|

시장보고서

상품코드

1934750

소독제 및 살균제 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Antiseptics And Disinfectants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

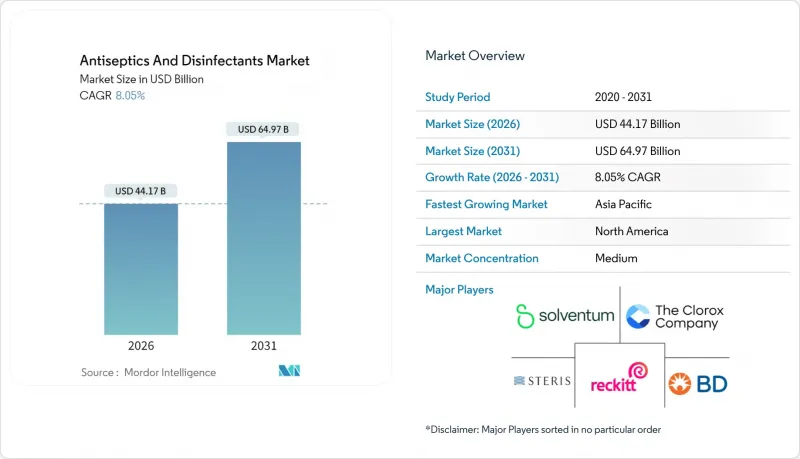

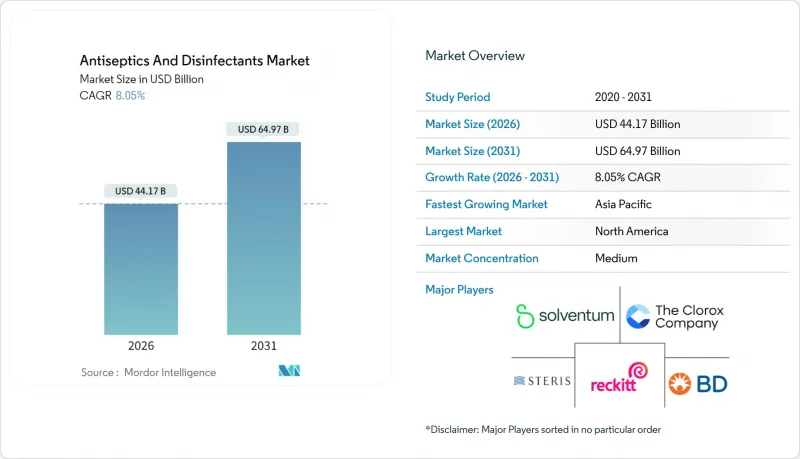

소독제 및 살균제 시장은 2025년에 408억 8,000만 달러로 평가되었고, 2026년 441억 7,000만 달러에서 2031년까지 649억 7,000만 달러에 이를 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 8.05%로 예상됩니다.

현재 지출 패턴을 보면, 감염관리 예산과 의료관련감염(HAI)으로 인한 병원의 금전적 페널티 사이에 뚜렷한 상관관계가 있음을 알 수 있습니다. 예방 기술에 대한 자본 배분은 치료제보다 빠르게 증가하고 있으며, 이는 병원 구매 부서에서 치료보다 예방에 대한 전략적 우선순위를 반영하고 있습니다. 이 기회의 규모는 하루에 여러 번 소독이 필요한 고접촉 표면과 재사용 가능한 의료기기의 방대한 설치 기반에 의해 더욱 강화되고 있습니다. 시장이 꾸준히 성장하고 있다는 것은 감염 관리가 의료 서비스 제공업체에게 필수적인 지출 항목이기 때문에 수요는 경기 둔화에 대체로 견딜 수 있다는 것을 시사합니다. 따라서 제조업체들은 소비자 부문 수요가 증가하는 가운데서도 병원용 제품의 생산 능력을 우선적으로 확보하고 있습니다.

규제 감시 강화는 수요를 억제하기는커녕 오히려 수요를 가속화하고 있습니다. 의료 서비스 제공업체는 향후 처벌 위험이 낮고 규제에 부합하는 차세대 화학물질을 선호하기 때문입니다. 2024년 3월에 확정된 미국 환경보호청의 에틸렌옥사이드 살균기에 대한 90% 배출량 감축 의무가 좋은 예이며, 이로 인해 구매자들은 저잔류 효소계 혼합제나 기화 과산화수소 시스템으로 전환하고 있습니다. 이러한 대체 기술을 중심으로 구축된 지적재산권 포트폴리오는 인수합병(M&A)에서 높은 평가를 받고 있으며, 보다 안전하고 친환경적인 대안으로의 전략적 전환을 반영하고 있습니다. 투자자들은 또한 병원 인프라의 수명이 길어짐에 따라 호환 가능한 제제의 지속적인 판매가 보장된다는 점에 주목하고 있으며, 경제적 역풍이 제한적이라면 실제 성장률은 공시된 8%의 연평균 복합 성장률(CAGR)을 상회할 수 있음을 시사하고 있습니다.

세계 소독제 및 살균제 시장 동향과 인사이트

병원 내 감염 증가 추세

병원 내 감염(HAI)은 지속적으로 증가하고 있으며, 유럽 의료기관에서 연간 890만 건이 보고되고 있으며, 공공 및 민간 병원 모두에 예산 부담을 초래하고 있습니다. 병원은 감염 사례마다 수익 손실이 발생하기 때문에 예방 예산이 우선적으로 배정되며, 이는 소독제 및 살균제 시장의 성장을 뒷받침하고 있습니다. 고도의 모니터링 프로그램을 도입한 시설에서는 데이터 투명성을 통해 예방 투자에 대한 ROI를 경영진에게 가시화할 수 있기 때문에 고성능 소독제를 조기에 도입하는 경향이 있습니다.

수술 건수 증가

수술 건수는 증가 추세에 있으며, 특히 외래수술센터(ASC)의 경우 감염률이 0.1%(병원 1% 대비)에 불과할 정도로 낮은 수준입니다. 이러한 성공은 빠른 수술실 회전을 위한 전문적인 소독 프로토콜에 대한 의료기관의 신뢰를 높이고 있습니다. 외래수술센터(ASC)에 맞게 포장 크기와 접촉 시간을 조정한 공급업체는 기존 병원용 제품 라인과 직접 경쟁하지 않고도 소독제 및 살균제 시장에서 점유율을 확보할 수 있습니다.

엄격한 규제 요건

미국 환경보호청(EPA)은 에틸렌옥사이드 살균기 배출량을 90% 감축하도록 의무화했습니다. 이는 미국 내 의료기기 멸균의 약 절반에 영향을 미칩니다. 컴플라이언스 비용으로 인해 병원에서는 저온 대체법 도입을 검토하고 있습니다. 새로운 견해에 따르면, 이러한 대체 방법을 채택하는 시설은 동일한 공급업체에서 제공하는 호환 가능한 표면 소독제를 표준으로 채택하는 경향이 있어 공급업체에 대한 의존도가 높아질 수 있다고 합니다.

부문 분석

시장 규모 추정에 따르면, 2025년 기준 4급 암모늄 화합물(QAC)은 소독제 및 살균제 시장의 27.45%를 차지할 것으로 예상되며, 효소 기반 제품은 2031년까지 8.75%의 가장 빠른 CAGR을 나타낼 것으로 예측됩니다. 병원들은 QAC의 잔류 효과를 평가하고 있지만, 규제 당국의 감시 강화로 인해 독성 잔류물을 남기지 않고 바이오필름을 분해하는 효소 배합 제품으로의 조달 전환이 진행되고 있습니다. QAC와 효소를 결합한 제제는 효과와 환경 목표를 모두 충족하는 과도기적 제품 라인을 제공할 수 있을 것으로 추측됩니다.

염소 화합물과 알코올-알데히드 혼합물은 저렴한 비용과 빠른 효과로 인해 고빈도 와이프다운 용도로 계속 활용되고 있습니다. 클로르헥시딘과 같은 비구아니드계 약제는 높은 살균 지속성으로 인해 수술 전 피부 소독에 여전히 선호되고 있습니다. 여기서 시사하는 바는 전체 시장의 흐름이 친환경 솔루션으로 전환되더라도 임상 프로토콜과 연계된 틈새 화학물질은 그 존재의미를 유지한다는 것입니다.

2025년 기준 소독제 및 살균제 시장 규모에서 액제는 51.10%를 차지할 것으로 예상되며, 물티슈는 9.05%의 예측 CAGR을 나타낼 것으로 예상되며, 병원이 용량 조절이 가능한 일회용 형태를 선호할 것으로 보입니다. 새로운 제안으로, 물티슈는 환자 수와 단위 수가 밀접하게 연동되어 재고 관리를 지원하고 예산 편성을 단순화합니다.

광범위한 응급 오염 제거에는 스프레이가 여전히 인기가 있지만, 만성 상처 클리닉에서는 소독과 치유 효과를 겸비한 젤과 폼이 인기를 끌고 있습니다. 폼 포장은 수직면이나 불규칙한 표면에 정밀하게 적용할 수 있어 낭비를 줄이고 고객의 가치 인식을 높일 수 있다는 추론이 도출됩니다.

지역별 분석

북미는 2025년 소독제 및 살균제 시장의 37.60%를 차지하며 선두를 유지할 것입니다. 이는 의료 관련 감염(HAI)에 대한 높은 처벌과 에틸렌옥사이드 배출을 규제하는 새로운 EPA 규정에 의해 촉진되고 있습니다. EPA와 FDA의 규제 정합성으로 기술 업그레이드 의사결정 주기가 단축되고 제품 업데이트 속도가 빨라지고 있습니다. 캘리포니아 등 감염자 수가 가장 많은 주에 있는 병원들은 공식적인 보고 의무가 경영진에게 압박을 가하기 때문에 빠르게 대응하는 경향이 있습니다.

아시아태평양은 9.12%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장률을 보이고 있으며, 대규모 병원 건설과 손 위생을 중시하는 문화가 주도하고 있습니다. 현지 생산은 증가하고 있지만 중환자실에서는 여전히 고급 수입품이 주류를 이루고 있어 품질 인식의 격차를 시사하고 있습니다. 세계 브랜드가 지방 도시에 진출할 경우, 현지 경쟁업체가 배합 기준을 개선하기 전에 점유율을 확보할 수 있습니다.

유럽에서는 엄격한 환경독성 기준과 감염 위험이 높은 고령 인구 증가를 배경으로 꾸준한 성장세를 유지하고 있습니다. 조달 정책은 휘발성유기화합물(VOC) 저감 제품을 우선시하고 있으며, 제조업체는 기존 제품의 재배합을 장려하고 있습니다. EU의 환경규제는 사실상 세계 표준이 되는 경우가 많으며, 조기 대응은 다른 규제 시장에 대한 수출 우위로 이어집니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The Antiseptics and Disinfectants market was valued at USD 40.88 billion in 2025 and estimated to grow from USD 44.17 billion in 2026 to reach USD 64.97 billion by 2031, at a CAGR of 8.05% during the forecast period (2026-2031).

Current spending patterns reveal a clear correlation between infection-control budgets and the financial penalties hospitals incur for healthcare-associated infections (HAIs). Capital allocations for preventive technologies are rising faster than for therapeutic drugs, reflecting a strategic preference for prevention over cure in hospital purchasing departments. The scale of the opportunity is reinforced by the large installed base of high-touch surfaces and reusable medical devices that require disinfection multiple times daily. Consistent market expansion suggests that demand is broadly resilient to economic slowdowns, as infection control is a non-discretionary purchase for healthcare providers. Manufacturers are therefore prioritizing production capacity for hospital-grade products, even as demand from consumer segments grows.

Regulatory scrutiny is accelerating rather than dampening demand, because providers prefer compliant, next-generation chemistries that are less likely to trigger future penalties. The United States Environmental Protection Agency's 90 % emission reduction mandate for ethylene oxide sterilizers, finalised in March 2024 is a prime example: it has pushed purchasers toward low-residue enzymatic blends and vaporised hydrogen peroxide systems . Intellectual property portfolios built around these alternatives are commanding premium valuations in mergers and acquisitions, reflecting a strategic shift toward safer, greener options. Investors also note the long useful life of hospital infrastructure, which locks in repeat sales of compatible formulations, suggesting that actual growth may exceed the headline 8 % CAGR if economic headwinds remain modest.

Global Antiseptics And Disinfectants Market Trends and Insights

Growing Incidences of Hospital Acquired Infections

HAIs continue to climb, with European facilities reporting 8.9 million annual cases, placing budgetary strain on public and private hospitals alike . Hospitals face lost revenue per infection episode, so prevention budgets are receiving priority, which in turn sustains growth in the Antiseptics and Disinfectants market. Facilities with advanced surveillance programs tend to adopt high-performance disinfectants early because data transparency makes the ROI on prevention visible to management.

Increasing Number of Surgical Procedures

Surgical volumes are rising, particularly in ambulatory surgery centers (ASCs) where infection rates sit at just 0.1 % compared with 1 % in hospitals. This success raises institutional confidence in specialized disinfectant protocols designed for rapid room turnover. Suppliers that tailor packaging sizes and contact times for ambulatory surgery centers can gain Antiseptics and Disinfectants market share without direct head-to-head competition with incumbent hospital product lines.

Stringent Regulatory Requirements

The Environmental Protection Agency (EPA) has mandated 90% emission cuts for ethylene oxide sterilizers, affecting roughly half of all device sterilization in the United States. Compliance costs encourage hospitals to trial on-site low-temperature alternatives. A fresh inference is that facilities adopting such alternatives will standardize on compatible surface disinfectants from the same suppliers, reinforcing vendor stickiness.

Other drivers and restraints analyzed in the detailed report include:

- Rising Awareness of Hygiene and Infection Control

- Growth in Healthcare Sector and Hospital Admissions

- Issues Related to Sterilization and Disinfectants of Advanced Medical Instruments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Market size estimates show Quaternary Ammonium Compounds (QACs) hold 27.45 % Antiseptics and Disinfectants market share in 2025, while enzymes record the fastest CAGR of 8.75 % through 2031. Hospitals value QACs for residual activity, but growing regulatory attention is nudging procurement teams toward enzymatic blends that degrade biofilms without leaving toxic residues. A clear inference is that formulators combining QACs with enzymes could offer a transitional product line that meets both efficacy and environmental goals.

Chlorine compounds and alcohol-aldehyde mixes continue serving high-frequency wipe-down tasks thanks to low cost and rapid action. Biguanides such as chlorhexidine remain favored for pre-operative skin prep owing to extended bactericidal persistence. The inference here is that niche chemicals sustain relevance when tied to clinical protocols, even if overall market momentum shifts toward greener solutions.

Liquids account for 51.10 % of Antiseptics and Disinfectants market size in 2025, but wipes display a 9.05% forecast CAGR as hospitals seek dose-controlled, single-use formats. The fresh inference is that wipes also aid inventory control because unit counts align closely with patient volumes, simplifying budgeting.

Sprays remain popular for emergency decontamination of wide areas, while gels and foams gain favor in chronic-wound clinics for their combined disinfectant and healing attributes. An inference is that foam packaging allows precise application on vertical or irregular surfaces, reducing wastage and boosting perceived value.

The Antiseptics and Disinfectants Market Report is Segmented by Product Type (Quaternary Ammonium Compounds, Chlorine Compounds, and More), Formulation (Liquid, Wipes, and More), Application (Enzymatic Cleaners, Medical Device Disinfectants, More), End User (Hospitals & Clinics, Ambulatory & Day-Surgery Centers, and Others), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America leads with 37.60% Antiseptics and Disinfectants market share in 2025, fueled by high HAI penalties and new EPA rules curbing ethylene oxide emissions. Regulatory alignment between the EPA and FDA is compressing decision cycles for technology upgrades, accelerating product replacement rates. Hospitals in states with the highest infection counts, such as California, are often the first to move because public reporting pressures executive teams.

The Asia-Pacific region shows the fastest growth rate of 9.12% CAGR, driven by large-scale hospital construction and a cultural emphasis on hand hygiene. Local production is increasing, yet premium imports still dominate critical care units, indicating gaps in quality perception. Global brands entering tier-2 cities may gain share before local competitors improve formulation standards.

Europe maintains steady growth underpinned by stringent eco-toxicity standards and a large aging population susceptible to infections. Procurement policies favor products with reduced volatile organic compounds, incentivizing manufacturers to reformulate legacy lines. EU environmental rules often serve as de facto global benchmarks, and early compliance can provide export advantages in other regulated markets.

- Solventum Corporation

- STERIS

- Ecolab

- Reckitt Benckiser Group

- The Clorox Company

- Procter & Gamble

- SC Johnson Professional

- Johnson & Johnson

- Cardinal Health

- Schulke & Mayr GmbH

- Metrex Research, LLC

- GlaxoSmithKline

- Molnlycke Health Care

- Pal International Ltd.

- Diversey Holdings, Ltd.

- GOJO Industries, Inc.

- Zep Inc.

- Kimberly-Clark Worldwide

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Incidences Of Hospital Acquired Infections

- 4.2.2 Increasing Number Of Surgical Procedures

- 4.2.3 Rising Awareness Of Hygeiene And Infection Control

- 4.2.4 Mandatory Endoscope Reprocessing Standards Strengthening High-Level Disinfectant Uptake

- 4.2.5 Growth In The Healthcare Sector And Hospital Admissions

- 4.2.6 Innovative Production Formulations And Technologies

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Requirements

- 4.3.2 Issues Related To The Sterilization And Disinfectants Of Advanced Medical Instruments

- 4.3.3 Volatile Quaternary Ammonium Compound Feedstock Costs

- 4.3.4 Shift To Single-Use Instruments Shrinking Reusable Disinfection Volumes

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Quaternary Ammonium Compounds

- 5.1.2 Chlorine Compounds

- 5.1.3 Alcohols & Aldehydes

- 5.1.4 Biguanides & Iodine Derivatives

- 5.1.5 Enzymes

- 5.1.6 Phenolic & Others

- 5.2 By Formulation

- 5.2.1 Liquids

- 5.2.2 Sprays & Aerosols

- 5.2.3 Wipes

- 5.2.4 Gels & Foams

- 5.3 By Application

- 5.3.1 Surface Disinfectants

- 5.3.2 Medical Device Disinfectants

- 5.3.3 Enzymatic Cleaners

- 5.3.4 Skin & Wound Antiseptics

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory & Day-Surgery Centers

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Solventum Corporation

- 6.3.2 STERIS plc

- 6.3.3 Ecolab Inc.

- 6.3.4 Reckitt Benckiser Group plc

- 6.3.5 The Clorox Company

- 6.3.6 Procter & Gamble Co.

- 6.3.7 SC Johnson Professional

- 6.3.8 Johnson & Johnson

- 6.3.9 Cardinal Health Inc.

- 6.3.10 Schulke & Mayr GmbH

- 6.3.11 Metrex Research, LLC

- 6.3.12 GSK plc

- 6.3.13 Molnlycke Health Care AB

- 6.3.14 Pal International Ltd.

- 6.3.15 Diversey Holdings, Ltd.

- 6.3.16 GOJO Industries, Inc.

- 6.3.17 Zep Inc.

- 6.3.18 Kimberly-Clark Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment