|

시장보고서

상품코드

1934902

자동차 부품 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Parts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

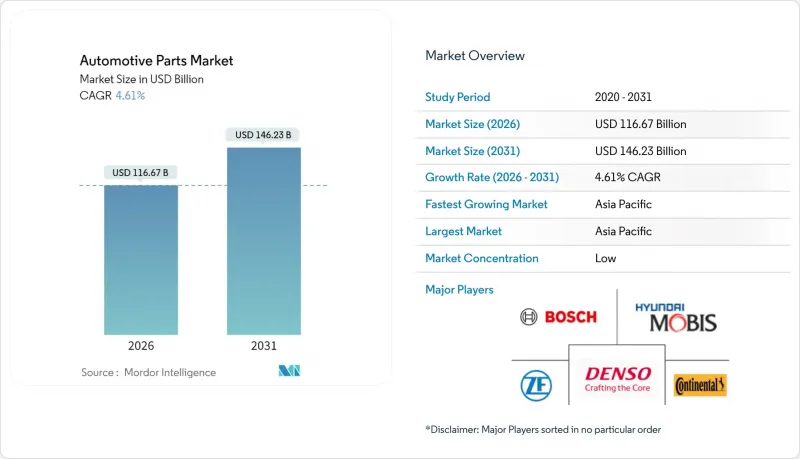

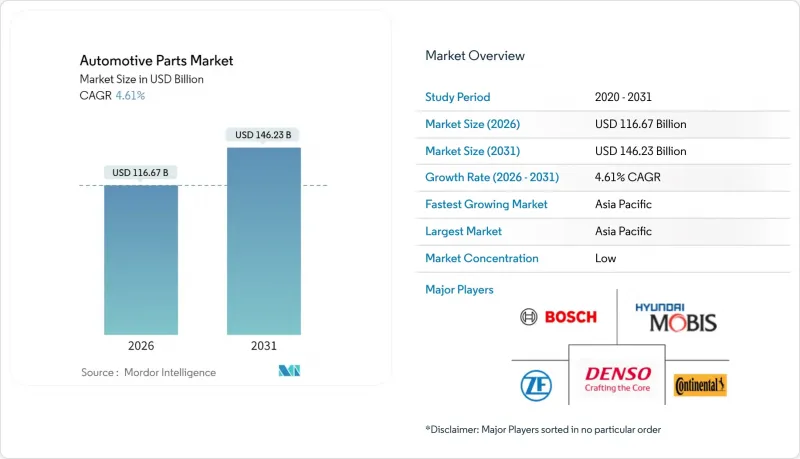

자동차 부품 시장은 2025년에 1,115억 3,000만 달러로 평가되며, 2026년 1,166억 7,000만 달러에서 2031년까지 1,462억 3,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 4.61%로 예상됩니다.

자동차 생산량 증가, 세계 차량 노후화에 따른 애프터마켓 수요의 안정화, 전동화 가속화가 결합되어 완만한 성장 경로를 지원하고 있습니다. 전기 파워트레인은 일부 내연기관 부품 수요를 감소시키는 한편, 수입원을 고부가가치 전기 및 전자 부품으로 전환하고 있습니다. 디지털 상거래는 예비 부품의 세계 유통 경로를 재구성하고 수천 개의 소규모 공급업체를 공식적인 밸류체인에 통합하고 있습니다. 아시아태평양은 구조적인 비용 우위, 대규모 제조거점, 그리고 현지 수요가 풍부하여 신차 조달에서 불균형적인 이익을 얻을 수 있는 지역입니다. 한편, 반도체 공급 부족, 원자재 가격 변동, 데이터 접근 규제 강화 등은 분기별 생산량과 수익성을 왜곡시킬 수 있는 주요 역풍 요인으로 남아있습니다.

세계 자동차 부품 시장 동향과 인사이트

세계 자동차 생산량 증가

2023년 세계 자동차 생산량은 9,050만 대에 달하고, 코로나 사태 이전 수준을 회복했습니다. 그러나 2024년에는 8,850만대로 둔화된 후 회복세를 보일 것으로 예측됩니다. 이러한 생산 확대는 특히 자동차 보유율이 지속적으로 증가하는 신흥 시장에서 순정 부품과 애프터마켓 부품에 대한 수요 증가와 직접적으로 연동되어 있습니다. 중국이 저가의 내연기관차 및 전기자동차의 순수출국으로 변모하면서 세계 공급망이 재편되고 부품 공급업체에 대한 새로운 수요 패턴이 형성되고 있습니다. '멀티 에너지' 생산 라인으로의 전환을 통해 제조업체는 시장의 불확실성에 신속하게 대응하고 다양한 파워트레인 기술에 걸쳐 안정적인 부품 수요를 유지할 수 있습니다.

소프트웨어 정의 차량이 요구하는 업그레이드 가능한 하드웨어

자동차 소프트웨어 시장은 향후 수년간 강력한 성장이 예상되며, 업계 임원들은 2035년까지 차량이 소프트웨어 정의 및 AI 구동이 될 것으로 예측했습니다. 이러한 변화를 위해서는 무선 업데이트(OTA)와 지속적인 기능 향상을 지원하는 근본적으로 다른 하드웨어 아키텍처가 필요합니다. 기존의 고정된 기능을 가진 자동차 부품과 달리, 소프트웨어 정의 차량은 차량 수명 주기 동안 진화하는 소프트웨어 요구 사항을 충족시키기 위해 모듈식 및 업그레이드 가능한 하드웨어 플랫폼이 필요합니다. 이러한 변화는 고성능 컴퓨팅 유닛, 첨단 센서, 원격 재프로그래밍이 가능한 유연한 전자제어장치(ECU)에 대한 수요를 증가시키고, 이러한 첨단 부품을 공급할 수 있는 공급업체에게 새로운 매출 기회를 창출하고 있습니다.

반도체 부족 지속

자동차용 반도체 시장은 회복 노력에도 불구하고 공급 제약이 지속되고 있으며, 업계는 공급 부족이 최고조에 달했던 시기에 최대 40%의 생산 감소를 경험했습니다. 자동차 산업이 소프트웨어 정의 차량으로 전환함에 따라 차량 당 반도체 탑재량은 2023년 800달러에서 2030년 1,350달러에 달할 것으로 예측됩니다. 특정 지역에 생산이 집중되어 있고, 자동차 등급 부품 조달에 긴 리드 타임이 필요하므로 공급망의 취약성은 여전히 남아있습니다. 이 부족은 특히 첨단운전자보조시스템(ADAS)와 인포테인먼트 부품에 영향을 미치고 있으며, OEM 업체들은 칩 할당에 우선순위를 두어야 하고, 생산 일정을 유지하기 위해 차량에서 기능을 삭제하는 경우도 있습니다.

부문 분석

전기 및 전자 부품은 2025년 29.56%로 가장 큰 시장 점유율을 차지할 것으로 예상되며, 2031년까지 연평균 9.12%의 가장 빠른 성장률을 나타낼 것으로 전망됩니다. 이 두 분야의 선도적 지위는 첨단 전자 시스템을 필요로 하는 커넥티드카, 자율주행차, 전기자동차로의 자동차 산업의 근본적인 전환을 반영합니다. 현대 차량에는 평균 80개의 센서와 100개의 전자 장치가 탑재되어 있으며, 2030년까지 전자 부품이 신차 가격의 50%를 차지할 것으로 예측됩니다. 이 부문에는 첨단운전자보조시스템(ADAS), 인포테인먼트 플랫폼, 배터리 관리 시스템, V2X(차량과 모든 사물과의 통신) 모듈 등 핵심 시스템이 포함됩니다.

구동계 및 파워트레인 부품은 전통적 내연기관 부품 수요가 감소하는 반면, 전기 파워트레인 부품 수요가 급증하는 복잡한 변화의 시기에 직면해 있습니다. 내/외장 부문은 프리미엄화 추세와 사용자 경험에 대한 관심이 높아지면서 특히 소프트웨어 정의 차량에서 캐빈 기술이 주요 차별화 요소로 작용하고 있습니다. 차체 및 섀시 부품은 신소재 및 경량화 요구에 대응하기 위해 계속 진화하고 있습니다. 반면, 휠 및 타이어 부문은 상대적으로 안정적이며, 노후화된 차량군의 교체 수요와 전 세계 차량 대수 증가가 성장을 촉진하고 있습니다.

내연기관 차량은 2025년 기준 75.88%로 가장 큰 시장 점유율을 유지하고 있으며, 이는 기존 차량의 보급과 많은 세계 시장에서의 지속적인 생산량을 반영하고 있습니다. 그러나 규제 요건, 배터리 기술 향상, 충전 인프라 확충 등을 배경으로 배터리 전기자동차(BEV)가 연평균 34.1%의 놀라운 성장률을 기록하며 가장 빠르게 성장하는 부문으로 부상했습니다. 세계 전기자동차 생산량은 2024년 1,730만 대에 달할 것이며, 중국은 1,240만 대를 생산하여 세계 생산량의 70% 이상을 차지할 것입니다.

하이브리드 및 플러그인 하이브리드차량은 전기 파워트레인과 내연기관 부품을 모두 필요로 하는 과도기적 기술로서 공급업체에게 복잡성을 유발하고 수요 패턴을 다양화시키는 역할을 하고 있습니다. 연료전지 전기자동차는 여전히 틈새 시장이지만, 수소의 에너지 밀도 우위가 더욱 두드러지는 상용차 응용 분야에서 유망한 분야입니다. 추진 시스템의 구성은 지역에 따라 크게 다르며, 중국과 유럽이 전동화를 주도하고 있습니다. 한편, 북미와 신흥 시장에서는 내연기관차 점유율이 높게 유지되고 있으며, 공급업체는 다양한 파워트레인 기술에 대응할 수 있는 유연한 생산 능력을 유지해야 합니다.

지역별 분석

아시아태평양은 2025년 45.31% 시장 점유율로 선두를 유지하며, 중국의 자동차 제조 우위 및 확대되는 국내 시장에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 6.19%로 지역 성장을 주도할 것으로 예측됩니다. 중국은 2024년 1,240만 대의 전기자동차를 생산하여 전 세계 전기자동차 생산량의 70% 이상을 차지함과 동시에 순수 전기자동차 수출국으로 변모하고 있습니다. 생산국이자 수출국이라는 이중적 역할은 내수 및 수출용 자동차 부품에 대한 큰 수요를 창출하고 있습니다. 인도 자동차 애프터마켓은 차량 보유대수 증가와 애프터마켓 서비스 수요 증가에 힘입어 2028년까지 140억 달러 규모에 달할 것으로 예측됩니다. 일본은 하이브리드 파워트레인, 정밀 제조 기술 등 첨단 부품 분야의 기술적 전문성을 지속적으로 활용하고 있습니다. 한편, 한국은 전기자동차 기술과 자동차 용도용 반도체 솔루션에 집중하고 있습니다.

북미와 유럽은 자동차 생태계가 확립된 성숙한 시장이지만, 산업 변화에 적응하는 데 있으며, 고유한 문제에 직면해 있습니다. 640억 유로 규모의 유럽 자동차 애프터마켓은 경제 변동, 규제 변화, 그리고 기존 유지보수 서비스가 필요 없는 전기자동차로의 전환에 따른 압력에 직면해 있습니다. 이 지역의 독립형 애프터마켓은 차량의 고령화와 예산 중심의 소비자들로 인해 60% 시장 점유율을 차지하고 있지만, 전기자동차 보급의 영향으로 2026년 이후 성장세가 둔화될 것으로 예측됩니다. 북미는 니어쇼어링 동향과 인플레이션 억제법에 의한 국내 전기자동차 생산 지원의 혜택을 누리고 있지만, 무역정책과 중국 자동차 업체들의 경쟁으로 인한 시장 혼란의 가능성에 직면해 있습니다.

남미, 중동 및 아프리카의 신흥 시장은 현재 시장 점유율은 작지만, 상당한 성장 잠재력을 가지고 있습니다. 멕시코의 자동차 부품 부문은 2024년 25억 달러 이상의 외국인 직접투자를 유치하여 미국의 전기자동차 생산 확대와 전기 부품 수요 증가로 인해 전년 대비 23.5% 증가율을 기록했습니다. 중동 및 북아프리카에서는 2024년 1분기에 11개의 신규 자동차 프로젝트가 발표되었으며, 총 투자액은 29억 달러가 넘었습니다. 사우디의 13억 달러 규모의 전기자동차 제조 단지가 주도적인 역할을 하고 있습니다. 이들 지역에서는 정부 주도의 자동차 산업 육성책과 수입 의존도를 낮추기 위한 정책이 추진되고 있으며, 국내외 부품 공급업체들에게 비즈니스 기회가 창출되고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

The automotive parts market was valued at USD 111.53 billion in 2025 and estimated to grow from USD 116.67 billion in 2026 to reach USD 146.23 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031).

Higher vehicle production volumes, steady aftermarket demand from an aging global fleet, and accelerating electrification together sustain this moderate growth path. Electrified powertrains shift revenue pools toward high-value electrical and electronic content, even as they reduce demand for some internal-combustion components. Digital commerce is redrawing global distribution routes for spare parts, bringing thousands of smaller suppliers into the formal supply chain. Asia-Pacific holds structural cost advantages, extensive manufacturing scale, and deep local demand, allowing the region to capture disproportionate gains in new-model sourcing. Meanwhile, semiconductor constraints, volatile raw-material input costs, and stricter data-access rules remain primary headwinds that can distort quarterly output and profitability.

Global Automotive Parts Market Trends and Insights

Rise in Global Vehicle Production

Global automotive production reached 90.5 million units in 2023, returning to pre-COVID levels, though production is expected to moderate to 88.5 million units in 2024 before recovering. This production expansion directly correlates with increased demand for both original equipment and aftermarket parts, particularly in emerging markets where vehicle ownership rates continue to climb. China's transformation into a net vehicle exporter, primarily of low-cost internal combustion engine and electric vehicles, reshapes global supply chains and creates new demand patterns for component suppliers. The shift toward "multi-energy" production lines allows manufacturers to adapt quickly to market uncertainties while maintaining consistent parts demand across different powertrain technologies.

Software-Defined Vehicles Requiring Upgradeable Hardware

The automotive software market is projected to demonstrate strong growth over the next few years, with industry executives believing vehicles will be software-defined and AI-powered by 2035. This transformation requires fundamentally different hardware architectures supporting over-the-air updates and continuous feature enhancements. Unlike traditional automotive components with fixed functionality, software-defined vehicles demand modular, upgradeable hardware platforms to accommodate evolving software requirements throughout the vehicle's lifecycle. This shift drives demand for high-performance computing units, advanced sensors, and flexible electronic control units that can be reprogrammed remotely, creating new revenue opportunities for suppliers capable of delivering these sophisticated components.

Persistent Semiconductor Shortages

The automotive semiconductor market faces continued supply constraints despite recovery efforts, with the industry experiencing production reductions of up to 40% during peak shortage periods. The automotive sector's transition to software-defined vehicles is increasing semiconductor content per vehicle from USD 800 in 2023 to an expected USD 1,350 by 2030. Supply chain vulnerabilities persist due to concentrated production in specific geographic regions and the long lead times required for automotive-grade components. The shortage particularly impacts advanced driver assistance systems and infotainment components, forcing OEMs to prioritize chip allocation and sometimes remove features from vehicles to maintain production schedules.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of E-commerce Parts Platforms

- "Right-to-Repair" Legislation Widening Independent Service Share

- EV Shift Eroding Demand for ICE-Specific Parts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical and electronics components command the largest market share at 29.56% in 2025 while achieving the fastest growth rate of 9.12% CAGR through 2031. This dual leadership reflects the automotive industry's fundamental shift to ward connected, autonomous, and electrified vehicles that require sophisticated electronic systems. Modern vehicles average 80 sensors and 100 electronic units, with electronic components expected to comprise 50% of a new car's cost by 2030. The segment encompasses critical systems including advanced driver assistance systems (ADAS), infotainment platforms, battery management systems, and vehicle-to-everything communication modules.

Driveline and powertrain components face a complex transition as traditional internal combustion engine parts experience declining demand while electric powertrain components surge. Interior and exterior segments benefit from premiumization trends and increased focus on user experience, particularly in software-defined vehicles where cabin technology becomes a key differentiator. Body and chassis components are evolving to accommodate new materials and lightweighting requirements. At the same time, wheel and tire segments remain relatively stable, with growth driven by replacement demand from aging vehicle fleets and expanding global vehicle populations.

Internal combustion engine vehicles maintain the largest market share at 75.88% in 2025, reflecting the installed base of existing vehicles and continued production in many global markets. However, battery-electric vehicles represent the fastest-growing segment with an extraordinary 34.1% CAGR, driven by regulatory mandates, improving battery technology, and expanding charging infrastructure. Global electric car production reached 17.3 million units in 2024, with China producing 12.4 million vehicles and dominating over 70% of global output.

Hybrid and plug-in hybrid electric vehicles serve as transitional technologies, requiring components for electric and combustion powertrains, creating complexity for suppliers and diversifying demand patterns. Fuel-cell electric vehicles remain a niche segment but show promise in commercial vehicle applications where hydrogen's energy density advantages become more pronounced. The propulsion mix varies significantly by region, with China and Europe leading electrification. At the same time, North America and emerging markets maintain higher ICE shares, requiring suppliers to maintain flexible production capabilities across multiple powertrain technologies.

The Automotive Parts Market Report is Segmented by Type (Driveline and Powertrain, Electrical and Electronics, and More), Propulsion (Internal Combustion Engine, Battery-Electric Vehicle, and More), Vehicle Type (Passenger Car and Commercial Vehicle), Sales Channel (OEM and Aftermarket), and Geography (North America, South America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific maintains its dominant position with 45.31% market share in 2025 and leads regional growth at 6.19% CAGR through 2031, driven by China's automotive manufacturing supremacy and expanding domestic markets. China produced 12.4 million electric vehicles in 2024, representing over 70% of global electric car output, while transforming into a net vehicle exporter. This dual role as producer and exporter creates substantial demand for automotive parts both domestically and for export vehicles. India's automotive aftermarket is projected to reach USD 14 billion by 2028, supported by increasing vehicle ownership and growing demand for aftermarket services. Japan continues to leverage its technological expertise in advanced components, particularly in hybrid powertrains and precision manufacturing. At the same time, South Korea focuses on electric vehicle technologies and semiconductor solutions for automotive applications.

North America and Europe represent mature markets with established automotive ecosystems but face distinct challenges in adapting to industry transformation. Europe's automotive aftermarket, valued at EUR 64 billion, confronts pressure from economic volatility, regulatory changes, and the transition to electric vehicles that require fewer traditional maintenance services. The region's independent aftermarket holds a 60% market share, driven by aging vehicles and budget-conscious consumers, but growth is expected to slow post-2026 due to EV adoption. North America benefits from nearshoring trends and the Inflation Reduction Act's support for domestic EV production, though the market faces potential disruption from trade policies and Chinese automotive competition.

Emerging markets in South America, the Middle East, and Africa demonstrate significant growth potential despite smaller current market shares. Mexico's auto parts sector attracted over USD 2.5 billion in foreign direct investment in 2024, representing a 23.5% increase driven by electric vehicle production growth in the U.S. and rising demand for electric components. The Middle East and North Africa region saw 11 new automotive projects with investments exceeding USD 2.9 billion in Q1 2024, led by Saudi Arabia's USD 1.3 billion electric vehicle manufacturing complex. These regions benefit from government initiatives to develop local automotive capabilities and reduce dependence on imports, creating opportunities for domestic and international parts suppliers.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Magna International Inc.

- Valeo SA

- Hyundai Mobis Co. Ltd

- Faurecia SE

- Lear Corporation

- Aisin Corporation

- Aptiv Plc

- BorgWarner Inc.

- Schaeffler AG

- Cummins Inc.

- CATL

- Tenneco Inc.

- Brembo SpA

- Mando Corporation

- ACDelco (GM Genuine Parts)

- Nidec Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in global vehicle production

- 4.2.2 Software-defined vehicles requiring upgradeable hardware

- 4.2.3 Aging vehicle fleet boosting aftermarket spend

- 4.2.4 Rapid growth of e-commerce parts platforms

- 4.2.5 Right-to-repair" legislation widening independent service share"

- 4.2.6 Light-weighting push for advanced material components

- 4.3 Market Restraints

- 4.3.1 Persistent semiconductor shortages

- 4.3.2 EV shift eroding demand for ICE-specific parts

- 4.3.3 Volatile raw material prices disrupting cost structures

- 4.3.4 Labor shortages in key manufacturing hubs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Supplier Information By Type

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Driveline and Powertrain

- 5.1.2 Interior and Exterior

- 5.1.3 Electrical and Electronics

- 5.1.4 Body and Chassis

- 5.1.5 Wheel and Tires

- 5.1.6 Other Types

- 5.2 By Propulsion

- 5.2.1 Internal Combustion Engine

- 5.2.2 Battery-Electric Vehicle

- 5.2.3 Hybrid Electric Vehicle

- 5.2.4 Plug-in Hybrid Electric Vehicle

- 5.2.5 Fuel-Cell Electric Vehicle

- 5.3 By Vehicle Type

- 5.3.1 Passenger Car

- 5.3.2 Commercial Vehicle

- 5.4 By Sales Channel

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of APAC

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Egypt

- 5.5.5.4 Turkey

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 ZF Friedrichshafen AG

- 6.4.5 Magna International Inc.

- 6.4.6 Valeo SA

- 6.4.7 Hyundai Mobis Co. Ltd

- 6.4.8 Faurecia SE

- 6.4.9 Lear Corporation

- 6.4.10 Aisin Corporation

- 6.4.11 Aptiv Plc

- 6.4.12 BorgWarner Inc.

- 6.4.13 Schaeffler AG

- 6.4.14 Cummins Inc.

- 6.4.15 CATL

- 6.4.16 Tenneco Inc.

- 6.4.17 Brembo SpA

- 6.4.18 Mando Corporation

- 6.4.19 ACDelco (GM Genuine Parts)

- 6.4.20 Nidec Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment