|

시장보고서

상품코드

1934858

버티컬 소프트웨어 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vertical Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

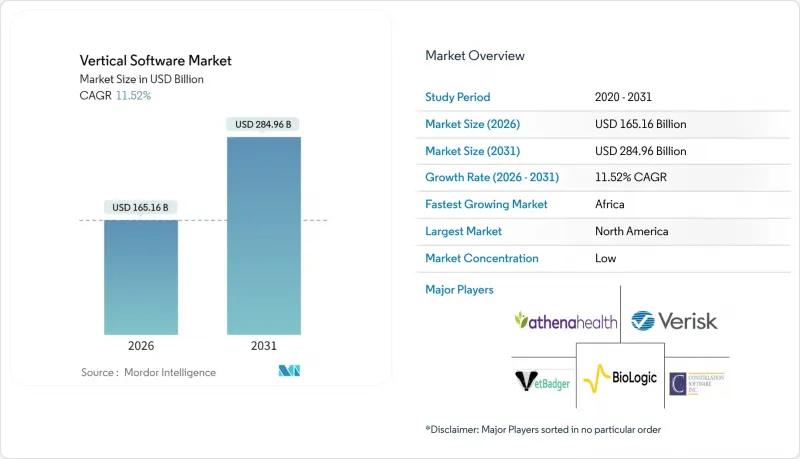

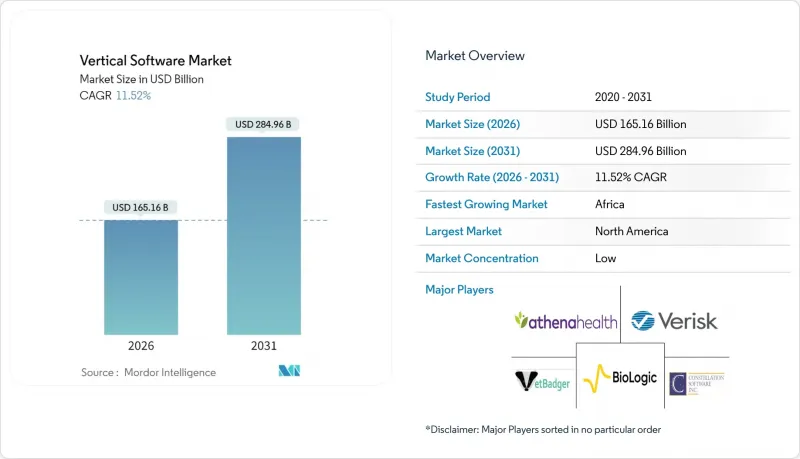

버티컬 소프트웨어 시장은 2025년에 1,481억 달러로 평가되었으며, 2026년 1,651억 6,000만 달러에서 2031년까지 2,849억 6,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 11.52%로 예상됩니다.

클라우드 우선 제공 모델, 임베디드 규제 프레임워크, 인공지능 툴킷은 규제 산업, 중규모 제조업, 농업 분야에서의 도입을 가속화하고 있습니다. 기존 수평형 벤더와 순수 전문업체 간 경쟁 심화로 도메인 레벨의 워크플로우, 임베디드 결제를 통한 제품 차별화가 진행되고 있습니다. 북미가 선두를 유지하고 있지만, 아프리카는 정부의 디지털 현대화 지원과 구독 가격 책정을 통한 중소기업의 장벽을 낮춤으로써 가장 빠르게 성장하고 있습니다. 반면, 사이버배상책임보험료의 상승과 공공부문의 레거시 데이터 사일로화 현상이 지속되면서 도입 속도는 더디게 진행되고 있습니다.

세계 버티컬 소프트웨어 시장 동향 및 인사이트

산업별 클라우드 플랫폼의 부상으로 미국 및 유럽에서 도입 가속화

전용으로 설계된 산업별 특화 클라우드는 호환 가능한 데이터 모델과 사전 설정된 워크플로우를 통합하여 도입 주기를 크게 단축합니다. 유럽 클라우드 시장은 2023년 1,970억 달러에서 2024년 2,320억 달러로 급성장하고 있으며, 빠른 보급이 눈에 띕니다. 병원, 공장, 은행, 소매업체들은 커스텀 코딩과 감사 위험을 최소화하기 위해 턴키 플랫폼을 선택하는 경향이 증가하고 있습니다. 이러한 클라우드에 내장된 금융 서비스는 지속적인 수익과 락인(lock-in)을 강화하여 전체 버티컬 소프트웨어 시장의 CAGR을 3.5%로 끌어올리는 요인으로 작용하고 있습니다. 실시간 데이터 리니지, 레퍼런스 아키텍처, 지속적인 컴플라이언스 모니터링 등의 기능은 전환 비용을 더욱 강화하여 방어 가능한 경쟁 우위를 구축합니다.

BFSI(은행, 금융, 보험) 및 의료 분야의 규제 준수 압력이 증가함에 따라 전문 솔루션이 확대되고 있습니다.

2025년 10월부터 시행되는 공정대출 규정 개정으로 자동 평가 모델 도입이 의무화됨에 따라 은행은 감사추적과 모델 리스크 거버넌스가 내장된 소프트웨어로 전환해야 합니다. 마찬가지로, AI 기반 의료기기에 대한 모니터링이 강화되면서 의료 서비스 제공자는 추적 가능한 데이터 파이프라인과 관리형 업데이트 기능을 갖춘 플랫폼에 의존할 수밖에 없습니다. 이러한 압력으로 인해 벌금 및 평판 리스크를 피하려는 구매자의 수요가 증가하여 산업별 SaaS 성장률에 +2.8%의 기여를 하고 있습니다.

공공 부문의 수직적 클라우드 전환을 가로막는 레거시 데이터 사일로의 문제점

미 국방부 혁신위원회의 평가에서 알 수 있듯이, 파편화된 온프레미스 환경은 데이터의 발견성과 접근성이 낮아 상호운용성을 저해하고 있습니다. 복잡한 마이그레이션 프로그램은 예산을 부풀리고, 일정을 연장시키며, 버티컬 소프트웨어 시장에 1.2%의 부정적인 영향을 미치고 있습니다. 정부 기관에서는 단계적인 듀얼 런 아키텍처를 요구하는 경우가 많으며, 레거시 시스템 폐지가 완료될 때까지 클라우드의 이점 실현이 늦어지는 경향이 있습니다.

부문 분석

2025년 버티컬 소프트웨어 시장 규모의 69.92%는 클라우드 기반 서비스가 차지할 것으로 예상됩니다. 종량제, 자동 스케일링, 관리형 컴플라이언스 서비스를 통해 총소유비용(TCO)을 최대 30%까지 절감할 수 있습니다. 또한 기업들은 의사결정 지원을 강화하는 퍼블릭 클라우드 AI 서비스와의 임베디드 통합을 높이 평가하고 있습니다. 반면, 온프레미스 솔루션은 지출의 30.08%에 불과하지만, 데이터 주권 의무화 및 에어갭형 보안 요구사항이 다시 계획 의제로 떠오르면서 13.97%의 CAGR을 기록했습니다.

하이브리드 아키텍처가 표준화되고 있습니다. 조직은 고객의 개인 식별 정보(PII)와 유전체 데이터를 온프레미스에 보관하고, 익명화된 텔레메트리 데이터를 클라우드 분석 엔진으로 스트리밍합니다. 이러한 접근 방식은 규제 당국의 요구 사항을 충족시키면서 민첩성을 보장합니다. IoT 도입은 이러한 혼합 형태를 더욱 강화하여 운영 센서가 로컬 에지 서버와 클라우드 모델 모두에 데이터를 공급함으로써 실시간 인사이트와 장기적인 최적화를 실현할 수 있습니다. 이러한 환경을 아우르는 통합 오케스트레이션을 제공하는 벤더들은 현재 높은 수주율을 기록하고 있습니다.

기업이 2025년 매출의 51.67%를 차지할 것으로 예상되며, 이는 여러 지역에 걸친 배포와 복잡한 컴플라이언스 요구사항을 반영하고 있습니다. 기업들은 일반적으로 벤더의 로드맵을 기반으로, 임베디드 결제 및 데이터 교환 모듈을 통해 계정 확장을 촉진하는 단계별 세계 템플릿을 실행합니다. 그러나 중소기업(SME)의 채택도 가속화되고 있으며, 14.38%의 CAGR로 업계 전체 소프트웨어 시장을 능가하는 성장세를 보이고 있습니다. 월정액 요금제, 가이드 도입 마법사, 마켓플레이스 애드온을 통해 재정적 장벽과 기술적 장벽을 모두 낮췄습니다.

빅데이터 분석은 중소기업의 측정 가능한 이익 증대를 촉진하고, 자체 대시보드를 통한 공급업체 및 고객 행동에 대한 가시성 확보로 수익과 효율성을 개선하는 것으로 입증되었습니다. 벤더는 단계적 도입이 가능한 모듈형 패키지로 대응하여 업셀링 전 즉각적인 가치 창출을 보장하고 있습니다. 지방의 광대역 확대와 모바일 퍼스트 인터페이스는 특히 아프리카 및 동남아시아의 잠재적 수요를 더욱 개척하여 버티컬 소프트웨어 산업의 장기적인 대상 시장 규모를 강화하고 있습니다.

본 버티컬 소프트웨어 시장 보고서는 도입 모델(클라우드/온프레미스), 조직 규모(중소기업/대기업), 최종사용자 산업(은행/금융서비스/보험(BFSI)/교육기관 등), 애플리케이션(고객관계관리/기업 자원 계획 등), 지역별로 세분화하여 분석하였습니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 2025년 매출의 51.76%를 차지할 것으로 예상되며, 높은 수준의 클라우드 인프라, 풍부한 벤처 자금, 도메인이 풍부한 플랫폼을 평가하는 엄격한 컴플라이언스 체제가 뒷받침되고 있습니다. 전자건강기록 현대화 및 오픈 뱅킹 API에 대한 연방 정부의 인센티브는 수요를 더욱 강화하고 있습니다. 규제 분야의 대규모 레퍼런스 고객은 중견 시장 부문에 파급되는 실증 사례를 제공하여 네트워크 효과와 전체 수직적 소프트웨어 시장을 강화합니다.

아시아태평양은 14.02%의 CAGR로 성장하고 있습니다. 중국, 일본, 한국 등 제조업 중심의 경제권에서는 예측보전과 스마트 팩토리 구축을 위한 AI 툴킷이 도입되고 있습니다. 한편, 인도의 중소기업들은 구독 모델을 활용하여 레거시 시스템을 뛰어넘는 형태로 AI를 도입하고 있습니다. 이 지역의 AI 지출은 2027년까지 907억 달러에 달할 것으로 예상됩니다. 인재 부족은 계속되고 있지만, 일류 대학과 국경을 초월한 교육 파트너십이 기술 격차를 해소하는 데 기여하고 있습니다.

유럽에서는 복잡한 양상을 보이고 있습니다. 엄격한 데이터 보호 프레임워크는 인증된 통제 기능을 갖춘 산업용 클라우드에 대한 수요를 촉진하는 반면, 국경 간 규제 차이로 인해 복잡성과 비용이 발생합니다. 호스팅의 현지화, 주권 클라우드 표준에 대한 적합성 증명, ESG 보고 도구의 통합을 실현할 수 있는 공급자가 조달 경쟁에서 우위를 점하고 있으며, 수직 소프트웨어 시장의 모멘텀을 강화하고 있습니다. 아프리카는 15.97%의 가장 빠른 CAGR로 성장하고 있습니다. 중소기업의 급속한 디지털화와 농업, 핀테크, 의료 분야의 탄탄한 수요에 힘입어 아프리카는 버티컬 소프트웨어 시장에서 중요한 역할을 하기 시작했습니다. 남아프리카공화국, 나이지리아, 이집트가 선두에 서서 정부 주도의 디지털 혁신 이니셔티브에 힘입어 현지 규정 준수, 언어적 뉘앙스, 모바일 퍼스트 접근 방식에 대응하는 수직적 SaaS 솔루션 도입을 추진하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The vertical software market was valued at USD 148.10 billion in 2025 and estimated to grow from USD 165.16 billion in 2026 to reach USD 284.96 billion by 2031, at a CAGR of 11.52% during the forecast period (2026-2031).

Cloud-first delivery models, embedded regulatory frameworks, and artificial-intelligence toolkits are accelerating adoption across regulated industries, mid-sized manufacturing, and agriculture. Intensifying competition between incumbent horizontal vendors and pure-play specialists is sharpening product differentiation through domain-level workflows and embedded payments. North America retains a leadership position, but Africa is expanding fastest as governments support digital modernization and as subscription pricing lowers barriers for small and medium enterprises. Simultaneously, rising cyber-liability premiums and persistent legacy data silos in the public sector temper deployment velocity.

Global Vertical Software Market Trends and Insights

Emergence of Industry-specific Cloud Platforms Accelerating Adoption in US & Europe

Purpose-built industry clouds radically shorten implementation cycles by bundling compliant data models and pre-configured workflows. Rapid uptake is evident in the European cloud market, which rose from USD 197 billion in 2023 to USD 232 billion in 2024. Hospitals, factories, banks, and retailers increasingly choose turnkey platforms to minimise custom coding and audit risk. Embedded financial services within these clouds augment recurring revenue and lock-in, driving the +3.5% lift to the overall vertical software market CAGR. Capabilities such as real-time data lineage, reference architectures, and continuous compliance monitoring further strengthen switching costs and create defensible moats.

Regulatory Compliance Pressures in BFSI & Healthcare Boosting Specialized Solutions

Evolving fair-lending rules effective October 2025 require automated valuation models, pushing banks toward software that embeds audit trails and model-risk governance. Parallel scrutiny surrounds AI-enabled medical devices, compelling providers to rely on platforms with traceable data pipelines and managed updates. These pressures escalate demand for sector-specific SaaS, producing a +2.8% contribution to growth as buyers seek to avoid fines and reputational risk.

Legacy Data Silos Slowing Vertical Cloud Migration in the Public Sector

Fragmented on-premise estates hinder interoperability, as documented by the US Defense Innovation Board's assessment of poor data discoverability and access. Complex migration programs inflate budgets and extend timelines, causing a -1.2% drag on the vertical software market. Agencies often require phased dual-run architectures that slow realisation of cloud benefits until legacy retirement is complete.

Other drivers and restraints analyzed in the detailed report include:

- AI/ML Toolkits Driving Mid-sized Manufacturing Modernization in Asia-Pacific

- Digitalization of Ag-food Supply Chains Fueling AgTech SaaS in South America

- Rising Cyber-Liability Insurance Costs Inflating TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based offerings account for 69.92% of the vertical software market size in 2025. Pay-as-you-go pricing, auto-scaling, and managed compliance services lower total ownership costs by up to 30%. Enterprises also value built-in integration to public cloud AI services that sharpen decision support. Conversely, on-premise solutions, while only 30.08% of spending, register a 13.97% CAGR as data-sovereignty mandates and air-gapped security requirements re-enter the planning agenda.

Hybrid architectures are becoming standard; organisations retain customer PII or genomic data on-site while streaming anonymised telemetry into cloud analytics engines. The approach satisfies regulators yet still captures agility. IoT adoption amplifies this mix, as operational sensors feed both local edge servers and cloud models, yielding real-time insights and long-term optimisation. Suppliers that offer unified orchestration across these environments now enjoy premium win rates.

Enterprises accounted for 51.67% of 2025 revenue, reflecting multi-site rollouts and complex compliance demands. They typically execute phased global templates that anchor vendor roadmaps and feed account expansion via embedded payments or data-exchange modules. However, SME uptake is accelerating, delivering a 14.38% CAGR that outpaces the overall vertical software market. Pay-monthly pricing, guided implementation wizards, and marketplace add-ons lower both financial and skills barriers.

Big-data analytics drive measurable gains for smaller firms, with studies showing revenue and efficiency improvements once proprietary dashboards reveal supplier and customer behavior. Vendors respond with modular packaging that allows incremental adoption, ensuring immediate value before upsell. Rural broadband expansion and mobile-first interfaces further open latent demand, particularly in Africa and Southeast Asia, reinforcing the long-run addressable pool for the vertical software industry.

The Vertical Software Market Report Segmented by Deployment Model (Cloud, and On-Premises), Organization Size (Small and Medium Enterprise, and Large Enterprise), End-User Industry (Banking, Financial Services, and Insurance (BFSI), Educational Institution, and More), Application (Customer Relationship Management, Enterprise Resource Planning, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 51.76% of 2025 revenue, supported by sophisticated cloud infrastructure, deep venture funding, and strict compliance regimes that reward domain-rich platforms. Federal incentives for electronic health-record modernisation and open banking APIs further cement demand. Large-scale reference customers in regulated arenas provide proof points that ripple through mid-market segments, reinforcing network effects and the overall vertical software market.

Asia-Pacific is advancing at a 14.02% CAGR. Manufacture-heavy economies, such as China, Japan, and South Korea, deploy AI toolkits for predictive maintenance and smart-factory orchestration, while India's SME population leverages subscription models to leapfrog legacy systems. Regional AI spending is expected to hit USD 90.7 billion by 2027. Although talent constraints persist, tier-one universities and cross-border training partnerships are helping to narrow the skills gap.

Europe presents mixed dynamics with a stringent data-protection framework spurs demand for industry clouds with certified controls, yet cross-border regulatory divergence introduces complexity and cost. Providers able to localise hosting, attest to sovereign-cloud standards, and integrate ESG reporting tools are winning procurement contests and reinforcing momentum in the vertical software market. Africa is expanding at fastest CAGR of 15.97%. Driven by swift SME digitization and robust demand in agriculture, fintech, and healthcare, Africa is carving out a pivotal role in the vertical software market. South Africa, Nigeria, and Egypt are at the forefront, championing the adoption of vertical SaaS solutions that cater to local compliance, language nuances, and a mobile-first approach, all bolstered by government-led digital transformation initiatives.

- Constellation Software Inc.

- Verisk Analytics, Inc.

- athenahealth, Inc.

- Bio-Logic Science Instruments SA

- VetBadger LLC

- FastBound LLC

- Mail Technologies Inc.

- Granular, Inc. (Corteva)

- Farmbrite, LLC

- Renderforest LLC

- Veeva Systems Inc.

- Guidewire Software, Inc.

- Epic Systems Corporation

- Procore Technologies, Inc.

- Toast, Inc.

- Shopify Inc.

- Oracle Health (Cerner Corp.)

- Teladoc Health, Inc.

- IFS AB

- Infor, Inc.

- ServiceTitan, Inc.

- Blackbaud, Inc.

- MINDBODY, Inc.

- Intelerad Medical Systems Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Emergence of Industry-specific Cloud Platforms Accelerating Adoption in US and Europe

- 4.2.2 Regulatory Compliance Pressures in BFSI and Healthcare Boosting Specialized Solutions

- 4.2.3 AI/ML Toolkits Driving Mid-sized Manufacturing Modernization in Asia-Pacific

- 4.2.4 Digitalization of Ag-food Supply Chains Fueling AgTech SaaS in South America

- 4.2.5 Government-funded Smart-Hospital Programs Propelling Health-tech Software

- 4.2.6 Subscription Pricing Unlocking SME Penetration in Africa

- 4.3 Market Restraints

- 4.3.1 Legacy Data Silos Slowing Vertical Cloud Migration in Public Sector

- 4.3.2 Shortage of Domain-savvy Talent Limiting Customization Speed

- 4.3.3 Rising Cyber-Liability Insurance Costs Inflating TCO

- 4.3.4 Multi-jurisdiction Regulations Hindering Cross-border Rollouts in EU and ASEAN

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By End-User Industry

- 5.3.1 BFSI

- 5.3.2 Healthcare and Life Sciences

- 5.3.3 Education

- 5.3.4 Government and Legal

- 5.3.5 Media, Entertainment and Hospitality

- 5.3.6 Clothing and Apparel

- 5.3.7 Agriculture and Farming

- 5.3.8 Other End-user Industries

- 5.4 By Application

- 5.4.1 Customer Relationship Management

- 5.4.2 Enterprise Resource Planning

- 5.4.3 Supply Chain Management

- 5.4.4 Human Resource Management

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emiartes

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global and Market Overviews, Segments, Financials, Strategy, Rank/Share, Products, Developments)

- 6.4.1 Constellation Software Inc.

- 6.4.2 Verisk Analytics, Inc.

- 6.4.3 athenahealth, Inc.

- 6.4.4 Bio-Logic Science Instruments SA

- 6.4.5 VetBadger LLC

- 6.4.6 FastBound LLC

- 6.4.7 Mail Technologies Inc.

- 6.4.8 Granular, Inc. (Corteva)

- 6.4.9 Farmbrite, LLC

- 6.4.10 Renderforest LLC

- 6.4.11 Veeva Systems Inc.

- 6.4.12 Guidewire Software, Inc.

- 6.4.13 Epic Systems Corporation

- 6.4.14 Procore Technologies, Inc.

- 6.4.15 Toast, Inc.

- 6.4.16 Shopify Inc.

- 6.4.17 Oracle Health (Cerner Corp.)

- 6.4.18 Teladoc Health, Inc.

- 6.4.19 IFS AB

- 6.4.20 Infor, Inc.

- 6.4.21 ServiceTitan, Inc.

- 6.4.22 Blackbaud, Inc.

- 6.4.23 MINDBODY, Inc.

- 6.4.24 Intelerad Medical Systems Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment