|

시장보고서

상품코드

1937285

수의 의료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Veterinary Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

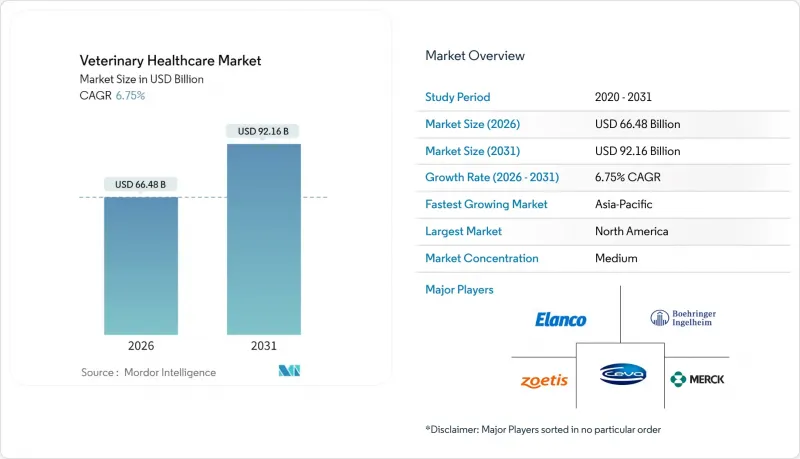

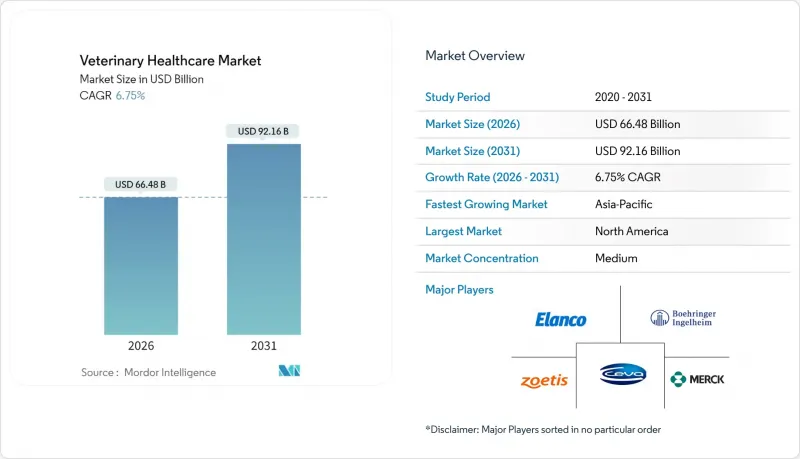

수의 의료 시장은 2025년 622억 8,000만 달러에서 2026년에는 664억 8,000만 달러에 이르고, 2026-2031년 CAGR 6.75%로 성장을 지속하여 2031년까지 921억 6,000만 달러에 달할 것으로 예측됩니다.

반려동물 관련 지출 증가, 신흥국의 견조한 축산 확대, 수의학 분야에서의 디지털 기술 도입이 수의 의료 시장의 꾸준한 성장을 뒷받침하고 있습니다. 보호자의 질병 조기발견 요구, 보험사의 위험감소 프로토콜 추진, 규제당국의 생물안전 대책 강화에 따라 예방의료 모델이 주류로 자리 잡고 있습니다. 진단기술의 혁신, 특히 분자 포인트 오브 케어 시스템은 결과 보고를 며칠에서 몇 분으로 단축하여 임상 워크플로우를 혁신적으로 변화시키고 있습니다. 한편, 치료 포트폴리오는 항균제 적정 사용 요구에 부합하는 백신, 면역조절제, 신규 구충제 등으로 진화하고 있습니다. 디지털 헬스 플랫폼은 환자 기록, 농장 센서, 유전자 데이터를 연결하여 임상의가 복잡한 치료 옵션을 탐색하는 동시에 실시간으로 수익을 창출할 수 있도록 돕습니다.

세계 수의 의료 시장 동향과 인사이트

단백질이 풍부한 동물성 제품에 대한 수요 증가

축산 사업자들은 2030년까지 개발도상국에서 40% 증가할 것으로 예상되는 단백질 소비량에 대응하기 위해 생산 규모를 확대하고 있습니다. 이러한 추세에 따라 농장에서는 엄격한 생물학적 안전 조치와 예방 프로토콜을 도입해야 합니다. 사육 밀도가 높아지면 감염 위험이 높아지기 때문에 수의사들은 종합적인 백신 접종과 지속적인 건강 모니터링을 실시하여 치명적인 발병을 방지하고 있습니다. 아시아의 양식업자들은 현재 진단 센서를 순환식 시스템에 직접 내장하여 실시간 데이터를 원격지의 수의사에게 제공하여 치료 계획을 즉각적으로 조정하고 있습니다. 사료 첨가제와 진단 피드백 루프를 결합한 정밀 영양 프로그램은 기존의 동물 위생과 생산의 경계를 모호하게 만들고 있습니다. 질병 관리 비용 증가는 결국 마리당 건강 관리 예산을 확대하여 수의학 시장의 지속적인 수요를 강화하고 있습니다.

반려동물의 인간화와 의료비 지출 증가

2024년 기준 미국 가구의 70%가 최소 1마리 이상의 반려동물을 키우고 있으며, 가구당 연간 평균 반려동물 진료비는 1,480달러로 2019년 대비 23% 증가했습니다. 반려동물을 가족의 일원으로 여기고 암 면역치료, 치과 임플란트, 행동치료 등 고가의 치료비도 부담하는 보호자들도 있습니다. 반려동물 보험의 보급률은 전 세계적으로 5% 미만으로, 보험사는 고가의 치료비 분산을 통해 잠재적 수요를 개척할 수 있는 위치에 있습니다. 백신, 진단, 영양상담을 포함한 건강관리 플랜에 대한 수요는 동물병원의 지속적인 수익원을 촉진합니다. 이러한 인식의 변화는 진단 순응도를 높이고, 일반 진료에 있어 Point-of-Care 플랫폼의 도입을 가속화하고 있습니다. 정서적 애착 증가는 가격에 민감하지 않은 계층을 확대하여 경기 침체기에도 수의학 시장을 지탱하고 있습니다.

엄격한 규제 준수 및 승인 프로세스

현재 동물용의약품의 평균 개발기간은 7년 이상 소요되고 있습니다. 이는 FDA가 2024년 도입한 환경영향기준으로 인해 신청 당 최대 2년의 추가 기간이 발생했기 때문입니다. 소규모 혁신 기업들은 장기간의 시험과 여러 지역에 걸친 신청 서류에 대한 자금 조달에 어려움을 겪고 있으며, 파이프라인의 다양성이 감소하고 있습니다. 수수료 체계와 승인 후 모니터링 요구가 높아지면서 기업들은 블록버스터 치료제를 우선시하고, 틈새 치료제는 보류하고 있습니다. 이로 인한 혁신의 병목현상은 차세대 치료법의 도입을 지연시킬 수 있지만, 계약 연구 기관과의 제휴 계약은 자본 부담 완화에 기여할 수 있습니다. 스폰서 간의 통합은 규제에 대한 전문성을 집중시키지만, 수의학 시장에서 가격 결정력을 강화할 수 있습니다.

부문 분석

2031년까지 연평균 성장률(CAGR) 7.12%로 가장 빠른 매출 성장을 보인 분야는 진단 분야이며, 2025년 수의학 시장에서 치료제의 매출 점유율은 62.45%를 차지할 것으로 예측됩니다. Point of Care 분석기는 혈액 검사, 생화학 검사, PCR 카트리지를 컴팩트한 케이스에 통합하여 1차 진료 클리닉에 적합합니다. 병원 내 검사는 환자 수용률을 높이고, 기존 외부 검사기관으로 흘러가던 수익을 확보합니다. 분자 패널 검사는 단일 검체에서 여러 병원체 프로파일을 검출할 수 있으며, 과거에는 인간 의료에 국한되었던 정밀의료 프로토콜을 지원합니다. 한편, 백신 제품군은 치료제의 탄탄한 기반을 뒷받침하고 가축의 건강을 보호하면서 항균제의 과도한 사용을 억제합니다. 기존 항균제는 제네릭 경쟁으로 인해 수익률이 압박을 받고 있어 주요 업체들은 생물학적 제제, 면역조절제, 표적형 구충제에 집중하고 있습니다. 특허 만료 후 바이오시밀러의 진입은 가격 경쟁을 촉진하는 한편, 비용 중심의 환경에서 접근성 확대를 가져와 결과적으로 대상 동물용 의약품 시장을 확대합니다.

치료 파이프라인은 항균제 적정 사용 가이드라인에 대응하고, 박테리오파지 칵테일, 프로바이오틱스 사료 첨가제 등의 대체 수단을 제공합니다. 지속성 주사제는 대규모 축산 시설에서 취급 스트레스와 노동력을 최소화합니다. 반려동물 분야에서는 벼룩-진드기-필라리아 예방 복합제제가 컴플라이언스 편의성 때문에 높은 가격대를 유지하고 있습니다. 미국 환경보호청(EPA)의 잔류 기준 개정으로 신속한 잔류 진단에 대한 수요가 증가하면서 치료와 진단의 판매 전략이 연동됩니다. 옴니채널 유통망을 보유한 기업은 전자상거래, 병원, 농기계 판매점에서의 제품 출시를 동기화하여 수의 의료 시장 규모의 성장 모멘텀을 극대화할 수 있습니다.

개와 고양이는 2025년 매출의 55.10%를 차지할 것으로 예상되며, 이는 헬스케어 시장에서 임의 지출을 뒷받침하는 정서적 애착이 얼마나 중요한지 보여줍니다. 보호자들이 인간과 같은 수준의 케어를 원하는 가운데 종양학, 정형외과, 만성질환 분야가 성장하고 있습니다. 반려동물 보험사들은 인간의 건강 보험 혜택을 모방하는 형태로 보험 적용 범위를 확대하고, 유전성 질환과 행동 치료의 보장 범위를 넓히고 있습니다. 한편, 가금류 분야는 통합 업체의 사업 확장과 규제 당국의 식품 안전 모니터링 강화로 인해 6.38%의 연평균 복합 성장률(CAGR)로 가장 빠른 카테고리 성장을 달성했습니다. 조류독감, 살모넬라, 뉴캐슬병에 대한 백신 접종은 필수적인 운영 비용으로 지속적인 수요가 발생하고 있습니다.

반추동물 및 양돈 분야는 생식호르몬, 루멘개량제 등 생산성 향상 관련 처치로 인해 안정적인 점유율을 유지하고 있습니다. 경주마에게는 줄기세포 주사나 다혈소판 혈장치료와 같은 고수익 재생의료가 부유층 소유주들을 대상으로 제공되고 있습니다. 종을 불문하고 국제수역사무국(OIE)의 감시보고 의무가 확대됨에 따라 진단 처리 능력이 향상되고 있습니다. 이러한 종을 초월한 추세로 인해 수의학 시장은 지역적 수요 충격에 대한 내성을 유지하고 있습니다.

지역별 분석

북미는 2025년에도 가장 규모가 큰 지역 점유율을 유지했습니다. 이는 높은 반려동물 보유율, 성숙한 보험 네트워크, 지원적인 규제에 힘입은 것입니다. 미국의 지방 진료용 융자 면제 제도와 캐나다의 인재 육성 보조금은 의료 소외 지역을 완화하고, 의료 서비스가 부족한 지역 사회에 제품 보급을 촉진하고 있습니다. 유럽은 2위를 차지하고 있으며, 제품 출시를 간소화하는 EU 내 통일된 라이선스 프로세스와 예방적 개입을 촉진하는 엄격한 동물복지 기준을 바탕으로 하고 있습니다. 제조업체들은 공급 연속성을 보장하는 이중 창고 모델을 통해 브렉시트 이후 통관 마찰을 극복하고 있습니다.

아시아태평양은 가장 빠른 성장세를 보이며 2031년까지 절대 매출에서 유럽을 능가할 것으로 예측됩니다. 중국, 한국, 인도의 도시화된 중산층 가구가 반려동물 관련 지출을 주도하는 한편, 지역 축산 현대화 프로그램이 백신 및 진단 의약품 분야에 지속적인 자본을 투입하고 있습니다. 외국인 직접투자와 현지 합작투자와 함께 기술 이전이 가속화되면서 선진국 시장 기준과의 격차가 좁혀지고 있습니다. 아세안 국가들은 수의학 시장의 장기적인 전망을 확고히 하기 위해 수의학 서비스를 공중보건 체계에 통합하고, 인수공통전염병 감시를 위한 예산을 배정하고 있습니다.

남미와 중동 및 아프리카에서는 가금류 및 양식업의 확대로 인해 중간 정도의 한 자릿수 성장이 예상됩니다. 환율 변동과 규제 집행의 불균등성이 단기적으로 지출을 억제하는 반면, 지역 유통업체와의 다국적 제휴를 통해 유통 효율성은 꾸준히 개선되고 있습니다. 지역 간 전자상거래 플랫폼이 진료소를 위한 저비용 공급 경로로 부상하면서 경쟁 우위는 옴니채널 대응이 가능한 사업자에게로 이동하고 있습니다. 따라서 지리적 다각화는 지역적 충격에 대한 완충 역할을 하며 세계 수의학 시장의 성장 궤도를 유지하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The veterinary healthcare market is expected to grow from USD 62.28 billion in 2025 to USD 66.48 billion in 2026 and is forecast to reach USD 92.16 billion by 2031 at 6.75% CAGR over 2026-2031.

Companion-animal spending, robust livestock expansion in emerging economies, and rapid digital adoption inside veterinary practices underpin the steady rise in the veterinary healthcare market. Preventive care models are becoming mainstream as owners demand earlier disease detection, insurers encourage risk-mitigation protocols, and regulators tighten biosecurity requirements. Diagnostic innovations, especially molecular point-of-care systems, are reshaping clinical workflows by compressing result turnaround from days to minutes. Meanwhile, therapeutic portfolios evolve toward vaccines, immunomodulators, and novel parasiticides that comply with antimicrobial-stewardship mandates. Digital health platforms link patient records, on-farm sensors, and genetic data, allowing clinicians to navigate complex treatment choices while monetizing real-time insights.

Global Veterinary Healthcare Market Trends and Insights

Rising Demand for Protein-Rich Animal Products

Livestock producers are scaling operations to meet a projected 40% rise in protein consumption across developing nations by 2030, a dynamic that forces farms to adopt intensive biosecurity and prophylactic protocols. Higher stocking densities increase infection risk, so veterinarians deploy blanket vaccination and continuous health monitoring to avoid catastrophic outbreaks. Asian aquaculture operators now embed diagnostic sensors directly into recirculating systems, feeding real-time data to remote veterinarians who adjust treatment regimens on the fly. Precision nutrition programs that combine feed additives with diagnostic feedback loops blur lines between traditional animal health and production. The heightened disease-control costs ultimately expand per-animal healthcare budgets, reinforcing sustained demand in the veterinary healthcare market.

Increasing Pet Humanization and Healthcare Spending

Seventy percent of U.S. households owned at least one pet in 2024, and average annual veterinary outlay climbed to USD 1,480 per household, up 23% from 2019. Owners treat pets as family members, tolerating premium prices for cancer immunotherapies, dental implants, and behavioral tele-consults. Pet insurance penetration remains below 5% worldwide, positioning underwriters to unlock latent demand by spreading high-ticket costs. Demand for wellness plans that bundle vaccines, diagnostics, and nutrition counseling promotes recurring revenue for clinics. This sentiment shift elevates diagnostic compliance, accelerating adoption of point-of-care platforms inside general practices. Growing emotional attachment fuels non-price-sensitive segments, upholding the veterinary healthcare market even during broader economic slowdowns.

Stringent Regulatory Compliance and Approval Timelines

Average development times for novel veterinary drugs now exceed seven years, partly due to the FDA's 2024 environmental-impact standards that added up to two extra years per submission. Small innovators struggle to finance protracted trials and multiregional dossiers, reducing pipeline diversity. As fee schedules and post-approval surveillance demands climb, firms prioritize blockbuster indications and shelve niche therapies. The resulting innovation bottleneck could slow adoption of next-generation treatments, although partnering deals with contract research organizations help mitigate capital strain. Consolidation among sponsors concentrates regulatory expertise but may intensify pricing power within the veterinary healthcare market.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Livestock Production in Emerging Economies

- Regulatory Shift Toward Preventive Vaccination Programs

- High Cost of Advanced Therapeutics and Diagnostic Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostics generated the fastest revenue growth at a 7.12% CAGR through 2031, even though therapeutics held a 62.45% share of 2025 sales inside the veterinary healthcare market. Point-of-care analyzers integrate hematology, chemistry, and PCR cartridges in compact footprints that suit first-opinion clinics. In-clinic testing boosts case acceptance and captures revenue previously routed to reference labs. Molecular panels detect multi-pathogen profiles from a single swab, supporting precision medicine protocols once confined to human care. Meanwhile, vaccine portfolios underpin the therapeutic stronghold, safeguarding herd health and limiting antimicrobial overuse. Generic competition pressures margins for legacy antimicrobials, so leading firms emphasize biologics, immunomodulators, and targeted parasiticides. Post-patent biosimilar entries spur price competition but widen access in cost-sensitive settings, ultimately expanding the addressable veterinary healthcare market.

Therapeutic pipelines respond to antimicrobial-stewardship guidance with alternatives such as bacteriophage cocktails and probiotic feed additives. Sustained-release injectables minimize handling stress and labor at large livestock units. In companion animals, combination flea-tick-heartworm preventives command premium price points due to compliance convenience. The United States Environmental Protection Agency's updated residue-limit rules elevate demand for rapid residue diagnostics, binding therapeutic and diagnostic sales strategies. Companies with omnichannel distribution capabilities synchronize product launches across e-commerce, hospitals, and farm-supply outlets to optimize the veterinary healthcare market size momentum.

Dogs and cats represented 55.10% of 2025 revenue, underscoring the emotional attachment that underpins discretionary spending power in the veterinary healthcare market. Oncology, orthopedic, and chronic-disease segments flourish as owners pursue human-grade care. Pet insurers broaden formularies to mirror human health benefits, expanding coverage of hereditary conditions and behavioral therapy. In contrast, poultry achieved the fastest category growth at 6.38% CAGR as integrators scale operations, and regulators tighten food-safety scrutiny. Vaccination against avian influenza, Salmonella, and Newcastle disease forms a mandatory cost of operation, embedding ongoing demand.

Ruminant and swine segments maintain steady share driven by productivity-linked interventions such as reproductive hormones and rumen modifiers. Equine athletes command high-margin regenerative therapies like stem-cell injections and platelet-rich plasma, tapping affluent owner demographics. Across species, the World Organisation for Animal Health expands surveillance reporting obligations, elevating diagnostic throughputs. Such cross-species dynamics keep the veterinary healthcare market resilient against localized demand shocks.

The Veterinary Healthcare Market Report is Segmented by Product (Therapeutics and Diagnostics), Animal Type (Dogs & Cats, and More), Route of Administration (Oral, and More), End User (Veterinary Hospitals & Clinics, and More), and Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained the largest regional share in 2025, propelled by high pet ownership, mature insurance networks, and supportive regulation. Rural-practice loan forgiveness in the United States and workforce grants in Canada mitigate care deserts, extending product uptake into underserved communities. Europe ranked second, supported by pan-EU licensing pathways that streamline product launches and by stringent animal-welfare standards that drive preventive interventions. Manufacturers navigate post-Brexit customs friction through dual warehousing models that secure supply continuity.

Asia-Pacific recorded the fastest growth and is forecast to surpass Europe in absolute sales before 2031. Urbanizing middle-class households in China, South Korea, and India fuel companion-animal spend, while regional livestock modernization programs inject sustained capital into vaccines and diagnostics. Foreign direct investment teamed with local joint ventures accelerates technology transfer, narrowing the gap with developed-market standards. Governments across ASEAN allocate budget to zoonotic-disease surveillance, integrating veterinary services into public-health frameworks, thereby cementing the long-run outlook for the veterinary healthcare market.

South America and the Middle East & Africa post mid-single-digit growth tied to poultry and aquaculture expansion. Currency volatility and uneven regulatory enforcement temper short-term spending, but multinational alliances with regional distributors steadily improve channel efficiency. Pan-regional e-commerce platforms emerge as low-cost supply routes for clinics, tilting competitive balance toward players with omnichannel fulfillment. Thus, geographic diversification acts as a buffer against localized shocks, sustaining the global veterinary healthcare market trajectory.

- Bimeda

- Boehringer Ingelheim

- Ceva Sante Animale

- Covetrus

- Dechra Pharmaceuticals

- Elanco

- Heska

- IDEXX

- ImmuCell

- INDICAL Bioscience

- Innovative Diagnostics

- Merck

- Neogen

- Norbrook

- PetIQ

- Phibro Animal Health

- Randox Laboratories

- Thermo Fisher Scientific

- Vetoquinol

- Virbac

- Zomedica

- Zoetis

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Protein-Rich Animal Products

- 4.2.2 Increasing Pet Humanization and Healthcare Spending

- 4.2.3 Expanding Livestock Production in Emerging Economies

- 4.2.4 Regulatory Shift Toward Preventive Vaccination Programs

- 4.2.5 Digital Transformation of Veterinary Practices

- 4.2.6 Integration of One Health Surveillance Systems

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Compliance and Approval Timelines

- 4.3.2 High Cost of Advanced Therapeutics and Diagnostic Equipment

- 4.3.3 Growing Antimicrobial Resistance Stewardship Restrictions

- 4.3.4 Persistent Veterinary Workforce Shortages in Rural Areas

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat Of New Entrants

- 4.7.2 Bargaining Power Of Buyers

- 4.7.3 Bargaining Power Of Suppliers

- 4.7.4 Threat Of Substitute Products

- 4.7.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Therapeutics

- 5.1.1.1 Vaccines

- 5.1.1.2 Parasiticides

- 5.1.1.3 Anti-Infectives

- 5.1.1.4 Medical Feed Additives

- 5.1.1.5 Other Therapeutics

- 5.1.2 Diagnostics

- 5.1.2.1 Immunodiagnostic Tests

- 5.1.2.2 Molecular Diagnostics

- 5.1.2.3 Diagnostic Imaging

- 5.1.2.4 Clinical Chemistry

- 5.1.2.5 Other Diagnostics

- 5.1.1 Therapeutics

- 5.2 By Animal Type

- 5.2.1 Dogs & Cats

- 5.2.2 Horses

- 5.2.3 Ruminants

- 5.2.4 Swine

- 5.2.5 Poultry

- 5.2.6 Other Animal Types

- 5.3 By Route Of Administration

- 5.3.1 Oral

- 5.3.2 Parenteral

- 5.3.3 Topical

- 5.3.4 Other Route of Administrations

- 5.4 By End User

- 5.4.1 Veterinary Hospitals & Clinics

- 5.4.2 Reference Laboratories

- 5.4.3 Point-Of-Care / In-House Testing Settings

- 5.4.4 Academic & Research Institutes

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Bimeda

- 6.3.2 Boehringer Ingelheim

- 6.3.3 Ceva Sante Animale

- 6.3.4 Covetrus

- 6.3.5 Dechra Pharmaceuticals

- 6.3.6 Elanco

- 6.3.7 Heska Corporation

- 6.3.8 IDEXX Laboratories

- 6.3.9 ImmuCell

- 6.3.10 INDICAL Bioscience

- 6.3.11 Innovative Diagnostics (IDVet)

- 6.3.12 Merck & Co., Inc.

- 6.3.13 Neogen Corporation

- 6.3.14 Norbrook

- 6.3.15 PetIQ

- 6.3.16 Phibro Animal Health

- 6.3.17 Randox Laboratories

- 6.3.18 Thermo Fisher Scientific

- 6.3.19 Vetoquinol

- 6.3.20 Virbac

- 6.3.21 Zomedica

- 6.3.22 Zoetis, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment