|

시장보고서

상품코드

1934845

클라우드 컴퓨팅 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cloud Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

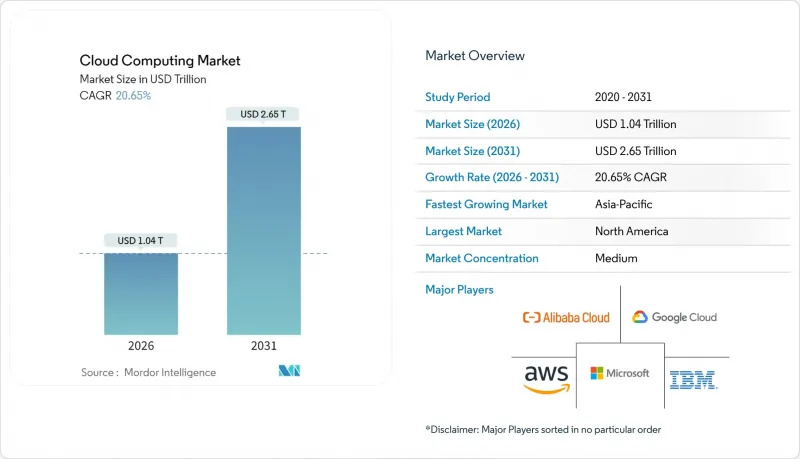

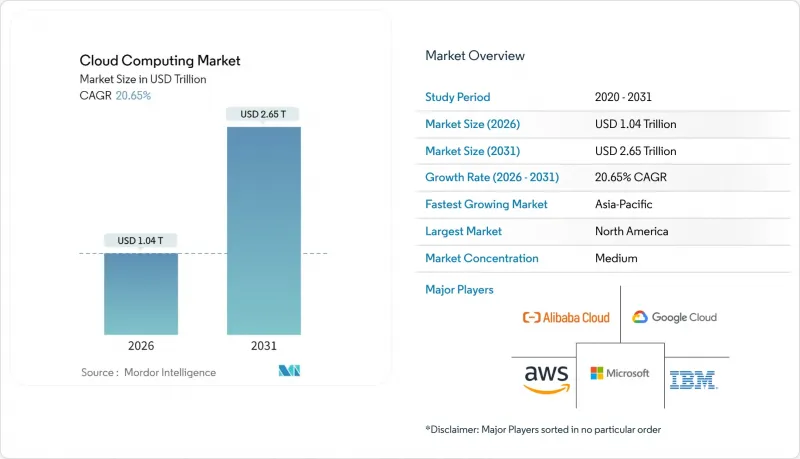

클라우드 컴퓨팅 시장은 2025년 8,600억 달러에서 2026년에는 1조 400억 달러로 성장하며, 2026-2031년에 CAGR 20.65%로 추이하며, 2031년까지 2조 6,500억 달러에 달할 것으로 예측됩니다.

이러한 빠른 성장은 AI를 최우선으로 하는 디지털 전환 계획, 핵심 용도의 SaaS 플랫폼으로의 전환, 유럽 및 걸프 지역의 소버린 클라우드 규제 확대, 확장현실(XR) 및 자율 운영 이용 사례를 지원하는 10밀리초 미만의 엣지 클라우드 존의 구축과 밀접하게 연관되어 있습니다. 확장현실(XR) 및 자율운영 사용사례를 지원하는 10밀리초 미만 엣지 클라우드 존의 구축과 밀접한 관련이 있습니다. 이에 따라 하이퍼스케일 프로바이더들은 GPU가 풍부한 데이터센터 설치 면적을 빠르게 확장하고 있으며, 산업별 특화 클라우드 설계도는 의료, 금융, 공공 부문의 컴플라이언스 대응을 간소화하고 있습니다. 동시에 기업의 워크로드 이동성 및 비용 관리 추구에 따라 하이브리드 클라우드 전략의 중요성이 커지고 있습니다. 공급자 간 경쟁 심화로 멀티 클라우드 상호운용성이 최우선 과제로 떠오르며, 새로운 가치 창출의 원천으로 락인(Lock-in)보다 개방형 생태계가 강조되고 있는 상황입니다.

세계 클라우드 컴퓨팅 시장 동향 및 인사이트

핵심 업무용 소프트웨어에서 SaaS의 폭발적 확산

클라우드 전환 대상은 생산성 워크로드뿐만 아니라 핵심 업무인 ERP(전사적 자원관리), CRM(고객관계관리), 재무 시스템까지 확대되고 있으며, 이러한 변화가 클라우드 컴퓨팅 시장 전체를 형성하는 경향이 강해지고 있습니다. 델타항공은 2024년까지 5억 달러를 투자해 디지털 기반 혁신에 투자하고, SaaS를 활용하여 AI 기반 개인화 및 정시 운항률 향상을 실현합니다. 이러한 전환을 통해 On-Premise 소프트웨어에서는 불가능한 지속적인 기능 업데이트와 내장형 분석이 가능해져 실시간 의사결정이 가능해졌습니다. 규제 대상 산업에서는 SaaS 스택에 내장된 표준화된 컴플라이언스 관리 기능을 통해 감사 속도를 높이고 운영 비용을 절감할 수 있습니다. 전환을 늦추는 조직은 SaaS를 우선적으로 도입하는 경쟁사에 비해 기능 격차 및 제품 주기 지연의 위험에 직면하게 됩니다.

탄력적 컴퓨팅을 필요로 하는 생성형 AI 워크로드의 급격한 증가

거대 언어 모델 학습을 위해서는 수천 개의 고대역폭 GPU를 병렬로 실행해야 하는데, 이는 기존 기업 워크로드 규모를 훨씬 능가하는 수준입니다. Oracle은 2025년 OpenAI를 지원하는 텍사스 거점을 위해 400억 달러 상당의 엔비디아 프로세서를 확보했습니다. 이 규모는 데이터센터의 전력 공급, 냉각, 네트워크 패브릭 설계에 근본적인 변화를 가져올 것입니다. 각 업체들은 AI 최적화 실리콘, 직접 액체 냉각, 고속 인터커넥트를 중심으로 재설계하여 증가하는 수요에 대응하고 있습니다. 고객들은 폭발적인 AI 실험과 생산 추론에서 용량 보장 및 유리한 경제성을 제공할 수 있는 벤더를 선택하는 경향이 있습니다.

데이터 현지화법으로 세계 발자국을 분할하는 방법

각 관할권별 거주지 규정으로 인해, 공급자는 인프라를 복제하고 독립적인 논리적 환경을 구축해야 하며, 이는 비용과 운영상의 복잡성을 증가시킵니다. 다국적 기업은 스토리지, 처리 및 인력 접근에 대한 중복된 의무에 직면하여 종종 아키텍처 재설계와 서비스 가격 상승을 강요당하고 있습니다.

부문 분석

서비스형 플랫폼(PaaS)은 2026-2031년 22.85%의 연평균 성장률(CAGR)을 보일 것으로 예상되며, 서비스 모델 중 가장 빠른 속도로 성장할 것으로 예측됩니다. SaaS는 2025년 매출의 52.87%라는 압도적인 점유율을 유지할 것이며, IaaS(Infrastructure as a Service)는 그 아래에서 유연한 기반 역할을 계속할 것입니다. PaaS의 물결은 컨테이너 오케스트레이션, 서버리스 런타임, 로우코드 툴에 의해 추진되어 릴리스 주기를 몇 달에서 몇 주 단위로 단축시킵니다. 아마존은 이러한 PaaS 워크로드를 지원하는 AI 중심 데이터센터에 1,500억 달러를 투자했습니다. 공급자가 임베디드 보안 및 AI 서비스로 플랫폼을 강화함에 따라 개발자는 배관 작업이 아닌 사용자 가치에 집중할 수 있는 자유를 얻게 되었습니다.

클라우드 컴퓨팅 시장에서 PaaS 업체들은 산업별 프레임워크와 통합형 MLOps를 통해 차별화를 강화하고 있습니다. 이러한 기능들은 고급 분석의 배포 기간을 단축하고, 코드 품질을 향상시키며, 개발자의 수고를 덜어줍니다. 이러한 조합으로 PaaS는 디지털 제품의 전략적 수단으로 자리매김하여 신속한 실험과 지속적 제공을 지원하고 있습니다.

2025년 프라이빗 클라우드는 매출의 46.62%를 차지했으며, 하이브리드 클라우드는 CAGR 22.24%로 성장하고 있습니다. 이 모델은 민감한 워크로드에 대한 데이터 근접성을 유지하면서 테스트, 분석, 재해복구를 위해 퍼블릭 클라우드의 용량을 버스트(Burst) 방식으로 활용합니다. 기업이 On-Premise 기반과 아웃소싱 용량에 걸쳐 쿠버네티스 컨트롤 플레인을 표준화함에 따라 하이브리드 배포 클라우드 컴퓨팅 시장 규모는 급격히 확대될 것으로 예측됩니다.

Oracle과 AWS의 크로스 클라우드 계약으로 데이터 전송 수수료가 불필요해졌고, Oracle 데이터베이스가 두 공급자 모두에서 원활하게 운영될 수 있게 되었습니다. 상호운용성을 통해 벤더 종속 우려를 줄이고, 고객은 성능과 가격을 최적화할 수 있습니다. 결과적으로 하이브리드 전략은 컴플라이언스의 안전판이자 위험부담이 큰 전면적 전환 없이 현대화를 위한 발판으로 자리매김하고 있습니다.

클라우드 컴퓨팅 시장은 서비스 모델(IaaS, PaaS, SaaS), 도입 모델(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 최종사용자 업종(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 제조업 등), 조직 규모(대기업, 중소기업(SME)), 지역별로 세분화됩니다. 및 지역별로 세분화됩니다. 시장 예측은 금액(USD)으로 제공됩니다.

지역별 분석

북미는 클라우드 배포의 선도적 우위와 디지털 네이티브 기업의 밀집으로 2025년 매출의 24.18%를 차지할 것으로 예측됩니다. 아마존은 펜실베니아와 노스 캐롤라이나 캠퍼스에 300억 달러를 투자하고, 마이크로소프트는 2025 회계연도에 800억 달러의 설비투자를 계획하고 있습니다. 이 지역의 성장은 현재 인력 및 연구 거점과의 근접성을 필요로 하는 AI 워크로드를 중심으로 이루어지고 있습니다. 캐나다와 멕시코에서는 기업이 워크로드를 분산시켜 중복성과 비용 최적화를 위해 워크로드를 분산시킴으로써 새로운 기회가 창출되고 있습니다.

유럽에서는 적극적인 디지털 혁신 목표와 엄격한 데이터 주권 규제의 균형이 클라우드 컴퓨팅 시장에서 이 지역의 궤도를 형성하고 있습니다. 조직은 민감한 데이터는 로컬에 보관하고 개발 및 분석은 세계 클라우드를 활용하는 하이브리드 아키텍처를 선호합니다. OVHcloud와 같은 프로바이더들은 유럽 데이터 거주성을 고유한 세일즈 포인트로 강조하고 있습니다. 브렉시트 이후 지정학적 변화로 인해 영국 기업은 진화하는 국경 간 데이터 협정에 대응해야 하며, 하이브리드 도입이 더욱 강화되고 있습니다.

아시아태평양은 미래 성장 동력이며, 예상 CAGR은 21.65%입니다. 인프라 프로젝트는 빠르게 확장되고 있으며, Sify는 인도의 AI 전문 데이터센터에 50억 달러를 투자할 예정입니다. 알리바바 클라우드, 텐센트 클라우드 등 국내 대기업이 중국 시장을 독점하고 있는 반면, 해외 업체들은 일본, 한국, 인도, 급성장하는 아세안 국가를 타겟으로 삼고 있습니다. 각국 정부는 클라우드 퍼스트 정책과 스마트 시티 계획을 지원하고 있으며, 확장 가능한 플랫폼에 대한 수요를 가속화하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The Cloud Computing market is expected to grow from USD 0.86 trillion in 2025 to USD 1.04 trillion in 2026 and is forecast to reach USD 2.65 trillion by 2031 at 20.65% CAGR over 2026-2031.

The surge is tied to AI-first digital-transformation agendas, enterprise migration of core applications to Software-as-a-Service (SaaS) platforms, expanding sovereign-cloud rules in Europe and the Gulf, and the rollout of sub-10 millisecond edge-cloud zones that underpin extended-reality (XR) and autonomous-operations use cases. Hyperscale providers are therefore racing to enlarge GPU-rich data-center footprints, while industry-specific cloud blueprints simplify compliance for health, finance, and the public sector. At the same time, hybrid-cloud strategies gain prominence as enterprises seek workload portability and cost discipline. Intensifying competition among providers is pushing multi-cloud interoperability to the forefront, positioning open ecosystems over lock-in as a new source of value creation.

Global Cloud Computing Market Trends and Insights

Explosive SaaS adoption in core enterprise software

Cloud migrations now encompass mission-critical enterprise-resource-planning, customer-relationship-management, and finance systems rather than only productivity workloads, a shift that is increasingly shaping the broader Cloud Computing Market. Delta Air Lines finalized a USD 500 million overhaul of its digital core in 2024, using SaaS to enable AI-driven personalization and punctuality improvements. The pivot delivers continuous feature updates and embedded analytics, unlocking real-time decision-making that on-premises software cannot match. Regulated sectors benefit from standardized compliance controls baked into SaaS stacks, accelerating audits and lowering operational overhead. Organizations delaying migration risk capability gaps and slower product cycles compared with SaaS-first peers

Proliferation of Gen-AI workloads demanding elastic compute

Large-language-model training requires thousands of high-bandwidth GPUs operating in parallel, dwarfing previous enterprise-workload footprints. Oracle reserved USD 40 billion worth of Nvidia processors for a Texas site supporting OpenAI in 2025. Such scale drives radical shifts in data-center power, cooling, and network fabric design. Providers are re-architecting around AI-optimized silicon, direct-liquid cooling, and high-speed interconnects to satisfy growing demand. Customers gravitate toward vendors able to guarantee capacity and favorable economics for bursty AI experiments and production inference.

Data-localization laws fragmenting global footprints

Jurisdiction-specific residency rules compel providers to duplicate infrastructure and create discrete logical environments, adding cost and operational complexity. Multinationals face overlapping obligations on storage, processing, and personnel access, often forcing architectural redesigns and higher service prices.

Other drivers and restraints analyzed in the detailed report include:

- Industry-specific cloud platforms (compliance-ready blueprints)

- Sovereign-cloud mandates in EU and GCC

- Run-rate cost overruns vs on-prem TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform-as-a-Service is forecast to compound at 22.85% from 2026-2031, the quickest pace among service models. SaaS retained a commanding 52.87% of 2025 revenue, while Infrastructure-as-a-Service remains the elastic foundation underneath. The PaaS wave is fueled by container orchestration, serverless runtimes, and low-code tools that compress release cycles from months to weeks. Amazon earmarked USD 150 billion for AI-centric data centers catering to those PaaS workloads. As providers enrich platforms with built-in security and AI services, developers gain more freedom to focus on user value rather than plumbing.

In the cloud computing market, PaaS vendors increasingly differentiate through industry frameworks and integrated MLOps. These capabilities shorten deployment of advanced analytics, raise code quality, and reduce developer toil. The combination positions PaaS as a strategic lever for digital products, underpinning rapid experimentation and continuous delivery.

Although private clouds captured 46.62% revenue in 2025, hybrid clouds are expanding at 22.24% CAGR. The model preserves data closeness for sensitive workloads while bursting to public capacity for testing, analytics, and disaster recovery. The cloud computing market size for hybrid deployments is set to rise sharply as firms standardize Kubernetes control planes across on-premises cores and outsourced capacity.

Oracle's cross-cloud pact with AWS eliminates data-egress fees and permits Oracle Database to run seamlessly on either provider. Interoperability curbs vendor-lock fears and lets customers optimize on performance or price. Consequently, the hybrid strategy is viewed as a safety valve for compliance and a springboard for modernization without risky forklift migrations.

Cloud Computing Market is Segmented by Service Model (IaaS, Paas, Saas). Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), End User Vertical (IT and Telecom, BFSI, Manufacturing, and More), Organization Size (Large Enterprises, Small and Mid-Sized Enterprises (SMEs)) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 24.18% of 2025 revenue thanks to an early lead in cloud adoption and dense clusters of digital-native enterprises. Investment continues: Amazon is channeling USD 30 billion into Pennsylvania and North Carolina campuses, while Microsoft plans USD 80 billion in fiscal-year 2025 capacity. Growth in the region now pivots around AI workloads that demand proximity to talent and research hubs. Canada and Mexico open incremental opportunities as firms spread workloads for redundancy and cost optimization.

Europe balances aggressive digital-transformation targets with stringent data-sovereignty rules, shaping the region's trajectory within the Cloud Computing Market. Organizations favor hybrid architectures that keep sensitive data local yet leverage global clouds for development and analytics. Providers such as OVHcloud emphasize European data residency as a unique selling point. Geopolitical shifts post-Brexit compel UK businesses to navigate evolving cross-border data agreements, further reinforcing hybrid adoption.

Asia-Pacific is the engine of future expansion, with a projected 21.65% CAGR. Infrastructure projects scale rapidly: Sify will invest USD 5 billion in Indian AI-focused data centers. Domestic champions such as Alibaba Cloud and Tencent Cloud dominate China, while international providers target Japan, South Korea, India, and fast-growing ASEAN states. Governments back cloud-first policies and smart-city programs, accelerating demand for scalable platforms.

- Amazon (AWS)

- Microsoft

- Google Cloud

- Alibaba Cloud

- IBM

- Oracle

- Salesforce

- SAP SE

- Adobe

- Tencent Cloud

- Huawei Cloud

- Rackspace

- VMware

- Snowflake

- Workday

- ServiceNow

- DigitalOcean

- OVHcloud

- Linode

- Nutanix

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive SaaS adoption in core enterprise software

- 4.2.2 Proliferation of Gen-AI workloads demanding elastic compute

- 4.2.3 Industry-specific cloud platforms (compliance-ready blueprints)

- 4.2.4 Sovereign-cloud mandates in EU and GCC

- 4.2.5 Rise of less than 10 ms edge-cloud zones for XR and autonomous ops

- 4.2.6 Green-cloud buying criteria tied to Scope-3 targets

- 4.3 Market Restraints

- 4.3.1 Data-localisation laws fragmenting global footprints

- 4.3.2 Run-rate cost overruns vs on-prem TCO

- 4.3.3 Advanced chip export controls limiting GPU supply

- 4.3.4 Scarcity of low-carbon power for hyperscale DCs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Model

- 5.1.1 IaaS

- 5.1.2 PaaS

- 5.1.3 SaaS

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By End-user Vertical

- 5.3.1 IT and Telecom

- 5.3.2 BFSI

- 5.3.3 Manufacturing

- 5.3.4 Retail and Consumer Goods

- 5.3.5 Healthcare and Life Sciences

- 5.3.6 Others

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Mid-Sized Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Southeast Asia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.2.5 Egypt

- 5.5.5.2.6 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon (AWS)

- 6.4.2 Microsoft

- 6.4.3 Google Cloud

- 6.4.4 Alibaba Cloud

- 6.4.5 IBM

- 6.4.6 Oracle

- 6.4.7 Salesforce

- 6.4.8 SAP SE

- 6.4.9 Adobe

- 6.4.10 Tencent Cloud

- 6.4.11 Huawei Cloud

- 6.4.12 Rackspace

- 6.4.13 VMware

- 6.4.14 Snowflake

- 6.4.15 Workday

- 6.4.16 ServiceNow

- 6.4.17 DigitalOcean

- 6.4.18 OVHcloud

- 6.4.19 Linode

- 6.4.20 Nutanix

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment