|

시장보고서

상품코드

1937293

무균 주사제 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sterile Injectable Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

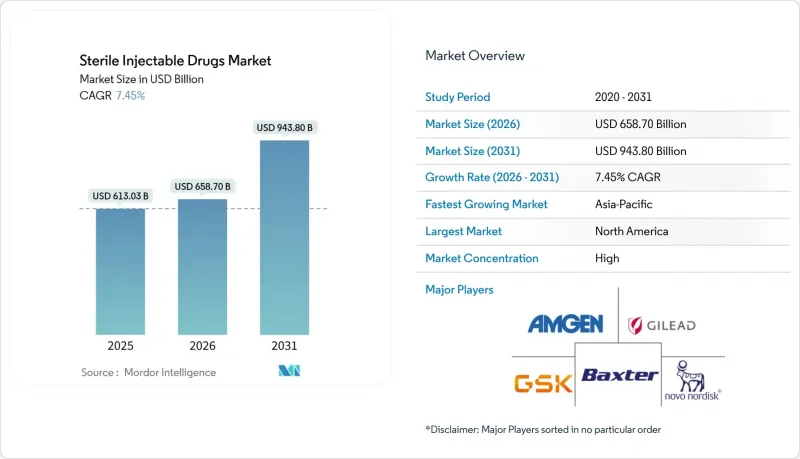

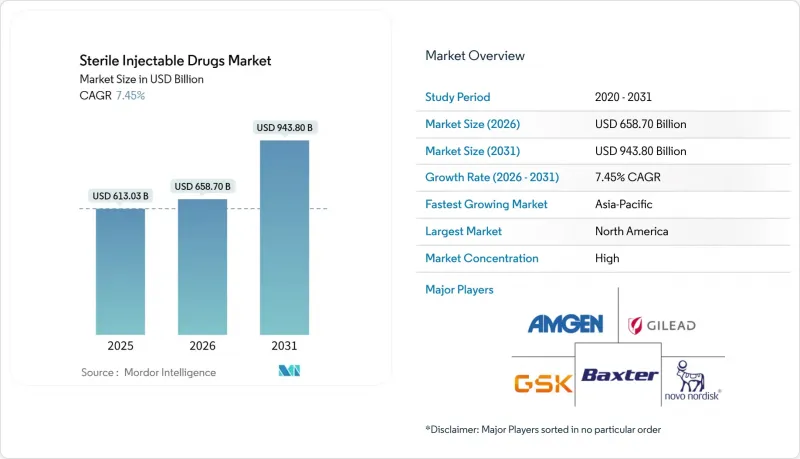

무균 주사제 시장 규모는 2025년 6,130억 3,000만 달러, 2026년 6,587억 달러에서 2031년까지 9,438억 달러로 확대될 것으로 예측되며, 2026년부터 2031년까지 CAGR 7.45%를 기록할 전망입니다.

경쟁의 초점은 바이오로직스(생물학적 제제)에 맞춰져 있으며, 암 치료, 자가면역질환, 희귀질환 파이프라인을 배경으로 고분자 제제가 빠르게 규모를 확장하고 있습니다. 한편, 저분자 제제는 복잡한 주사제 및 급성기 의료 사용 사례를 통해 다시금 활기를 되찾고 있습니다. 단클론항체는 새로운 적응증 확대와 바이오시밀러의 진입으로 우위를 확대하고 있으며, 지역 의료 현장에서의 접근성 확대와 채택 가속화를 촉진하고 있습니다. 병원이 의료 과실 감소를 우선시하고, 지불 기관이 임상적으로 적절한 경우 고비용의 정맥주사 시설 밖에서 치료를 장려하는 가운데, 포장 및 투약 형태는 '투약 준비 완료' 및 '재택 사용' 형식으로 전환되고 있습니다. 지역별로는 북미가 가장 큰 수익 기반을 가지고 있으며, 아시아태평양은 규제 시장을 뒷받침하는 생산능력 확대와 수출 대응 제조 체제 구축으로 성장세를 보이고 있습니다.

세계 무균 주사제 시장 동향 및 전망

생명공학 기술을 이용한 항암제 연구개발(R&D) 집중화

암 생물학적 제제에 대한 파이프라인 투자는 면역 종양학 및 표적 치료제가 치료 효과를 얻기 위해 비경구 투여가 필요하기 때문에 주사제 시장을 계속 재구성하고 있습니다. 2025년에도 새로운 항암제의 FDA 승인은 활발할 것으로 예상되며, 무균 충전 및 포장 공정과 높은 봉쇄 시설과 일치하는 항체약물접합체(ADC) 및 이중특이성항체의 지속적인 발전을 반영하고 있습니다.

화이자의 430억 달러 규모의 씨젠 인수는 ADC 플랫폼의 프리미엄 가치를 뒷받침하고, 표적지향성 비경구 치료제를 기반으로 한 화이자의 광범위한 종양학 사업 기반을 강화했습니다. 제조 전략은 소량 생산과 고효율화가 주류를 이루고 있으며, 검증 기간을 연장하지 않고 교차 오염 위험을 줄이는 폐쇄형 아이솔레이터와 일회용 시스템에 대한 수요를 주도하고 있습니다. 이러한 추세는 복잡한 분석적 동등성 평가를 수행하는 스폰서 기업을 위해 상업적 규모의 결합 화학 및 무균 포장을 결합하는 전문 CDMO의 대응 기반을 확장하고 있습니다. 2024년 말까지 추가 결합체 구조가 FDA 승인을 받은 것은 링커와 페이로드 혁신이 계속 성숙하고 향후 몇 년 동안 상업적 출시가 지속될 것임을 시사합니다.

생물학적 제제용 프리필드 시린지의 급격한 성장세

병원 시스템 및 외래 의료 서비스 제공자가 준비 과정을 줄이고 투약 오류를 방지하는 동시에 병상 및 가정에서의 투약 표준화를 추구함에 따라, 프리필드 플랫폼은 바이알을 대체하고 있습니다. 안전 설계 바늘, 연결 기능, 통합형 자동 주사기 형식은 만성 생물학적 요법에서 사용성과 복약 순응도를 향상시킵니다. 유럽연합(EU) 및 일본 규제 당국은 프리필드 제제의 추출물 및 용출물 관리를 중요시하고 있으며, 개발 리드타임이 길어지고 실제 사용 환경에서의 품질이 강화되고 있습니다. 기기 데이터 수집을 통해 피드백 루프를 형성하고, 일상 진료에서 투약 타이밍과 연속성을 측정할 수 있게함으로써 가치 기반 상환을 지원합니다. 이와 함께 고점도, 소량 투여 제제가 자가 투여의 범위를 확장하고 있으며, 프리필드 시스템은 주사제 시장에서 약물전달의 핵심이 되고 있습니다.

무균 재고 관리의 높은 비용

무균 재고 관리는 창고 보관, 검증된 운송, 온도 모니터링 등 엄격한 규정 준수 요건을 충족해야 하는 모든 공정에서 비용을 증가시킵니다. 저스트인타임 방식은 보유비용 절감에 기여하지만, 수요 변동이 큰 소량 희귀질환 치료제나 항암제의 경우 재고 소진 리스크가 높아집니다. 콜드체인에 대한 투자는 라스트 마일 배송과 재택의료로 확대되고 있으며, 고부가가치 바이오의약품의 직렬화 및 관리망 제어의 복잡성을 증가시키고 있습니다. 디지털 추적 솔루션은 가시성을 향상시키지만, 아직 개발 중인 데이터 표준과 네트워크 간 상호운용성을 필요로 합니다. 전반적으로 이러한 요인들은 무균 및 온도 관리가 필수 조건인 주사제 시장에서 수익률을 압박하고 공급 전략을 복잡하게 만들고 있습니다.

부문 분석

2025년 기준, 대형 분자 바이오의약품은 주사제 시장 점유율의 74.30%를 차지했습다. 한편, 소형 분자는 복잡한 주사제의 보급 확대에 따라 2031년까지 CAGR 8.30%로 더욱 빠른 성장이 예상됩니다. 소형 분자는 포유류 세포배양 및 다운스트림 공정의 정제에 비해 무균 여과 및 충전의 개발 주기를 단축하고 자본 집약도를 낮출 수 있다는 장점이 있습니다. 생물학적 제제는 임상적 차별화로 인해 높은 가격을 유지하고 있지만, 바이오시밀러의 진입으로 접근성이 확대되고 처방집 전환이 가속화되고 있습니다. 많은 병원 주도의 적응증은 집중 치료에서 빠른 효과 발현과 예측 가능한 약동학으로 인해 여전히 저분자 주사제에 의존하고 있습니다. 두 카테고리의 파이프라인의 다양성은 병원 및 소매 채널에서 고가 생물학적 제제와 대량 생산 제네릭 의약품이 공존하는 양극화된 시장 구조를 보장합니다.

단클론항체는 2025년 주사제 시장 점유율의 38.00%를 차지할 것으로 예상되며, 종양학 및 면역학 분야에서의 채택 확대에 힘입어 2031년까지 연평균 8.00%의 성장률을 보일 것으로 전망됩니다. 유전자 치료는 혈우병 A와 같은 특정 혈액질환 영역에서 정기적인 예방요법을 대체하기 시작했으며, 해당 영역에서는 단회 치료가 승인되었습니다. 펩타이드 호르몬은 전문 내분비학 및 불임 치료 분야에서 계속 사용되는 반면, GLP-1 및 이중 인크레틴 제제는 체중 관리 및 심장 대사 결과를 향한 당뇨병 치료 경로를 재구성하고 있습니다. 인크레틴이 제2형 당뇨병 치료에서 더 큰 역할을 하게 되면서 인슐린 사용 패턴이 변화하고 있으며, 장치와 제형 모두에서 혁신이 일어나고 있습니다. 오리지널 제약사와 바이오시밀러 개발사들은 차별화된 투여 방법, 지속성 향상 및 결과에서 명확한 가치 제안이 평가되는 환경에 직면해 있습니다.

지역별 분석

북미는 2025년 지역 점유율의 38.40%를 차지했습니다. 이는 높은 1인당 지출, 전문 분야에서의 높은 채택률, 혁신적 주사제에 대한 유리한 상환 환경이 주도하고 있습니다. 미국 내 의사 투여 제품의 사용 패턴과 보험 적용 범위는 종양학 및 면역학 분야에서 오리지널 및 바이오시밀러 제품의 성장을 뒷받침하고 있습니다. 캐나다에서는 보다 엄격한 의료 기술 평가가 적용되어 새로운 치료법에 대한 접근 시간을 연장하고 있지만, 그럼에도 불구하고 주마다 바이오시밀러의 도입이 꾸준히 진행되고 있습니다. 멕시코에서는 병원에 대한 투자와 보험 적용 범위 확대로 필수 치료 분야에서 무균 주사제에 대한 접근성이 지속적으로 확대되고 있습니다.

유럽은 바이오시밀러 도입을 위한 조정된 도입 경로, 경쟁 입찰, 그리고 시간이 지남에 따라 광범위한 환자 접근을 가능하게 하는 조정된 도입 경로를 통해 두 번째 점유율을 유지하고 있습니다. 유럽의약품청(EMA)의 바이오시밀러에 대한 경험은 종양학 및 면역학 분야의 전환과 가격 경쟁의 정상화에 기여했습니다. 아시아태평양은 규제 시장 공급을 위한 생산능력 확대와 수출 지향적 제조에 힘입어 2031년까지 CAGR 8.03%로 성장할 것으로 예측됩니다. 인도와 중국은 CDMO 계약과 종양학 및 만성질환 치료제에 대한 국내 접근을 지원하기 위해 발효 및 충전 및 마무리 능력을 확장하고 있습니다.

일본에서는 고령화로 인해 바이오의약품의 높은 사용률이 지속되고 있지만, 보수적인 처방 경향과 심사기간의 장기화로 인해 신규 클래스의 도입이 늦어지고 있습니다. 중동 및 아프리카(GCC 국가 포함)에서는 수입 의존도 감소와 공급 탄력성 향상을 위해 현지 제조 역량과 병원 시설에 대한 투자가 진행되고 있습니다. 남미에서는 브라질과 아르헨티나에 집중되어 있으며, 공공 조달은 백신과 필수 항균제를 중심으로 전문 바이오의약품에 대한 접근 경로가 진화하고 있습니다. 지역별로 정책과 조달 구조가 가격과 접근성을 결정하지만, 세계 파이프라인과 제조 투자는 주사제 시장의 꾸준한 도입을 지속적으로 뒷받침하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액 : 달러)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05The Sterile Injectable Drugs Market size is projected to expand from USD 613.03 billion in 2025 and USD 658.70 billion in 2026 to USD 943.80 billion by 2031, registering a CAGR of 7.45% between 2026 to 2031.

The competitive focus tilts toward biologics, where large-molecule formats have scaled quickly on the back of oncology, autoimmune, and rare disease pipelines. At the same time, small molecules regain momentum through complex injectables and acute-care use cases. Monoclonal antibodies extend their lead due to new indications and biosimilar entry, which broaden access and accelerate adoption in community settings. Packaging and delivery are shifting toward ready-to-administer and home-use formats as hospitals prioritize error reduction and, when clinically appropriate, payers move therapies out of high-cost infusion sites. Regionally, North America has the most significant revenue base, while Asia-Pacific is advancing through capacity expansion and export-ready manufacturing that support regulated markets.

Global Sterile Injectable Drugs Market Trends and Insights

Rising R&D Focus on Biotechnology-Engineered Anti-Cancer Drugs

Pipeline investment in oncology biologics continues to reshape the injectable drugs market, with immuno-oncology and targeted modalities requiring parenteral delivery to reach therapeutic exposure. FDA approvals of novel cancer agents remained active in 2025, reflecting ongoing advances in antibody-drug conjugates and bispecifics that align with sterile fill-finish and high-containment operations.

Pfizer's acquisition of Seagen for USD 43 billion underscored the premium for ADC platforms and strengthened its larger oncology franchise, anchored in targeted parenteral therapies. Manufacturing strategies increasingly favor smaller batch sizes and higher potency, which drives demand for closed isolators and single-use systems to mitigate cross-contamination risks without lengthening validation timelines. The trend expands the addressable base for specialized CDMOs that combine conjugation chemistry and sterile packaging at commercial scale for sponsors navigating complex analytical comparability. FDA approvals of additional conjugate constructs through late 2024 signaled continued maturation of linker and payload innovation, pointing to sustained commercial launches over the next several years.

Rapid Growth In Pre-Filled Syringes for Biologics

Prefilled platforms continue to displace vials as hospital systems and ambulatory providers reduce reconstitution steps and dosing errors while seeking to standardize administration at the bedside and in the home. Safety-engineered needles, connectivity features, and integrated autoinjector formats are improving usability and adherence for chronic biologic therapies. Regulators in the European Union and Japan emphasize extractables-and leachables controls for prefilled components, which extend development lead times but reinforce quality in real-world use. Device-data capture is creating feedback loops that support value-based reimbursement, as dose timing and persistence become measurable in routine care. In parallel, high-viscosity formulations with smaller volumes are expanding the scope of self-administration, making prefilled systems central to therapy delivery in the injectable drugs market.

High Expenses in Sterile-Inventory Management

Sterile inventory management elevates costs across warehousing, validated transport, and temperature monitoring, all of which must meet stringent compliance requirements. Just-in-time practices help reduce carrying costs but increase the risk of stockouts for small-volume orphan and oncology products subject to variable demand. Cold-chain investments are extending into last-mile delivery and home-based care, which increases the complexity of serialization and chain-of-custody controls for high-value biologics. Digital track-and-trace solutions offer better visibility but require data standards and interoperability that are still evolving across networks. Overall, these factors weigh on margins and complicate fulfillment strategies in the injectable drugs market, where sterility and temperature control are non-negotiable.

Other drivers and restraints analyzed in the detailed report include:

- Increased Outsourcing Across the Injectable Value-Chain

- Growing Chronic-Disease Burden Demanding Parenteral Therapies

- Availability of Alternative Drug-Delivery Routes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large-molecule biologics held 74.30% of the injectable drugs market share in 2025, while small molecules are projected to grow faster at an 8.30% CAGR through 2031 as complex injectables see broader use. Small molecules benefit from shorter development cycles and lower capital intensity for sterile filtration and filling compared to mammalian cell culture and downstream purification. Biologics continue to command premium pricing due to clinical differentiation, but biosimilar entry is broadening access and accelerating formulary shifts. Many hospital-driven indications still rely on small-molecule injectables for rapid onset and predictable pharmacokinetics in critical care. Pipeline diversity across both categories ensures a two-speed market in which high-value biologics coexist with high-volume generics in hospital and retail channels.

Monoclonal antibodies accounted for 38.00% of the injectable drugs market share in 2025 and are set to grow at an 8.00% CAGR through 2031, driven by expanded adoption in oncology and immunology. Gene therapies have begun to displace routine prophylaxis in select hematology indications, including hemophilia A, where a one-time treatment has been approved. Peptide hormones maintain use in specialty endocrinology and fertility, while GLP-1 and dual-incretin agents reshape diabetes care pathways toward weight and cardiometabolic outcomes. Insulin use patterns are evolving as incretins take on a larger role in type 2 diabetes, with device and formulation innovation advancing on both fronts. Originators and biosimilar developers face an environment that rewards differentiated delivery, improved persistence, and a clear value proposition in outcomes.

The Sterile Injectable Drugs Market is Segmented by Molecule Type (Small Molecule, Large Molecule), Drug Class (Blood Factors, Cytokines, and More), Application (Oncology, Neurology, Cardiovascular Diseases, Autoimmune Diseases, Infectious Diseases, Pain, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 38.40% of the regional share in 2025, driven by higher per-capita spending, strong specialty uptake, and a favorable reimbursement environment for innovative injectables. United States utilization patterns and coverage for physician-administered products support the growth of originator and biosimilar products across oncology and immunology. Canada applies more restrictive health-technology assessments that lengthen time-to-access for new therapies, while still enabling meaningful biosimilar uptake province by province. Mexico's hospital investments and expanded coverage continue to broaden access to sterile injectables across essential therapeutic categories.

Europe maintains the second-largest share with coordinated pathways that enable biosimilar entry, competitive tendering, and broad patient access over time. EMA's experience with biosimilars has helped normalize switching and price competition in oncology and immunology classes. Asia-Pacific is forecast to grow at an 8.03% CAGR through 2031, driven by capacity build-outs and export-oriented manufacturing that feed regulated markets. India and China expand fermentation and fill-finish capabilities to support CDMO contracts and local access to oncology and chronic therapies.

Japan's aging demographic sustains high biologics use, although conservative prescribing and longer review timelines slow adoption of novel classes. The Middle East and Africa, including GCC countries, invest in local manufacturing and hospital capacity to reduce import dependency and improve supply resilience. South America sees concentration in Brazil and Argentina, with public procurement emphasizing vaccines and essential antimicrobials and evolving pathways for specialty biologics. Across regions, policy and procurement structures shape price and access, yet the global pipeline and manufacturing investments continue to support steady adoption in the injectable drugs market.

- Abbvie

- Amgen

- AstraZeneca

- Baxter

- Bristol-Myers Squibb

- Dr. Reddy's Laboratories Inc.

- Eli Lilly and Company

- Fresenius

- Gilead Sciences

- GlaxoSmithKline

- Hikma Pharmaceuticals Public Limited Company

- Johnson & Johnson

- Merck

- Novartis

- Novo Nordisk

- Pfizer

- Roche

- Sanofi

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising R&D Focus on Biotechnology-Engineered Anti-Cancer Drugs

- 4.2.2 Rapid Growth In Pre-Filled Syringes for Biologics

- 4.2.3 Increased Outsourcing Across the Injectable Value-Chain

- 4.2.4 Growing Chronic-Disease Burden Demanding Parenteral Therapies

- 4.2.5 Closed-System Robotics Cutting Contamination & Batch Failures

- 4.2.6 Lyophilized Nano-Suspensions Enabling Room-Temperature Shipping

- 4.3 Market Restraints

- 4.3.1 High Expenses in Sterile-Inventory Management

- 4.3.2 Availability of Alternative Drug-Delivery Routes

- 4.3.3 Global Shortage of Pharma-Grade Vials & Stoppers

- 4.3.4 Tariff-Driven Volatility in Sterile API Import Costs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Molecule Type

- 5.1.1 Small Molecule

- 5.1.2 Large Molecule (Biologics)

- 5.2 By Drug Class

- 5.2.1 Blood Factors

- 5.2.2 Cytokines

- 5.2.3 Peptide Hormones

- 5.2.4 Immunoglobulins

- 5.2.5 Monoclonal Antibodies (mAbs)

- 5.2.6 Insulin

- 5.2.7 Other Classes

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Neurology

- 5.3.3 Cardiovascular Diseases

- 5.3.4 Autoimmune Diseases

- 5.3.5 Infectious Diseases

- 5.3.6 Pain Management

- 5.3.7 Other Applications

- 5.4 By Packaging Type

- 5.4.1 Vials (RTU/Bulk)

- 5.4.2 Prefilled Syringes

- 5.4.3 Cartridges & Ampoules

- 5.4.4 Ready-to-Use Blow-Fill-Seal Containers

- 5.5 By Route of Administration

- 5.5.1 Intravenous (IV)

- 5.5.2 Subcutaneous (SC)

- 5.5.3 Intramuscular (IM)

- 5.5.4 Intravitreal / Other Specialty Routes

- 5.6 By Distribution Channel

- 5.6.1 Hospital Pharmacies

- 5.6.2 Retail Pharmacies

- 5.6.3 Online & Specialty Pharmacies

- 5.7 By Geography

- 5.7.1 By Geography

- 5.7.1.1 North America

- 5.7.1.1.1 United States

- 5.7.1.1.2 Canada

- 5.7.1.1.3 Mexico

- 5.7.1.2 Europe

- 5.7.1.2.1 Germany

- 5.7.1.2.2 United Kingdom

- 5.7.1.2.3 France

- 5.7.1.2.4 Italy

- 5.7.1.2.5 Spain

- 5.7.1.2.6 Rest of Europe

- 5.7.1.3 Asia-Pacific

- 5.7.1.3.1 China

- 5.7.1.3.2 India

- 5.7.1.3.3 Japan

- 5.7.1.3.4 South Korea

- 5.7.1.3.5 Australia

- 5.7.1.3.6 Rest of Asia-Pacific

- 5.7.1.4 Middle East and Africa

- 5.7.1.4.1 GCC

- 5.7.1.4.2 South Africa

- 5.7.1.4.3 Rest of Middle East and Africa

- 5.7.1.5 South America

- 5.7.1.5.1 Brazil

- 5.7.1.5.2 Argentina

- 5.7.1.5.3 Rest of South America

- 5.7.1.1 North America

- 5.7.1 By Geography

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca Plc

- 6.3.4 Baxter International Inc.

- 6.3.5 Bristol-Myers Squibb Company

- 6.3.6 Dr. Reddy's Laboratories Inc.

- 6.3.7 Eli Lilly & Company

- 6.3.8 Fresenius Kabi AG

- 6.3.9 Gilead Sciences Inc.

- 6.3.10 GSK plc

- 6.3.11 Hikma Pharmaceuticals Public Limited Company

- 6.3.12 Johnson & Johnson Services, Inc.

- 6.3.13 Merck & Co., Inc.

- 6.3.14 Novartis AG

- 6.3.15 Novo Nordisk A/S

- 6.3.16 Pfizer Inc.

- 6.3.17 F. Hoffmann-La Roche AG

- 6.3.18 Sanofi SA

- 6.3.19 Sun Pharmaceutical Industries Limited

- 6.3.20 Teva Pharmaceutical Industries Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment