|

시장보고서

상품코드

1934886

아메리카의 센서 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Americas Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

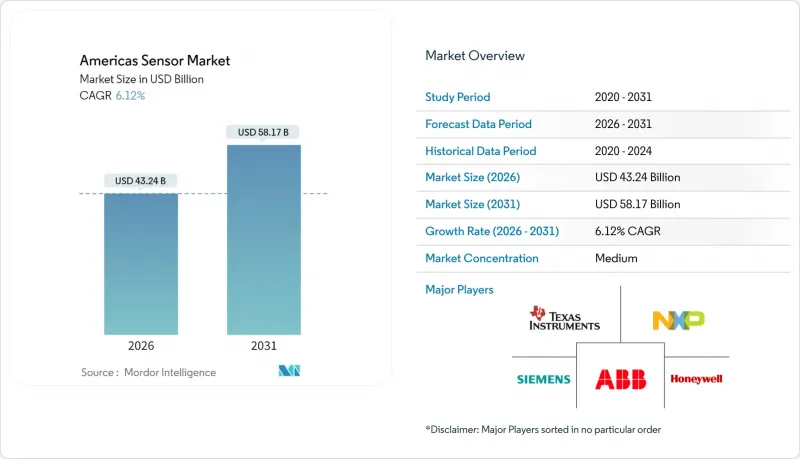

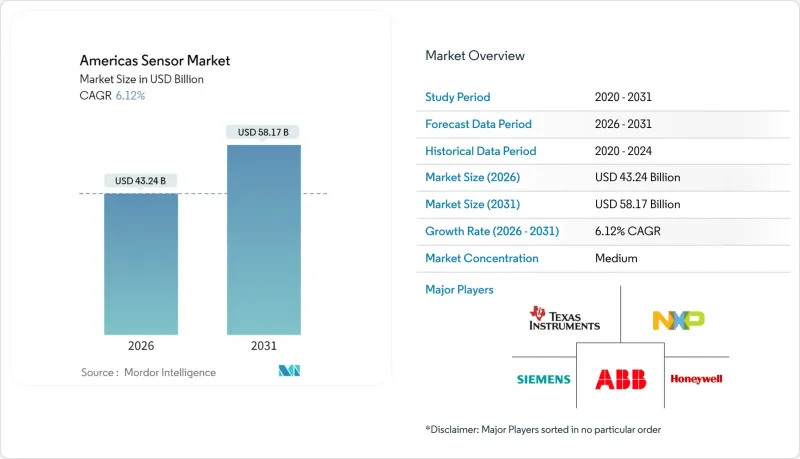

아메리카의 센서 시장은 2025년 407억 5,000만 달러에서 2026년에는 432억 4,000만 달러로 성장하며, 2026-2031년에 CAGR 6.12%로 추이하며, 2031년까지 581억 7,000만 달러에 달할 것으로 예측됩니다.

양자 기술을 활용한 내비게이션 시스템, 저전력 엣지 AI 처리, MEMS의 소형화가 맞물려 수요를 가장 강력하게 견인하고 있습니다. 한편, 스마트 인프라에 대한 막대한 공적 자금 투입이 대규모 도입을 가속화하고 있습니다. 자율주행차, 정밀농업, 재생에너지 모니터링에 대한 투자가 LiDAR, 환경, 진동 감지 기술을 둘러싼 경쟁을 심화시키고 있습니다. 지정학적 마찰이 계속되는 가운데, 질화갈륨 및 탄화규소 기판공급망 국내 복귀가 시급한 상황입니다. 전략적 M&A(특히 ST마이크로일렉트로닉스의 NXP 센서 부문 9억 5,000만 달러 인수 계획)는 안전하고 AI 지원 센서 융합 기능을 제공하는 수직 통합 플랫폼으로의 전환을 시사합니다.

북미 및 남미 센서 시장 동향 및 인사이트

소비자용 IoT 기기의 급속한 보급

스마트홈 보급률은 미국 및 캐나다 주요 도시에서 대중 시장 수준에 도달하여 코인 셀 배터리로 수년간 작동 가능한 저전력 무선 센서에 대한 지속적인 수요를 창출하고 있습니다. 미국 교통부의 SMART 보조금은 도시 전체의 교통 및 대기질 센서 도입을 촉진하고, 조달 예산 확보와 연결 프로토콜 표준화를 추진하고 있습니다. 이러한 디바이스에 내장된 엣지 AI 칩셋은 클라우드의 지연을 없애고 데이터 프라이버시를 보호합니다. 이는 엄격한 디지털 주권 규제를 시행하는 관할권에서 매우 중요합니다. 이로 인한 물량 증가는 MEMS 공급업체의 규모의 경제를 지원하고, 대중교통 네트워크를 업그레이드하는 라틴아메리카의 도시 지역으로 수요가 파급되고 있습니다.

북미 및 남미 제조업의 자동화 투자 증가

미국과 멕시코의 OEM 업체들은 예지보전 알고리즘에 정보를 제공하는 진동, 음향, 열 센서로 생산라인을 재구축하여 계획되지 않은 다운타임을 크게 줄이고 있습니다. 페트로브라스가 공급하는 브라질 국내 공장에서는 센서 기반의 에너지 대시보드를 도입하여 광열비 절감과 ESG 보고 의무를 달성하기 위해 노력하고 있습니다. 토탈에너지의 정유소에 무선 진동센서를 시범적으로 도입한 결과, 분기별로 예정에 없던 정전사고가 발생하지 않아 대규모 도입에 대한 투자대비효과(ROI)를 입증했습니다. 이러한 성과로 인해 디트로이트에서 몬테레이, 상파울루에 이르는 자동차, 금속, 식품 가공 산업 회랑에서 센서 도입이 정착되는 형태로 국경을 초월한 기술 이전이 가속화되고 있습니다.

안전에 중요한 센서에 대한 엄격한 규정 인증

자동차 기능 안전 규제에 따라 검증 주기가 최대 18개월까지 연장되어, 전담 컴플라이언스 팀이 없는 벤처기업은 불리한 입장에 놓여 있습니다. FDA의 임상용 웨어러블 기기에 대한 규제는 고비용의 생체 적합성 시험과 시판 후 조사 감사를 의무화하고 있으며, 북미와 남미의 센서 산업이 통합되는 가운데 기존 기업의 우위가 강화되고 있습니다.

부문 분석

환경 센서는 7.86%의 가장 빠른 CAGR을 기록했습니다. 이는 기업이 Scope 1 배출량 목표 달성을 서두르는 한편, 지자체 기관이 실시간 대기질 데이터 제공을 의무화하고 있기 때문입니다. 그러나 온도 측정 장치는 HVAC(냉난방 환기) 시스템 및 가전제품에 보급되면서 북미 및 남미 센서 시장 점유율 19.46%로 가장 큰 비중을 차지하고 있습니다. 압력 및 레벨 센서는 에너지 파이프라인과 스마트 상수도 네트워크에서 보급이 확대되고 있으며, 미국 서부의 가뭄 대책 프로젝트가 이러한 추세를 가속화하고 있습니다. 유량 및 근접 센서는 공장의 무인화 전환에 따라 로봇 공학 및 포장 라인에서 채택이 확대되고 있습니다. 하니웰이 국방 계약용으로 시험 도입한 양자 자력계와 관성측정장치는 초정밀 항법 응용 분야의 도래를 예고하고 있습니다.

농업 분야에서는 진동 센서와 화학 센서가 각각 토양의 다짐도와 영양분 수준을 진단하는 2차 보급 효과가 나타나고 있습니다. 웨어러블 기기에 내장된 소형 MEMS 습도 센서는 건강 모니터링 이용 사례를 촉진하고, 자기 센서는 재생에너지 터빈의 위치 추적을 지원합니다. 이러한 추세와 더불어 환경 솔루션이 조달 계획의 최우선 과제로 자리 잡으면서 북미 및 남미 센서 시장에서 점유율을 확대하고 있습니다.

LiDAR의 CAGR 8.02%는 자동차 OEM 업체들이 차세대 ADAS 플랫폼을 확정하고 있는 가운데 다른 모든 운전 등급을 능가하는 수치입니다. 동시에 정전식 디바이스는 소비자 및 산업 분야의 터치스크린, 근접, 충전 레벨 용도에 대한 지속적인 수요로 인해 출하량 기준 17.88%의 점유율을 차지하며 1위를 유지했습니다. 광학 및 이미징 센서는 엣지 AI 강화형 노이즈 억제 기술의 혜택을 받아 원격의료 및 대기질 분석 분야로의 침투가 심화되고 있습니다. 전기저항식 센서와 바이오센서는 정확도와 교정 드리프트에 매우 민감한 콜드체인 물류 및 연속 혈당 모니터링 분야에서 틈새 시장을 개발하고 있습니다.

레이더 모듈은 충돌 방지 시스템을 넘어 주변 보안 및 산업용 크레인 자동화에 적용되어 광학 시선(LOS)이 작동하지 않는 환경에서의 성능 격차를 해소하고 있습니다. LiDAR, 레이더, 이미징 유닛을 공동 패키징한 멀티모드 융합 스택은 자율주행 셔틀의 표준 아키텍처로 부상하며 자율주행 솔루션에 수반되는 미주 센서 시장 규모를 더욱 확대하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.06The Americas sensor market is expected to grow from USD 40.75 billion in 2025 to USD 43.24 billion in 2026 and is forecast to reach USD 58.17 billion by 2031 at 6.12% CAGR over 2026-2031.

Quantum-enabled navigation systems, low-power edge-AI processing, and MEMS miniaturization together create the strongest pull on demand, while heavy public-sector funding for smart infrastructure accelerates large-scale deployments. Investments in autonomous vehicles, precision agriculture, and renewable-energy monitoring are intensifying competition around LiDAR, environmental, and vibration sensing technologies. Supply-chain reshoring for gallium-nitride and silicon-carbide substrates gains urgency as geopolitical frictions persist. Strategic M&A - most notably STMicroelectronics' planned USD 950 million purchase of NXP's sensor unit - signals a shift toward vertically integrated platforms offering secure, AI-ready sensor fusion capabilities.

Americas Sensor Market Trends and Insights

Rapid Proliferation of Consumer IoT Devices

Smart-home penetration now reaches mass-market levels in major U.S. and Canadian cities, creating sustained demand for low-power wireless sensors that can operate for years on a coin cell. The U.S. Department of Transportation's SMART Grants are catalyzing citywide traffic and air-quality sensor rollouts, locking in procurement budgets and standardizing connectivity protocols. Edge-AI chipsets embedded inside these devices eliminate cloud latency and protect data privacy - critical for jurisdictions implementing strict digital sovereignty rules. The resulting volume lift underpins economies of scale for MEMS suppliers, with spillover demand in Latin American metros upgrading public-transport networks.

Rising Automation Investments in North and South American Manufacturing

OEMs across the United States and Mexico retool production lines with vibration, acoustic, and thermal sensors that feed predictive-maintenance algorithms, slashing unplanned downtime. Petrobras-supplied Brazilian plants deploy sensor-based energy dashboards to curb utility costs and satisfy ESG reporting mandates. TotalEnergies' refinery pilot with wireless vibration sensors demonstrated a full quarter without unscheduled shutdowns, validating ROI for widescale rollouts. These wins accelerate cross-border knowledge transfer, hardwiring sensor adoption into automotive, metals, and food-processing corridors from Detroit to Monterrey and Sao Paulo.

Stringent Regulatory Certification for Safety-Critical Sensors

Automotive functional-safety regulations extend validation cycles by up to 18 months, disfavoring venture-backed startups that lack dedicated compliance teams. FDA mandates for clinical-grade wearables impose costly biocompatibility and post-market surveillance audits, reinforcing incumbent advantage as the Americas sensor industry consolidates.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Smart-Infrastructure Retrofits

- Expansion of Electric and Autonomous Vehicles Requiring Multi-Sensor Suites

- Supply-Chain Concentration in Exotic Materials (GaN, SiC)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Environmental sensors post the fastest 7.86% CAGR as corporates race to meet Scope-1 emissions targets and municipal bodies mandate real-time air-quality data. Temperature devices nonetheless hold the largest 19.46% slice of the Americas sensor market share, thanks to ubiquitous HVAC and consumer-electronics integration. Pressure and level sensors scale within energy pipelines and smart water networks, a trend amplified by drought-mitigation projects across the Western United States. Flow and proximity sensing gain traction in robotics and packaging lines as factories pivot to lights-out operations. Quantum magnetometers and inertial units - piloted by Honeywell for defense contracts - hint at a coming wave of ultra-precise navigation applications.

Second-order adoption effects surface in agriculture, where vibration and chemical sensors diagnose soil compaction and nutrient levels, respectively. Miniaturized MEMS humidity sensors embedded in wearables push health-monitoring use cases, while magnetic sensors underpin renewable-energy turbine position tracking. Collectively, these dynamics keep environmental solutions front and center in procurement roadmaps and increase their proportion of the Americas sensor market.

LiDAR's 8.02% CAGR outpaces all other operational classes as automotive OEMs lock in next-generation ADAS platforms. Simultaneously, capacitive devices maintain an 17.88% leading share by unit shipments because of sustained touchscreen, proximity, and fill-level applications across consumer and industrial sectors. Optical and imaging sensors deepen penetration in telemedicine and air-quality analytics, benefitting from edge-AI-enhanced noise suppression. Electrical-resistance and biosensors carve niches in cold-chain logistics and continuous glucose monitoring-segments highly sensitive to accuracy and calibration drift.

Radar modules extend beyond collision-avoidance systems into perimeter security and industrial crane automation, filling performance gaps where optical LOS is compromised. Multi-mode fusion stacks that co-package LiDAR, radar, and imaging units emerge as the reference architecture for autonomous shuttles, further expanding the Americas sensor market size attached to autonomy solutions.

The Americas Sensor Market Report is Segmented by Parameters Measured (Temperature, Pressure, Level, Flow, and More), Mode of Operations (Optical, Electrical Resistance, Biosensor, Piezoresistive, and More), Sensor Technology (MEMS Sensors, and More), End-User Industry (Automotive, Consumer Electronics, Energy, and More), and Country (United States, Canada, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Texas Instruments Incorporated

- TE Connectivity Ltd.

- Omega Engineering Inc.

- Honeywell International Inc.

- Rockwell Automation Inc.

- Siemens AG

- ams-OSRAM AG

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Bosch Sensortec GmbH

- SICK AG

- ABB Ltd.

- OMRON Corporation

- STMicroelectronics N.V.

- Analog Devices, Inc.

- Microchip Technology Inc.

- Sensata Technologies Holding plc

- Murata Manufacturing Co., Ltd.

- Panasonic Holdings Corporation

- Qualcomm Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid proliferation of consumer IoT devices

- 4.2.2 Rising automation investments in North and South American manufacturing

- 4.2.3 Government incentives for smart-infrastructure retrofits

- 4.2.4 Expansion of electric and autonomous vehicles requiring multi-sensor suites

- 4.2.5 Emergence of low-power edge AI enabling on-sensor analytics

- 4.2.6 Increasing adoption of printable/flexible sensors in healthcare wearables

- 4.3 Market Restraints

- 4.3.1 Stringent regulatory certification for safety-critical sensors

- 4.3.2 High capital expenditure for MEMS fabrication lines

- 4.3.3 Supply-chain concentration in exotic materials (GaN, SiC)

- 4.3.4 Cyber-security liabilities tied to sensor data integrity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Parameter Measured

- 5.1.1 Temperature

- 5.1.2 Pressure

- 5.1.3 Level

- 5.1.4 Flow

- 5.1.5 Proximity

- 5.1.6 Environmental

- 5.1.7 Chemical

- 5.1.8 Inertial

- 5.1.9 Magnetic

- 5.1.10 Vibration

- 5.1.11 Other Parameters

- 5.2 By Mode of Operation

- 5.2.1 Optical

- 5.2.2 Electrical Resistance

- 5.2.3 Biosensor

- 5.2.4 Piezoresistive

- 5.2.5 Image

- 5.2.6 Capacitive

- 5.2.7 Piezoelectric

- 5.2.8 LiDAR

- 5.2.9 Radar

- 5.2.10 Other Modes

- 5.3 By Sensor Technology

- 5.3.1 MEMS Sensors

- 5.3.2 Non-MEMS Sensors

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Consumer Electronics

- 5.4.2.1 Smartphones

- 5.4.2.2 Tablets, Laptops and Computers

- 5.4.2.3 Wearable Devices

- 5.4.2.4 Smart Appliances

- 5.4.2.5 Other Consumer Electronics

- 5.4.3 Energy and Utilities

- 5.4.4 Industrial Automation

- 5.4.5 Medical and Wellness

- 5.4.6 Construction, Agriculture and Mining

- 5.4.7 Aerospace

- 5.4.8 Defense and Security

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Brazil

- 5.5.4 Mexico

- 5.5.5 Argentina

- 5.5.6 Chile

- 5.5.7 Rest of Americas

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Texas Instruments Incorporated

- 6.4.2 TE Connectivity Ltd.

- 6.4.3 Omega Engineering Inc.

- 6.4.4 Honeywell International Inc.

- 6.4.5 Rockwell Automation Inc.

- 6.4.6 Siemens AG

- 6.4.7 ams-OSRAM AG

- 6.4.8 NXP Semiconductors N.V.

- 6.4.9 Infineon Technologies AG

- 6.4.10 Bosch Sensortec GmbH

- 6.4.11 SICK AG

- 6.4.12 ABB Ltd.

- 6.4.13 OMRON Corporation

- 6.4.14 STMicroelectronics N.V.

- 6.4.15 Analog Devices, Inc.

- 6.4.16 Microchip Technology Inc.

- 6.4.17 Sensata Technologies Holding plc

- 6.4.18 Murata Manufacturing Co., Ltd.

- 6.4.19 Panasonic Holdings Corporation

- 6.4.20 Qualcomm Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment