|

시장보고서

상품코드

1934777

인공 피부 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Artificial Skin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

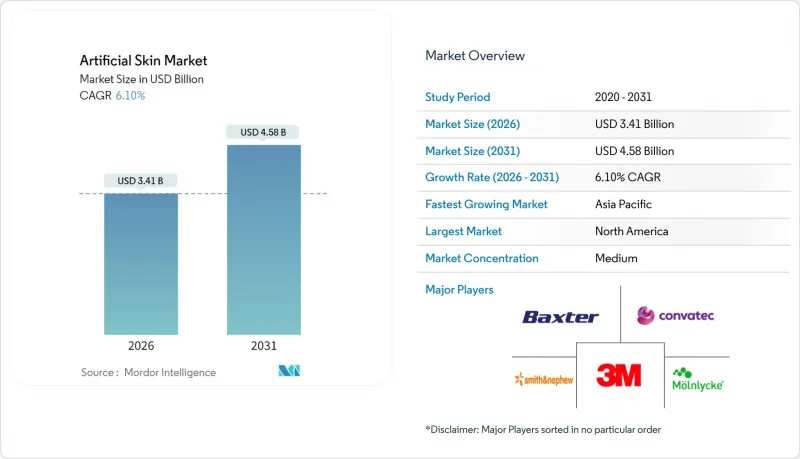

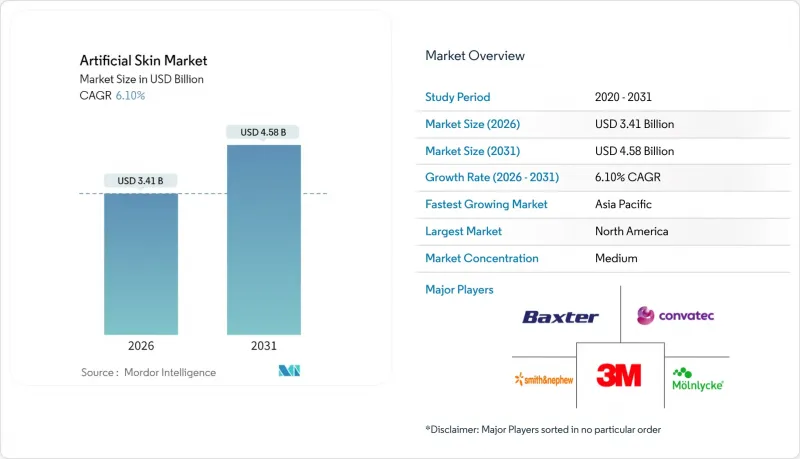

인공 피부 시장은 2025년 32억 1,000만 달러에서 2026년에는 34억 1,000만 달러로 성장하며, 2026-2031년에 CAGR 6.1%로 추이하며, 2031년까지 45억 8,000만 달러에 달할 것으로 예측되고 있습니다.

이러한 성장세는 치료기간 단축과 임상 적응 범위 확대를 실현하는 3D 바이오프린팅, 스마트 바이오소재, AI 탑재 전자피부 플랫폼의 시너지 효과에 기인합니다. 당뇨병성 족부 병변 관리, 욕창 예방, 미용 피부 재생 분야에서의 채택 가속화가 수요 기반 확대에 기여하고 있습니다. 병원에서는 이식편 실패와 재수술을 줄임으로써 총 의료비를 절감할 수 있으므로 고품질 복합 스커폴드를 지속적으로 조달하고 있습니다. 정액 상환제로의 규제 전환으로 제조업체들은 생산 자동화, 바이오 하이브리드 제품 파이프라인 확대, 위탁 개발 기업과의 효율화 파트너십 구축을 추진하고 있습니다. 연구기관과 의료기기 제조업체의 협력은 실험실에서의 획기적인 성과를 빠르게 상용 제품으로 전환하고, 가격 압박이 가중되는 상황에서도 높은 한 자릿수 성장률을 유지하는 데 기여하고 있습니다.

세계 인공피부 시장 동향과 전망

재생의료의 기술 혁신

AI 가이드형 3D 바이오프린팅 기술은 현재 마이크론 단위의 해상도로 생체 외 세포 매트릭스를 모방한 환자 특이적 래티스를 제작할 수 있습니다. 한국과학기술연구원 연구진은 무선 센서가 내장된 콜라겐-피브린 이식편으로 치유율을 120% 향상시켜 스마트 소재가 조직 수복과 생체역학적 피드백을 융합하는 방법을 제시했습니다. 그라나다 대학의 UGRSKIN 플랫폼은 2016년 이후 중증 화상 환자에서 약 80%의 생존율을 달성하여 중증 외상 치료에서 생세포 구조물의 유효성을 입증했습니다. 모공 모양과 사이토카인 농도 구배를 조정하는 정밀 소프트웨어를 통한 개인별 맞춤 치료는 인공피부 시장의 프리미엄 부문을 지원하고 있습니다. 지불자의 가격 감시가 강화되고 있는 가운데, 병원들은 이러한 성과를 높이 평가하여 처방약 리스트에 우선적으로 채택하고 있습니다.

만성 및 급성 피부 손상 증가 추세

당뇨병성 족부 궤양은 5억 4,000만 명 이상에게 영향을 미치며, 전 세계 상처 관리 비용을 연간 170억 달러 이상으로 증가시키고 있습니다. 바이오엔지니어링 어피 이식편은 16주 이내에 44%의 당뇨성 궤양을 폐쇄하여 절단 위험과 입원일수를 감소시켰으며, 표준 드레싱의 26%와 비교하여 16주 이내에 44%의 당뇨성 궤양을 폐쇄시켰습니다. 아시아 도시 지역의 교통사고와 산업 화상 증가는 즉각적인 피부 매트릭스에 대한 수요를 확대시키고 있습니다. 의료진은 조기 이식편 배치가 감염률을 낮추고 퇴원을 촉진한다는 증거를 지지하고 있으며, 이는 전체 인공피부 시장의 성장을 가속하고 있습니다.

고가의 치료비와 예산 제약

중증 화상 환자의 경우, 여러 번의 이식이나 중환자실(ICU) 입원이 겹치면서 환자 1인당 980만 달러가 넘는 경우도 있으며, 지불기관의 우려를 낳고 있습니다. 메디케어-메디케이드 서비스 센터(CMS)는 피부 대체재에 대한 상환액을 평방 센티미터당 125.38달러로 일괄 인하하는 안을 제시했습니다. 이는 기존의 높은 가격 책정을 부추기던 원가 가산 방식에서 급격한 전환입니다. 저소득 경제권의 의료 서비스 프로바이더들은 예산의 한계로 인해 도입이 늦어지는 경우가 많으며, 이는 인공피부 시장의 초기 침투를 제한하고 있습니다. 제조업체는 린 생산 방식을 가속화하고, 저가의 콜라겐 원료를 찾고, 가격 상한선 아래에서 이익률 유지를 위해 위탁 생산업체와 제휴를 추진하고 있습니다.

부문 분석

2025년 인공피부 시장에서 가장 큰 점유율(매출의 47.92%)을 차지한 분야는 임시 장치입니다. 이는 임상의들이 삼출물 조절과 감염 위험 감소를 통한 신속한 보호에 중점을 두고 있기 때문입니다. 비세포성이고 비용 효율적이며, 이러한 매트릭스는 상처가 진피층에 도달하면 후속 이식 수술이 필요합니다. 복합형 및 하이브리드형은 일시적인 표피층과 내구성 있는 진피층이 결합되어 수술 과정의 수를 줄이고 입원 기간을 단축하므로 현재 8.3%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. 병원에서는 기증자 부위의 합병증 위험을 줄이고 고통스러운 드레싱 교환을 최소화하는 통합적 접근 방식을 높이 평가하고 있으며, 이는 꾸준한 보급을 촉진하고 있습니다. 전기방사 및 용융전기도금 기술의 지속적인 연구개발로 단층 제품과의 비용 차이가 좁혀지고 있으며, 금세기 후반에는 하이브리드 플랫폼이 기존 제품을 추월할 수 있는 기반이 마련되고 있습니다. 이러한 전환은 임상의들이 즉각적인 피복과 장기 재생을 통합한 턴키 구조물로 전환하는 가운데 인공피부 시장의 전환점을 보여주고 있습니다.

2세대 이중층 필름은 생체 피부의 인장강도에 5% 이내의 정확도로 근접하여 이식 후 10일이라는 초기 단계의 혈관 침투를 촉진합니다. 자동화된 롤투롤 제조 기술로 균일한 기공 구조를 실현하여 체액 배출과 세포 이동을 개선했습니다. 이러한 기술적 진보로 인해 가격 개혁 이후에도 복합형 솔루션은 고빈도 화상 치료 부문의 보험 적용 리스트에 남아있을 것으로 예측됩니다. 한편, 영구적 인 전층 피부 대체품은 증후군 질환에서 틈새 시장을 차지하고 있지만, 생체 세포 공급원과 콜드체인 물류가 강화됨에 따라 꾸준히 성장하고 있습니다. 따라서 인공피부 산업은 이분법적 전환이 아니라 임상적 고도화의 폭이 넓어지는 것을 반영하고 있으며, 중증도에 관계없이 선택권을 유지하고 있습니다.

진피 매트릭스는 강도와 탄력을 제공하는 콜라겐이 풍부한 층을 재현하여 2025년 매출의 57.02%를 창출했습니다. 외과 의사들은 오랫동안 표피 자가 이식이 나중에 표면을 재건할 수 있으므로 진피 수복을 우선시해 왔습니다. 바이오리액터가 각질세포와 섬유아세포를 분리하지 않고 동일한 스캐폴드에서 공동 배양할 수 있게 됨에 따라 전층 이식편이 현재 8.52%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. 이 올인원 구조는 단계별 수술이 필요없고, 바쁜 외상 센터에서 중요시하는 효율성을 통해 수술 시간을 단축합니다. RECELL과 같은 시스템을 사용했을 때, 초기 도입 기관에서는 기증 부위가 27% 감소하여 합병증 위험 감소와 환자 만족도 향상에 기여한 것으로 보고되고 있습니다. 표피 전용 필름은 여전히 미용 목적의 피부 재생 및 경미한 화상 치료에 사용되고 있지만, 복합형 디바이스의 가격 하락에 따라 대체 위험에 직면해 있습니다.

향후 전망으로는 학술 컨소시엄에서 혈관생성 전 조립식 피부판막의 실험이 진행되고 있으며, 치료기간의 추가 단축이 기대되고 있습니다. 임상시험에서 우수한 생착률이 입증된다면, 심부열상 1차 치료로 전층 피부이식을 승인할 가능성이 있으며, 인공피부 시장 규모 계층내 구성비 변화가 가속화될 것으로 보입니다. 그러나 규제 데이터 요구사항이 여전히 엄격하므로 당분간은 진피 대체품이 시장 규모를 유지할 것으로 예측됩니다.

지역별 분석

북미는 탄탄한 외상 치료 인프라, 풍부한 상환 제도, 촘촘한 화상 센터 네트워크 덕분에 2025년 세계 매출의 40.10%를 차지할 것으로 예측됩니다. 미국은 최대 480제곱센티미터의 상처를 치료하고 자가 이식의 필요성을 줄여주는 RECELL GO mini 등 초기 FDA 승인으로 이 지역에서의 우위를 주도하고 있습니다. 캐나다와 멕시코는 후발주자이지만, 보편적 의료보험제도가 현대적 상처 치료 경로에 대한 투자를 늘리면서 꾸준히 성장하고 있습니다. 향후 지불자 개혁으로 단가는 압축될 가능성이 있지만, 적응증 확대를 통해 물량을 자극할 것으로 예측됩니다. 북미 인공피부 시장 규모는 고가의 생세포 이식을 저렴한 바이오하이브리드로 대체하는 혁신가들의 등장으로 치료 성과의 동등성을 유지하면서 한 자릿수 성장이 예상됩니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 7.28%로 세계에서 가장 빠르게 성장할 것으로 예측됩니다. 급속한 도시화, 고령화, 당뇨병 환자 증가는 치료 건수 증가를 지원하고, 정부는 보험 적용 범위를 확대하고 있습니다. 중국은 '중국제조' 정책의 인센티브 하에 국내 바이오프린팅 사업 추진을 통해 자급자족과 수출 가능성을 추구하고 있습니다. 일본은 첨단 조직공학 규제를 유지하고, 검증된 구조물의 승인을 앞당겨 조기 도입을 지원하고 있습니다. 인도와 인도네시아에서는 여전히 저렴한 가격이 문제이지만, 민관 협력을 통해 주요 간선도로변 외상센터에 보조 이식편을 공급하는 것을 목표로 하고 있습니다. 규모 확대에 따라 현지 생산을 통한 물류 비용 절감과 가격 민감 시장 지원이 진행되어 인공피부 시장에서 아시아태평양의 전략적 성장 동력으로서의 입지가 강화될 것으로 예측됩니다.

유럽은 성숙한 의료 시스템과 조정된 외상 네트워크로 인해 큰 점유율을 차지하고 있습니다. 독일과 프랑스는 증거에 기반한 조달을 우선시하며, 무작위 시험으로 입증된 제품을 선호합니다. 이 지역의 엄격한 의료기기 규제는 높은 문서화를 요구하지만, 임상의에게 제품 품질을 보장하고 꾸준한 보급을 유지하고 있습니다. 동유럽 국가들은 결속 기금을 활용하여 화상 치료 부문을 업그레이드하고 점차적으로 수요를 창출하고 있습니다. 중동 및 아프리카 및 남미는 아직 개발 중이지만 유망한 시장입니다. 부유한 걸프 지역 국가들은 복잡한 미용 수술용 고급 제품을 수입하는 반면, 브라질은 사고 피해자를 위한 이식편을 국민건강보험에 포함시키고 있습니다. 환율 변동과 보험 적용 범위의 제한으로 보급이 늦어지고 있는 가운데, 인도적 지원 프로젝트에서는 화상 피해가 빈번한 분쟁지역에서 복합 이식편이 간혹 활용되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

The artificial skin market is expected to grow from USD 3.21 billion in 2025 to USD 3.41 billion in 2026 and is forecast to reach USD 4.58 billion by 2031 at 6.1% CAGR over 2026-2031.

The upward path reflects synergistic gains from 3D bioprinting, smart biomaterials and AI-enabled electronic skin platforms that shorten healing times and widen clinical indications. Accelerated adoption in diabetic foot management, pressure-injury prevention and cosmetic resurfacing adds breadth to the demand base. Hospitals continue to procure premium composite scaffolds because they lower total cost of care by reducing graft failures and revision surgeries. Regulatory moves to flat-rate reimbursement are prompting manufacturers to automate production, expand bio-hybrid pipelines and cultivate efficiency partnerships with contract developers. Collaboration between research institutes and device firms speeds translation of laboratory breakthroughs into commercial products, helping preserve high single-digit growth even as pricing pressure intensifies.

Global Artificial Skin Market Trends and Insights

Technological Innovations in Regenerative Medicine

AI-guided 3D bioprinting now fabricates patient-specific lattices that mimic native extracellular matrices at micron resolution. Korea Institute of Science and Technology researchers achieved a 120% uplift in healing rates with wireless sensor-embedded collagen-fibrin grafts, showing how smart materials merge tissue repair with biomechanical feedback. The University of Granada's UGRSKIN platform has shown nearly 80% survival in major burn patients since 2016, validating living-cell constructs in severe trauma care. Precision software that tailors pore geometry and cytokine gradients personalizes therapy, supporting the premium segment of the artificial skin market. Hospitals reward these outcomes with formulary preference even while payer scrutiny on price intensifies.

Increasing Incidence of Chronic and Acute Skin Injuries

Diabetic foot ulcers affect more than 540 million people, driving annual global wound-management costs above USD 17 billion. Bioengineered fish-skin grafts closed 44% of diabetic ulcers within 16 weeks versus 26% under standard dressings, cutting amputation risk and inpatient days. Rising traffic trauma and industrial burns in urban Asia amplify demand for fast-acting dermal matrices. Providers embrace evidence that early graft placement reduces infection rates and accelerates discharge, reinforcing growth across the artificial skin market.

High Treatment Costs and Budget Constraints

Extreme burn cases can exceed USD 9.8 million per patient when multiple grafts and ICU stays accumulate, prompting payer alarm. The Centers for Medicare & Medicaid Services has proposed cutting skin-substitute reimbursement to a flat USD 125.38 per square centimeter, a sharp shift from cost-plus formulas that previously encouraged premium pricing. Providers in low-income economies often delay adoption due to budget caps, limiting early-stage penetration of the artificial skin market. Manufacturers accelerate lean manufacturing, seek lower-cost collagen sources and partner with contract producers to preserve margins under price ceilings.

Other drivers and restraints analyzed in the detailed report include:

- Rising Geriatric and Diabetic Population

- Growing Demand for Advanced Wound Care Solutions

- Stringent Multiregional Regulatory Frameworks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Temporary devices retained the largest slice of the artificial skin market in 2025 at 47.92% revenue because clinicians rely on them for prompt protection that controls exudate and lowers infection risk. Although non-cellular and cost-effective, these matrices require follow-up grafting when wounds penetrate the dermis. Composite and hybrid formats are now rising at an 8.3% CAGR as they combine a temporary epidermal layer with a durable dermal scaffold, reducing the number of surgical steps and shortening hospital stay. Hospitals value the integrated approach because it cuts donor-site morbidity and minimizes painful dressing changes, propelling steady uptake. Continuous R&D in electrospinning and melt-electrowriting is closing the cost gap with single-layer products, setting the stage for hybrid platforms to overtake incumbents later in the decade. The transition signals an inflection point for the artificial skin market as clinicians gravitate toward turnkey constructs that fuse immediate coverage with long-term regeneration.

Second-generation bilayer films exhibit tensile strength within 5% of native human skin and support vascular ingrowth as early as day 10 post-implantation. Automated roll-to-roll fabrication now produces homogenous pore structures that improve fluid drainage and cell migration. These technical gains will likely keep composite solutions on the reimbursement formularies of high-volume burn units even after pricing reform. Meanwhile, permanent full-take skin substitutes hold a niche in syndromic conditions yet grow steadily as living-cell sourcing and cold-chain logistics become more robust. The artificial skin industry therefore reflects a widening ladder of clinical sophistication rather than a binary shift, preserving choice across acuity levels.

Dermal matrices generated 57.02% of 2025 revenue by recreating the collagen-rich layer that provides strength and elasticity. Surgeons have long targeted dermal repair first because epidermal autografts can later repopulate the surface. Full-thickness grafts are expanding fastest at an 8.52% CAGR now that bioreactors can co-culture keratinocytes and fibroblasts on the same scaffold without delamination. These all-in-one constructs reduce operative time by eliminating staged procedures, an efficiency prized in busy trauma centers. Early adopters report 27% smaller donor sites when using systems such as RECELL, easing morbidity and improving patient satisfaction. Epidermal-only films still serve cosmetic resurfacing and minor burns but face substitution risk as composite devices fall in price.

Looking ahead, academic consortia are experimenting with vascularized pre-assembled skin flaps that may further compress treatment timelines. If trials validate superior graft-take rates, reimbursement committees could endorse full-thickness options as first-line therapy for deep burns, accelerating their mix shift within the artificial skin market size hierarchy. However, regulatory data requirements remain high, so dermal substitutes will retain scale for the foreseeable future.

The Artificial Skin Market Report is Segmented by Product Type (Permanent, Temporary, and Composite/Hybrid), Replacement Area (Dermal, Epidermal, and Full-Thickness), Material (Natural, Synthetic, and Bio-Hybrid), Application (Acute Wounds, and More), End-User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 40.10% of 2025 global revenue thanks to robust trauma care infrastructure, generous reimbursement and a dense network of burn centers. The United States drives regional dominance with early FDA clearances such as RECELL GO mini, which treats wounds up to 480 cm2 and reduces autograft requirements. Canada and Mexico trail but grow steadily as universal healthcare systems invest in modern wound-care pathways. Upcoming payer reforms may compress unit prices yet also stimulate volume through broadened indications. The artificial skin market size for North America is forecast to advance in single digits as innovators substitute costly living-cell grafts with cheaper bio-hybrids that retain outcome parity.

Asia-Pacific is projected to post a 7.28% CAGR to 2031, the fastest worldwide. Rapid urbanization, aging populations and rising diabetes prevalence underpin high procedure volumes, while governments expand insurance coverage. China pushes domestic bioprinting ventures under Made-in-China policy incentives, seeking self-sufficiency and export potential. Japan maintains sophisticated tissue-engineering regulations that accelerate approval of proven constructs, helping early adoption. India and Indonesia still face affordability hurdles, but public-private partnerships aim to supply subsidized grafts for trauma centers along major highway corridors. As scale rises, localized production will trim logistics costs and support price-sensitive markets, reinforcing APAC as a strategic growth engine within the artificial skin market.

Europe holds significant share via mature healthcare systems and coordinated trauma networks. Germany and France prioritize evidence-based purchasing, favoring products backed by randomized trials. The region's strict Medical Device Regulation imposes high documentation but assures clinicians of product quality, sustaining steady uptake. Eastern European nations leverage cohesion funds to upgrade burn units, creating incremental demand. Middle East & Africa and South America remain nascent yet promising. Wealthier Gulf states import premium constructs for complex cosmetic surgeries, whereas Brazil integrates grafts into its Unified Health System for accident victims. Exchange-rate volatility and limited reimbursement slow broader penetration, though humanitarian aid projects occasionally deploy composite grafts in conflict zones where burn injuries are prevalent.

- 3M

- Smiths Group

- Integra LifeSciences

- Baxter

- Convatec Group

- Molnlycke Health Care

- Medtronic

- Hartmann Group

- MIMEDX Group

- Bioventus (Solsys Medical)

- Organogenesis Holdings

- Avita Medical

- Episkin (L'Oreal)

- Stratatech (Mallinckrodt)

- Tissue Regenix

- PolarityTE

- RenovaCare

- Gunze Limited

- Vericel

- TissUse

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological Innovations in Regenerative Medicine

- 4.2.2 Increasing Incidence of Chronic and Acute Skin Injuries

- 4.2.3 Rising Geriatric and Diabetic Population

- 4.2.4 Growing Demand for Advanced Wound Care Solutions

- 4.2.5 Favorable Government Funding and Reimbursement Policies

- 4.2.6 Expanding Applications in Aesthetic and Robotic Fields

- 4.3 Market Restraints

- 4.3.1 High Treatment Costs and Budget Constraints

- 4.3.2 Stringent Multiregional Regulatory Frameworks

- 4.3.3 Limited Vascularization and Integration Challenges

- 4.3.4 Supply Chain Vulnerability for Biological Raw Materials

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Intensity Of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Permanent

- 5.1.2 Temporary

- 5.1.3 Composite / Hybrid

- 5.2 By Replacement Area

- 5.2.1 Dermal

- 5.2.2 Epidermal

- 5.2.3 Full-Thickness (Composite)

- 5.3 By Material

- 5.3.1 Natural (Collagen, Fibrin, Etc.)

- 5.3.2 Synthetic (PGA, PCL, PU, Etc.)

- 5.3.3 Bio-Hybrid

- 5.4 By Application

- 5.4.1 Acute Wounds (Burns, Trauma)

- 5.4.2 Chronic Wounds (Diabetic Ulcers, Pressure Ulcers)

- 5.4.3 Cosmetic & Aesthetic Procedures

- 5.5 By End-User

- 5.5.1 Hospitals

- 5.5.2 Specialised Burn & Wound-Care Centres

- 5.5.3 Ambulatory Surgical Centres

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M Company

- 6.3.2 Smith & Nephew Plc

- 6.3.3 Integra Lifesciences Corporation

- 6.3.4 Baxter International Inc.

- 6.3.5 Convatec Group

- 6.3.6 Molnycke Health Care AB

- 6.3.7 Medtronic

- 6.3.8 Paul Hartmann AG

- 6.3.9 MiMedX

- 6.3.10 Bioventus (Solsys Medical)

- 6.3.11 Organogenesis Holdings

- 6.3.12 Avita Medical

- 6.3.13 Episkin (L'Oreal)

- 6.3.14 Stratatech (Mallinckrodt)

- 6.3.15 Tissue Regenix

- 6.3.16 PolarityTE

- 6.3.17 RenovaCare

- 6.3.18 Gunze Limited

- 6.3.19 Vericel Corporation

- 6.3.20 TissUse GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment