|

시장보고서

상품코드

1937287

영국의 체외진단 시장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom In-Vitro Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

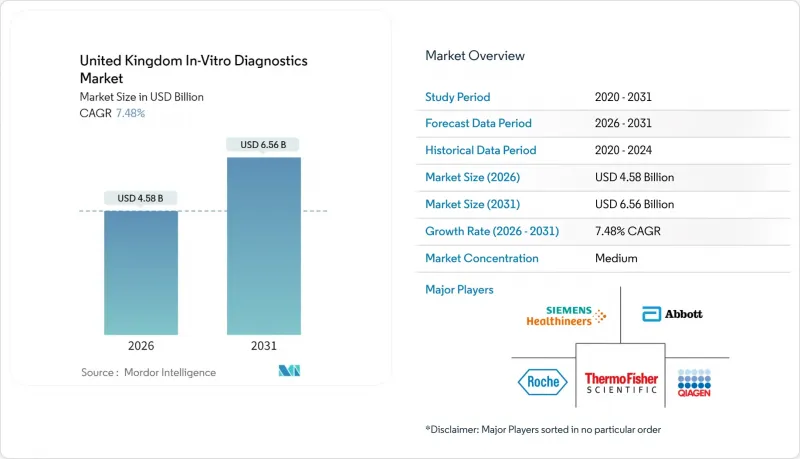

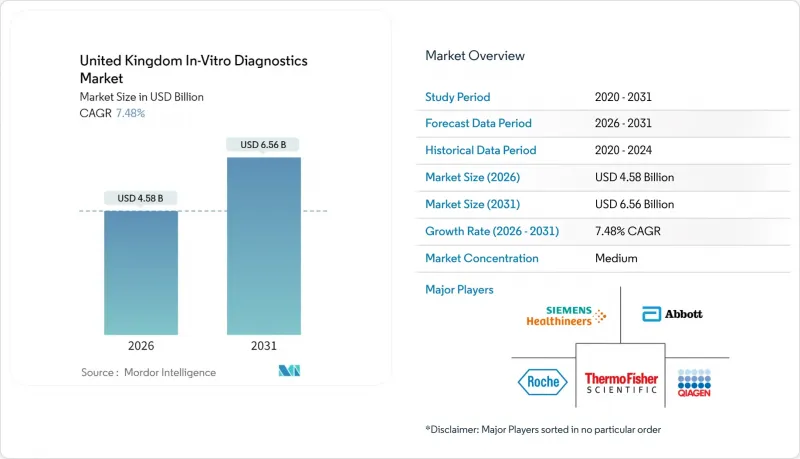

영국의 체외진단 시장은 2025년에 42억 6,000만 달러로 평가되었고, 2026년 45억 8,000만 달러에서 2031년까지 65억 6,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년)의 CAGR은 7.48%로 예상됩니다.

이러한 성장은 이미 700만 건 이상의 검사를 실시했으며, 2025년 3월까지 1,700만 건을 목표로 하는 NHS 지역 진단센터에 의해 추진되고 있습니다. 고령화, 특히 85세 이상 인구층(25년 내 260만 명으로 두 배로 증가할 것으로 예상)이 만성질환 관리 검사에 대한 수요를 확대하고 있습니다. NHS 앱과 재택 검사 프로그램을 중심으로 한 디지털 혁신으로 인해 전자 건강 기록과 원활하게 연동되는 현장 진료 검사 및 분자진단 플랫폼에 대한 수요가 증가하고 있습니다. 한편, 의약품의료기기규제청(MHRA)의 국제 인증 프레임워크에 따른 규제 정합화가 진행되어 승인까지의 기간이 단축됨에 따라 해외 혁신 기업들의 영국 시장 진출이 활발해지고 있습니다. 경쟁의 강도는 여전히 중간 정도입니다. 대형 다국적 기업들은 IVDR 준수 규정에 적응하고 있으며, 옥스포드 나노포어(Oxford Nanopore)와 같은 현지 기업들은 NHS와의 제휴를 통해 감염성 질환 분야의 틈새 시장을 확보하고 있습니다.

영국의 체외진단 시장 동향과 인사이트

만성질환 유병률 증가

성인의 7.8%가 당뇨병을 앓고 있으며, 특히 웨스트미들랜즈 지역에서는 8.6%의 높은 유병률을 보여 다항목 검사 패널에 대한 수요가 집중되고 있습니다. 또한, 관상동맥질환 환자 중 187만 9,000명이 심혈관 질환을 동반하고 있어 일상적인 바이오마커 검사에 대한 수요를 더욱 높이고 있습니다. 50세 이상 당뇨병 환자의 3분의 1은 여러 질환을 동반하고 있어 대사, 신장 기능, 지질 검사를 통합한 플랫폼으로의 조달을 촉진하고 있습니다. 환자가 집에서 질병 관리를 하는 가운데, 지역 의료 현장에서의 검사 실시가 증가하고 있어 휴대용 분석기 도입을 뒷받침하고 있습니다. NHS의 예방 정책은 조기 발견 프로그램에 중점을 두고 있으며, 지역 보건 대시보드에 적합한 선별 키트를 제공하는 공급업체가 우위를 점하고 있습니다.

고령화와 동반질환 부담 증가

영국의 85세 이상 인구는 260만 명에 달하며, 2040년까지 910만 명이 심각한 질병을 앓고 있을 것으로 예측됩니다. 노인 부양비는 309명에서 364명으로 증가하여 검사실 워크플로우 자동화와 AI 지원 진단 도입이 시급한 상황입니다. 남서부는 고령화 지표에서 앞서고 있으며, 고령자를 위한 검사 패널 및 뼈 건강 검진에 대한 지역 수요를 형성하고 있습니다. 2040년까지 주요 질환을 앓고 있는 평균 수명은 12.6년에 달할 것으로 예상되며, 정기적인 모니터링 수익이 보장됩니다. 따라서 재택 및 웨어러블 진단기기 업체들은 NHS 계획 담당자들이 재택 고령화 솔루션을 모색하는 과정에서 정책적 지원을 받고 있습니다.

IVDR 준수 규제 강화

EU의 IVDR 시행으로 인증기관 심사가 필요한 의료기기의 비율이 15%에서 최대 90%로 확대되면서 인증 파이프라인이 타이트해져 제품 출시가 지연되고 있습니다. 북아일랜드는 EU 규정이 적용되기 때문에 영국 전역에서 판매되는 제품에는 이중 표시와 다른 시판 후 조사가 의무화되어 있습니다. MHRA의 2025년 규제 개정으로 사건 보고 기간 단축과 시판 후 조사 의무 강화가 예정되어 있습니다. 중소기업은 불균형한 문서 관리 부담과 높은 감사 비용에 직면하여 제품 파이프라인이 축소될 수 있습니다. 그러나 호주, 캐나다, EU 또는 미국에서 취득한 승인에 대한 새로운 상호 승인 경로를 통해 2026년까지 컴플라이언스 마찰이 완화될 수 있습니다.

부문 분석

분자진단은 2025년 매출 10억 2,000만 달러에 기여하고 9.38%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되며, 영국의 체외진단 시장에서 가장 높은 성장률을 보일 것으로 예측됩니다. 면역진단은 NHS 연구소에 도입된 고처리량 분석기기에 힘입어 32.12%의 점유율로 수량 기준 1위 자리를 지키고 있습니다. Oxford Nanopore의 6.7시간 만에 패혈증 병원균을 배제하는 기술 등 분자진단의 혁신은 항생제 남용을 억제하고 항균제 적정 사용 프로그램을 강화합니다. 한편, 만성질환 모니터링의 확대에 따라 임상화학 분야의 영국의 체외진단 시장 규모는 꾸준히 성장하고 있으며, 지질, 신장기능, 간기능 패널은 여전히 필수적입니다. 수혈 반응을 억제하는 새로운 유전자형 검사로 혈액학 분야 수요도 뒷받침되고 있습니다. 미생물학은 갈림길에 서 있습니다. 일부 배양 검사는 당일 결과를 제공하는 다중 PCR로 대체되고 있지만, 전통적인 감수성 검사는 여전히 항생제 지도의 기초가 되고 있습니다. 응고 검사는 심방세동 위험이 높은 고령자 집단에서 그 중요성이 유지되고 있습니다. MHRA(의약품 및 의료제품 규제기관)의 AI 전략은 머신러닝 지원 돌연변이 검출의 성능 지표를 정의하여 분자진단의 채택을 촉진하고, 유전체학을 일상 업무 흐름에 더욱 통합할 수 있도록 합니다.

2차적인 효과로 바이오인포매틱스 파이프라인과 클라우드 스토리지의 소프트웨어 라이선스 수요가 증가하고 있습니다. 면역진단 벤더는 NHS 데이터 레이크에 연결되는 모듈을 내장하여 플랫폼의 정착성을 확보하는 방식으로 대응하고 있습니다. 시약 공급업체는 나노포어 분석 워크플로우에 특화된 추출 화학물질을 번들링할 수 있는 기회를 얻었습니다. 다만, 차세대염기서열분석의 보험 적용 범위가 제한적이기 때문에 의료경제적 근거가 확립되기 전까지는 전문기관 외에는 병원 도입이 확산되기 어려운 상황입니다.

시약 및 키트는 2025년 27억 8,000만 달러로 영국의 체외진단 시장 점유율의 65.10%를 차지할 것으로 예측됩니다. 소프트웨어 서비스는 4억 5,000만 달러로 규모는 작지만, 디지털 병리학과 AI 분석이 종양학 및 미생물학 분야에 침투함에 따라 CAGR 11.42%로 성장하고 있습니다. 영국의 체외진단 시장의 장비 판매 규모는 병원이 기존 설비를 최대한 활용하는 가운데 보합세를 보이고 있지만, 업데이트 주기에서는 원격진단 대응 자동화 시스템이 초점이 되고 있습니다. 34억 파운드 규모의 NHS 기술 업데이트 프로그램에서는 분석 장비와 NHS 앱을 연동하는 상호 운용 가능한 미들웨어에 대한 자금이 할당되어 있습니다. 구독형 분석 제품군을 제공하는 벤더들은 자본 제약을 완화하고, 수익을 가동률에 연동하여 수익을 창출하고 있습니다.

동시에, 임상검사 시스템 공급업체는 지역 및 병원 데이터를 통합하는 지역 의료 대시보드를 통합합니다. 시약 공급업체는 동반 분석 교정 소프트웨어를 도입하여 소모품의 연동 수요를 확보함으로써 리스크를 헤지하고 있습니다. AI를 통한 품질 관리 기능을 갖춘 기기는 MHRA의 시판 후 조사 요건을 충족하고 수동 감사를 최소화합니다. 그러나 데이터 주권 관련 규제가 순수한 클라우드 호스팅형 솔루션을 저해할 수 있어 하이브리드 아키텍처의 채택을 촉진하고 있습니다. 조달 평가 기준에는 사이버 보안 준수가 포함되어 있으며, 중소규모의 ISV(독립 소프트웨어 벤더)가 기존 주요 계약업체와 협력하도록 유도하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.03.10The United Kingdom In-Vitro Diagnostics market was valued at USD 4.26 billion in 2025 and estimated to grow from USD 4.58 billion in 2026 to reach USD 6.56 billion by 2031, at a CAGR of 7.48% during the forecast period (2026-2031).

Growth is propelled by NHS Community Diagnostic Centres that have already delivered more than 7 million tests and aim for 17 million by March 2025. An aging population-particularly the cohort aged 85 and over, which is set to double to 2.6 million within 25 years-is expanding chronic-care testing volumes. Digital transformation built around the NHS App and home testing programs is boosting demand for point-of-care and molecular platforms that integrate seamlessly with electronic health records. Meanwhile, regulatory alignment through the MHRA's international recognition framework is shortening approval timelines and encouraging overseas innovators to enter the UK market. Competitive intensity remains moderate; large multinationals are adapting to IVDR-aligned rules while local firms such as Oxford Nanopore capture infectious-disease niches through NHS partnerships.

United Kingdom In-Vitro Diagnostics Market Trends and Insights

Rising Prevalence of Chronic Diseases

Diabetes affects 7.8% of UK adults, with the West Midlands recording an 8.6% hotspot that concentrates demand for multi-analyte panels. Cardiovascular disease adds 1.879 million coronary-heart-disease patients, further lifting routine biomarker testing volumes. One-third of diabetics aged 50 plus live with multiple conditions, steering procurement toward integrated platforms that consolidate metabolic, renal, and lipid assays. Community care settings increasingly host this testing as patients manage conditions at home, underpinning portable analyzer uptake. NHS prevention policy favors early detection programs, incentivizing suppliers that tailor screening kits to population-health dashboards.

Aging Population & Higher Comorbidity Burden

England's over-85 cohort is forecast to hit 2.6 million, while 9.1 million citizens may live with major illness by 2040. The old-age dependency ratio will rise from 309 to 364, urging laboratories to automate workflows and adopt AI-aided interpretation. The South West leads aging metrics, shaping localized demand for geriatric panels and bone-health assays. Average years lived with major illness could reach 12.6 by 2040, locking in recurring monitoring revenues. Therefore, vendors of home-based and wearable diagnostics enjoy policy support as NHS planners seek aging-in-place solutions.

IVDR-Aligned Regulatory Stringency

EU IVDR raised the proportion of devices needing notified-body review from 15% to up to 90%, crowding certification pipelines and deferring launches. Northern Ireland remains under EU rules, compelling dual labeling and divergent post-market surveillance for products sold across the UK. The MHRA's 2025 overhaul adds shorter incident-reporting windows and stricter PMS obligations. Smaller firms face disproportionate document-control burdens and higher audit fees, potentially thinning product pipelines. However, new mutual-recognition pathways for approvals secured in Australia, Canada, the EU, or the USA may mitigate compliance friction by 2026.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Point-of-Care Testing

- Increased Acceptance of Personalized Medicine & Companion Dx

- Reimbursement Pressure on High-Cost Molecular Assays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Molecular diagnostics contributed USD 1.02 billion to 2025 turnover and is poised for a 9.38% CAGR, the fastest within the UK In-Vitro Diagnostics market. Immunodiagnostics retains the volume crown with a 32.12% slice, supported by high-throughput analyzers embedded across NHS labs. Molecular innovations like Oxford Nanopore's 6.7-hour sepsis-pathogen rule-out reduce antibiotic overuse and strengthen antimicrobial stewardship programs. Meanwhile, the UK In-Vitro Diagnostics market size for clinical chemistry grows steadily as chronic-care monitoring expands; lipid, renal, and liver panels remain essential. Haematology demand is buoyed by new genotyping assays that curb transfusion reactions. Microbiology stands at a crossroads-a portion of cultures is being displaced by multiplex PCR that delivers same-day results, yet traditional susceptibility testing still underpins antibiotic guidance. Coagulation maintains relevance in elderly cohorts prone to atrial fibrillation. The MHRA's AI strategy boosts molecular adoption by defining performance metrics for machine-learning-assisted variant calling, further integrating genomics into routine workflows.

Second-order effects include increased software licenses for bioinformatics pipelines and cloud storage. Immunodiagnostics vendors respond by embedding connectivity modules that feed NHS data lakes, ensuring platform stickiness. Reagent manufacturers face opportunities to bundle extraction chemistries tailored to nanopore workflows. However, limited reimbursement for next-generation sequencing constrains broader hospital uptake beyond specialized centers until health-economic cases mature.

Reagents and kits generated USD 2.78 billion in 2025, comprising 65.10% of the UK In-Vitro Diagnostics market share. Software & services, though smaller at USD 405 million, enjoys an 11.42% CAGR as digital pathology and AI analytics penetrate oncology and microbiology benches. The UK In-Vitro Diagnostics market size for instrument sales plateaus as hospitals exploit existing capacity, but refresh cycles focus on automated systems compatible with remote diagnostics. The GBP 3.4 billion NHS tech-upgrade program allocates funds to interoperable middleware that links analyzers to the NHS App. Vendors offering subscription-based analytical suites mitigate capital constraints and align revenues with utilization.

In parallel, LIS vendors integrate population-health dashboards that pool community and hospital data. Reagent suppliers hedge by launching companion assay-calibration software to lock in consumable pull-through. Instruments with AI-guided quality control satisfy MHRA post-market surveillance, minimizing manual audits. Nevertheless, data-sovereignty rules may deter purely cloud-hosted solutions, pushing hybrid architectures. Procurement scores now bundle cybersecurity compliance, nudging smaller ISVs to partner with established prime contractors.

The United Kingdom In-Vitro Diagnostics Market Report is Segmented by Technique (Clinical Chemistry, Molecular Diagnostics, Immunodiagnostics, and More), Product (Instruments, Reagents, and More), Usability (Disposable IVD Devices and Re-Usable IVD Devices), Application (Infectious Disease, Diabetes, Oncology, and More), and End-User (Hospital & Reference Labs, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Abbott Laboratories

- Roche

- Siemens Healthineers

- Danaher Corp. (Beckman Coulter & Cepheid)

- Thermo Fisher Scientific

- Beckton Dickinson

- Bio-Rad Laboratories

- bioMerieux

- Sysmex

- FUJIFILM

- Randox Laboratories

- Oxford Nanopore Technologies

- LumiraDx

- Genedrive plc

- EKF Diagnostics

- Quotient Ltd.

- Hologic

- Illumina

- Revvity, Inc.

- LGC Group

- QIAGEN

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence Of Chronic Diseases

- 4.2.2 Ageing Population & Higher Comorbidity Burden

- 4.2.3 Growing Adoption Of Point-Of-Care Testing

- 4.2.4 Increased Acceptance Of Personalised Medicine & Companion Dx

- 4.2.5 NHS Community Diagnostic Centres Roll-Out

- 4.2.6 AI-Driven Digital Pathology Accelerating Test Volumes

- 4.3 Market Restraints

- 4.3.1 IVDR-Aligned Regulatory Stringency

- 4.3.2 Reimbursement Pressure On High-Cost Molecular Assays

- 4.3.3 Post-Brexit Supply-Chain Friction & Customs Delays

- 4.3.4 Shortage Of Skilled Molecular Laboratory Workforce

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technique

- 5.1.1 Clinical Chemistry

- 5.1.2 Immunodiagnostics

- 5.1.3 Molecular Diagnostics

- 5.1.4 Haematology

- 5.1.5 Coagulation

- 5.1.6 Microbiology

- 5.1.7 Point-of-Care Tests

- 5.1.8 Other Techniques

- 5.2 By Product

- 5.2.1 Instruments

- 5.2.2 Reagents & Kits

- 5.2.3 Software & Services

- 5.3 By Usability

- 5.3.1 Disposable IVD Devices

- 5.3.2 Re-usable IVD Devices

- 5.4 By Application

- 5.4.1 Infectious Disease

- 5.4.2 Diabetes

- 5.4.3 Oncology

- 5.4.4 Cardiology

- 5.4.5 Auto-immune Disorders

- 5.4.6 Other Applications

- 5.5 By End-User

- 5.5.1 Hospital & Reference Labs

- 5.5.2 Point-of-Care Settings

- 5.5.3 Academic & Research Institutes

- 5.5.4 Home-Care & Self-Testing

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche AG

- 6.3.3 Siemens Healthineers

- 6.3.4 Danaher Corp. (Beckman Coulter & Cepheid)

- 6.3.5 Thermo Fisher Scientific

- 6.3.6 Becton Dickinson

- 6.3.7 Bio-Rad Laboratories

- 6.3.8 bioMerieux

- 6.3.9 Sysmex

- 6.3.10 Fujifilm Holdings

- 6.3.11 Randox Laboratories

- 6.3.12 Oxford Nanopore Technologies

- 6.3.13 LumiraDx

- 6.3.14 Genedrive plc

- 6.3.15 EKF Diagnostics

- 6.3.16 Quotient Ltd.

- 6.3.17 Hologic, Inc.

- 6.3.18 Illumina, Inc.

- 6.3.19 Revvity, Inc.

- 6.3.20 LGC Group

- 6.3.21 QIAGEN N.V.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment