|

시장보고서

상품코드

1934756

아시아태평양의 드론 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

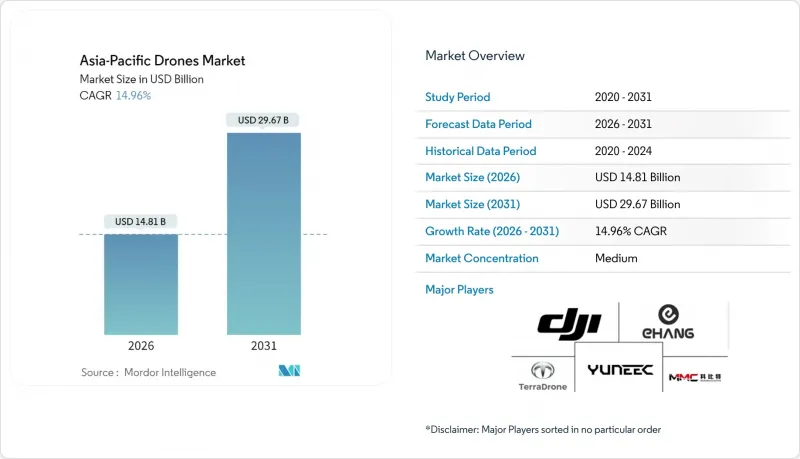

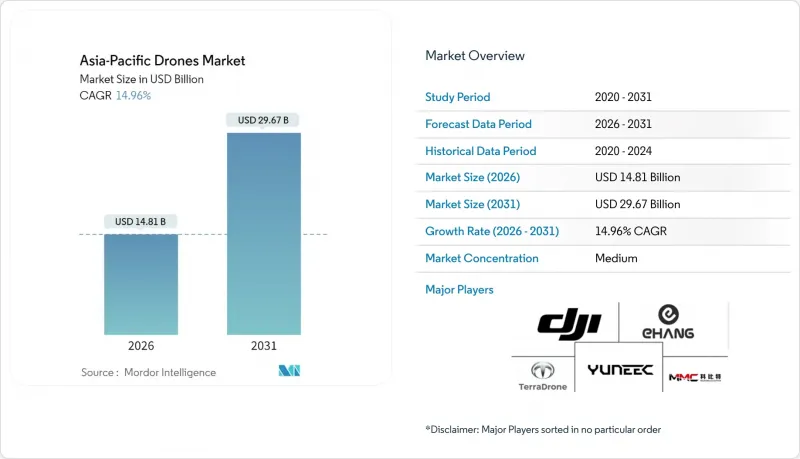

아시아태평양의 드론 시장은 2025년 128억 8,000만 달러에서 2026년에는 148억 1,000만 달러로 성장하고, 2026-2031년 CAGR 14.96%로 성장을 지속하여, 2031년까지 296억 7,000만 달러에 이를 것으로 예측됩니다.

공공 부문의 강력한 인센티브, 확대되는 기업용 이용 사례, 안정적인 센서 비용 감소로 인해 아시아태평양의 드론 시장은 두 자릿수 성장의 뚜렷한 성장 기반을 갖추고 있습니다. 건설 모니터링, 정밀 농업, 도시 물류가 상업적 수요의 기반이 될 것입니다. 동시에 중국 정부의 '저고도 경제'에 대한 정책적 지원은 현지 생산과 수출의 모멘텀을 증폭시키고 있습니다. 이와 함께 인도 시장이 2024 회계연도(FY2024) 5억 달러에서 2030 회계연도(FY2030) 110억 달러 규모로 확대될 것이라는 전망은 아시아태평양의 드론 시장의 결정적인 지리적 다변화를 보여줍니다. 예측 기간 동안 자율 소프트웨어, 하이브리드/VTOL 설계 혁신, 다양한 배터리 화학 기술이 공급업체 간 차별화를 촉진할 가능성이 높습니다.

아시아태평양의 드론 시장 동향과 인사이트

상업용 UAV 도입을 위한 정부 우대 조치

주요 경제권의 정책 이니셔티브는 규제 리드 타임 단축과 소유 비용 절감을 촉진하고 있습니다. 중국은 2024년 정부 활동 보고서에 저고도 경제를 명시하고, 수직 이착륙장(버티포트)과 디지털 항공 교통 인프라에 대한 자금을 배정했습니다. 일본은 2023년도에 방위성 연구개발 파트너십을 30개 프로젝트로 두 배로 늘리고, 민군겸용 드론 플랫폼에 자금을 집중하고 있습니다. 인도에서는 최대 4억 7,000만 달러의 신규 투자가 승인되었으며, 세제 혜택과 수입 대체 의무를 통해 국내 기체 생산을 촉진하고 있습니다. 호주의 '첨단 항공 모빌리티 전략' 초안은 상호 운용 가능한 규칙 체계를 수립하고, 아시아태평양의 드론 사업자가 아비오닉스의 재설계 없이 국경을 넘나드는 비행을 가능하게 하는 방침을 제시하고 있습니다. 이러한 프레임워크는 총 소유비용을 국내 제조업체에 유리하게 만들고, 국제 표준 설정을 가속화할 것입니다.

정밀농업 프로그램의 빠른 보급

농업 분야의 시범 사업에서 대규모 살포 및 영상 촬영으로 전환하면서 아시아태평양의 드론 시장은 구조적인 호황을 누리고 있습니다. 중국에는 현재 약 22만 대의 농업용 무인항공기가 운영되고 있으며, 국토의 3분의 1에 달하는 농지를 관리하고 있습니다. AI 탑재 멀티 스펙트럼 분석 기술을 통해 농약 사용량을 30% 절감하고, 수확량 향상을 실현하고 있습니다. 동남아시아의 쌀 재배 지역에서는 자동 관개 시스템을 통해 물 사용량을 25% 절감하면서 곡물의 품질을 유지하고 있습니다. 호주의 광활한 밀밭에서 드론이 가변 비율 비료 시비 구역을 실시간으로 매핑합니다. 농촌 지역의 노동력 이동으로 인해 이러한 효율성은 즉각적인 비용 절감으로 이어져 아시아태평양의 드론 시장에서 연평균 16.32%의 지속적인 연평균 성장률(CAGR)을 보일 것으로 예측됩니다.

대도시 지역의 항공 교통 관리의 병목현상

기존의 항공 교통 관제 시스템은 유인 항공을 우선시하고 수천 개의 저고도 경로를 동적으로 조정할 수 없습니다. 서울시의 도심항공모빌리티(UAM) 계획은 디지털 분리 기준이 없으면 드론이 속도 우위를 잃는 오프 피크 시간대로 밀려날 수 있음을 보여줍니다. 뭄바이와 자카르타 공항 주변의 혼잡도 비슷한 문제를 드러내고 있습니다. 감지 및 회피 도구는 계산량이 많아 소규모 사업자에게는 비용 장벽이 될 수 있습니다. 따라서 아시아태평양의 드론 시장은 규모의 경제를 실현하기 위해 U-공간(유스페이스)의 빠른 전개에 의존하고 있습니다.

부문 분석

건설 분야는 현장 측량, 자재 추적, 안전 감사를 통한 즉각적인 투자 회수 효과로 인해 2025년 아시아태평양의 드론 시장 점유율의 34.74%를 차지했습니다. 고해상도 사진 측량은 4D BIM 대시보드에 정보를 제공하여 계약자가 진행 상황을 계획 기준선과 실시간으로 비교할 수 있도록 합니다. 일대일로 연선 클러스터에서 사업을 전개하는 기업들은 군집형 드론을 동시에 투입하여 토공 작업을 디지털화하여 지상 측량 노동력을 60% 절감하고 있습니다. 농업 분야는 15.88%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 분야로, 아시아태평양의 농업 솔루션용 드론 시장 규모는 10년 이내에 10억 달러 규모에 육박할 것으로 예측됩니다. 동남아시아의 협동조합은 멀티 스펙트럼 데이터를 활용하여 비료 투여를 자동화하고, 호주의 농부들은 수확량 지도를 중첩하여 가변 비율 파종을 미세 조정하고 있습니다.

두 번째 성장 분야는 수익원 다각화입니다. 전력회사는 LiDAR 탑재 드론을 이용한 송전선로 열화상 검사를 도입하여 계획정전 시간을 절반으로 줄였습니다. 미디어 플레이어은 관광 및 스포츠 이벤트에 대한 항공 촬영 생중계권으로 수익을 창출하고, 공공 안전 기관은 AI 기반 군중 분석을 도시 모니터링에 도입하고 있습니다. 이러한 기능과 모델의 상호 활용으로 아시아태평양의 드론 시장에서 활동하는 고정익 및 회전익 OEM 업체들의 주문이 꾸준히 증가하고 있습니다.

고정익 플랫폼은 2025년 기준 아시아태평양의 드론 시장 규모의 40.77%를 차지할 것으로 예상되며, 몇 시간 이상 지속 비행이 필요한 회랑 매핑, 농작물 조사, 파이프라인 순찰 등에 선호되고 있습니다. 그러나 하이브리드/VTOL 설계는 16.94%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다. 가스 터빈 하이브리드 eVTOL 프로토타입은 2024년 초에 호버링 테스트에 성공하여 배터리 구동기로는 달성할 수 없는 항속 성능을 달성했습니다. 도심 물류 사업자들은 활주로 인프라를 피할 수 있는 수직 이착륙 능력과 적재 효율을 극대화할 수 있는 고정익 순항 능력을 중시하고 있습니다.

회전익 항공기는 항속거리보다 호버링 정확도가 중요한 외벽 점검 및 긴급 대응 분야에서 틈새 시장을 유지하고 있습니다. 이러한 설계의 분화는 틸트 로터 메커니즘에서 분산형 전기 추진 시스템에 이르기까지 부품의 전문화를 촉진하고 아시아태평양의 드론 시장 공급업체 생태계를 풍요롭게 하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.05The Asia-Pacific drones market is expected to grow from USD 12.88 billion in 2025 to USD 14.81 billion in 2026 and is forecast to reach USD 29.67 billion by 2031 at 14.96% CAGR over 2026-2031.

Solid public-sector incentives, widening enterprise use cases, and steady sensor cost deflation give the Asia-Pacific drones market a clear runway for double-digit expansion. Construction surveillance, precision agriculture, and urban logistics to anchor commercial demand. At the same time, Chinese policy support for a "low-altitude economy" multiplies local production and export momentum. Concurrently, India's scale-up from USD 500 million in FY2024 to an expected USD 11 billion by FY2030 signals a decisive geographic diversification within the Asia-Pacific drones market. Over the forecast horizon, autonomy software, hybrid/VTOL design breakthroughs, and diversified battery chemistries will likely widen supplier differentiation.

Asia-Pacific Drones Market Trends and Insights

Government Incentives for Commercial UAV Adoption

Policy initiatives across leading economies are shrinking regulatory lead times and lowering ownership costs. China embedded the low-altitude economy in its 2024 Work Report, earmarking funds for vertiports and digital air-traffic infrastructure. Japan doubled Ministry of Defense R&D partnerships to 30 projects in fiscal 2023, channeling funds toward a dual-use drone platform. India cleared up to USD 470 million in new investment commitments, with fiscal perks and import-substitution mandates encouraging domestic airframe production. Australia's draft Advanced Air Mobility Strategy outlines interoperable rulesets that should let Asia-Pacific drone market operators fly cross-border without redesigning avionics. Together, these frameworks tilt the total ownership cost in favor of local manufacturers and accelerate international standard setting.

Rapid Proliferation of Precision-Agriculture Programs

The Asia-Pacific drones market gains structural tailwinds as farming shifts from pilot projects to fleet-scale spraying and imaging. China now fields about 220,000 agricultural UAVs that treat one-third of the national farmland. AI-enabled multispectral analytics trim pesticide volumes by 30% and deliver yield lifts. In Southeast Asian rice belts, automated irrigation routines cut water use by 25% while preserving grain quality. For Australian broad-acre wheat, drones map variable-rate fertilizer zones in real time. Labor migration from rural areas converts these efficiency gains into immediate cost offsets, ensuring sustained 16.32% segment CAGR inside the Asia-Pacific drones market.

Air-Traffic-Management Bottlenecks in Mega-Cities

Legacy ATC systems prioritize manned aviation and cannot dynamically de-conflict thousands of low-altitude paths. Seoul's urban-air-mobility roadmap shows that drones may be forced into off-peak slots that undermine promised speed advantages without digital separation standards. Congestion around Mumbai and Jakarta airports exposes similar gaps. Detect-and-avoid tooling adds heavy compute loads that present cost hurdles for smaller operators. The Asia-Pacific drones market, therefore, depends on accelerated U-space rollouts to unlock scale economics.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure-Monitoring Demand Along Belt and Road Projects

- Urban E-commerce BVLOS Delivery Pilots

- Limited Pool of Certified Commercial Drone Pilots

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Construction captured 34.74% of the Asia-Pacific drones market share in 2025, thanks to immediate ROI from site surveying, materials tracking, and safety audits. High-resolution photogrammetry feeds 4D BIM dashboards, letting contractors compare real-time progress against schedule baselines. Companies operating across Belt and Road clusters deploy swarms to digitize earthworks simultaneously, cutting ground survey labor by 60%. Agriculture follows as the fastest-growing vertical, expanding at 15.88% CAGR and moving the Asia-Pacific drones market size for farm solutions toward a USD-billion scale by decade-end. Southeast Asian cooperatives use multispectral data to automate fertilizer dosing, while Australian growers overlay yield maps to fine-tune variable-rate seeding.

Second-tier verticals add diversified revenue. Energy utilities deploy LiDAR-equipped drones for power-line thermography, halving mandatory outage durations. Media firms monetize aerial live-stream rights for tourism and sports events, and public-safety agencies embrace AI-driven crowd analytics for urban surveillance. This cross-pollination of features and models sustains healthy order books for both fixed-wing and rotary-wing OEMs operating within the Asia-Pacific drones market.

Fixed-wing platforms accounted for 40.77% of the Asia-Pacific drones market size in 2025, preferred for corridor mapping, crop scouting, and pipeline patrols that require multi-hour endurance. Yet, hybrid/VTOL designs are scaling at a 16.94% CAGR. Gas-turbine hybrid eVTOL prototypes demonstrated successful hover tests in early 2024, unlocking range profiles that battery-only craft cannot match. City-center logistics players value vertical take-off to avoid runway infrastructure and fixed-wing cruise to maximize payload economics.

Rotary-wing craft keep their niche in facade inspection and emergency response, where hover precision outranks range. The resulting design segmentation encourages component specialization-from tilt-rotor assemblies to distributed electric propulsion-that enriches supplier ecosystems inside the Asia-Pacific drones market.

The Asia-Pacific Drones Market Report is Segmented by Application (Construction, Agriculture, Energy, and More), Type (Fixed-Wing Drones, Rotary-Wing Drones, and More), Weight Class (Nano/Micro, Small, and More), Mode of Operation (Remotely Piloted, and More), End-User (Commercial and Consumer/Hobbyist, Government and Civil), and Country (China, India, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SZ DJI Technology Co., Ltd.

- Guangzhou EHang Intelligent Technology Co. Ltd.

- Terra Drone Corporation

- MicroMultiCopter (MMC) Aero Technology Co. Ltd.

- Yuneec International (ATL Drone)

- Shenzhen Hubsan Technology Co., Ltd.

- Garuda Aerospace Pvt. Ltd.

- XAG Co., Ltd.

- Chengdu JOUAV Automation Tech Co., Ltd.

- Autel Robotics Co., Ltd.

- Skydio, Inc.

- Parrot Drones SAS

- ideaForge Technology Ltd.

- Throttle Aerospace System Pvt. Ltd. (TAS)

- Primoco UAV SE

- Aerosense Inc.

- Motodoro UAV

- Alphaswift Industries Sdn Bhd

- MATA Aerotech Sdn Bhd

- Asteria Aerospace Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government incentives for commercial UAV adoption

- 4.2.2 Rapid proliferation of precision-agriculture programs

- 4.2.3 Infrastructure-monitoring demand along Belt and Road projects

- 4.2.4 Urban e-commerce BVLOS delivery pilots

- 4.2.5 Pay-per-flight insurtech coverage models

- 4.2.6 Falling LiDAR and multispectral sensor costs

- 4.3 Market Restraints

- 4.3.1 Air-traffic-management bottlenecks in mega-cities

- 4.3.2 Limited pool of certified commercial drone pilots

- 4.3.3 Lithium-cell supply risk from EV sector crowd-out

- 4.3.4 Escalating GNSS spoofing and jamming incidents

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Construction

- 5.1.2 Agriculture

- 5.1.3 Energy

- 5.1.4 Entertainment

- 5.1.5 Law-Enforcement

- 5.1.6 Other Applications

- 5.2 By Type

- 5.2.1 Fixed-Wing Drones

- 5.2.2 Rotary-Wing Drones

- 5.2.3 Hybrid/VTOL Drones

- 5.3 By Weight Class

- 5.3.1 Nano/Micro (Less than 2 kg)

- 5.3.2 Small (2-25 kg)

- 5.3.3 Medium (25-150 kg)

- 5.3.4 Large (Greater than 150 kg)

- 5.4 By Mode of Operation

- 5.4.1 Remotely Piloted

- 5.4.2 Optionally Piloted

- 5.4.3 Fully Autonomous

- 5.5 By End-User

- 5.5.1 Commercial and Consumer/Hobbyist

- 5.5.2 Government and Civil

- 5.6 By Country

- 5.6.1 China

- 5.6.2 India

- 5.6.3 Japan

- 5.6.4 South Korea

- 5.6.5 Australia

- 5.6.6 Indonesia

- 5.6.7 Singapore

- 5.6.8 Malaysia

- 5.6.9 Thailand

- 5.6.10 Vietnam

- 5.6.11 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes global overview, market overview, core segments, financials, strategic info, market rank/share, products and services, recent developments)

- 6.4.1 SZ DJI Technology Co., Ltd.

- 6.4.2 Guangzhou EHang Intelligent Technology Co. Ltd.

- 6.4.3 Terra Drone Corporation

- 6.4.4 MicroMultiCopter (MMC) Aero Technology Co. Ltd.

- 6.4.5 Yuneec International (ATL Drone)

- 6.4.6 Shenzhen Hubsan Technology Co., Ltd.

- 6.4.7 Garuda Aerospace Pvt. Ltd.

- 6.4.8 XAG Co., Ltd.

- 6.4.9 Chengdu JOUAV Automation Tech Co., Ltd.

- 6.4.10 Autel Robotics Co., Ltd.

- 6.4.11 Skydio, Inc.

- 6.4.12 Parrot Drones SAS

- 6.4.13 ideaForge Technology Ltd.

- 6.4.14 Throttle Aerospace System Pvt. Ltd. (TAS)

- 6.4.15 Primoco UAV SE

- 6.4.16 Aerosense Inc.

- 6.4.17 Motodoro UAV

- 6.4.18 Alphaswift Industries Sdn Bhd

- 6.4.19 MATA Aerotech Sdn Bhd

- 6.4.20 Asteria Aerospace Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment