육을 받은 수부외과 전문의의 촘촘한 네트워크를 바탕으로 2025년 전체 매출의 39.84%를 차지할 것으로 예측됩니다. AI 기반 초음파 시스템의 조기 도입과 다기관 공동 레지스트리를 통해 실제 임상 증거를 신속하게 검증할 수 있는 에코시스템이 이 지역의 지속적인 선도적 지위를 뒷받침하고 있습니다. 유럽은 공공 보험 제도와 표준화된 임상 가이드라인으로 꾸준한 보급을 유지하고 있지만, 주정부 예산의 상한선으로 인해 고가 키트의 보급이 다소 억제되고 있습니다.

아시아태평양은 5.93%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 인구 고령화와 산업 분야의 작업장 확대로 인해 가장 빠르게 성장하는 지역입니다. 한국의 정부 보험 확대와 인도의 파일럿 기기 대여 프로그램은 민간 클리닉의 초기 비용을 절감하고 수술 건수를 더욱 증가시키고 있습니다. 베트남 보건부가 국가급 병원에 MicroAire 내시경 유닛을 승인한 사례는 지역적 정책적 지원의 좋은 예입니다. 중국 도시지역 노동자 보험제도가 내시경적 해방술에 대한 보험 적용을 시작함에 따라 고등공공병원의 장비 조달이 활발해졌고, 그 시술 기술이 현급 시설로 파급되고 있습니다. 라틴아메리카의 경우, 브라질의 보충 보험 시장이 저침습적 방출술을 재정적으로 뒷받침하는 반면, 장비 수입 관세가 보급에 걸림돌이 되고 있습니다. 중동 및 아프리카은 여전히 개발 중인 지역입니다. 걸프 국가들은 3차 정형외과 센터에 대한 투자를 추진하는 반면, 사하라 이남 국가들은 전문 수술에 있어 인도적 지원 임무에 계속 의존하고 있습니다. 제조업체들은 이 지역을 장기적인 성장 기회로 보고, 자본 장비 임대와 외과 의사 연수 장학금을 결합한 하이브리드 판매 모델을 도입할 필요가 있다고 판단하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05carpal tunnel release systems market size in 2026 is estimated at USD 724.67 million, growing from 2025 value of USD 688.98 million with 2031 projections showing USD 932.76 million, growing at 5.18% CAGR over 2026-2031.

Rising median-nerve decompression demand from an aging workforce, growing surgeon preference for minimally invasive techniques, and payer support for ultrasound-guided approaches are the prime growth levers. Endoscopic solutions drive adoption because they shorten recovery times, while office-based wide-awake surgery models cut facility fees and anesthesia costs by an estimated USD 750 million each year in the United States alone. Technological innovations-including AI-enabled nerve mapping, disposable optics, and single-use instrumentation-further strengthen the value proposition for outpatient settings. Regionally, North America leads due to robust reimbursement and specialist density, yet Asia-Pacific is set to outpace all other regions as healthcare access broadens and awareness of minimally invasive options rises.

Global Carpal Tunnel Release Systems Market Trends and Insights

Aging Workforce Driving CTS Incidence

Workers aged 45-60 experience the highest rates of carpal tunnel syndrome, a demographic fact closely tied to postponed retirement ages and longer exposure to repetitive tasks. Tissue aging reduces tendon elasticity and increases median-nerve compression vulnerability, making ergonomic programs insufficient for many patients. As 3.8% of the global population is affected, the persistent patient pipeline underpins robust procedure volumes and, by extension, sustained demand for the carpal tunnel release systems market. Developed economies remain epicenters because of their older labor forces, but industrializing Asian nations are quickly converging. Employers' awareness of productivity losses fosters corporate adoption of early-intervention pathways, ensuring that surgical demand continues even with preventive measures in place.

Shift to Outpatient & Office-Based CTR Procedures

Endoscopic releases enable same-day discharge, with patients resuming light activities in a matter of days versus weeks for open surgery. Wide-awake local-anesthetic protocols further compress total procedure time, allowing more cases per surgical day and reducing costs for payers. This configuration unlocks revenue opportunities for ambulatory surgery centers and office suites that can market convenience alongside equivalent clinical outcomes. Such settings reinforce adoption of disposable kits that eliminate re-processing, thereby strengthening infection-control compliance while streamlining logistics.

Post-Operative Pillar Pain & Litigation Risk

Pillar pain occurs in 7-48% of release procedures and may linger up to a year, fueling dissatisfaction and malpractice exposure, especially in litigious regions. While endoscopic routes demonstrate somewhat lower incidence, they do not eliminate the syndrome. Preoperative sensory-profile assessments can stratify risk, yet add time and cost. Surgeons may hesitate to adopt new devices if perceived incremental benefits fail to outweigh legal hazards, temporarily dampening uptake.

Other drivers and restraints analyzed in the detailed report include:

- Reimbursement Expansion for Ultrasound-Guided CTR

- Surge in Ergonomic-Injury Prevention Programs

- Shortage of Hand Surgeons in Emerging Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Endoscopic solutions captured 55.64% of carpal tunnel release systems market share in 2025, underlining sustained surgeon preference for minimally invasive visualization with sub-15-mm incisions. The carpal tunnel release systems market size for endoscopic devices is set to compound thanks to disposable kit launches that remove sterilization overhead. Single-portal variants offer reduced learning curves, while two-portal systems deliver broader visual fields for complex ligament anatomy. Ultrasound-guided platforms, although representing a smaller absolute base, are logging the fastest 5.63% CAGR because they enable true office-suite procedures without general anesthesia. AI-assisted imaging overlays streamline ligament-division path planning, narrowing skill-gap barriers for early adopters. Open systems linger for revision cases complicated by adhesions, and mini-invasive knife-light kits provide hybrid cost-saving alternatives that merge tactile feedback with LED illumination.

In parallel, price competitiveness intensifies as manufacturers introduce tiered configurations ranging from reusable scopes for high-volume centers to single-use blades packaged for remote ambulatory sites. The United States, benefitting from insurers' facility-fee incentives, is the principal revenue generator, yet growth hotspots are shifting to high-population countries such as India and China, where industrial job expansion accelerates CTS incidence. Product differentiation now emphasizes software upgrades as much as hardware refinements, underscoring an ecosystem view that links diagnostics, surgical guidance, and postoperative analytics into an integrated workflow.

The Carpal Tunnel Release Systems Report is Segmented by Product Type (Open Carpal Tunnel Release Systems, Endoscopic Carpal Tunnel Release Systems, Ultrasound-Guided CTR Systems, Mini-Invasive Kit-Based CTR Systems), End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39.84% of total 2025 revenues on the back of comprehensive insurance coverage and dense networks of fellowship-trained hand surgeons. Its continued leadership is helped by early adoption of AI-enabled ultrasound systems and an ecosystem that quickly validates real-world evidence via multicenter registries. Europe maintains steady uptake through public-payer mechanisms and standardized clinical guidelines; however, state budget caps moderately temper premium-priced kit penetration.

Asia-Pacific, forecast at a 5.93% CAGR, is the fastest-growing territory as demographic aging converges with industrial workplace expansion. Government insurance expansions in South Korea and pilot device-rental programs in India reduce upfront costs for private clinics, further stimulating procedure volumes. Vietnam's Ministry of Health approving MicroAire endoscopic units for national-level hospitals exemplifies regional policy endorsement. China's urban-worker insurance pool now reimburses endoscopic releases, triggering procurement by high-tier public hospitals and cascading procedure familiarity to county-level facilities. Latin America exhibits mixed dynamics: Brazil's supplemental insurance market funds minimally invasive releases, but device import duties slow broader adoption. The Middle East and Africa remain nascent; Gulf countries invest in tertiary orthopedic centers, whereas Sub-Saharan nations still rely on humanitarian missions for specialist surgeries. Manufacturers view these regions as long-tail opportunities necessitating hybrid sales models that blend capital-equipment leasing with surgeon-training scholarships.

- Arthrex

- Stryker

- Conmed

- MicroAire

- Smiths Group

- AM Surgical

- Sonex Health Inc.

- Seg-WAY Orthopaedics Inc.

- Spirecut SA

- Valor Health Co. Ltd.

- MPR Surgical

- Innomed Inc.

- Karl Storz

- Trice Medical Inc.

- Integra LifeSciences Holdings Corp.

- Surgical Instruments (Evans Knife Guide)

- ThreadTech Medical Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging workforce driving CTS incidence

- 4.2.2 Shift to outpatient & office-based CTR procedures

- 4.2.3 Reimbursement expansion for ultrasound-guided CTR

- 4.2.4 Surge in ergonomic-injury prevention programs

- 4.2.5 AI-enabled pre-operative nerve mapping tools

- 4.2.6 Disposable single-use endoscopes reducing SSI risks

- 4.3 Market Restraints

- 4.3.1 Post-operative pillar pain & litigation risk

- 4.3.2 Shortage of hand surgeons in emerging economies

- 4.3.3 Capital cost barrier for ultrasound systems

- 4.3.4 Supply-chain fragility in medical-grade optics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Threat of Substitutes

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Bargaining Power of Buyers

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Product Type

- 5.1.1 Open Carpal Tunnel Release Systems

- 5.1.2 Endoscopic Carpal Tunnel Release Systems

- 5.1.3 Ultrasound-Guided CTR Systems

- 5.1.4 Mini-invasive Kit-based CTR Systems

- 5.2 By End User

- 5.2.1 Hospitals

- 5.2.2 Ambulatory Surgical Centers

- 5.2.3 Specialty Clinics

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 GCC

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Arthrex Inc.

- 6.3.2 Stryker Corporation

- 6.3.3 CONMED Corporation

- 6.3.4 MicroAire Surgical Instruments LLC

- 6.3.5 Smith & Nephew plc

- 6.3.6 AM Surgical Inc.

- 6.3.7 Sonex Health Inc.

- 6.3.8 Seg-WAY Orthopaedics Inc.

- 6.3.9 Spirecut SA

- 6.3.10 Valor Health Co. Ltd.

- 6.3.11 MPR Surgical

- 6.3.12 Innomed Inc.

- 6.3.13 Karl Storz SE & Co. KG

- 6.3.14 Trice Medical Inc.

- 6.3.15 Integra LifeSciences Holdings Corp.

- 6.3.16 Surgical Instruments (Evans Knife Guide)

- 6.3.17 ThreadTech Medical Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment