|

시장보고서

상품코드

1934819

독일의 용기용 유리 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Container Glass - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

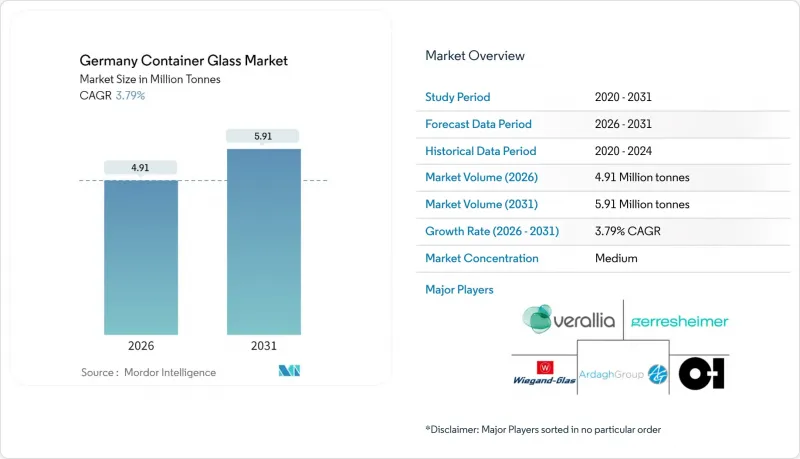

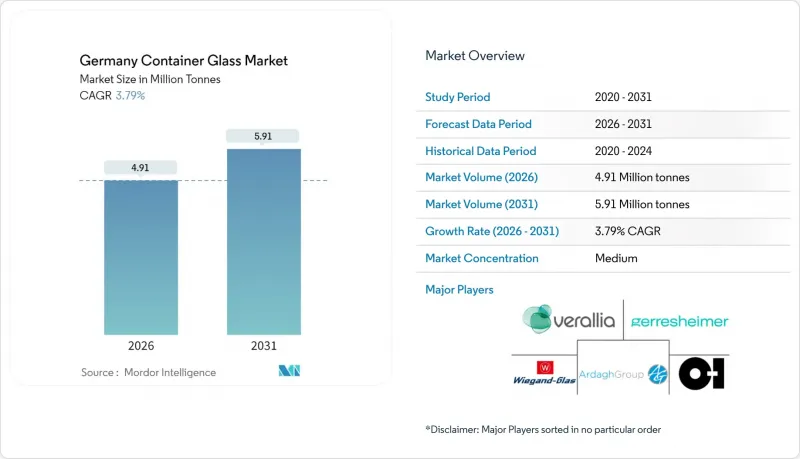

독일의 용기용 유리 시장은 2025년 473만 톤에서 2026년에는 491만 톤으로 성장하며, 2026-2031년에 CAGR 3.79%로 추이하며, 2031년까지 591만 톤에 달할 것으로 예측되고 있습니다.

에너지 가격의 영향과 다년간의 맥주 판매량 감소가 단기적인 성장에 영향을 미치고, 경량 유리 기술 혁신, 하이브리드 용광로 도입, 정부의 순환 경제 전략이 시장의 중기적 성장을 지원하고 있습니다. 고급 음료 제조업체는 브랜드 아이덴티티를 강화하면서 탄소발자국을 줄이는 맞춤형 병을 지정하고 있으며, 의약품 충전업체는 EU GMP 부속서 1 가이드라인을 준수하는 무균 및 즉시 사용 가능한 용기로 전환하고 있습니다. 재생원료 25% 사용과 유리 회수율 80%라는 국가적 목표에 따라 용기용 유리는 플라스틱에 비해 우위를 점하고 있습니다. 플라스틱 생산업체들은 현재 재생원료 함량 최소 기준치에 직면해 있다(ihk.de). 주요 제조업체들은 생산 능력의 효율화와 저탄소 기술에 대한 투자라는 이중 전략에 대응하고 있으며, 이를 통해 생산성을 향상시키고 톤당 배출량을 줄일 수 있을 것으로 예측됩니다. 재생에너지 확보와 하이브리드 용해기술 도입이 가능한 독일 용기유리 시장 진출기업은 고부가가치 의약품, 화장품, 고급 주류 용도에서 증가하는 수요의 대부분을 차지할 것으로 예측됩니다.

독일 용기용 유리 시장 동향 및 전망

독일에서 재생 포장재에 대한 수요 증가

2025년 1월에 채택된 '국가 순환형 경제 전략'은 전략 원자재 수요의 25%를 재활용으로 충당하고, 2030-2040년까지 1인당 도시 쓰레기를 10-20% 감축하는 것을 의무화하고 있습니다. 이 프레임워크는 무한한 재활용이 가능하고 안정된 품질을 가진 용기 유리가 폴리머 대체품보다 우위를 점할 수 있도록 도와줍니다. 약 30만 곳의 공공 유리 회수 거점에서는 이미 80% 이상의 유리 회수율을 달성하여 생산자에게는 안정적인 칼렛 공급원을 제공하고, 용융유리 1톤당 최대 30%의 용해로 에너지 수요를 절감할 수 있습니다. 본 전략에서 계획하고 있는 디지털 제품 여권은 재활용 함량을 기록하여 고율의 카렛 함유 병에 경쟁적 차별화를 가져다 줄 것입니다. 향후 도입될 일회용 플라스틱 재활용 의무화에 대응하고자 하는 브랜드에게 유리는 포장의 지속가능성 목표를 달성할 수 있는 분명한 길이며, 독일 용기 유리 시장에 대한 수요를 촉진하고 있습니다.

성장하는 제약 부문은 고품질 유리 수요를 가속화

SCHOTT Pharma의 2024년 매출은 9억 5,700만 유로(10억 8,000만 달러)를 기록하여 환율 변동 영향을 제외한 기준으로는 12% 증가했습니다. 고부가가치 주사기 및 즉시 사용(RTU) 용기가 매출의 55%를 차지하게 되었습니다. 독일의 바이오의약품 생산 집중과 새로운 GLP-1 요법의 도입은 동결 건조를 견디고 약물 안정성을 유지할 수 있는 저알칼리성, 저입자 유리 용기에 대한 수요를 주도하고 있습니다. SCHOTT Pharma, Gerresheimer, Stevanato Group의 'Alliance for RTU'는 RTU 사양 표준화를 통해 제약 충전 라인의 효율성과 오염 위험을 줄이고, 고품질 붕규산 유리 및 알루미노실리케이트 유리의 대상 시장을 더욱 확대할 수 있는 기회를 제공합니다. 확대하고 있습니다. 이러한 추세에 따라 USP(660) 및 EU 약전 Type I 인증을 획득하고, 신속한 전환 및 무균 공급 능력을 제공하는 제조업체에 대한 수요가 증가할 것으로 예측됩니다.

에너지 비용 상승으로 유리 생산 비용 상승

2024-2025년까지 산업용 전기요금은 1MWh당 약 40유로(43.2달러)로, 위기 이전 대비 약 4배에 달할 것으로 예측됩니다. 한편, 천연가스 가격의 급등으로 인해 일시적인 정부 보조금에도 불구하고 전체 용해비용이 상승했습니다. 1,600℃의 용해 공정이 용광로 운영 비용의 70-75%를 차지하므로 전력 가격의 상승은 수익성을 떨어뜨리고 투자 예산을 압박하고 있습니다. Ardagh의 NextGen 라인에서 입증된 바와 같이, 하이브리드 용광로는 CO2 배출량을 최대 64%까지 줄일 수 있지만, 여전히 경쟁력 있는 가격의 재생 전력에 의존하고 있습니다. 전력망의 탈탄소화와 산업용 전력 가격의 완화로 인해 투입 비용이 안정화될 때까지 독일 컨테이너 유리 시장의 생산 능력 확대는 잠재적 수요에 비해 뒤쳐질 것입니다.

부문 분석

음료 부문은 2025년 독일 용기용 유리 시장 점유율 51.60%(2,440 킬로톤 상당)를 유지하며 맥주와 와인 리필 문화가 여전히 강세를 보이고 있음을 반영합니다. 그러나 2025년 1월부터 5월까지 맥주 출하량은 6.8% 감소한 3,410만 헥토리터로 통일 이후 최저치를 기록했습니다. 이로 인해 병에 대한 수요가 줄어들고 양조장의 합리화가 진행되었습니다. 표준 맥주병에 연동되는 독일 용기 유리 시장 규모는 2030년까지 낮은 한 자릿수 CAGR로 축소될 것으로 예측됩니다. 반면, 증류주, 수제맥주, 무알코올 맥아 음료는 프리미엄 가격을 실현하는 주문 제작 경량 유리를 채택하여 이러한 감소를 일부 상쇄하고 있습니다. 이러한 틈새 시장에 공급하는 제조업체는 신속한 금형 대응과 저CO2 유리 인증 제공으로 이익률을 유지할 수 있습니다.

의약품 용도는 2025년 기준 독일 용기유리 시장 규모의 약 10.40%를 차지하고 있으며, 바이오의약품, GLP-1 주사제, mRNA 백신에 대한 수요 증가로 음료 분야를 상회하는 5.05% 이상의 CAGR로 성장할 것으로 예측됩니다. EU 부속서 1의 엄격한 규정으로 인해 무균 보장 및 라인 효율성이 높은 RTU 바이알 주사기가 촉진되어 평균 판매 가격이 상승하고 필요한 칼렛 등급이 감소하고 있습니다. 화장품 및 퍼스널케어 분야는 수량 기준 8.10%로 규모는 작지만, 고급 스킨케어 브랜드가 플라스틱에서 유리로 전환하여 고급스러운 개봉 경험을 제공함에 따라 5.12%의 가장 빠른 CAGR을 기록했습니다. 식품용 병은 소비자들이 유리를 불활성이며 재사용이 가능하다는 인식으로 인해 한 자릿수 중반의 견고한 점유율을 유지하고 있습니다. 그러나 그 성장률은 전체 식품 시장 성장률과 거의 비슷한 수준입니다.

이 보고서 '독일의 용기용 유리 시장'은 최종사용자별(음료(알코올음료(맥주, 와인, 증류주, 기타 알코올음료), 무알코올음료(주스, 탄산음료, 유제품 베이스 음료, 기타 무알코올음료)), 식품, 화장품-퍼스널케어, 의약품, 향수, 색(녹색, 호박색, 무색투명 등))으로 분석했습니다. 향수), 색상(녹색, 호박색, 무색투명 등) 별로 분석했습니다. 시장 예측은 톤 단위로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The Germany Container Glass Market is expected to grow from 4.73 million tonnes in 2025 to 4.91 million tonnes in 2026 and is forecast to reach 5.91 million tonnes by 2031 at 3.79% CAGR over 2026-2031.

The market's medium-term momentum is underpinned by lightweight glass innovation, hybrid furnace deployment, and the government's circular economy strategy, despite the impact of energy prices and a multi-year decline in beer volumes on near-term growth. Premium beverage owners are specifying customized bottles that reinforce brand identity while reducing their carbon footprint, and pharmaceutical fillers are shifting toward sterile, ready-to-use containers that meet EU Good Manufacturing Practice Annex 1 guidelines. National targets for 25% recycled raw material use and 80% glass collection rates position container glass favorably against plastic, whose producers now face minimum recycled-content thresholds ihk.de. Scale manufacturers are responding with capacity rationalization and investments in low-carbon technology, a dual strategy that is expected to boost productivity and reduce per-ton emissions. Germany container glass market participants able to secure renewable power and deploy hybrid melting technology are forecast to capture the bulk of incremental demand from high-value pharmaceutical, cosmetics, and premium spirits applications.

Germany Container Glass Market Trends and Insights

Increasing Demand for Recyclable Packaging in Germany

The National Circular Economy Strategy, adopted in January 2025, mandates that 25% of strategic raw material demand be met through recycling and that per capita municipal waste decline by 10-20% by 2030-2040. This framework elevates container glass, whose infinite recyclability and stable quality outperform polymer substitutes. Roughly 300,000 public glass-collection points already deliver glass return rates above 80%, providing producers with a dependable cullet stream and reducing furnace energy demand by up to 30% per ton of glass melted. Digital product passports planned under the strategy will document the recycled content, creating competitive differentiation for bottles containing high levels of cullet. Brands seeking to comply with forthcoming single-use plastic recycled-content mandates find glass to be a straightforward path to achieving packaging sustainability targets, thereby bolstering demand for Germany's container glass market.

Growing Pharmaceutical Sector Accelerates High-Quality Glass Demand

SCHOTT Pharma recorded EUR 957 million (USD 1.08 billion) in revenue for 2024, representing a 12% constant-currency increase. High-value syringes and ready-to-use (RTU) containers now account for 55% of turnover. Germany's concentration of biologics production and the introduction of new GLP-1 therapies are driving demand for low-alkali, low-particle glass formats that can withstand lyophilization and maintain drug stability. The "Alliance for RTU" formed by SCHOTT Pharma, Gerresheimer, and Stevanato Group is standardizing RTU specifications to streamline pharma filling lines and reduce contamination risk, further expanding the addressable market for premium borosilicate and aluminosilicate glass. These trends channel incremental volume to producers that can certify USP (660) and EU Pharmacopoeia Type I compliance while offering rapid changeover and sterile supply capabilities.

Rising Energy Costs Elevate Glass Production Expenses

Industrial electricity hovered near EUR 40 (USD 43.2) per MWh in 2024-2025, roughly four times pre-crisis levels, while natural-gas price spikes raised total melt costs despite temporary government subsidies. Because melting at 1,600 °C accounts for 70-75% of furnace operating cost, elevated power prices erode profitability and compress investment budgets. Hybrid furnaces can reduce CO2 by up to 64%, as demonstrated by Ardagh's NextGen line, yet still rely on competitively priced renewable electricity. Until grid decarbonization and industrial power-price relief stabilize input costs, Germany's container glass market capacity growth will lag potential demand.

Other drivers and restraints analyzed in the detailed report include:

- Premium Beverages Drive Customized Bottle Requirements

- Circular Economy Policies Strengthen Glass Recycling Systems

- Competition from PET and Imported Glass Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Beverages retained 51.60% of the German container glass market share in 2025, equivalent to 2.44 thousand kilotons, reflecting the entrenched traditions of refillable beer and wine. However, from January to May 2025, beer shipments fell 6.8% to 34.1 million hectoliters, marking the lowest post-reunification level, which trimmed bottle demand and prompted brewery rationalization. Germany's container glass market size linked to standard beer bottles is projected to contract at a low single-digit CAGR through 2030. Spirits, craft, and alcohol-free malt drinks partly offset this decline by adopting bespoke lightweight glass that commands premium shelf prices. Producers serving these niches can defend margins by offering rapid mold turnaround and low-CO2 glass certificates.

Pharmaceutical applications accounted for an estimated 10.40% of Germany's container glass market size in 2025, yet are forecast to outpace beverages, expanding at a 5.05% or more CAGR, thanks to the growing demand for biologics, GLP-1 injectables, and mRNA vaccines. Stringent EU Annex 1 rules promote RTU vials and syringes that deliver sterility assurance and line efficiency, thereby lifting average selling prices and reducing the grades of cullet required. Cosmetics and personal care hold only 8.10% volume but post the fastest 5.12% CAGR as premium skin-care brands switch from plastic to glass for a luxury unboxing experience. Food jars maintain a resilient mid-single-digit share, benefiting from consumer perception of glass as inert and reusable, although growth mirrors that of the broader grocery market.

The Germany Container Glass Market Report is Segmented by End-User (Beverages [Alcoholic (Beer, Wine, Spirits, and Other Alcoholic Beverages), Non-Alcoholic (Juices, Carbonated Drinks, Dairy Product Based Drinks, and Other Non-Alcoholic Beverages]), Food, Cosmetics and Personal Care, Pharmaceuticals, and Perfumery), Color (Green, Amber, Flint, and More). The Market Forecasts are Provided in Terms of Volume (Tonnes).

List of Companies Covered in this Report:

- Ardagh Glass GmbH

- Systempack Manufaktur GmbH

- HEINZ-GLAS GmbH & Co. KGaA

- Schott AG

- Saint-Gobain Oberland AG (Verallia Deutschland AG)

- Rixius AG

- O-I Germany GmbH & Co KG

- Gerresheimer AG

- Wiegand-Glas GmbH

- Noelle + von Campe GmbH & Co. KG

- SGD Pharma Germany GmbH

- Glashutte Freital GmbH

- KP Glas GmbH & Co. KG

- Verallia Deutschland AG

- Glashutte Eisch GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Recyclable Packaging in Germany

- 4.2.2 Growing Pharma Sector Boosts High-Quality Glass Packaging

- 4.2.3 Premium Beverages Drive Customized Bottle Requirements

- 4.2.4 Circular Economy Policies Strengthen Glass Recycling Systems

- 4.2.5 Sustainability Targets Accelerate Lightweight Glass Innovation

- 4.2.6 Industry Consolidation Reshapes Container Glass Capacity

- 4.3 Market Restraints

- 4.3.1 Rising Energy Costs Elevate Glass Production Expenses

- 4.3.2 Competition from PET and Imported Glass Packaging

- 4.3.3 Regulatory Compliance Raises Barriers for Small Producers

- 4.3.4 Plant Closures Reduce Local Supply Availability

- 4.4 PESTEL Analysis

- 4.5 Industry Value Chain Analysis

- 4.6 Container Glass Furnace Capacity and Locations in Germany

- 4.6.1 Plant Locations and Year of Commencement

- 4.6.2 Production Capacities

- 4.6.3 Types of Furnaces

- 4.6.4 Color of Glass Produced

- 4.7 Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.7.1 Import Volume and Value, 2021-2024

- 4.7.2 Export Volume and Value, 2021-2024

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Raw Material Analysis

- 4.10 Recycling Trends for Glass Packaging

- 4.11 Demand vs Supply Analysis for Glass Packaging

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By End-user

- 5.1.1 Beverages

- 5.1.1.1 Alcoholic

- 5.1.1.1.1 Beer

- 5.1.1.1.2 Wine

- 5.1.1.1.3 Spirits

- 5.1.1.1.4 Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2 Non-Alcoholic

- 5.1.1.2.1 Juices

- 5.1.1.2.2 Carbonated Drinks (CSDs)

- 5.1.1.2.3 Dairy Product Based Drinks

- 5.1.1.2.4 Other Non-Alcoholic Beverages

- 5.1.1.1 Alcoholic

- 5.1.2 Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3 Cosmetics and Personal Care

- 5.1.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5 Perfumery

- 5.1.1 Beverages

- 5.2 By Color

- 5.2.1 Green

- 5.2.2 Amber

- 5.2.3 Flint

- 5.2.4 Other Colors

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ardagh Glass GmbH

- 6.4.2 Systempack Manufaktur GmbH

- 6.4.3 HEINZ-GLAS GmbH & Co. KGaA

- 6.4.4 Schott AG

- 6.4.5 Saint-Gobain Oberland AG (Verallia Deutschland AG)

- 6.4.6 Rixius AG

- 6.4.7 O-I Germany GmbH & Co KG

- 6.4.8 Gerresheimer AG

- 6.4.9 Wiegand-Glas GmbH

- 6.4.10 Noelle + von Campe GmbH & Co. KG

- 6.4.11 SGD Pharma Germany GmbH

- 6.4.12 Glashutte Freital GmbH

- 6.4.13 KP Glas GmbH & Co. KG

- 6.4.14 Verallia Deutschland AG

- 6.4.15 Glashutte Eisch GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment