|

시장보고서

상품코드

1937296

중국의 고급차 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)China Luxury Car - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

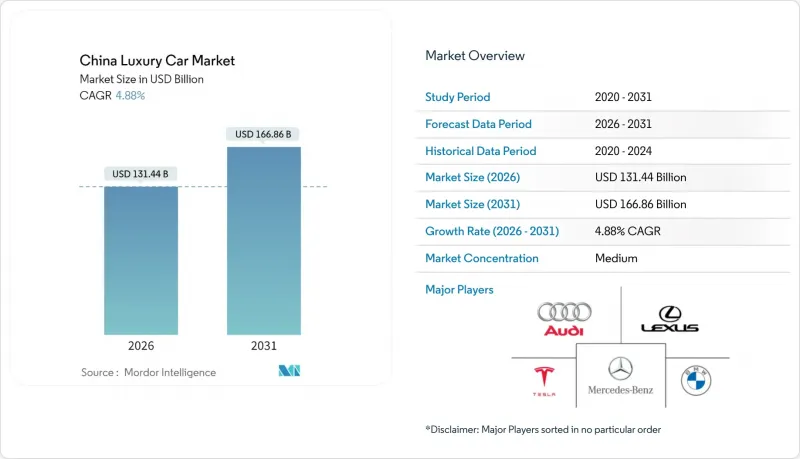

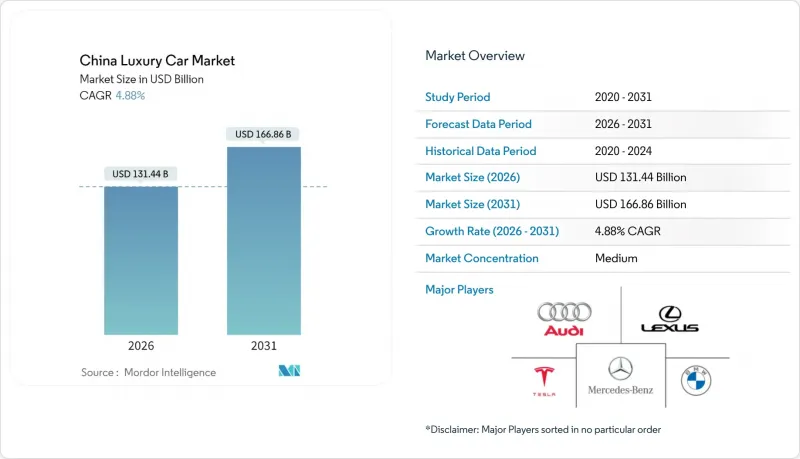

중국의 고급차 시장은 2025년 1,253억 2,000만 달러에서 2026년에는 1,314억 4,000만 달러로 성장할 것으로 예상되며, 2026년부터 2031년까지 CAGR 4.88%를 기록하며 2031년까지 1,668억 6,000만 달러에 달할 것으로 예측됩니다.

이러한 확대는 가속화되는 전기화, 지방 도시의 가처분 소득 증가, 그리고 신에너지 자동차(NEV)를 우대하는 정책적 지원으로 뒷받침되고 있습니다. 프리미엄 차량을 이동형 기술 플랫폼으로 인식하는 소비자의 인식 변화도 수요 증가의 원동력으로 작용하고 있으며, 제조사들은 자율주행 기능과 커넥티드 서비스 생태계를 강화해야 하는 상황에 직면해 있습니다. 국내 전기 고급 브랜드가 기존 기술 격차를 줄이는 반면, 외자 브랜드는 플랫폼 현지화를 통해 중국 고급차 시장에서의 지위를 지키려 하고 있어 경쟁이 치열해지고 있습니다. 반도체 현지화의 진전과 세제 개정 동향은 가치사슬 전반의 수익률, 공급망 전략, 제품 구성 결정에 지속적으로 영향을 미칠 것으로 예상됩니다.

중국 고급차 시장 동향과 인사이트

지방도시의 소비자 부유층 확대

지방도시의 가계소득은 매년 대도시의 성장률을 상회하는 속도로 증가하고 있으며, 자동차를 지위의 상징이자 기술의 쇼케이스로 여기는 새로운 고급차 구매층을 창출하고 있습니다. Li Auto 등 국내 브랜드는 2024년 50만 508대를 인도할 예정으로, ADAS가 탑재된 대형 고급 SUV를 수용하는 가정이 얼마나 많은지 보여주고 있습니다. 최대 2만 위안(약 2,800달러) 상당의 보상판매 보조금이 구매력을 증폭시켜 중산층 가구가 중국 고급차 시장에 진입할 수 있도록 하고 있습니다.

국내 EV 고급 브랜드 확대

국내 유수의 제조업체는 배터리 교체 네트워크, 레벨 2+의 자동 운전 기능, 무선 업데이트를 결합하여 수요를 확보하고 있습니다. NIO는 2024년 22만 1,970대를 인도했고, Li Auto는 출시 5년 만에 연간 인도량 50만 대를 달성했습니다. 이러한 성장은 경쟁의 기반을 내연기관 전통에서 소프트웨어 생태계와 서비스 모델로 전환함으로써 중국 고급차 시장을 재편하고 있습니다.

커넥티드카 관련 데이터 보안 규제

중국의 데이터 보안법은 자동차 제조업체에 차량 생성 데이터의 국내 저장을 의무화하고 있으며, 이는 세계 클라우드 아키텍처를 복제해야 하는 외국 제조업체의 비용을 증가시키고 있습니다. 국경 간 데이터 유통의 제한은 무선 업데이트(OTA) 파이프라인을 복잡하게 만들고, 세계 플랫폼과의 기능 격차를 확대하며, 중국 프리미엄 자동차 시장에서의 차별화를 가로막고 있습니다.

부문 분석

2025년 기준 SUV는 중국 고급차 시장의 63.12%를 차지했으며, 소비자들이 높은 운전석 위치와 가족 친화적인 실내 공간을 선호하는 경향이 두드러졌습니다. NIO ES6, Li Auto L9와 같은 배터리 전기자동차 플래그십 모델들이 쇼룸 방문객을 견인하는 가운데, SUV 서브 부문은 2031년까지 연평균 6.25%의 성장률을 보일 것으로 예상됩니다. 세단은 임원용 운송 수단으로서 위엄을 유지하면서 판매량 증가분은 다세대 가구를 위한 다목적 차량으로 이동하고 있습니다. 광치그룹(GAC)의 레벨 3 자동운전 도입과 Li MEGA의 유연한 좌석 배치, 자동화와 인테리어의 다양성이 새로운 고급 표준을 확립하고 있음을 보여줍니다.

2차적인 영향으로는 지방 도시의 도로 상황에 따라 승차감을 개선하기 위한 롱 휠베이스 섀시 및 적응형 에어 서스펜션 패키지에 대한 수요가 증가하고 있습니다. 해치백은 틈새시장이지만, 특히 교통체증이 심각한 해안 대도시권에서 도심의 주차 공간 제약으로 인한 혜택을 누리고 있습니다. SUV의 선도적 위치는 배터리 교체 보급을 촉진하고 있으며, 대형 차체가 표준화된 모듈을 수용할 수 있기 때문에 중국 고급차 시장 특유의 인프라 네트워크 효과를 강화하고 있습니다.

2025년 판매량에서 내연기관차가 차지하는 비중은 여전히 61.95%로 중국 고급차 시장 규모에서 가장 큰 비중을 차지하고 있습니다. 그러나 구매세 면제, 배터리 비용 감소, 전국적인 충전기 밀도 증가에 힘입어 배터리 전기자동차 모델은 2031년까지 연평균 9.72%의 성장률을 기록할 것으로 예상됩니다. 플러그인 하이브리드 자동차는 주행거리 불안에 대한 헤지 역할을 하며, 연안 지역의 인프라 격차를 해소하는 역할을 합니다. 연료전지차의 시험 도입은 수소 물류 문제로 인해 실험 단계가 계속되고 있으며, 단기적인 영향은 제한적일 것입니다.

배터리 전기자동차의 장점은 첨단 운전 보조 시스템, 몰입형 인포테인먼트, 지속적인 무선 업데이트와 같은 소프트웨어 중심의 가치 제안을 강화하여 내연기관차에서는 실현 불가능한 영역을 개척하고 있습니다. 국내 완성차 업체들은 수직계열화된 파워 일렉트로닉스 공급망을 활용하여 부품 비용 절감과 반도체 국산화 지침에 대응하고 있습니다. 그 결과, 중국 고급차 시장에서 30만 위안-60만 위안 가격대의 전기자동차 브랜드 점유율은 2031년까지 55%를 넘어설 것으로 예상되며, 지위를 중시하는 경영층이 선호하는 터보차저 6기통 세단을 대체할 것으로 전망됩니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액(달러) 및 수량(대수))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05The China luxury car market is expected to grow from USD 125.32 billion in 2025 to USD 131.44 billion in 2026 and is forecast to reach USD 166.86 billion by 2031 at 4.88% CAGR over 2026-2031.

This expansion is underpinned by accelerating electrification, rising disposable income in lower-tier cities, and policy support that favors new-energy vehicles. Demand momentum also stems from consumers who now view premium vehicles as mobile technology platforms, prompting manufacturers to elevate autonomous-driving capabilities and connected-services ecosystems. Competitive intensity has sharpened as domestic electric-luxury brands close traditional technology gaps, while foreign marques localize platforms to safeguard their positions within the China premium car market. Ongoing semiconductor localization and evolving tax regulations will continue to reshape margins, supply-chain strategies, and product-mix decisions across the value chain.

China Luxury Car Market Trends and Insights

Growing Consumer Wealth in Tier-2 and Tier-3 Cities

Household incomes in secondary urban centers are growing annually, outpacing tier-1 growth and spawning a new cohort of premium buyers who view vehicles as status symbols and technology showcases. Domestic brands such as Li Auto delivered 500,508 units in 2024, illustrating how aspirational families embrace large premium SUVs equipped with ADAS. Trade-in subsidies worth up to RMB 20,000 (~USD 2,800 ) have amplified purchasing power, allowing middle-class households to enter the China premium car market.

Expansion of Domestic EV-Luxury Brands

Domestic champions have combined battery-swapping networks, Level 2+ autonomy, and over-the-air upgrades to capture demand. NIO delivered 221,970 vehicles in 2024, and Li Auto reached half a million annual deliveries within five years of launch. Such growth reshapes the China premium car market by shifting the basis of competition from combustion-engine heritage to software ecosystems and service models .

Data-Security Regulation on Connected Vehicles

China's Data Security Law compels automakers to store vehicle-generated data domestically, inflating costs for foreign OEMs that must duplicate global cloud architectures. Limitations on cross-border data flows complicate over-the-air update pipelines, diminishing feature parity with global platforms and restraining differentiation in the China premium car market.

Other drivers and restraints analyzed in the detailed report include:

- L3 Autonomy Features Driving Higher ASP

- NFT-Based Digital Ownership Perks

- Premium Ride-Hailing Curbing Ownership Intent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

SUVs captured 63.12% of the Chinese premium car market 2025, underscoring consumer preference for commanding driving positions and family-oriented interiors. The SUV sub-segment will expand at a 6.25% CAGR through 2031 as battery-electric flagships like the NIO ES6 and Li Auto L9 dominate showroom traffic. Sedans maintain gravitas in executive transport, but incremental volume shifts to versatile multi-purpose vehicles designed for multi-generational households. GAC's forthcoming Level 3 rollout and Li MEGA's flexible seating highlight how automation and interior versatility set new luxury benchmarks.

The second-order effects include a stronger demand for long-wheelbase chassis and adaptive air-suspension packages that enhance ride comfort on variable road quality in lower-tier cities. Hatchbacks remain niche yet benefit from tight urban parking constraints, particularly in coastal megacities where congestion is severe. SUV leadership also advances battery-swapping adoption because larger underbodies accommodate standardized modules, reinforcing infrastructure network effects unique to the Chinese premium car market.

Internal-combustion vehicles still represented 61.95% of the 2025 volume, translating to the most significant current slice of the China premium car market size. Yet battery-electric models will climb at a 9.72% CAGR through 2031, propelled by purchase-tax exemptions, falling battery costs, and growing charger density nationwide. Plug-in hybrids serve as range-anxiety hedges, bridging coastal infrastructure gaps. Fuel-cell pilots remain experimental owing to hydrogen logistics, limiting near-term influence.

Battery-electric leadership amplifies software-centric value propositions-advanced driver-assistance, immersive infotainment, and continuous over-the-air updates-that combustion rivals cannot match. Domestic OEMs leverage vertically integrated power-electronics supply chains to reduce bill-of-materials and comply with chip-localization directives. Consequently, the China premium car market share for electric nameplates in the RMB 300,000-600,000 bracket is projected to exceed 55% by 2031, displacing turbocharged six-cylinder sedans historically favored by status-conscious executives.

The China Luxury Car Market Report is Segmented by Vehicle Body Style (Hatchbacks, Sedans, and More), Powertrain Type (Internal Combustion Engine Vehicles and Electric Vehicles), Brand Origin (Domestic Chinese Brands and Foreign Brands), and Sales Channel (Authorized Dealerships, Company-Owned Stores, and Online Direct-To-Consumer). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Mercedes-Benz Group AG

- BMW Group

- Volkswagen Group (Audi AG)

- Lexus (Toyota Motor Corp.)

- Tesla Inc.

- Zhejiang Geely Holding (Zeekr)

- Dongfeng Motor Company

- China FAW Group (Hongqi)

- NIO Inc.

- Li Auto Inc.

- XPeng Motors

- SAIC-GM (Cadillac)

- GAC Aion

- Infiniti (Nissan Motor Co.)

- Acura (Honda Motor Co.)

- Porsche AG

- Jaguar Land Rover Ltd.

- Lincoln Motor Co. (Ford)

- Rolls-Royce Motor Cars

- Maserati S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Consumer Wealth in Tier-2 and Tier-3 Cities

- 4.2.2 Government NEV Incentives for the Premium Segment

- 4.2.3 Rising Demand for Premiumization and Brand Status

- 4.2.4 Expansion of Domestic EV-Luxury Brands (NIO, Li Auto)

- 4.2.5 L3 Autonomy Features Driving Higher ASP

- 4.2.6 NFT-Based Digital Ownership Perks

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost and Luxury Tax

- 4.3.2 Data-Security Regulation on Connected Vehicles

- 4.3.3 High-End Semiconductor Supply Constraints

- 4.3.4 Premium Ride-Hailing Curbing Ownership Intent

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Body Style

- 5.1.1 Hatchbacks

- 5.1.2 Sedans

- 5.1.3 Sport-Utility Vehicles (SUVs)

- 5.1.4 Multi-purpose Vehicles (MPVs)

- 5.2 By Powertrain Type

- 5.2.1 Internal-Combustion (ICE) Vehicles

- 5.2.2 Electric Vehicles (BEV, PHEV, HEV, FCEV)

- 5.3 By Brand Origin

- 5.3.1 Domestic Chinese Brands

- 5.3.2 Foreign Brands

- 5.4 By Sales Channel

- 5.4.1 Authorized Dealerships

- 5.4.2 Company-Owned Stores

- 5.4.3 Online Direct-to-Consumer

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Mercedes-Benz Group AG

- 6.4.2 BMW Group

- 6.4.3 Volkswagen Group (Audi AG)

- 6.4.4 Lexus (Toyota Motor Corp.)

- 6.4.5 Tesla Inc.

- 6.4.6 Zhejiang Geely Holding (Zeekr)

- 6.4.7 Dongfeng Motor Company

- 6.4.8 China FAW Group (Hongqi)

- 6.4.9 NIO Inc.

- 6.4.10 Li Auto Inc.

- 6.4.11 XPeng Motors

- 6.4.12 SAIC-GM (Cadillac)

- 6.4.13 GAC Aion

- 6.4.14 Infiniti (Nissan Motor Co.)

- 6.4.15 Acura (Honda Motor Co.)

- 6.4.16 Porsche AG

- 6.4.17 Jaguar Land Rover Ltd.

- 6.4.18 Lincoln Motor Co. (Ford)

- 6.4.19 Rolls-Royce Motor Cars

- 6.4.20 Maserati S.p.A.