|

시장보고서

상품코드

1934808

목탄 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Charcoal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

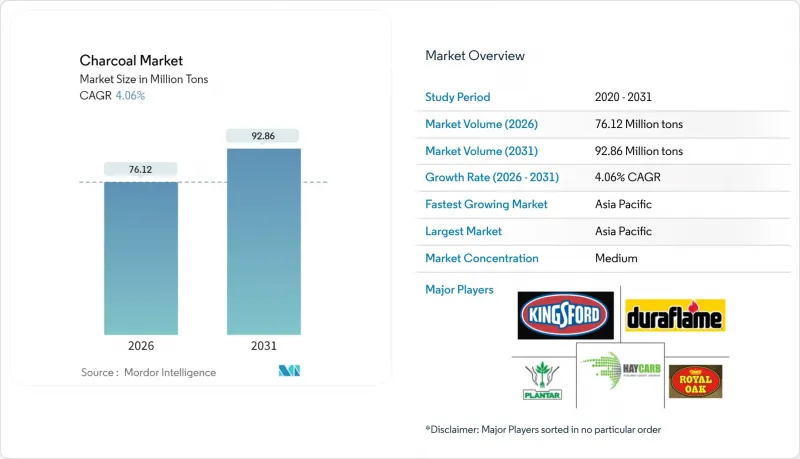

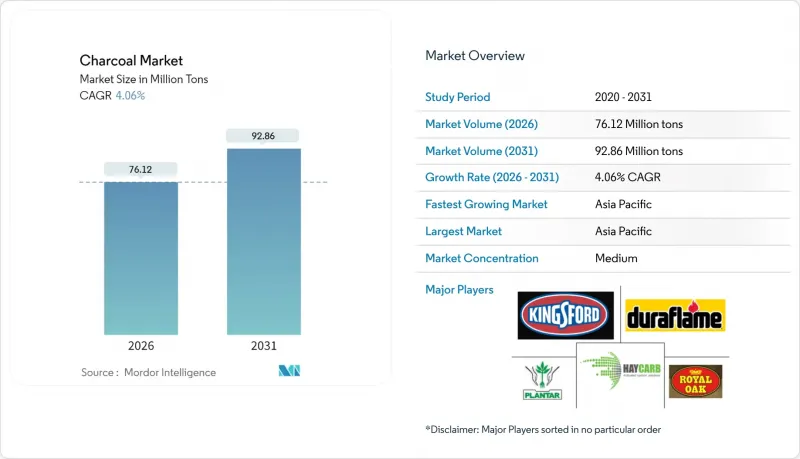

목탄 시장은 2025년 7,315만 톤에서 2026년에는 7,612만 톤으로 성장하며, 2026-2031년에 CAGR 4.06%로 추이하며, 2031년까지 9,286만 톤에 달할 것으로 예측되고 있습니다.

이러한 성장은 신흥 국가에서의 가정 요리용 숯에 대한 지속적인 의존도와 선진국의 바비큐 및 활성탄 응용 분야에서의 프리미엄 부문 성장이라는 두 가지 대조적인 요인에 의해 형성되었습니다. 공급망은 EU 삼림파괴 규제와 관련된 지속가능성 감사에 대한 수요 증가에 대응하기 위해 플랜테이션 원료와 코코넛 껍질 중심으로 재편되고 있습니다. 한편, 인증 비용의 상승 속에서 수직 통합은 이익률을 지키는 데 도움이 되고 있습니다. 경쟁 환경은 변화하고 있습니다. 대형 연탄업체들은 생산량을 유지하는 반면, 무첨가제를 강조하는 천연탄 제조업체들의 도전이 계속되고 있습니다. 제철소와 시멘트 공장에서 바이오차르 혼합연료의 시험이 진행되고 있으며, 부피 밀도 및 인 함량에 대한 기술적 과제가 해결되면 새로운 산업 수요처로서 매출 다변화를 기대할 수 있을 것으로 보입니다. 추적성을 입증하고 고온 가마를 가동할 수 있는 생산자는 ESG 중심의 수출 기회와 활성탄 응용 분야에서 톤당 높은 부가가치를 창출할 수 있는 위치에 있습니다.

세계 숯 시장 동향 및 인사이트

신흥 경제국에서 가정용 조리용 연료 수요 증가

LPG의 적극적인 보급에도 불구하고 인도, 중국, 아프리카 국가의 농촌 지역에서는 여전히 고체 연료에 대한 의존도가 높으며, 이는 숯 시장을 지탱하고 있습니다. 인도에서는 PMUY(빈곤층 가스 공급 계획) 수혜 가구는 비수혜 가구에 비해 연간 LPG 실린더 소비량이 적은 경향을 보입니다. 이 차이는 특히 세계 LPG 가격이 일정 수준 이상일 때 연료를 더 많이 싣는 경향이 있음을 보여줍니다. 중국에서는 농촌 가구의 에너지 수요의 상당 부분이 여전히 바이오매스에 의존하고 있습니다. 또한 14차 5개년 계획의 모호한 정책으로 인해 바이오매스로부터의 완전한 전환을 방해하고 있습니다. 국제에너지기구(IEA)는 현 정책이 지속될 경우 2030년까지 여전히 많은 인구가 깨끗한 조리 수단을 이용할 수 없어 숯에 대한 수요가 지속될 것이라고 경고했습니다. 흥미롭게도 LPG 보급 속도는 여성 문맹률, 도로망 밀도 등의 요인과 더 밀접한 관련이 있으며, 보조금뿐만 아니라 인프라와 교육이 더 중요한 역할을 하고 있음을 시사합니다.

선진국 시장에서의 아웃도어 그릴-바비큐 문화 급성장

프리미엄화가 진행되는 가운데 천연경질목탄과 특수 비장탄이 주목받으며 기존의 범용 숯을 가치 면에서 추월하고 있습니다. 미국에서는 킹스포드사가 숯 시장에서 압도적인 점유율을 차지하고 있는 반면, 로얄오크 등 경쟁사 및 틈새 시장 기업이 단일 수종을 고집하는 천연탄 제품을 중심으로 시장 진입을 시도하고 있습니다. 유럽과 북미에서는 고온을 유지하는 특성으로 유명한 비장탄이 전문 주방에서 사용되고 있습니다. EU의 삼림파괴 규제를 염두에 두고 독일 소매업체들은 FSC 인증 제품 라인에 초점을 맞추기 위해 상품 구색을 조정하고 있습니다. 인도네시아와 베트남공급업체들은 엄격한 고온 사양을 충족시키면서 라이치나 유칼립투스를 원료로 한 일본 기주 비장탄의 대체품을 제공함으로써 시장에 도전하고 있습니다. 한편, 노르딕스완 에코라벨은 인증된 목재 사용을 의무화하여 지속가능성을 촉진하고, 플랜테이션 원료로의 전환을 가속화하고 있습니다.

엄격한 산림 규제와 삼림 파괴 억제

EU 삼림파괴 규제에 따라 위반시 벌금이나 화물 압류가 적용됩니다. 2020년 이후 삼림파괴 제로를 증명하지 못하는 수출업체는 서류 작성 비용 증가에 직면하게 됩니다. 산림관리협의회(FSC)의 감사 비용은 아프리카나 동유럽의 소규모 생산자를 사실상 배제하고, 인증을 받은 대규모 사업자에게 수출이 집중되는 결과를 낳고 있습니다. 케냐와 탄자니아의 계절적 벌채 금지로 인해 현지 가격이 상승하고 있지만, 그 시행은 여전히 일관성이 부족합니다. 공급 위험으로 인해 유럽 바이어들은 브라질산 유칼립투스 껍질과 동남아시아산 코코넛 껍질 조달을 늘리고 있지만, 행정적 문제로 인해 리드 타임이 계속 길어지고 있습니다.

부문 분석

인도네시아의 야심찬 목표와 베트남의 HS 4402.90.10에 따른 수출세 면제에 힘입어 코코넛 껍질 숯은 5.25%의 연평균 복합 성장률(CAGR)로 성장하여 다른 제품보다 높은 성장세를 보이고 있습니다. 연탄은 킹스포드의 놀라운 연간 생산량에 힘입어 2025년에는 38.12%의 숯 시장 점유율을 유지하며 대량 판매 시장을 독점하고 있습니다. 한편, 바비큐 애호가들 사이에서는 목탄이나 장작숯을 선호하는 추세이며, 이러한 추세로 인해 천연 덩어리 숯의 가격은 표준 상품용 연탄에 비해 높은 수준으로 유지되고 있습니다. 코코넛 껍질 숯의 미세 다공성 구조는 지자체 정수장 및 산업용 VOC 스크러버 수요 증가를 촉진하여 이중의 수입원을 창출하고 있습니다.

고압, 무결합제 연탄 기술을 채택하여 연소 효율이 크게 향상되어 기존 노천 연소에 비해 배출량을 줄일 수 있습니다. 이러한 친환경적인 접근 방식은 노르딕 스완과 같은 인증 기준에도 부합합니다. 브라질과 파라과이의 유칼립투스 조림지에서는 EU 바이어들이 중요시하는 생산 유통 과정의 추적성이 확보되어 있습니다. 일본 기주 비장탄이 초고급품의 명성을 유지하고 있는 반면, 비슷한 열적 특성을 가진 인도네시아산과 베트남산 백탄은 수입비용이 저렴하여 현재 더 쉽게 구할 수 있게 되었습니다.

숯 시장 보고서는 제품 유형(연탄, 경재 덩어리 숯, 코코넛 껍질 숯, 비장탄, 기타), 용도(조리용 연료, 바비큐/야외 그릴, 야금용 연료, 물/공기 정화, 의료, 화장품/퍼스널케어, 기타), 지역(아시아태평양, 북미, 유럽, 기타)으로 분류되어 있습니다. 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 세계 전체의 55.05%를 차지할 것으로 예상되며, 2031년까지 5.03%의 가장 빠른 CAGR을 나타낼 것으로 예측됩니다. 이러한 성장은 인도네시아, 베트남, 인도의 코코넛 껍질 공급망 강화와 농촌 지역에서의 지속적인 요리 수요에 힘입은 바 큽니다. 인도네시아의 수출은 사우디아라비아와 미국 수요에 힘입어 성장했습니다. 인도에서는 LPG 연결 수가 사상 최고치를 기록했음에도 불구하고 PMUY(약속된 월간 유틸리티) 보충율은 예상보다 낮았습니다. 그러나 이 국가의 연료 비축 행동은 숯 수요량을 지탱했습니다. 한편, 중국의 가정용 에너지의 대부분은 여전히 농촌의 바이오매스에 의존하고 있으며, 도시 가스 공급망과 농촌의 숯 의존도의 격차가 두드러지고 있습니다.

북미의 경우, 톤수 기준 성장세는 완만하지만 이익률은 견고합니다. 킹스포드는 규모의 경제를 활용하고, 로얄오크는 천연 목탄 판매가 급증하고 있으며, 모두 프리미엄화라는 광범위한 추세 속에서 일어나고 있습니다. 캐나다와 멕시코는 소규모로 생산에 기여하고 있으며, 미국에서는 전문 레스토랑이 비장탄 수입을 늘리고 있습니다. 유럽에서는 수요는 인증 기준에 대한 적합성에 따라 달라지며, 독일이 바비큐 숯 소비량에서 선두를 달리고 있습니다. 북유럽의 스완에코라벨은 조림지 유래 장작을 장려하고 있으며, 폴란드가 주요 수출국으로서 존재감을 드러내는 한편, FSC의 생산량 감사 강화로 공급망의 투명성이 높아지고 있습니다.

남미에서는 수직 통합형 유칼립투스 조림이 활용되고 있습니다. 플랜탈, 브리카팔과 같은 기업은 특히 인증 공급이 부족한 유럽 시장에서 고가 판매를 실현하고 있습니다. 아프리카는 중요한 생산지이지만 주로 비공식적인 영역에서 운영되고 있습니다. 인증 비용이 소규모 생산자에게는 큰 부담으로 작용하고 있으며, 많은 생산자들이 비인증 제품을 중동이나 국내 바이어에게 재판매하는 경향이 있습니다. 중동에서는 주로 사우디아라비아의 수입업체들이 인도네시아와 중국공급처로 눈을 돌리고 있으며, 전통적 요리용과 물담배 라운지 모두에 대한 높은 의존도가 안정적인 수요를 보장하고 있음을 보여줍니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

The Charcoal market is expected to grow from 73.15 million tons in 2025 to 76.12 million tons in 2026 and is forecast to reach 92.86 million tons by 2031 at 4.06% CAGR over 2026-2031.

This expansion is shaped by two contrasting forces: the sustained reliance on charcoal for household cooking across emerging economies and premium-segment growth in developed regions for barbecue and activated carbon uses. Supply chains are reorganizing around plantation feedstocks and coconut shells to meet the increasing demands of sustainability audits linked to the EU Deforestation Regulation, while vertical integration helps shield profit margins amid rising certification costs. Competitive dynamics are evolving as large briquette producers defend volume against natural-lump challengers that emphasize additive-free formulations. Steelmakers and cement plants are testing biochar blends, offering a nascent industrial demand stream that could diversify revenues once technical hurdles on bulk density and phosphorus content are resolved. Producers able to document traceability and operate high-temperature kilns are positioned to capture both ESG-driven export opportunities and higher value per ton in activated-carbon applications.

Global Charcoal Market Trends and Insights

Rising Demand for Household Cooking Fuel in Emerging Economies

Despite an aggressive LPG rollout, rural areas in India, China, and many parts of Africa continue to rely on solid fuels, thereby bolstering the charcoal market. In India, beneficiaries of the PMUY scheme consume fewer LPG cylinders annually compared to non-PMUY households. This discrepancy highlights a tendency to stack fuels, especially when global LPG prices exceed a certain threshold. In China, rural households continue to rely on biomass for a substantial portion of their energy needs. Furthermore, the policy ambivalence of the 14th Five-Year Plan is hindering a complete transition away from biomass. The International Energy Agency warns that if current policies persist, by 2030, a large population will still lack access to clean cooking solutions, ensuring a sustained demand for charcoal. Interestingly, the pace of LPG adoption is more closely tied to factors like female literacy and road density, suggesting that infrastructure and education play a more pivotal role than subsidies alone.

Outdoor Grilling and BBQ Culture Surge in Developed Markets

As premiumization takes center stage, lump hardwood and specialty Binchotan are gaining traction, edging out traditional commodity briquettes in terms of value. While Kingsford commands a dominant share of the U.S. briquette market, competitors like Royal Oak and other niche players are making inroads, especially with their natural-lump offerings that emphasize single-species sourcing. In Europe and North America, professional kitchens are turning to Binchotan, known for its ability to maintain high temperatures. In anticipation of the EU Deforestation Regulation, German retailers are adjusting their assortments to focus on FSC-certified lines. Suppliers from Indonesia and Vietnam are challenging the market by offering alternatives to Japan's Kishu Binchotan, utilizing lychee and eucalyptus feedstocks, all while adhering to stringent high-heat specifications. Meanwhile, the Nordic Swan Ecolabel promotes sustainability by mandating certified wood content, thereby accelerating the shift towards plantation feedstocks.

Stringent Forestry Regulations and Deforestation Curbs

The EU Deforestation Regulation imposes fines and allows for shipment confiscation in cases of non-compliance. Exporters failing to prove zero deforestation post-2020 face rising documentation costs. Audit fees from the Forest Stewardship Council (FSC) effectively sideline smallholders in Africa and Eastern Europe, leading to a concentration of export flows among larger, certified entities. While seasonal harvest bans in Kenya and Tanzania elevate local prices, their enforcement remains inconsistent. Due to supply risks, European buyers are increasingly sourcing eucalyptus from Brazilian plantations and coconut shells from Southeast Asia, though administrative challenges continue to extend lead times.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Activated-Charcoal Demand in Purification and Healthcare

- Industrial Use as Coke Substitute in Iron, Steel, and Cement

- Rapid LPG and Electric-Cooking Roll-Out in Africa/Asia Urban Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Driven by Indonesia's ambitious target and Vietnam's export-tax exemption under HS4402.90.10, coconut-shell charcoal is expanding at a 5.25% CAGR, outpacing its counterparts. Briquettes continue to dominate the mass retail market with a 38.12% charcoal market share in 2025, bolstered by Kingsford's impressive annual output. While hardcore barbecue aficionados lean towards hardwood lump and Binchotan, this trend has propelled natural-lump prices to higher levels compared to standard commodity briquettes. The microporous structure of coconut-shell charcoal is fueling its growing demand from municipal water plants and industrial VOC scrubbers, creating a dual revenue stream.

Utilizing high-pressure, binder-free briquette technology, combustion efficiency improves significantly, resulting in reduced emissions compared to traditional open burning. This eco-friendly approach resonates with labels like the Nordic Swan. Eucalyptus plantations in Brazil and Paraguay are ensuring the chain-of-custody traceability that EU buyers prioritize. While Japan's Kishu Binchotan holds an ultra-premium reputation, Indonesian and Vietnamese white charcoals, boasting similar thermal specifications, are now more accessible due to their lower landed costs.

The Charcoal Market Report is Segmented by Product Type (Briquettes, Hardwood Lump, Coconut-Shell, Binchotan, and Other Product Types), Application (Cooking Fuel, Barbecue/Outdoor Grilling, Metallurgical Fuel, Water and Air Purification, Healthcare, Cosmetics and Personal Care, and Other Applications), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific delivered 55.05% of global volume in 2025 and will log the fastest 5.03% CAGR to 2031. This growth is driven by Indonesia, Vietnam, and India strengthening their supply chains around coconut shells, alongside enduring demand for rural cooking. Indonesia's exports were buoyed by demand from Saudi Arabia and the U.S. Despite record LPG connections, India's PMUY refill rates lagged behind expectations; yet, the nation's fuel-stocking behavior cushioned charcoal volumes. Meanwhile, a significant portion of household energy in China continues to derive from rural biomass, highlighting a divide between urban gas grids and rural reliance on charcoal.

In North America, while tonnage growth is modest, profit margins are robust. Kingsford capitalizes on scale, and Royal Oak experiences a surge in natural-lump sales, all amidst a broader trend of premiumization. While Canada and Mexico contribute with modest production, specialty restaurants across the U.S. are increasingly importing Binchotan. In Europe, demand hinges on compliance with certification standards, with Germany leading the way in barbecue volumes. The Nordic Swan Ecolabel is championing plantation sources, and while Poland stands out as a key exporter, tightening FSC volume audits are enhancing transparency in the supply chain.

South America is capitalizing on vertically integrated eucalyptus plantations. Companies like Plantar and BRICAPAR are reaping premiums in European markets, especially where certified supplies are in short supply. Africa, though a significant player, operates largely in the informal realm. Here, the costs of certification pose challenges for smallholders, leading many to redirect uncertified outputs to buyers in the Middle East and domestically. In the Middle East, importers, predominantly from Saudi Arabia, are turning to Indonesian and Chinese sources, underscoring their reliance on both traditional cooking and hookah lounges, which ensures a consistent demand.

- BRICAPAR S.A. Charcoal Briquettes

- Calgon Carbon Corporation

- Duraflame, Inc.

- E & C Charcoal

- Etosha

- Fire & Flavor

- Fogo Charcoal

- GRYFSKAND

- Haycarb PLC

- JACOBI CARBONS GROUP

- Kingsford Products Company

- MATSURI INTERNATIONAL CO. LTD

- Mesjaya Sdn Bhd

- NAMCHAR

- NamCo Charcoal and Timber Products

- Oxford Charcoal Company

- Paraguay Charcoal

- Plantar

- PT Cavron Global

- Royal Oak Enterprises, LLC

- Sagar Charcoal and Firewood Depot

- Subur Tiasa Holdings Berhad

- Timber Charcoal Company LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for household cooking fuel in emerging economies

- 4.2.2 Outdoor grilling and BBQ culture surge in developed markets

- 4.2.3 Expansion of activated-charcoal demand in purification and healthcare

- 4.2.4 Industrial use as coke substitute in iron, steel and cement

- 4.2.5 Premium certified-sustainable charcoal unlocking ESG export channels

- 4.3 Market Restraints

- 4.3.1 Stringent forestry regulations and deforestation curbs

- 4.3.2 Environmental concerns limiting wood-feedstock supply

- 4.3.3 Rapid LPG and electric-cooking roll-out in Africa/Asia urban hubs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Briquettes

- 5.1.2 Hardwood Lump

- 5.1.3 Coconut-Shell

- 5.1.4 Binchotan

- 5.1.5 Other Product Types (Sugar charcoal, Mangrove, Shisha, Sawdust, and Root)

- 5.2 By Application

- 5.2.1 Cooking Fuel

- 5.2.2 Barbecue/Outdoor Grilling (Retail and HoReCa)

- 5.2.3 Metallurgical Fuel

- 5.2.4 Water and Air Purification

- 5.2.5 Healthcare

- 5.2.6 Cosmetics and Personal Care

- 5.2.7 Other Applications (Barbeque and Horticulture)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BRICAPAR S.A. Charcoal Briquettes

- 6.4.2 Calgon Carbon Corporation

- 6.4.3 Duraflame, Inc.

- 6.4.4 E & C Charcoal

- 6.4.5 Etosha

- 6.4.6 Fire & Flavor

- 6.4.7 Fogo Charcoal

- 6.4.8 GRYFSKAND

- 6.4.9 Haycarb PLC

- 6.4.10 JACOBI CARBONS GROUP

- 6.4.11 Kingsford Products Company

- 6.4.12 MATSURI INTERNATIONAL CO. LTD

- 6.4.13 Mesjaya Sdn Bhd

- 6.4.14 NAMCHAR

- 6.4.15 NamCo Charcoal and Timber Products

- 6.4.16 Oxford Charcoal Company

- 6.4.17 Paraguay Charcoal

- 6.4.18 Plantar

- 6.4.19 PT Cavron Global

- 6.4.20 Royal Oak Enterprises, LLC

- 6.4.21 Sagar Charcoal and Firewood Depot

- 6.4.22 Subur Tiasa Holdings Berhad

- 6.4.23 Timber Charcoal Company LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment