|

시장보고서

상품코드

1934871

토양 안정화 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Soil Stabilization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

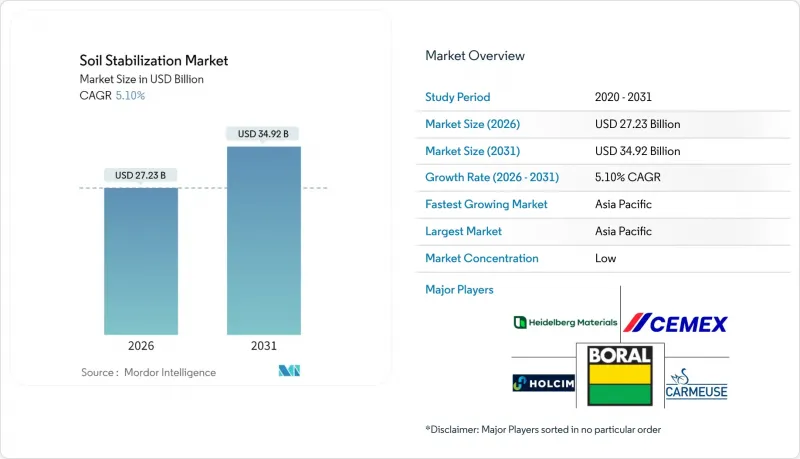

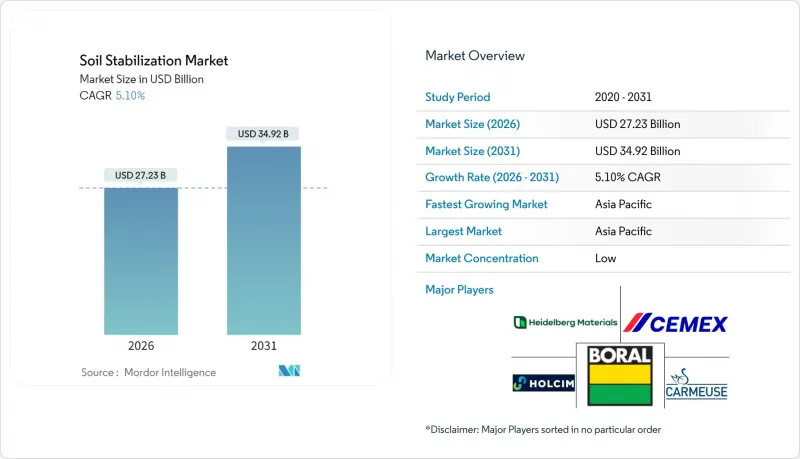

2026년 토양 안정화 시장의 규모는 272억 3,000만 달러로 추정되며, 2025년 259억 1,000만 달러에서 성장하며, 2031년에는 349억 2,000만 달러에 달할 것으로 예측됩니다.

2026-2031년에는 CAGR 5.1%로 성장할 전망입니다.

이 성장 경로는 기후 변화에 대응하는 유틸리티에 대한 지속적인 노력, 포장의 엄격한 내구성 기준, 저탄소 건축자재로 전환하는 세계의 변화를 반영하고 있습니다. 특히 신흥 메가시티의 도시화 확대는 다양한 토질 프로파일에 대응하고 공사 기간을 단축할 수 있는 지반 개량 솔루션에 대한 수요를 지속적으로 증가시키고 있습니다. 정부가 인프라 부양책을 지속가능성 지표와 연결시키면서, 소유주들은 고성능 안정화 처리를 임의적인 비용이 아닌 회복탄력성 투자로 인식하게 되었습니다. 기존 시멘트 및 석회 공급업체들은 저탄소화 및 규제 완화를 약속하는 바이오 혁신기업의 압력에 직면하여 경쟁이 심화되고 있습니다. 이를 통해 전체 밸류체인의 조달 기준이 재편되고 있습니다.

세계 토양 안정화 시장 동향 및 인사이트

인프라 및 도로 건설 활동의 성장

OECD에 따르면 기후 변화에 강한 인프라에 대한 연간 투자 필요액은 2,070억 달러에 달하며, 그 계획의 대부분은 도로, 철도, 공항에 집중되어 있습니다. 토목공사 계약에서는 수명주기 내구성과 조기사용을 실현하는 입찰자를 평가하는 지반개량 조항을 포함하는 경우가 증가하고 있습니다. 폭우로 인한 피해로 도로 관리 기관은 노반의 전단 강도 기준을 높여 노면 굴착과 토사 유출을 억제할 것을 요구하고 있습니다. 따라서 시산업체는 현지 토양의 이질성에 관계없이 재현성 있는 성능을 발휘하는 안정화 공법을 선호합니다. 이러한 경향은 정부가 복원력 지표에 연동된 그린본드 대출을 발행하고, 제3자의 성능 검증을 거친 프리미엄 안정화 기술에 대한 자금을 효과적으로 확보함에 따라 더욱 강화되고 있습니다.

비용 효율적인 지반 개량 솔루션에 대한 수요 증가

시멘트, 아스팔트, 골재 가격 상승 압력은 구조적 무결성을 유지하면서 자재량을 줄이는 처리 기술에 대한 소유자의 관심을 높이고 있습니다. 현장 혼합 공법은 토사 반출입 비용을 없애고, 연료 소비와 현장 교통량을 줄입니다. 물류비가 총 지출의 대부분을 차지하는 장거리 도로 구간에서는 이러한 절감 효과가 더욱 증폭됩니다. 또한 예상치 못한 지연이 예비 예산을 압박하는 경우가 많기 때문에 날씨로 인한 가동 중단 시간을 줄이는 솔루션이 우선시됩니다. 가치공학에 대한 검토가 활발해지면서 단위비용 절감과 검증된 전 생애주기 비용 절감을 동시에 달성할 수 있는 안정화 패키지는 특히 컨소시움이 장기 유지보수 의무를 부담하는 민관협력 계약에서 빠르게 수용되고 있습니다.

화학 안정제 관련 환경 문제

염화물계 첨가제에 따른 지하수 오염 위험으로 인해 환경영향 평가가 강화되고 있습니다. 유럽 규제 당국은 시멘트계 제품에 대해 제조 단계까지 탄소 공개를 요구하고 있으며, 캐나다에서도 유사한 규제를 검토 중입니다. 알트대학의 연구에 따르면 바이오차르계 결합재가 시멘트보다 더 나은 배출량 감소 효과와 흡착 특성을 보이는 것으로 보고되어 설계자들에게 고알칼리성 옵션의 채택을 재검토할 것을 촉구하고 있습니다. 책임 문제에 대한 우려는 브라운필드 재개발에도 적용되며, 복구 계약으로 인해 장기적인 컴플라이언스 비용이 개발업체에 전가되고 있습니다. 이러한 요인으로 인해 화학 혼합물의 승인이 지연되고 있지만, 높은 교통량 기준을 충족하는 기술적 대체품이 아직 존재하지 않는 분야에서는 과도기적 수요가 지속되고 있습니다.

부문 분석

화학 기술은 2025년 토양 안정화 시장의 73.45%를 차지할 것으로 예상되며, 이는 고속도로, 활주로 항만 플랫폼에서 수십년간 입증된 실적을 지원합니다. 이 부문은 설계 승인을 간소화하는 성숙한 기준과 대량 공급을 보장하는 세계 공급망의 혜택을 누리고 있습니다. 생물학적 대체 기술은 규모는 작지만, 효소 처리된 토양이 더 짧은 양생 기간으로 캘리포니아 지지력 비율(CBR) 기준을 달성할 수 있으므로 전체 방법 중 가장 높은 7.25%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다. 기계적 접근법은 첨가제가 제한되는 가설 공사나 생태계 보호 구역에서 여전히 유용합니다. 지오폴리머와 나노 강화 배합 기술은 틈새 시장이지만, 높은 굽힘 인성을 요구하는 지진 다발지역에서 주목받고 있습니다.

성능 기준은 기본적인 전단강도를 넘어 수명주기의 온실가스 배출량 산정, 흡수율 지표, 침출수 프로파일 등을 통합하는 방향으로 진화하고 있습니다. 이러한 재평가를 통해 상업적 성공과 환경적 평가가 연동되어 경쟁 환경의 재편이 진행되고 있습니다. 화학업체는 클링커 함량을 줄이기 위해 소성 점토 등 보조 시멘트질 재료를 배합하고, 생명공학 업체는 미생물에 의한 방해석 침전 기술을 특허로 출원하고 있습니다. 조달 기준이 성능 기반 사양으로 전환되는 가운데, 토양 안정화 시장에서는 재료 과학과 디지털 모니터링을 연계하여 현장 거동을 검증하는 다학제적 협업이 촉진되고 있습니다.

지역별 분석

아시아태평양은 2025년 일대일로, 인도의 스마트 시티 계획, 동남아시아의 항만 확장에 힘입어 전 세계 매출의 53.85%를 유지했습니다. 2031년까지 지역 CAGR 5.78%는 세계 평균을 상회하는 수치로, 각국 정부가 입찰 서류에 탄력성 지표를 포함시키고 있는 가운데, 세계 평균을 상회하는 수치입니다. 몬순에 의한 토양 변동성으로 인해 성토부 및 절토-성토 구간 전체에 대한 안정화가 필수적이며, 본 기술은 미션 크리티컬한 위치로 자리매김하고 있습니다. 중국의 석탄화력 발전의 단계적 억제에 따라 플라이애시 공급이 타이트해지면서 탄소강도가 낮은 마그네슘계 결합재의 시험 도입이 가속화되고 있습니다. 국책연구기관이 스타트업과 제휴하여 바이오찰 솔루션을 시범운영하는 움직임은 향후 조달구조의 변화를 시사하고 있습니다.

북미에서는 노반 개선에 자금을 투입하는 고속도로 포장재 갱신 사업으로 인해 견고한 수요가 유지되고 있습니다. 중서부 각 주 교통국에서는 실시간 탄성계수 센서를 도입하여 결합재 투여량을 미세 조정하여 재료 낭비를 줄이고 있습니다. 캐나다 각 주에서는 동결융해 사이클에서도 탄성을 유지하는 지오폴리머 혼합물의 한랭지 시험을 진행 중입니다. 규제 당국이 탄소 함량에 중점을 두면서 시멘트 대체율 50% 이상이 우선시되고, 시장은 혼합재 및 바이오소재로 전환되고 있습니다.

유럽에서는 지질공학적으로 실현 가능한 경우 굴착토의 재사용을 의무화하여 순환성 프런티어를 추진하고 있습니다. 독일과 프랑스에서는 도시철도 연장에 현장 안정화 처리를 적용하여 도심의 궤도 이동을 제한하고 있습니다. 스칸디나비아 기관은 시공 후 침하 데이터에 대한 계약자의 책임을 묻는 성능 보증을 선구적으로 도입하여 고품질 첨가제 사용을 장려하고 있습니다. 이 지역의 정책적 환경과 지속가능성에 대한 높은 사회적 인식이 결합되어 효소 및 지오폴리머 시스템의 채택이 가속화되고 있습니다.

남미, 중동, 아프리카는 정부가 물류 병목현상과 관광 인프라 문제를 해결하면서 새로운 핫스팟으로 떠오르고 있습니다. 브라질 교통부는 홍수가 발생하기 쉬운 아마존 강 유역의 고속도로 안정화를 규정하고 있으며, 걸프협력회의(GCC) 국가들은 고염분 토양을 상쇄하기 위해 나노실리카 혼합물을 실험하고 있습니다. 이 지역에서는 현지 재료에 맞는 비용 효율적인 솔루션이 중요시되고 있으며, 설계 서비스와 현장 교육을 패키지로 제공하는 공급업체가 선구자적 우위를 점하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

Soil Stabilization market size in 2026 is estimated at USD 27.23 billion, growing from 2025 value of USD 25.91 billion with 2031 projections showing USD 34.92 billion, growing at 5.1% CAGR over 2026-2031.

This growth path reflects sustained commitments to climate-resilient public works, stringent durability standards for pavements, and the global shift toward low-carbon construction materials. Expanding urban footprints, especially in emerging megacities, keep demand elevated for ground-improvement solutions that can handle variable soil profiles while shortening project schedules. Governments link infrastructure stimulus to sustainability metrics, so owners now view high-performance stabilization as a resilience investment rather than a discretionary cost. Competitive intensity is rising as established cement and lime suppliers face pressure from bio-based innovators that promise lower embodied carbon and easier regulatory clearance, reshaping procurement criteria across the value chain.

Global Soil Stabilization Market Trends and Insights

Growth in Infrastructure and Road Construction Activities

Annual climate-resilient infrastructure spending needs stand at USD 207 billion according to the OECD, and the pipeline mainly centers on roads, railways, and airports. Civil-engineering contracts are increasingly bundling ground-improvement clauses that reward bidders for lifecycle durability and quicker commissioning. Heavy precipitation events prompt highway agencies to specify higher shear-strength thresholds for subgrades to curb rutting and washouts. Contractors therefore favor stabilization methods that deliver repeatable performance regardless of local soil heterogeneity. The driver strengthens as governments release green-bond financing tied to resilience metrics, effectively ring-fencing capital for premium stabilization technologies with third-party performance validation.

Rising Demand for Cost-Effective Soil Treatment Solutions

Inflationary pressure on cement, bitumen, and aggregate keeps owners focused on treatments that cut material volumes while preserving structural integrity. In-situ mixing eliminates removal and haul-back costs, lowering fuel consumption and site traffic. Savings are amplified on long-haul road corridors where logistics represent a large fraction of total outlays. Owners also prioritize solutions that lessen weather-related downtime, since unplanned delays often erode contingency budgets. As value-engineering reviews intensify, stabilization packages that pair lower unit costs with documented whole-life savings find rapid acceptance, especially among public-private partnership contracts where concessionaires carry long-term maintenance obligations.

Environmental Concerns over Chemical Stabilizers

Groundwater contamination risks tied to chloride-based additives spur heightened environmental impact assessments. European regulators demand cradle-to-gate carbon disclosures for cementitious products, and similar rules are pending in Canada. Academic work at Aalto University reports biochar binders outperforming cement in both emissions and sorption properties, pressuring specifiers to downgrade high-alkali options. Liability fears extend to brownfield redevelopment, where remediation covenants shift long-term compliance costs to developers. These factors collectively slow approvals for chemical blends, although transitional demand persists where no technical substitute yet meets high-traffic load criteria.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Urbanization and Industrial Land Development

- Stricter Pavement-Durability Regulations

- Low Awareness and Skill Gaps in Emerging Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical techniques accounted for 73.45% of the 2025 soil stabilization market, underscoring decades of field validation across highways, runways, and port platforms. The segment benefits from mature standards that streamline design approval and from global supply chains that guarantee bulk availability. Biological alternatives, while holding a smaller volume, are expanding at a 7.25% CAGR, the fastest among all methods, as enzyme-treated soils achieve required California Bearing Ratio thresholds within shorter curing windows. Mechanical approaches remain relevant for temporary works and ecologically sensitive zones where additives are restricted. Geopolymer and nano-enhanced formulations occupy a niche but attract interest in seismic regions seeking high flexural toughness.

Performance criteria are evolving beyond basic shear strength to incorporate life-cycle greenhouse-gas accounting, water-absorption indices, and leachate profiles. This re-ranking aligns commercial success with environmental scoring, resulting in competitive realignment. Chemical suppliers are blending supplementary cementitious materials like calcined clay to lower clinker content, while bio-technology firms secure patents around microbial-induced calcite precipitation. As procurement moves to performance-based specifications, the soil stabilization market encourages cross-disciplinary collaborations linking materials science with digital monitoring to validate field behavior.

The Soil Stabilization Market Report is Segmented by Method (Mechanical Stabilization, Chemical Stabilization, Biological Stabilization, and Other Methods), Application (Infrastructure, Industrial, Commercial, and Residential), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 53.85% of global revenue in 2025, buoyed by Belt and Road corridors, India's smart-cities schemes, and Southeast Asian port expansions. Regional CAGR of 5.78% through 2031 outpaces the global average as governments embed resilience metrics into tender documents. Monsoon-driven soil variability necessitates stabilization across embankments and cut-and-fill sections, positioning the technology as mission-critical. China's gradual curbs on coal power are tightening fly-ash supply, accelerating trials of magnesium-based binders with lower carbon intensity. National research institutes partner with start-ups to pilot biochar solutions, signaling future procurement shifts.

North America maintains robust volume on the back of highway resurfacing bills that earmark funds for subgrade improvement. State DOTs in the Midwest deploy real-time modulus sensors to fine-tune binder dosage, reducing material waste. Canadian provinces are conducting cold-climate trials of geopolymer blends that maintain elasticity under freeze-thaw cycles. Regulatory emphasis on embodied carbon triggers preference for cement-replacement ratios above 50%, edging the market toward blended and bio-based options.

Europe pushes the frontier on circularity by mandating the reuse of excavated spoil where geotechnically feasible. Urban rail extensions in Germany and France apply in-place stabilization to limit truck movements through city centers. Scandinavian agencies pioneer performance warranties that hold contractors accountable for post-construction settlement data, incentivizing quality additives. The region's policy landscape, coupled with high public awareness of sustainability, accelerates the adoption of enzyme and geopolymer systems.

South America and the Middle East and Africa are emerging hot spots as governments tackle logistics bottlenecks and tourism infrastructure. Brazil's transport ministry specifies stabilization for Amazon basin highways prone to flooding, while the Gulf Cooperation Council states experiment with nano-silica blends to offset high-salinity soils. These regions value cost-effective solutions that adapt to local materials, and suppliers that bundle design services with field training gain an early mover advantage.

- Adbri Limited

- AggreBind Inc.

- BASF

- Boral

- Borregaard AS

- Carmeuse

- Cemex S.A.B DE C.V.

- Dow

- FAYAT Group

- Global Road Technology International Holdings (HK) Limited

- Graymont

- Heidelberg Materials

- HOLCIM

- Midwest Industrial Supply, Inc.

- Sika AG

- SNF

- Soilworks, LLC

- Substrata, LLC

- Terra-Firma Stabilization & Reclamation

- Wirtgen Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Infrastructure and Road Construction Activities

- 4.2.2 Rising Demand for Cost-Effective Soil Treatment Solutions

- 4.2.3 Increasing Urbanization and Industrial Land Development

- 4.2.4 Stricter Pavement-Durability Regulations

- 4.2.5 Adoption of Biopolymer and Enzyme-Based Eco-Stabilizers

- 4.3 Market Restraints

- 4.3.1 Environmental Concerns over Chemical Stabilizers

- 4.3.2 Low Awareness and Skill Gaps in Emerging Economies

- 4.3.3 Supply-Chain Volatility for Fly-Ash and Other By-Products

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Method

- 5.1.1 Mechanical Stabilization

- 5.1.2 Chemical Stabilization

- 5.1.3 Biological Stabilization

- 5.1.4 Other Methods

- 5.2 By Application

- 5.2.1 Infrastructure (roads, railways, airports)

- 5.2.2 Industrial

- 5.2.3 Commercial

- 5.2.4 Residential

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 Australia

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adbri Limited

- 6.4.2 AggreBind Inc.

- 6.4.3 BASF

- 6.4.4 Boral

- 6.4.5 Borregaard AS

- 6.4.6 Carmeuse

- 6.4.7 Cemex S.A.B DE C.V.

- 6.4.8 Dow

- 6.4.9 FAYAT Group

- 6.4.10 Global Road Technology International Holdings (HK) Limited

- 6.4.11 Graymont

- 6.4.12 Heidelberg Materials

- 6.4.13 HOLCIM

- 6.4.14 Midwest Industrial Supply, Inc.

- 6.4.15 Sika AG

- 6.4.16 SNF

- 6.4.17 Soilworks, LLC

- 6.4.18 Substrata, LLC

- 6.4.19 Terra-Firma Stabilization & Reclamation

- 6.4.20 Wirtgen Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment