|

시장보고서

상품코드

1934905

데이터센터용 와이어 및 케이블 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Data Center Wire And Cable - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

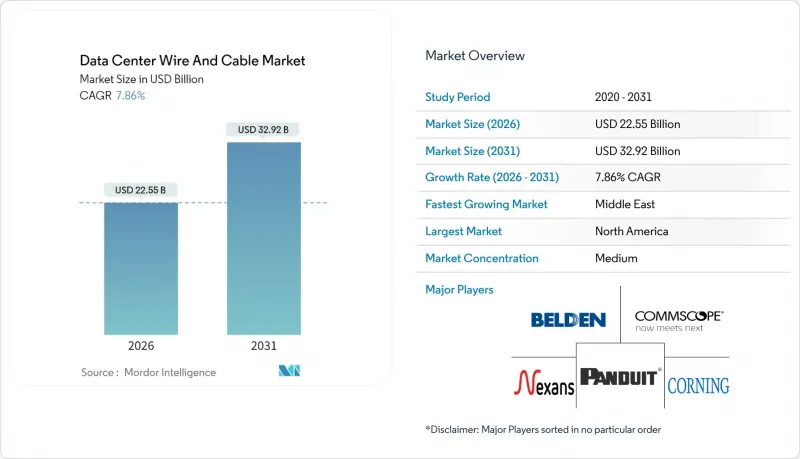

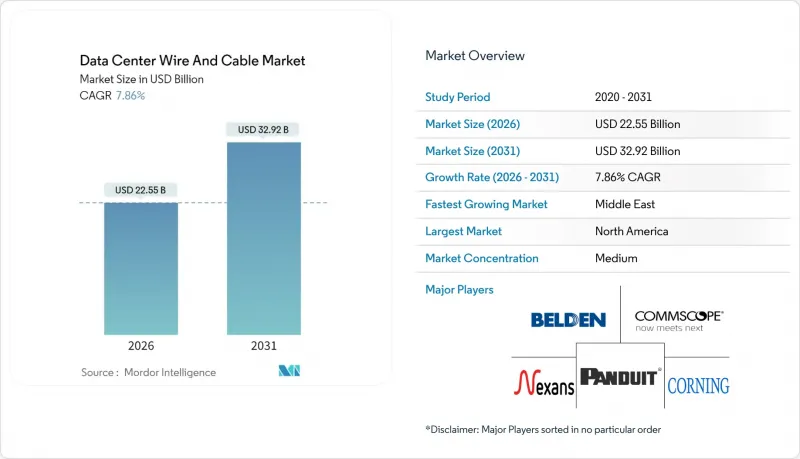

데이터센터용 와이어·케이블 시장은 2025년 209억 1,000만 달러에서 2026년에는 225억 5,000만 달러로 성장하며, 2026-2031년에 CAGR 7.86%로 추이하며, 2031년까지 329억 2,000만 달러에 달할 것으로 예측됩니다.

하이퍼스케일 시설의 지속적인 구축, 400G 및 800G 광 인터커넥트로의 빠른 전환, AI 및 고성능 컴퓨팅(HPC) 워크로드 수요 급증 등이 성장의 핵심 요인으로 작용하고 있습니다. 신규 건설 시설에서는 기존 CPU 중심 홀에 비해 최대 5배의 밀도를 가진 구조화된 배선 실적가 지정되고 있으며, 랙내 및 랙 간 링크에서 광섬유의 소비량이 구리선을 능가하고 있습니다. 5G 및 지연에 민감한 용도에 의해 가속화되고 있는 엣지 및 마이크로 데이터센터 구축은 환경 및 내열성 케이블 설계에 대한 새로운 이용 사례를 창출하고 있습니다. 'Build America by America Act'와 같은 정책적 인센티브가 국내 광섬유 투자를 촉진하는 한편, 유럽의 지속가능성 규제는 저손실 및 재활용이 가능한 소재의 구매를 유도하고 있습니다. 원자재 가격의 변동성은 계속 주목할 만한 항목으로, 구리는 2024년 한때 파운드당 5.20달러에 도달하여 케이블 비용을 최대 35%까지 끌어올렸습니다.

세계 데이터센터용 전선 및 케이블 시장 동향과 인사이트

전 세계 데이터센터의 견고한 확장

하이퍼스케일 클라우드 사업자들은 2025년 미국, 인도, 인도네시아에 멀티 기가급 캠퍼스를 잇따라 발표하며 각 시설에서 수백만 개의 광섬유 종단 처리를 필요로 하고 있습니다. 랙 평균 전력 밀도는 2022년 15kW에서 신설 AI홀의 경우 40kW로 상승하고, 랙당 수평 배선 거리가 두 배로 늘어났습니다. 이를 통해 시산업체는 케이블 트레이 용량을 늘리고 사전 종단 처리된 트렁크 번들을 채택하여 설치 일정을 단축할 수 있습니다. 싱가포르와 말레이시아의 지방 정부는 신규 데이터센터 허가에 제한을 두었지만, 조호르바루와 피닉스와 같은 지방 도시에서의 신규 프로젝트가 감소분을 상쇄하고 있습니다. 멀티모드 어셈블리의 빠른 납기를 보장할 수 있는 공급업체는 하이퍼스케일러와 다년간공급 계약을 체결하고 있습니다.

초저지연 링크가 필요한 AI/HPC 워크로드가 급증

수만 개의 GPU를 기반으로 하는 트레이닝 클러스터는 CPU 랙에 비해 서버당 4-5배의 파이버 점퍼가 필요하며, 부품표의 비중이 고밀도 MPO-to-MPO 트렁크로 이동하고 있습니다. 대규모 AI 패브릭에서 이더넷이 InfiniBand를 능가하고 있으며, 리프 앤 스파인 모델에 적합한 400G 및 800G 단거리 광모듈이 광범위하게 채택되고 있습니다. 코닝의 Contour Flow 케이블은 기존 144개 섬유 묶음과 동일한 외경에 288개의 섬유를 수용할 수 있으며, 배선 경로의 혼잡을 절반으로 줄일 수 있습니다. GPU 노드 간 5마이크로초의 낮은 지연 시간으로 인해 작업자는 연결 지점을 최소화해야 하므로 공장 종단 처리 솔루션이 선호되고 정밀 연마 MT 베이스 커넥터에 대한 수요가 증가하고 있습니다.

고밀도 번들의 열 관리 과제

케이블 사다리 내부의 기류 제한으로 인해 흡기 온도가 상승하고, 1℃ 상승할 때마다 DWDM 링크 마진이 0.08dB 감소합니다. 액체 냉각 매니폴드가 케이블 트레이 공간을 차지하므로 설계자는 더 가파른 곡률 반경으로 번들을 다시 배선해야 하며, 이는 마이크로 벤드 손실의 위험을 초래할 수 있습니다. 벤더는 85℃ 대응 젤 프리 케이블로 대응하고, 원형 디자인보다 단면을 30% 줄인 플랫팩형 트렁크 포맷을 도입하고 있습니다. 사업자는 55℃ 통로 내에서 포트 접근을 용이하게 하는 내열성 풀탭을 시험적으로 도입하고 있지만, 빈번한 재종단 처리에 따른 높은 운영비용은 여전히 예산으로 책정되어 있습니다.

부문 분석

CAGR은 CAGR을 의미하며, 광섬유는 2025년 데이터센터용 전선 및 케이블 시장의 59.30%를 차지하고 2031년까지 연평균 복합 성장률(CAGR) 8.12%로 확대되어 거의 모든 지표에서 동선을 능가할 것으로 예측됩니다. 광섬유 케이블의 데이터센터 시장 규모는 2031년까지 198억 달러에 달할 것으로 예상되며, 400G, 800G, 그리고 향후 도입 예정인 1.6T로의 업그레이드에 필수적임을 보여줍니다. 구리 데이터 케이블은 10G 이하 및 저지연 바이패스 영역에서 여전히 유용하지만, 증가하는 열 부하와 전자기 간섭(EMI) 우려로 인해 전송 거리에 제한이 있습니다. 전력 케이블은 부피는 작지만 랙 전력이 90kW를 초과하고 시설이 415V 배전을 채택함에 따라 미션 크리티컬한 존재로 남아있습니다.

기술 혁신은 고밀도화에 초점을 맞추었습니다. 코닝의 SMF-28 컨투어는 기존 144 섬유 수용 케이스에 288 섬유를 수용할 수 있으며, 설계자에게 40%의 굽힘 반경 완화를 제공합니다. 구리 피복 알루미늄 대체품은 금속 가격 변동을 상쇄하기 위해 단거리 및 저전류 용량 용도로 등장하고 있습니다. 각 업체들은 유럽 환경 규제 대응을 위해 바이오 기반 재킷을 채용한 광섬유 어셈블리도 출시. 케이블-커넥터-트랜시버를 통합 채널로 공동 설계하는 경쟁은 공급업체 간의 차별화와 장기적인 마스터 서비스 계약 체결을 촉진하고 있습니다.

2025년 매출에서 하이퍼스케일 시설이 48.60%를 차지하여 데이터센터용 전선 및 케이블 시장에서 가장 큰 비중을 차지할 것으로 예측됩니다. 그러나 엣지 및 마이크로 노드가 8.78%의 연평균 복합 성장률(CAGR)로 성장을 주도할 것으로 예상되며, 2031년까지 데이터센터용 전선 및 케이블 시장 규모는 65억 5,000만 달러에 달할 것으로 전망됩니다. 오하이오, 버지니아, 우타르 프라데시의 기가급 캠퍼스에서는 GPU 포드를 상호 연결하기 위해 수천 킬로미터의 단일 모드 광섬유가 필요합니다. 반면, 조립식 마이크로 EDC(µEDC)는 배선 거리가 짧지만, 견고한 피복과 IP 표준 대응 커넥터가 필요하며, 가격이 비쌉니다.

프랑크푸르트와 애쉬번의 코로케이션 사업자들은 AI 테넌트 확보를 위해 구조화된 배선을 계속 업데이트하고 있지만, 많은 레거시 기업 시설들은 고가의 리노베이션보다 클라우드 오프로드를 선택하고 있습니다. 공급업체는 SKU를 최적화합니다. 하이퍼스케일 시설내 배선에는 내굴곡성 멀티모드 광섬유를, 보도 캐비닛에는 기갑 루즈 튜브를 채택하고 있습니다. 5G 스탠드얼론 코어의 보급과 함께 마이크로 사이트에서는 무선 헤드용 PoE(Power over Ethernet)도 도입되어 구리선 수요가 소폭 증가하고 있습니다. 중앙집중형과 분산형 투자의 균형이 업체 간 R&D 자금 배분을 좌우할 것입니다.

지역별 분석

2025년 북미는 데이터센터용 전선 및 케이블 시장을 주도했습니다. 340억 달러가 넘는 하이퍼스케일 투자에 더해, 공공 자금이 투입되는 브로드밴드 사업에 국산 광섬유의 사용을 의무화하는 연방정부의 정책도 한몫을 하고 있습니다. 코닝, 컴스코프, AFL은 총 5억 달러 이상의 신규 생산능력을 약속하며 수입 의존도를 낮추고 프로젝트 리드타임을 단축할 수 있게 되었습니다. 캐나다는 추운 기후와 재생에너지의 이점을 활용하여 퀘벡 주에 코로케이션 시설 건설을 유치하고 있습니다. 멕시코에서는 니어쇼어링의 물결로 인해 케레타로주의 Tier III 시설이 활성화되고 있으며, 현재 미국 표준에 정통한 이중언어 설치 인력이 필요하게 되었습니다.

아시아태평양은 2031년까지 가장 높은 지역별 CAGR을 달성할 것입니다. 인도의 데이터 주권 규제와 중국의 클라우드 서비스 확대가 견인차 역할을 하고 있습니다. 싱가포르의 건설 모라토리엄으로 인해 사업자들은 조호르 주와 바탐 섬으로 진출하여 국경을 넘나드는 광섬유 회랑이 활성화되었습니다. 호주에서는 서부 해안에 새로운 해저 케이블 상륙이 기록되어 퍼스와 무스카트, 몸바사를 연결했습니다. 한편, 일본과 한국은 1.6T 이더넷의 연구개발을 주도하여 시제품 간선 케이블의 국내 수요를 가속화하고 있습니다.

유럽은 안정성을 유지하는 것에 대한 규제가 엄격하며, EN 50575 및 CPR 규정에 따라 건물에 영구적으로 설치되는 케이블은 CE 마킹과 화재 등급 인증이 의무화되어 있습니다. 독일, 네덜란드, 북유럽 국가들은 재생에너지 공급력과 안정적인 송전망으로 경쟁하고 있으며, 지속가능성을 중시하는 케이블 사양을 장려하고 있습니다. 중동 및 아프리카은 규모는 작지만 UAE, 사우디아라비아, 케냐가 국제적인 클라우드 사업자를 유치하면서 두 자릿수 성장을 기록하고 있습니다. 정치적 리스크 프리미엄이 남아있지만, 아프리카 대륙을 둘러싼 해저 프로젝트가 초장거리 광섬유의 장기적인 수요를 보장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 전 세계에서 데이터센터 건설 활동의 분석

제6장 시장 규모와 성장 예측

제7장 경쟁 구도

제8장 시장 기회와 향후 전망

KSA 26.03.06The Data Center Wire and Cable market is expected to grow from USD 20.91 billion in 2025 to USD 22.55 billion in 2026 and is forecast to reach USD 32.92 billion by 2031 at 7.86% CAGR over 2026-2031.

Continued hyperscale construction, rapid migration to 400 G and 800 G optical interconnects, and surging demand from AI and high-performance computing (HPC) workloads are the core growth engines. New-build facilities now specify structured cabling footprints up to five times denser than legacy CPU-centric halls, pushing optical-fiber consumption ahead of copper for intra-rack and inter-rack links. Edge and micro-data-center roll-outs, accelerated by 5G and latency-sensitive applications, are creating fresh use cases for ruggedized, temperature-hardened cable designs. Policy incentives such as the Build America Buy America Act are spurring domestic fiber investments, while sustainability mandates in Europe are steering purchasing toward low-loss and recyclable formulations. Commodity volatility remains a watch item; copper briefly touched USD 5.20 per pound in 2024 and lifted cable bills by as much as 35%.

Global Data Center Wire And Cable Market Trends and Insights

Robust Data-Center Expansion Worldwide

Hyperscale cloud operators announced multi-gigawatt campuses across the United States, India, and Indonesia in 2025, each demanding several million fiber terminations. Average rack densities rose from 15 kW in 2022 to 40 kW in new AI halls, doubling the horizontal cable runs per rack. Contractors, therefore, specify higher cable-tray capacities and pre-terminated trunk bundles to compress installation schedules. Regional governments in Singapore and Malaysia capped new data-center permits, yet green-field projects in secondary metros such as Johor Bahru and Phoenix offset the slowdown. Suppliers able to guarantee short lead times on multimodal assemblies are winning multi-year supply agreements with hyperscalers.

Surge in AI/HPC Workloads Requiring Ultra-Low-Latency Links

Training clusters built around tens of thousands of GPUs need four to five times more fiber jumpers per server than CPU racks, shifting bill-of-materials weighting toward high-density MPO-to-MPO trunks. Ethernet is overtaking InfiniBand for large-scale AI fabrics, prompting broad adoption of 400 G and 800 G short-reach optics that still fit the leaf-and-spine model. Corning's Contour Flow cable now ships with 288 fibers in the same outer diameter as earlier 144-fiber bundles, halving pathway congestion. Latency budgets of 5 µs between GPU nodes force operators to minimize splice points, favoring factory-terminated solutions and driving demand for precision-polished MT-based connectors.

Thermal-Management Challenges in High-Density Bundles

Airflow constriction inside cable ladders raises inlet temperatures, and each 1 °C rise cuts DWDM link margin by 0.08 dB. Liquid-cooling manifolds occupy space once used for cable trays, forcing designers to reroute bundles in tighter radii that risk micro-bending losses. Vendors counter with gel-free cables rated to 85 °C and introduce flat-pack trunk formats that occupy 30% less cross-section than round designs. Operators trial heat-resistant pull-tabs to ease port access inside 55 °C aisles but still budget higher OpEx for frequent re-termination.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of 400 G/800 G Optical Interconnects

- Proliferation of Edge and Micro Data Centers

- Retrofitting Legacy Facilities with High-Speed Cabling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Optical fiber captured 59.30% of the Data Center Wire and Cable market in 2025 and is forecast to grow at an 8.12% CAGR to 2031, outpacing copper on nearly every metric. The Data Center Wire and Cable market size for fiber cables is projected to reach USD 19.8 billion by 2031, reflecting its indispensability for 400 G, 800 G, and forthcoming 1.6 T upgrades. Copper data cables retain relevance below 10 G and in low-latency bypass zones, yet rising thermal loads and EMI concerns cap their lane length. Power cables, while volumetrically smaller, remain mission-critical as rack power climbs past 90 kW and facilities adopt 415 V distribution.

Innovation centers on density: Corning's SMF-28 Contour enables 288 fibers within earlier 144-fiber envelopes, giving designers 40% bend-radius relief. Copper-clad aluminum substitutes appear in short, low-ampacity applications to offset metal volatility. Vendors also release fiber-optic assemblies with bio-based jackets to meet European environmental regulations. The race to co-design cable, connector, and transceiver as a holistic channel differentiates suppliers and cements long-term master-service agreements.

Hyperscale facilities held 48.60% of 2025 revenue, equal to the largest share in the Data Center Wire and Cable market. Edge and micro nodes, however, lead growth at 8.78% CAGR, lifting the Data Center Wire and Cable market size for these deployments to USD 6.55 billion by 2031. Gigawatt-scale campuses in Ohio, Virginia, and Uttar Pradesh require thousands of kilometers of single-mode fiber to interconnect GPU pods. Conversely, prefabricated µEDCs consume shorter runs but demand ruggedized sheathing and IP-rated connectors that command premium pricing.

Colocation operators in Frankfurt and Ashburn keep refreshing structured cabling to court AI tenants, yet many legacy enterprise halls opt for cloud offload rather than expensive overhauls. Suppliers tailor SKUs: bend-insensitive multimode for hyperscale intra-build runs and armored loose-tube for sidewalk cabinets. As 5G standalone cores proliferate, micro sites also install power-over-ethernet for radio heads, subtly raising copper volumes. The balance between centralized and distributed spends will dictate the allocation of R&D funds across vendors.

The Data Center Wire and Cable Market is Segmented by Cable Type (Optical Fiber, Copper Data and More), Data Center Type (Enterprise, Colocation and More), Application (Structured Cabling, Power Distribution and More), Cable Construction(Shielded, Unshielded and More), Deployment Environment (Indoor White Space, Outdoor Plant and More), and Geography(North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the Data Center Wire and Cable market in 2025, driven by hyperscale investments exceeding USD 34 billion and reinforced by federal policies mandating domestic fiber for publicly funded broadband projects. Corning, CommScope, and AFL collectively pledged more than USD 500 million in new capacity, reducing import reliance and shortening project lead times. Canada benefits from colder climates and renewable energy, luring colocation builds in Quebec. Mexico's near-shoring wave fuels Tier III halls in Queretaro, which now require bilingual installation crews versed in U.S. standards.

Asia-Pacific delivers the highest regional CAGR through 2031, propelled by India's data-sovereignty rules and China's cloud service scale-up. Singapore's construction moratorium pushed operators to Johor and Batam, stimulating cross-border fiber corridors. Australia records new submarine landings on its western coast, linking Perth to Muscat and Mombasa. Meanwhile, Japan and South Korea spearhead 1.6 T Ethernet R&D, accelerating domestic demand for prototype trunk cables.

Europe remains steady but highly regulated; EN 50575 and CPR rules require CE marking and fire-class certification for any cable permanently installed in buildings. Germany, the Netherlands, and the Nordics compete on renewable energy availability and stable grids, fostering sustainability-driven cable specifications. Middle East and Africa, though smaller, post double-digit growth as UAE, Saudi Arabia, and Kenya entice international cloud incumbents. Subsea projects circling the African continent guarantee long-term pull for ultra-long-haul fiber, even as political risk premiums linger.

- Nexans S.A.

- Belden Inc.

- Panduit Corp.

- CommScope Holding Co. Inc.

- Corning Inc.

- TE Connectivity plc

- Yangtze Optical Fibre and Cable (YOFC)

- Legrand Group

- Southwire Company LLC

- Furukawa Electric Co. Ltd.

- Prysmian Group

- Sumitomo Electric Industries Ltd.

- LS Cable and System

- Superior Essex Inc.

- AFL Global

- Rosenberger Hochfrequenztechnik GmbH

- Hexatronic Group AB

- HUBER+SUHNER AG

- Fujikura Ltd.

- Datwyler IT Infra

- Ciena Corporation

- Tratos Cavi S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust data-center expansion worldwide

- 4.2.2 Surge in AI/HPC workloads requiring ultra-low-latency links

- 4.2.3 Rapid adoption of 400G/800G optical inter-connects

- 4.2.4 Proliferation of edge and micro data centers

- 4.2.5 Sustainability mandates for low-loss recyclable cabling

- 4.2.6 Government incentives for domestic fiber and power-cable production

- 4.3 Market Restraints

- 4.3.1 Thermal-management challenges in high-density bundles

- 4.3.2 Retrofitting legacy facilities with high-speed cabling

- 4.3.3 Volatility in copper and aluminum commodity prices

- 4.3.4 Skilled-labor shortage for advanced fiber termination

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 ANALYSIS OF DATA CENTER CONSTRUCTION ACTIVITY WORLDWIDE

- 5.1 Upcoming Data Center Construction Hotspots (planned IT-load additions)

- 5.2 Growth of Hyperscale Data Centers

- 5.3 Regional DC Construction - Vendor Landscape

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Cable Type

- 6.1.1 Optical Fiber Cables

- 6.1.2 Copper Data Cables (Twisted Pair)

- 6.1.3 Power Cables

- 6.1.3.1 Voltage Type

- 6.1.3.1.1 High Voltage (HV)

- 6.1.3.1.2 Medium Voltage (MV)

- 6.1.3.1.3 Low Voltage (LV)

- 6.1.3.2 Material Type

- 6.1.3.2.1 Copper

- 6.1.3.2.2 Aluminum

- 6.1.3.3 Application

- 6.1.3.3.1 PDUs and UPS Systems

- 6.1.3.3.2 HVAC System

- 6.1.3.3.3 Networking and IT Equipment

- 6.1.3.3.4 Others

- 6.1.3.1 Voltage Type

- 6.1.4 Other Cables (Grounding, Sensor, Control)

- 6.2 By Data Center Type

- 6.2.1 Enterprise/ Edge / Micro

- 6.2.2 Colocation

- 6.2.3 Hyperscale

- 6.3 By Application

- 6.3.1 Structured Cabling

- 6.3.2 Power Distribution

- 6.3.3 HVAC and Building Systems

- 6.3.4 Monitoring and Control

- 6.3.5 High-Speed Interconnects (>100 G)

- 6.4 By Cable Construction

- 6.4.1 Shielded

- 6.4.2 Unshielded

- 6.4.3 Armored

- 6.4.4 Plenum-Rated

- 6.5 By Deployment Environment

- 6.5.1 Indoor (White Space)

- 6.5.2 Outdoor Plant

- 6.5.3 Sub-sea / Inter-facility

- 6.6 By Geography

- 6.6.1 North America

- 6.6.1.1 United States

- 6.6.1.2 Canada

- 6.6.1.3 Mexico

- 6.6.2 South America

- 6.6.2.1 Brazil

- 6.6.2.2 Argentina

- 6.6.2.3 Rest of South America

- 6.6.3 Europe

- 6.6.3.1 Germany

- 6.6.3.2 United Kingdom

- 6.6.3.3 France

- 6.6.3.4 Nordic Region

- 6.6.3.5 Russia

- 6.6.3.6 Rest of Europe

- 6.6.4 Asia-Pacific

- 6.6.4.1 China

- 6.6.4.2 India

- 6.6.4.3 Japan

- 6.6.4.4 South Korea

- 6.6.4.5 Southeast Asia

- 6.6.4.6 Rest of Asia-Pacific

- 6.6.5 Middle East

- 6.6.5.1 UAE

- 6.6.5.2 Saudi Arabia

- 6.6.5.3 Turkey

- 6.6.5.4 Rest of Middle East

- 6.6.6 Africa

- 6.6.6.1 South Africa

- 6.6.6.2 Nigeria

- 6.6.6.3 Rest of Africa

- 6.6.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Share Analysis

- 7.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.2.1 Nexans S.A.

- 7.2.2 Belden Inc.

- 7.2.3 Panduit Corp.

- 7.2.4 CommScope Holding Co. Inc.

- 7.2.5 Corning Inc.

- 7.2.6 TE Connectivity plc

- 7.2.7 Yangtze Optical Fibre and Cable (YOFC)

- 7.2.8 Legrand Group

- 7.2.9 Southwire Company LLC

- 7.2.10 Furukawa Electric Co. Ltd.

- 7.2.11 Prysmian Group

- 7.2.12 Sumitomo Electric Industries Ltd.

- 7.2.13 LS Cable and System

- 7.2.14 Superior Essex Inc.

- 7.2.15 AFL Global

- 7.2.16 Rosenberger Hochfrequenztechnik GmbH

- 7.2.17 Hexatronic Group AB

- 7.2.18 HUBER+SUHNER AG

- 7.2.19 Fujikura Ltd.

- 7.2.20 Datwyler IT Infra

- 7.2.21 Ciena Corporation

- 7.2.22 Tratos Cavi S.p.A.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment