|

시장보고서

상품코드

1937311

바이오 기반 폴리머 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Bio-based Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

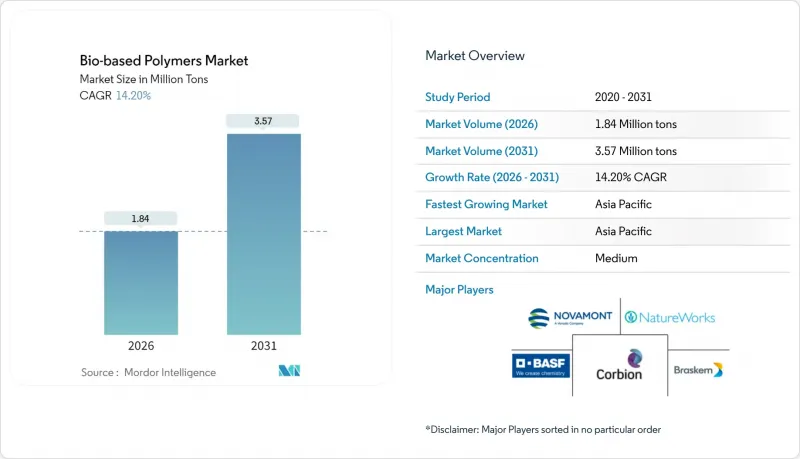

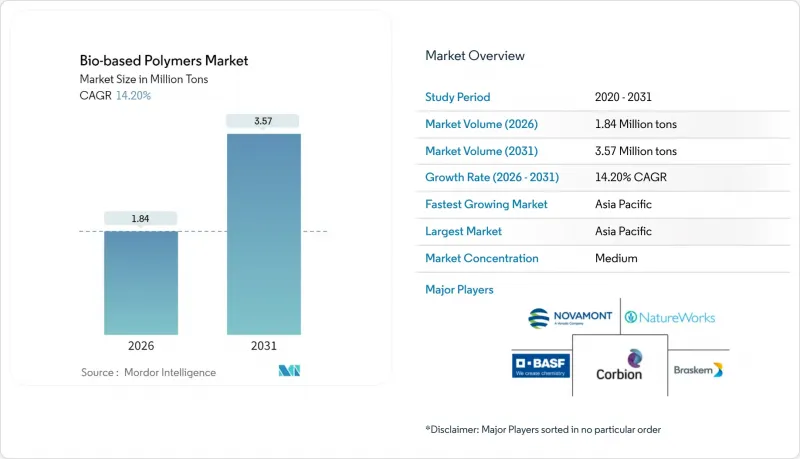

바이오 기반 폴리머 시장은 2025년 161만 톤에서 2026년에는 184만 톤으로 성장하고, 2026년부터 2031년까지 CAGR 14.2%를 기록하며 2031년까지 357만 톤에 달할 것으로 예측됩니다.

이러한 급격한 확대는 일회용 플라스틱 의무화, 빠르게 성숙하는 바이오리파이너리 기술, 기존 설비에서 드롭인 수지를 유통하는 매스밸런스 인증에 기인합니다. 생산자들은 넷 제로 목표를 추구하는 세계 브랜드와 장기적인 오프 테이크 계약을 체결하고 있으며, 이를 통해 금융 관계자들은 신규 설비 투자를 지원할 수 있는 전망을 얻게 되었습니다. 지역별로는 아시아태평양이 농업 잔재물이 저비용 원료를 공급하고 재생 가능한 재료를 장려하는 지역 정책으로 인해 증분 생산량의 대부분을 차지할 것으로 예상됩니다. 내열성 및 생체적합성 개선으로 바이오 기반 폴리머가 범용 포장재를 넘어 의료, 자동차, 전자기기 분야의 프리미엄 부문을 개척하고 있습니다.

세계 바이오 기반 폴리머 시장 동향과 인사이트

규제 주도의 일회용 플라스틱 금지

호주는 2024년 플라스틱 금지 범위를 확대하여 두꺼운 쇼핑백과 폴리스티렌 식품 용기를 금지합니다. 소매업체를 인증된 퇴비화 가능한 재료로 전환했습니다. 유럽연합(EU)에서는 현재 확대된 생산자책임제를 시행하여 각 포장재에 폐기비용을 가격 전가하고 있습니다. 바이오 기반 폴리머 시장과의 비용 차이를 줄이고 있습니다. 캐나다는 2024년 말 연방정부 차원의 플라스틱 금지 조치를 시행하여 재생 가능 포장재에 대한 북미 연속 시장을 형성했습니다. 중국은 폐플라스틱 수입금지에 이어 국내 규제를 강화하여 현지 가공업체에 적합성 있는 재료 조달을 압박하고 있습니다. 선행 도입 사례에서 알 수 있듯이, 금지 조치가 시행되면 가격 프리미엄보다 컴플라이언스 리스크가 더 커지면서 수요가 빠르게 이동합니다.

지속가능한 소재에 대한 소비자 수요 증가

전 세계 조사에 따르면, 구매자의 73%가 구매 결정 시 지속가능성 주장을 고려하고, 인증된 재생 가능 소재에 대해 15-20%의 추가 비용을 지불할 의향이 있는 것으로 나타났습니다. 브랜드 오너들은 이러한 추세를 반영하여, 머스밸런스 인증 원료를 우선적으로 조달하는 조달 규칙에 반영했습니다. 바이오 기반 폴리머 시장의 수익률을 보호하고 있습니다. 외식 체인은 폐기물 감소에 대한 고객의 기대에 부응하여 기존 코팅에서 퇴비화 가능한 필름으로 전환했습니다. B2B 바이어들은 공급업체 점수 카드에 탄소 강도 점수를 포함시켜 화석 유래 플라스틱의 진입장벽을 높이고 있습니다. 이러한 수요 확대는 전자기기와 의류 분야로까지 파급되고 있습니다. 라이프스타일 브랜드들이 재생 소재를 품질의 증거로 삼으려는 움직임이 확산되고 있습니다.

석유 유래 플라스틱과의 비용 비교

바이오 기반 등급은 소규모 공장이 규모의 경제성이 부족하여 화석 유래 대체품에 비해 20-50% 프리미엄 가격으로 판매되고 있습니다. 기존 화학공장과 유틸리티를 공유하면 생산비용을 절감할 수 있지만, 높은 자본집약도가 가격 평준화를 지연시키고 있습니다. 유가 급등은 일시적으로 격차를 좁히지만, 구조적인 차이를 해소하는 것은 아닙니다. 의료기기와 같은 특수 용도의 경우, 생분해성이 규제 부담을 줄여주기 때문에 프리미엄 가격이 인정받고 있습니다. 보다 광범위한 가격 평준화를 위해서는 현재의 생산능력을 두 배로 늘리고 고정비를 더 많은 생산량으로 분산시켜야 합니다.

부문 분석

기타 제품 유형(주로 폴리부틸렌 숙시네이트 및 폴리부틸렌 아디페이트 테레프탈레이트)은 2025년 바이오 기반 폴리머 시장 점유율의 44.12%를 차지했습니다. 생산자는 퇴비화성과 열 밀봉 강도를 겸비한 수지 특성으로 인해 멀티 필름 및 플렉서블 파우치 분야에서 채택을 얻고 있습니다. 이러한 대규모 기반은 전체 특수 등급 바이오 기반 폴리머 시장 규모를 높이고 단계적 병목 현상 해소 프로젝트를 지원하고 있습니다. 아시아 기업들이 숙신산과 아디프산을 현지 원료에 통합함으로써 운송 비용과 환위험이 감소하고 공급 안정성이 향상되었습니다.

폴리락트산(PLA)은 2031년까지 CAGR 18.22%로 성장을 견인할 것입니다. 이 분야는 전자기기 하우징 및 자동차 내장 부품 용도를 개척한 내열성 등급의 등장으로 수혜를 받고 있습니다. 의료 분야의 혁신가들은 PLA의 생체흡수성을 활용하여 치유 후 용해되는 스크류와 플레이트를 설계하여 2차 수술을 피하고 있습니다. 아랍에미리트(UAE)와 태국에서의 생산능력 확대는 규모를 확대하고, 비용 하한선을 낮추며, PLA 응용 분야에서 바이오 기반 폴리머 시장 규모를 확대할 것입니다. 기존에는 1-2개 업체에 국한되었던 기술 라이선싱으로 인해 신규 진입자가 증가하여 경쟁 심화가 예상됩니다.

바이오 기반 폴리머 보고서는 제품 유형별(생분해성 전분 혼합물, 바이오 폴리에틸렌(바이오 PE), 바이오 폴리에틸렌 테레프탈레이트(바이오 PET) 등), 최종사용자 산업별(농업, 의료 및 헬스케어, 포장, 자동차 및 운송, 섬유, 기타), 지역별(아시아태평양, 북미, 유럽, 기타 지역) 북미, 유럽, 기타 지역) 별로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 바이오 기반 폴리머 시장 규모의 44.02%를 차지하며 2031년까지 CAGR 16.63%로 확대될 것으로 예상됩니다. 중국은 세금환급, 그린론, COFCO 등이 운영하는 옥수수에서 폴리머까지 통합단지를 통해 지역 내 주도적인 입지를 구축하고 있습니다. 태국은 바이오화학 투자에 대해 8년간 면세혜택을 적용하고 있으며, 제당공장과 폴리머 제조시설을 겸비한 합작투자를 유치하고 있습니다. 인도는 잉여 사탕수수를 활용하여 국내 폴리머 수요를 보충하는 동시에 다국적 기업에 수출 크레딧을 제공하고 있습니다.

유럽은 '일회용 플라스틱 지침'과 생산자 책임 확대 제도가 결합된 성숙한 정책 조합으로 수요를 뒷받침하고 있습니다. 독일과 프랑스는 회수 비용을 내재화하여 화석 유래 플라스틱의 상대적 비용을 상승시키고, 인증된 생분해성 소재로 전환을 유도하고 있습니다. 산업용 퇴비화 시설은 3,500여 개소에 달하며, 진정한 순환성을 실현하고 있습니다. 지역별 인수 계약을 통해 공급업체는 다년간 가격을 고정할 수 있어 원료 가격 변동에 대한 바이오 기반 폴리머 시장의 안정화를 꾀하고 있습니다.

북미에서는 2032년까지 일회용 플라스틱 포장을 65% 감축하는 캘리포니아주 SB54법 등 주정부 차원의 법령에 의해 가속화되고 있습니다. 캐나다의 연방 금지령은 주정부 간 제품 사양을 통일하고 대륙 규모의 투자 기반을 구축했습니다. 기업 구매자는 공급계약서에 재생가능탄소 할당량을 명시하여 예측 가능한 공급량을 확보하고 있습니다. 다른 지역에서는 신흥 라틴아메리카 설탕 경제권 및 일부 아프리카 국가들이 농업 잔류물이 풍부한 지역에서 도입을 가속화하기 위해 정책 템플릿을 모방하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.12The Bio-based Polymers Market is expected to grow from 1.61 million tons in 2025 to 1.84 million tons in 2026 and is forecast to reach 3.57 million tons by 2031 at 14.2% CAGR over 2026-2031.

The sharp expansion comes from mandatory single-use plastic bans, fast-maturing bio-refinery technologies, and mass-balance certification that allows drop-in resins to flow through existing assets. Producers lock in long-term offtake agreements with global brands pursuing net-zero timelines, giving financiers visibility to support new capacity. Regionally, Asia-Pacific captures much of the incremental tonnage because agricultural residues supply low-cost feedstock and local policies encourage renewable materials. Premium segments open in medical, automotive, and electronics as improved heat resistance and biocompatibility formulations move bio-based polymers beyond commodity packaging.

Global Bio-based Polymers Market Trends and Insights

Regulation-led Bans on Single-use Plastics

Australia widened its plastics prohibition in 2024 to ban heavyweight shopping bags and polystyrene food containers, pushing retailers toward certified compostable options. The European Union now enforces extended producer responsibility that prices end-of-life costs into each package, narrowing the cost gap with the bio-based polymers market. Canada implemented a federal plastics prohibition in late 2024, creating a contiguous North American market for renewable packaging. China tightened domestic restrictions after banning waste plastic imports, forcing local converters to source compliant materials. Early adopters show that once bans enter force, demand shifts quickly because compliance risk outweighs price premiums.

Rising Consumer Demand for Sustainable Materials

Global surveys show that 73% of shoppers weigh sustainability claims in purchase decisions and will pay 15-20% more for verified renewable content. Brand owners translate this signal into procurement rules that favor mass-balance certified feedstocks, protecting margins in the bio-based polymers market. Food service chains swap conventional coatings for compostable films to meet customer expectations on waste reduction. B2B buyers embed carbon intensity scores in supplier scorecards, raising entry barriers for fossil plastics. The demand pull spreads to electronics and apparel as lifestyle brands position renewable materials as a marker of quality.

Higher Cost vs. Petro-plastics

Bio-based grades sell at 20-50% premiums compared with fossil alternatives because smaller plants lack scale efficiencies. Production costs ease when plants share utilities with existing chemical hubs, yet capital intensity delays parity. Price spikes in crude oil narrow the gap temporarily but do not erase structural differences. Specialty uses such as medical devices absorb premiums because biodegradability trims regulatory burdens. Broader parity depends on doubling current capacity so fixed costs spread across more tons.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-zero and Renewable-carbon Sourcing Pledges

- Scale-up of CO2- and Agri-waste-based Biorefineries

- Limited Composting and Recycling Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Other product types, dominated by polybutylene succinate and polybutylene adipate terephthalate, accounted for 44.12% of bio-based polymers market share in 2025. Producers win adoption in mulch films and flexible pouches because these resins combine compostability with heat-seal strength. Their large base lifts the overall bio-based polymers market size for specialty grades and supports incremental debottlenecking projects. Supply security improves as Asian firms integrate succinic acid and adipic acid back to local feedstock, trimming freight and currency risk.

Polylactic acid leads growth at an 18.22% CAGR to 2031. The segment benefits from recent heat-stable grades that unlock electronics housings and automotive trim. Medical innovators exploit PLA's bioresorption to design screws and plates that dissolve after healing, avoiding secondary surgeries. Capacity expansions in the UAE and Thailand add scale and lower cost floors, which enlarges the bio-based polymers market size for PLA applications. Competitive intensity rises as new entrants license technology that had been confined to one or two players.

The Bio-Based Polymers Report is Segmented by Product Type (Biodegradable Starch Blends, Bio Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), and More), End-User Industry (Agriculture, Medical and Healthcare, Packaging, Automotive and Transportation, Textiles, and Others), and Geography (Asia-Pacific, North America, Europe, and Rest of World). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific captured 44.02% of the bio-based polymers market size in 2025 and is expanding at a 16.63% CAGR to 2031. China anchors regional leadership through tax rebates, green loans, and integrated corn-to-polymer complexes run by COFCO and peers. Thailand grants eight-year tax holidays on bio-chemical investments, luring joint ventures that colocate sugar mills with polymer units. India leverages surplus bagasse to backfill domestic polymer demand while exporting credits to multinationals.

Europe supports demand with a mature policy mix that combines the Single-Use Plastics Directive and mandatory extended producer responsibility. Germany and France internalize collection fees that make fossil plastics relatively more expensive, steering converters toward certified compostables. Industrial composting coverage surpasses 3,500 sites, enabling true circularity claims. Regional offtake agreements let suppliers lock multi-year prices, stabilizing the bio-based polymers market against feedstock swings.

North America accelerates through state-level laws such as California's SB 54 that requires a 65% cut in single-use plastic packaging by 2032. Canada's federal ban synchronizes product specifications across provinces, creating a continental platform for investment. Corporate buyers formalize renewable-carbon quotas in supplier contracts, delivering predictable tonnage. Elsewhere, emerging Latin American sugar economies and selected African nations replicate policy templates that fast-track adoption where agricultural residues are plentiful.

- BASF

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Braskem

- Cardia Bioplastics

- CJ CHEIL JEDANG CORP.

- Corbion

- Covestro AG

- Danimer Scientific

- Eastman Chemical Company

- Emirates Biotech

- FKuR

- Futerro

- Mitsubishi Chemical Group Corporation

- NatureWorks LLC

- Novamont S.p.A.

- Rodenburg Biopolymers

- Sulzer Ltd.

- Ukhi India Pvt. Ltd.

- Yield10 Bioscience, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulation-led bans on single-use plastics

- 4.2.2 Rising consumer demand for sustainable materials

- 4.2.3 Corporate net-zero and renewable-carbon sourcing pledges

- 4.2.4 Mass-balance certified drop-in resins adoption

- 4.2.5 Scale-up of CO2- and agri-waste-based biorefineries

- 4.3 Market Restraints

- 4.3.1 Higher cost vs. petro-plastics

- 4.3.2 Limited composting and recycling infrastructure

- 4.3.3 Feedstock price volatility from biofuel mandates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Biodegradable Starch Blends

- 5.1.2 Bio Polyethylene (Bio-PE)

- 5.1.3 Bio-Polyethylene Terephthalate (Bio-PET)

- 5.1.4 Polylactic Acid (PLA)

- 5.1.5 Polyhydroxyalkanoate (PHA)

- 5.1.6 Other Product Types (Polybutylene Succinate (PBS), Polybutylene Adipate Terephthalate (PBAT), etc.)

- 5.2 By End-user Industry

- 5.2.1 Agriculture

- 5.2.2 Medical and Healthcare

- 5.2.3 Packaging

- 5.2.4 Automotive and Transportation

- 5.2.5 Textiles

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BASF

- 6.4.2 Biome Bioplastics

- 6.4.3 BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- 6.4.4 Braskem

- 6.4.5 Cardia Bioplastics

- 6.4.6 CJ CHEIL JEDANG CORP.

- 6.4.7 Corbion

- 6.4.8 Covestro AG

- 6.4.9 Danimer Scientific

- 6.4.10 Eastman Chemical Company

- 6.4.11 Emirates Biotech

- 6.4.12 FKuR

- 6.4.13 Futerro

- 6.4.14 Mitsubishi Chemical Group Corporation

- 6.4.15 NatureWorks LLC

- 6.4.16 Novamont S.p.A.

- 6.4.17 Rodenburg Biopolymers

- 6.4.18 Sulzer Ltd.

- 6.4.19 Ukhi India Pvt. Ltd.

- 6.4.20 Yield10 Bioscience, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment