|

시장보고서

상품코드

1934840

유럽의 종이 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Paper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

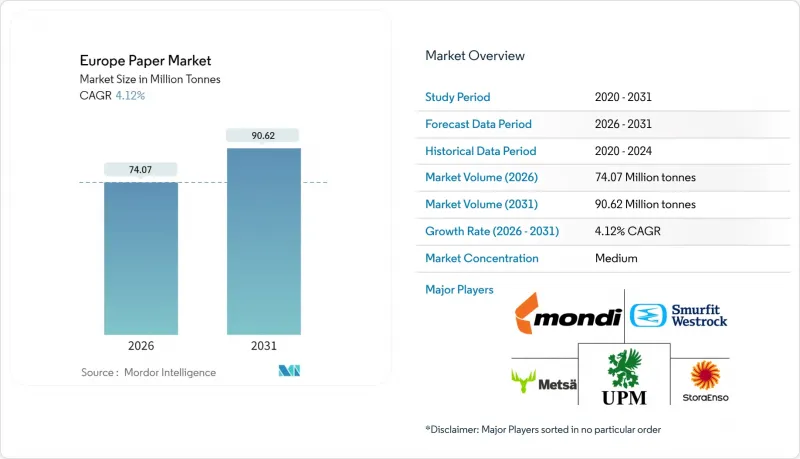

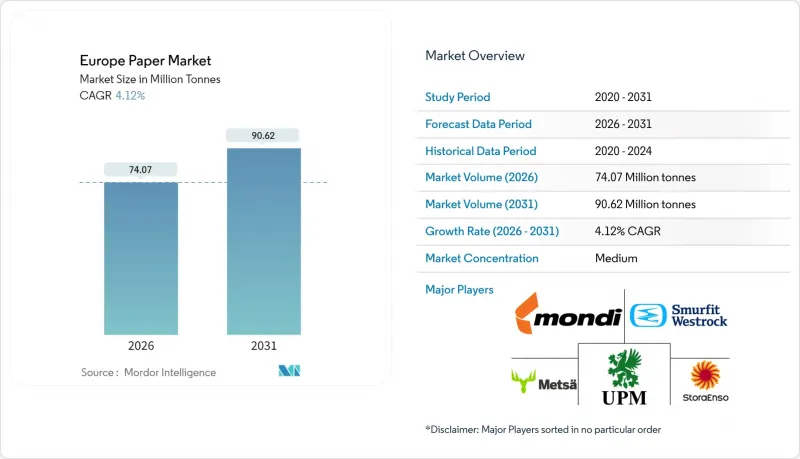

유럽의 종이 시장 규모는 2026년에 7,407만 톤으로 추정되며, 2025년 7,114만 톤으로부터 성장이 전망됩니다.

2031년 예측치는 9,062만 톤으로 2026-2031년 연평균 복합 성장률(CAGR) 4.12%로 성장할 전망입니다.

에너지 비용의 인플레이션 압력과 그래픽 용지의 디지털 대체가 진행되는 가운데, 유럽 종이 시장은 순환 경제에 대한 엄격한 규제, E-Commerce를 위한 포장 수요, 팬데믹 이후 티슈 소비 증가를 배경으로 계속 확대되고 있습니다. 재생섬유 도입 가속화는 원료 조달 리스크를 억제하고, 자원 주권 확보를 위한 지역내 전략적 노력을 강화하고 있습니다. 한편, 수직계열화 대기업은 수익성 유지를 위해 그래픽 용지 생산능력을 고매출 포장지 등급으로 전환하고 있습니다. 공급 측면에서는 2024년 스웨덴산 목재 펄프 가격이 30% 급등하면서 공급 부족이 지속되고 있으며, 장기 계약 및 원료 조달 다변화를 중심으로 한 조달 전략이 추진되고 있습니다.

유럽 제지 시장 동향 및 분석

지속가능한 포장재 사용 확대

EU 규정 2025/40에 따라 2030년까지 EU에서 판매되는 모든 포장재의 재활용이 의무화됨에 따라 브랜드 소유주들 수요가 섬유 기반 포장재로 급격히 이동하고 있습니다. 몬디는 이미 매출의 87%를 재사용, 재활용, 퇴비화 가능한 솔루션에서 얻고 있으며, 이는 규제 준수가 프리미엄 가격의 가치 제안으로 전환되었음을 보여줍니다. 골판지 가공업체들은 거시적 환경의 침체에도 불구하고 수주 잔고를 보유하고 있으며, 구매 기준에서 지속가능성이 비용보다 더 중요하다는 것을 보여주고 있습니다. 추가 자본은 회원국 전체에서 플라스틱 금지의 혜택을 받고 있는 푸드서비스용 성형 섬유 트레이로 이동하고 있습니다. OEM 업체들이 저탄소 인증을 받기 위해 경쟁하는 가운데, 이력추적성 및 재활용 소재 함유량에 대한 공장 인증은 소매점 진열대 진입을 좌우하는 중요한 요소가 되고 있습니다.

E-Commerce 및 외식 산업 수요 증가

온라인 소매는 매장 판매에 비해 거래당 골판지 사용량이 최대 3배까지 증가하여 유럽 종이 시장의 구조적인 톤수 증가를 가져오고 있습니다. 테이크아웃 배달 수요의 병행 성장으로 내유성 및 내습성 포장재에 대한 수요가 증가하고 있습니다. 제지업체들은 이에 대응하여 소량 생산을 비용 효율적으로 맞춤화할 수 있는 주문형 플렉소 인쇄기 및 잉크젯 인쇄 라인을 도입했습니다. 이를 통해 전자 소매업체의 재고 리스크를 줄일 수 있습니다. 도시 지역의 마이크로 풀필먼트 거점에서는 피킹 및 포장 효율을 높이고 공극을 줄이기 위해 간이 접이식 케이스 설계를 채택하고 있습니다. 이러한 유통 경로가 결합되어 기존 상업용 인쇄 수요 감소를 상쇄하고 포장재가 유럽 제지 시장의 회복력에서 안정적 요인으로의 역할을 강조하고 있습니다.

변동하는 목재 펄프 및 폐지 가격

2024년 스웨덴 통나무 비용 30% 상승은 제지공장의 이익률을 압박하고, 비통합 생산자의 원자재 가격 변동에 대한 취약성을 드러냈습니다. 러시아-벨로루시산 섬유 수입에 대한 지정학적 제약으로 인해 지역 공급처를 압박하고 있으며, 제지 공장들은 다년간의 판매 계약을 확보하거나 산림 자산을 직접 인수해야 하는 상황에 처해 있습니다. 회수지 수집 비용도 드라이버 부족과 디젤 가격 상승으로 인해 상승하여 버진 펄프에 대한 가격 우위가 축소되었습니다. 수직적 통합은 이제 결정적인 헤지 수단으로 자리 잡았으며, Stora Enso가 산림 자산의 일부 매각을 장기 벌채권 계약으로 상쇄한 사례는 이를 잘 보여줍니다. 상품화된 등급의 경우 가격 결정력이 약하므로 중소 독립 제조업체는 가격 급등시 현금 흐름 악화 위험에 직면하고, 원자재 가격 변동성이 가장 심각한 경영 역풍으로 부각되었습니다.

부문 분석

케이스 소재는 2025년 기준 유럽 종이 시장 점유율의 33.78%를 차지하며, E-Commerce, 식품 및 산업 공급망을 지원하는 포장 기반을 형성하고 있습니다. 골판지 케이스용 등급은 그래픽 공장에서의 다운스트림 전환을 포착하여 신규 공장 건설의 리드타임 없이 저비용 생산 능력을 추가했습니다. 생산자는 경량화 기술을 활용하여 적재 강도를 유지하면서 평량을 줄였습니다. 유통업체의 지속가능성 평가 기준에 따라 지속가능경영을 실천하고 있습니다. 특수지는 2025년 기준 892만 톤으로 규모는 작지만 식품용 배리어 코팅, 보안기판, 전자기기용 기술 라미네이트에 힘입어 CAGR 5.95%를 달성할 것으로 전망. 이러한 틈새 시장은 높은 가격 책정이 가능하고, 배합 비용과 적합성 테스트 증가를 상쇄할 수 있으므로 대규모 통합 제조업체에게 매력적인 다각화 전략이 될 수 있습니다.

그래픽 용지가 직면한 구조적 역풍은 여전히 지속되고 있지만, 고급 잡지나 미술 서적은 디지털 화면을 넘어선 촉각적 품질을 지속적으로 요구하고 있으며, 축소되는 추세지만 생존 가능한 틈새 시장을 유지하고 있습니다. 위생 및 가정용 용지는 수요의 방어적 특성과 지속적인 위생 의식 증가로 인해 수혜를 받고 있습니다. 포장지 및 판지는 소매업체의 비닐봉지 금지와 옴니채널 소매 포장의 재설계를 기회로 활용하고 있습니다. 향후 수성 플렉소 인쇄와 같은 산업 인쇄 기술 혁신은 새로운 부가가치 수입원을 창출하고, 유럽 제지 시장에서 케이스 소재의 핵심적인 역할을 확고히할 것입니다.

재생섬유는 2025년 기준 유럽 종이 시장 규모의 52.64%를 차지할 것으로 예상되며, 이는 유럽이 폐쇄형 재료 순환에서 선도적인 위치를 차지하고 있음을 보여줍니다. 확대된 생산자 책임제를 바탕으로 한 회수 시스템으로 다른 지역보다 높은 회수율을 달성하고 있습니다. 에코 디자인 기준의 진화에 따라 컨버터는 탈묵성과 섬유 유지성을 고려한 포장 재설계를 진행하여 재생 섬유의 유통량을 강화하고 있습니다. 관능적 순도와 인열 저항성이 필수 조건인 고급 포장 분야에서는 버진 섬유의 사용량이 4.34%의 가장 빠른 CAGR을 기록했습니다. 통합 임업 기업은 인증된 임업 자산을 활용하여 이들 부문에 공급하고, 전반적인 지속가능성 목표 달성을 위해 1차 펄프와 다른 분야의 재생섬유 사용량 증가를 결합하는 사례가 증가하고 있습니다.

농업잔재 섬유는 아직 개발 단계에 있지만, 조달 리스크 분산과 탄소 강도 감소를 목적으로 밀짚과 억새 펄프화를 시범적으로 도입하여 주목을 받고 있습니다. 대륙 정책의 삼림 벌채에 대한 추적성 요건 강화는 재생 섬유와 대체 섬유의 상대적 매력을 더욱 높이고 있습니다. 한편, 제지 공장에서의 효소 탈묵 시험은 재생 섬유의 백색도 향상, 고급 백색 등급으로의 적용 범위 확대, 그리고 유럽 제지 시장을 지원하는 순환형 스토리 강화에 있으며, 유망한 결과를 보여주고 있습니다.

유럽 종이 시장 보고서는 제품 유형(그래픽 용지, 케이스재, 위생 및 가정용 종이, 포장지, 판지, 특수지), 원료 공급원(버진 섬유, 재생 섬유, 농업 잔류 섬유), 평량(90gsm 미만 및 그 이상), 최종 사용 산업(포장 및 산업용 등), 지역(독일 등)으로 구성되어 있습니다. 지역(독일 등)으로 구성됩니다. 시장 예측은 톤 단위로 제공됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05Europe paper market size in 2026 is estimated at 74.07 million tonnes, growing from 2025 value of 71.14 million tonnes with 2031 projections showing 90.62 million tonnes, growing at 4.12% CAGR over 2026-2031.

Despite inflationary energy costs and digital substitution in graphic grades, the Europe paper market continues to expand on the back of strict circular-economy regulation, e-commerce packaging demand, and a post-pandemic rise in tissue consumption. Accelerated adoption of recycled fiber keeps material input risk in check and reinforces the bloc's strategic push for resource sovereignty. Meanwhile, vertically integrated leaders redirect graphic capacity toward higher-margin packaging grades to defend profitability. Supply-side dynamics remain tight as wood-pulp prices in Sweden jumped 30% in 2024, prompting procurement strategies that favor long-term contracts and diversified fiber sourcing.

Europe Paper Market Trends and Insights

Growth in Use of Sustainable Packaging

Mandatory recyclability targets under Regulation 2025/40 require all packaging sold in the bloc to be recyclable by 2030, pushing brand-owner demand sharply toward fiber-based formats. Mondi already derives 87% of revenue from reusable, recyclable, or compostable solutions, signalling how compliance has turned into a premium-priced value proposition. Corrugated converters report order backlogs even in a sluggish macro environment, indicating that sustainability now outweighs cost in purchasing criteria. Incremental capital has shifted toward molded-fiber trays for food service, a segment benefiting from plastic bans across member states. As OEMs scramble for low-carbon credentials, mill certifications around traceability and recycled content serve as gatekeepers to retail shelf space.

Expansion of E-commerce and Food-service Demand

Online retail requires up to three times more corrugated volume per transaction than store-based sales, adding structural tonnage growth to the Europe paper market. Parallel growth in takeaway and delivery meals inflates demand for grease- and moisture-resistant wraps. Mills have responded by installing on-demand flexo and ink-jet lines that cost-effectively customise small batches, lowering inventory risk for e-tailers. Urban micro-fulfilment hubs now specify easy-fold case designs that improve pick-pack efficiency and reduce void space. Together, these channels offset soft demand in legacy commercial print, underscoring packaging's role as the ballast of Europe paper market resilience.

Volatile Wood-Pulp and Recovered Paper Prices

Swedish roundwood cost inflation of 30% in 2024 eroded mill margins and exposed the vulnerability of non-integrated producers to commodity swings. Geopolitical constraints on Russian and Belarusian fiber imports have tightened the regional supply pool, pushing mills to secure multiyear offtake contracts or acquire forest assets outright. Recovered paper collection costs also escalated due to driver shortages and higher diesel prices, narrowing the price advantage versus virgin pulp. Vertical integration now confers a decisive hedge, illustrated by Stora Enso's partial forest divestiture balanced by long-term stumpage agreements. Without pricing power in commoditized grades, smaller independents risk negative cash flow during spikes, underscoring raw-material volatility as the most acute operational headwind.

Other drivers and restraints analyzed in the detailed report include:

- EU Circular-Economy Mandates on Fiber Packaging

- Rising Hygiene-Paper Consumption Post-COVID

- Digital Media Substitution of Graphic Papers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Case Materials represented 33.78% of Europe paper market share in 2025, underpinning the packaging backbone that services e-commerce, food, and industrial supply chains. Corrugated case grades captured downstream migration from graphic mills, adding low-cost capacity without green-field lead times. Producers leveraged lightweighting technology to cut grammage while maintaining stacking strength, aligning with retailer sustainability scorecards. Specialty Papers, though just 8.92 million tonnes in 2025, deliver a 5.95% CAGR, buoyed by food-grade barrier coatings, security substrates, and technical laminates for electronics. These niches command price premiums that offset higher formulation costs and compliance testing, making them an attractive diversification play for large integrated houses.

The structural headwinds facing Graphic Papers remain unabated; nonetheless, premium magazines and art books continue to demand tactile quality beyond digital screens, preserving a viable albeit shrinking niche. Sanitary and Household papers benefit from defensive demand characteristics and ongoing hygiene awareness. Wrappings and Carton Board capitalise on retailer plastic-bag bans and omnichannel retail packaging redesigns. Looking ahead, industrial printing innovation such as water-based flexo for Case Materials introduces new value-added revenue streams, cementing the central role of Case Materials in the Europe paper market.

Recycled Fiber accounted for 52.64% of Europe paper market size in 2025, confirming the region's leadership in closed-loop material flows. Collection systems supported by Extended Producer Responsibility schemes achieve recovery rates that outpace most other regions. As eco-design criteria evolve, converters redesign packaging for de-inkability and fiber retention, reinforcing recycled fiber throughput. Virgin Fiber usage posts the fastest 4.34% CAGR, owing to premium packaging where organoleptic purity and tear resistance are non-negotiable. Integrated forest companies exploit certified forestry assets to supply these segments, often pairing primary pulp with increased recycled content elsewhere to meet overall sustainability targets.

Agro-Residue Fiber remains nascent but garners interest as mills pilot wheat-straw and miscanthus pulping to diversify procurement risk and lower carbon intensity. Continental policy that tightens deforestation traceability requirements further elevates recycled and alternative fibers' relative attractiveness. Meanwhile, mill trials on enzymatic de-inking show promise in lifting recycled-fiber brightness, expanding its applicability in premium white grades, and bolstering the circular narrative that underpins the Europe paper market.

The Europe Paper Market Report is Segmented by Product Type (Graphic Papers, Case Materials, Sanitary and Household, Wrappings, Carton Board, and Specialty Papers), Raw-Material Source (Virgin Fiber, Recycled Fiber, and Agro-Residue Fiber), Basis-Weight (Below 90 Gsm, and More), End-Use Industry (Packaging and Industrial, and More), and Geography (Germany, and More). The Market Forecasts are Provided in Terms of Volume (Tonnes).

List of Companies Covered in this Report:

- Stora Enso Group

- UPM-Kymmene Corporation

- Smurfit Westrock plc

- Mondi plc

- Metsa Group

- Holmen AB

- Svenska Cellulosa Aktiebolaget SCA

- Mayr-Melnhof Karton AG

- PRINZHORN HOLDING GmbH

- Norske Skog ASA

- Burgo Group S.p.A

- Lecta Group

- Reno de Medici S.p.A

- Sappi Limited

- Grigeo AB

- Iberpapel Gestion S.A

- Heinzel Group

- Fedrigoni SpA

- Arctic Paper S.A

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Use of Sustainable Packaging

- 4.2.2 Expansion of E-commerce and Food-service Demand

- 4.2.3 EU Circular-Economy Mandates on Fiber Packaging

- 4.2.4 Rising Hygiene-Paper Consumption Post-COVID

- 4.2.5 Commercialisation of 3-D Molded-Fiber Packaging

- 4.2.6 On-demand Ink-jet Corrugated Printing Adoption

- 4.3 Market Restraints

- 4.3.1 Volatile Wood-Pulp and Recovered Paper Prices

- 4.3.2 Digital Media Substitution of Graphic Papers

- 4.3.3 Energy and Carbon-credit Price Inflation

- 4.3.4 Tighter Water-Use Regulations for Mills

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Product Type

- 5.1.1 Graphic Papers

- 5.1.1.1 Newsprint

- 5.1.1.2 Other Graphic Papers

- 5.1.2 Case Materials

- 5.1.3 Sanitary and Household

- 5.1.4 Wrappings

- 5.1.5 Carton Board

- 5.1.6 Specialty Papers

- 5.1.1 Graphic Papers

- 5.2 By Raw-Material Source

- 5.2.1 Virgin Fiber

- 5.2.2 Recycled Fiber

- 5.2.3 Agro-Residue Fiber

- 5.3 By Basis-Weight

- 5.3.1 Below 90 gsm (Lightweight)

- 5.3.2 90-200 gsm (Mediumweight)

- 5.3.3 Above 200 gsm (Heavyweight)

- 5.4 By End-use Industry

- 5.4.1 Packaging and Industrial

- 5.4.2 Printing and Publishing

- 5.4.3 Hygiene and Sanitary

- 5.4.4 Food-service Disposables

- 5.4.5 Other End-use Industries

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 France

- 5.5.3 Sweden

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Stora Enso Group

- 6.4.2 UPM-Kymmene Corporation

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Mondi plc

- 6.4.5 Metsa Group

- 6.4.6 Holmen AB

- 6.4.7 Svenska Cellulosa Aktiebolaget SCA

- 6.4.8 Mayr-Melnhof Karton AG

- 6.4.9 PRINZHORN HOLDING GmbH

- 6.4.10 Norske Skog ASA

- 6.4.11 Burgo Group S.p.A

- 6.4.12 Lecta Group

- 6.4.13 Reno de Medici S.p.A

- 6.4.14 Sappi Limited

- 6.4.15 Grigeo AB

- 6.4.16 Iberpapel Gestion S.A

- 6.4.17 Heinzel Group

- 6.4.18 Fedrigoni SpA

- 6.4.19 Arctic Paper S.A

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment