|

시장보고서

상품코드

1937316

자동차용 알루미늄 압출 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Automotive Aluminium Extrusion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

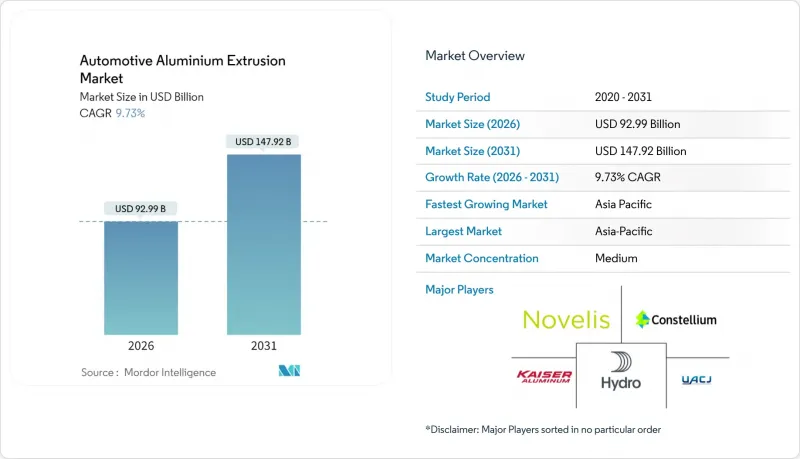

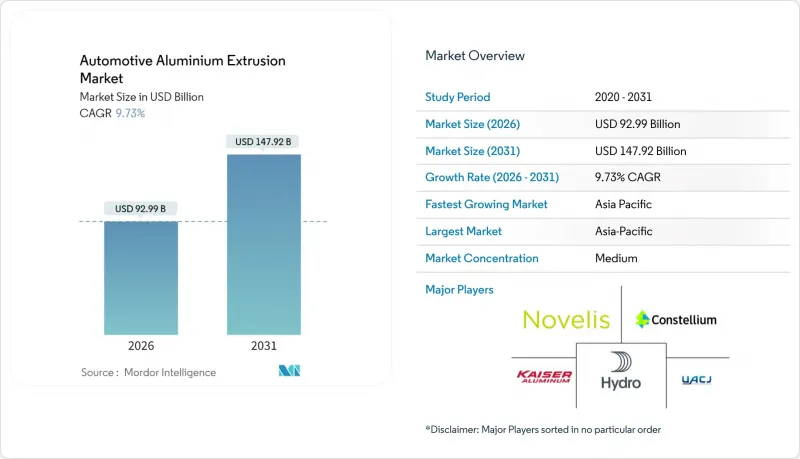

자동차용 알루미늄 압출 시장은 2025년에 847억 5,000만 달러로 평가되었으며, 2026년 929억 9,000만 달러에서 2031년까지 1,479억 2,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 9.73%로 추정됩니다.

수요의 모멘텀은 전기자동차(EV) 플랫폼으로의 전환 가속화에 기인하며, 압출 알루미늄은 경량 바디 인 화이트 구조, 충돌 에너지 흡수 레일, 고효율 배터리용 열 차단 인클로저를 지원하고 있습니다. 합금 화학 및 프레스 기술의 지속적인 개선으로 구조적 무결성을 유지하면서 차량 중량을 줄이는 복잡한 중공 프로파일을 구현할 수 있게 되었습니다. USMCA 규정과 EU의 탄소국경조정메커니즘(CBAM)을 계기로 한 역내 니어쇼어링으로 인해 공급망은 국내 프레스 역량으로 재조정되고 있으며, 북미에서만도 막대한 설비투자가 약속되어 있습니다. 통합 알루미늄 생산업체들이 빌릿 공급을 확보하고 폐쇄형 재활용을 실현하기 위해 업스트림 제련 및 다운스트림 압출 라인을 강화하면서 경쟁이 심화되고 있습니다. 동시에, 전문 1급 제조업체는 복합재료 접합 기술과 정밀 금형 설계를 통해 차별화를 꾀하고 있습니다.

세계 자동차용 알루미늄 압출 시장 동향과 인사이트

미국, EU, 중국의 자동차 CO2 배출 규제와 연비 기준

기업평균연비규제(CAFE)는 2026년까지 미국 차종의 평균 연비를 40.4mpg(약 17.3km/L)로 요구하고 있으며, EU 기준은 2025년까지 CO2 배출량을 95g/km로 고정하고 2035년까지 배출량을 거의 제로에 가깝게 만드는 것을 목표로 하고 있습니다. 중국의 듀얼 크레딧 제도도 마찬가지로 경량 소재를 우대하고, 미준수 시 처벌을 받게 됩니다. 압출 알루미늄은 자동차 제조업체가 배터리 무게를 상쇄하고 수천 달러에 달하는 벌금을 피할 수 있어 비용 효율적인 프리미엄 소재입니다. 예측 가능한 규제 일정을 통해 공급업체는 새로운 금형 및 생산능력에 대한 투자에 대한 확신을 가질 수 있습니다. 검증된 재활용성, 성숙한 충돌 성능 데이터, 확장 가능한 생산성은 마그네슘이나 탄소섬유와 같은 경쟁적인 경량화 옵션에 비해 압출 성형의 우위를 결정짓는 요소입니다.

배터리 열 관리 인클로저에는 복잡한 중공 압출 성형이 필요합니다.

배터리 화학이 허용하는 온도 범위가 좁아짐에 따라 다실 압출 성형품은 구조적 장착부와 액체 냉각 경로를 단일 부품으로 통합하여 접합부 및 누출 지점을 줄입니다. 미래의 고체 배터리는 열을 집중시키기 때문에 판금으로는 대응할 수 없는 냉각 요구가 높아질 것입니다. 일체형 매니폴드는 압력 손실과 무게를 줄이고, 표면처리는 글리콜 환경에서 내식성을 향상시킵니다. 차종별 표준화된 팩 설계를 통해 압출 제조업체는 규모의 경제를 실현하고 우수한 열전도율을 달성할 수 있는 합금 조성을 정제할 수 있습니다. 연속 용접 중공 프로파일은 조립을 단순화하여 EV의 대량 생산을 가능하게 합니다.

대형 EV 프로파일용 35MN 슈퍼 프레스 라인 부족

35MN 이상의 프레스 기계는 자동차 업계 설치 설비 용량의 5분의 1 미만에 불과하지만, EV용 스케이트보드 프레임과 배터리 인클로저에는 이러한 기계가 제공하는 긴 길이의 가공 능력이 필수적입니다. 단일 고톤수 라인의 비용은 5,000만-1억 달러에 달하며, 주문에서 가동까지 최대 3년이 소요되어 공급 대응이 지연됩니다. 설계의 복잡성과 함께 대응 가능한 금형 제조업체의 수는 더욱 제한됩니다. 지역 간 격차는 여전히 존재합니다. 아시아가 설비 대수에서 앞서고 있는 반면, 북미와 유럽의 전기자동차 생산량은 현지 생산능력을 크게 상회하고 있어 고가의 대형 부품을 수입할 수 밖에 없는 상황입니다. 그 결과, OEM 업체들은 대형 프레스 업체들과 다년간의 생산능력 예약 계약을 체결하여 기존의 현물 구매 조달 모델을 변화시키고 있습니다.

부문 분석

배터리 인클로저와 열관리 모듈은 EV용 팩의 보급에 따라 2031년까지 CAGR 9.79%로 가장 높은 성장세를 보일 것으로 예상됩니다. 차체 구조 부품은 2025년 기준 자동차용 알루미늄 압출재 시장 규모의 37.21%를 차지하며, 알루미늄의 충돌 안전성을 뒷받침하는 가장 큰 점유율을 유지하고 있습니다. 자동차 알루미늄 압출 시장은 주조 메가 컴포넌트 주변에 압출 보강 레일을 필요로 하는 기가 캐스팅 기술의 혜택을 누리고 있습니다. 충돌 관리 시스템에서 제어된 변형 특성은 수리 비용을 절감합니다. 외장 트림은 내식성과 고급스러운 마감 가능성으로 안정적인 점유율을 유지하고 있습니다. 시트 프레임 등 내장 모듈은 경량화를 추구하는 고급 부문에서 수요가 증가하고 있습니다.

부품 구성은 냉각, 배선, 구조적 하중 경로를 단일 프로파일에 통합하는 다기능 설계로 진화하고 있습니다. 공급업체는 유한요소해석을 활용하여 벽 두께의 최적화 및 가공 없이 보스부를 내장하는 것을 실현하고 있습니다. 단품의 폐쇄 루프 재활용을 통해 OEM의 재활용 재료 사용률 기준을 충족하고, 구매자와 압출 가공 파트너의 유대를 더욱 강화합니다. 적층 마찰 교반 접합 기술은 열 영향 영역 없이 긴 길이의 압출재를 접합하여 여러 개의 프레스 부품을 대체하는 연속적인 사이드실 어셈블리를 실현합니다. 전기자동차 보급이 가속화됨에 따라 배터리 전용 부품은 틈새에서 주류로 전환되어 전 세계 프레스 공장의 수주 구조를 재편할 것입니다.

승용차는 2025년 생산량의 51.84%를 차지하며 9.80%의 CAGR로 확대될 것으로 예상됩니다. 이는 전체 차종 중 가장 높은 수준으로, 소비자의 전기자동차 도입이 대형 부문에 대한 인프라 구축을 앞지르고 있기 때문입니다. 소형 상용차는 EC 물류 차량이 도심 노선을 전동화하려는 움직임을 따라갈 것입니다. 중대형 트럭은 배터리 에너지 밀도의 제약으로 인해 뒤쳐져 있지만, 메가 와트 충전 기술이 성숙하면 성장 여지가 있습니다. 버스용 알루미늄 압출 소재는 내식성을 향상시켜 대중교통의 라이프사이클 비용 절감에 기여합니다.

승용 EV 프로그램은 내연기관 차종에 비해 차량당 압출재 사용량이 증가하기 때문에 판매량이 정체되어도 단가 수익이 향상됩니다. OEM 플랫폼은 세단, 크로스오버, 해치백 파생 차종에 공통된 압출 서브프레임을 채택하여 규모의 경제를 촉진합니다. 상용차는 적재량을 중요시하기 때문에 압출 성형된 플로어 빔과 루프 보가 프레스 성형 강재를 대신하여 배터리 무게를 상쇄합니다. 규제가 강화되는 가운데, 승용차의 알루미늄 사용량은 공급업체들의 생산능력 계획의 지표가 될 것입니다.

지역별 분석

아시아태평양은 2025년 수요의 39.55%를 차지하며 9.83%의 CAGR로 선두를 유지했습니다. 중국 단독으로 2024년에 높은 수준의 1차 알루미늄을 제련하여 비용 경쟁력 있는 빌렛을 다운스트림 압출 클러스터에 공급했습니다. 국내 전기자동차 판매량은 800만 대를 넘어 현지 수요를 보장하고 있습니다. 일본은 고급 합금의 연구개발에 기여하고, 한국은 자동차 조립에 대한 전문성을 활용하고 있습니다. 보크사이트 광산에서 최종 크러쉬 레일까지 통합하여 리드 타임을 단축하고 비용 변동을 억제합니다.

북미의 성장은 압출 프레스 설비와 재활용 능력에 대한 투자 계획으로 뒷받침되고 있습니다. Novellis의 Bay Minette 공장은 60만 톤의 생산능력을 추가하고, 스크랩 재용해와 완전 통합하여 순환 공급을 실현합니다. 하이드로의 펜실베니아 공장 확장으로 지역 기반 강화. USMCA 원산지 규정과 중국산 압출재에 대한 반덤핑 관세가 국내 점유율을 고수하고 있습니다. 캐나다의 풍부한 수력발전은 빌릿의 탄소발자국을 줄이고, OEM의 지속가능성 약속을 지원합니다.

유럽에서는 에너지 가격 급등과 CBAM(Carbon Border Adjustment Mechanism) 도입으로 인해 기존 제련소가 압박을 받고 있는 반면, 저탄소화 이니셔티브가 촉진되고 있습니다. 노르웨이의 수력발전에 의한 잉곳과 스크랩 원료를 광범위하게 채택하여 비용 상승 압력을 완화합니다. 독일과 스웨덴의 프리미엄 부문 OEM은 기가 캐스트 보강을 위해 고급 중공 프로파일을 지정하여 공급업체가 부가가치 마진을 확보 할 수 있습니다. 재활용 의무화는 추적 가능한 스크랩 순환을 요구하고, 디지털화된 압출 제조업체에게 이익이 되는 데이터가 풍부한 밸류체인을 촉진합니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.12The Automotive Aluminium Extrusion Market was valued at USD 84.75 billion in 2025 and estimated to grow from USD 92.99 billion in 2026 to reach USD 147.92 billion by 2031, at a CAGR of 9.73% during the forecast period (2026-2031).

Demand momentum stems from the accelerated shift to electric vehicle (EV) platforms, where extruded aluminum supports lightweight body-in-white structures, crash-energy absorption rails, and high-efficiency battery thermal enclosures. Continual improvements in alloy chemistry and press technology unlock complex hollow profiles that shave curb weight without sacrificing structural integrity. Regional near-shoring, prompted by USMCA rules and the EU Carbon Border Adjustment Mechanism (CBAM), is realigning supply chains toward domestic press capacity, and capital expenditure commitments exceed a huge amount in North America alone. Competitive intensity rises as integrated aluminum producers fortify upstream smelting with downstream extrusion lines to guarantee billet availability and closed-loop recycling. At the same time, specialized Tier-1 houses differentiate through multi-material joining and precision die design.

Global Automotive Aluminium Extrusion Market Trends and Insights

Fleet CO2 & Fuel-Economy Mandates in the U.S., EU, China

Corporate Average Fuel Economy rules require 40.4 mpg U.S. fleet averages by 2026, while EU standards fix 95 g CO2/km for 2025 and move toward near-zero emissions by 2035 . China's dual-credit system likewise rewards lightweight materials and penalizes non-compliance. Extruded aluminum enables automakers to offset battery weight and avoid multi-thousand-dollar fines, making the material premium cost-effective. Predictable regulation timetables give suppliers confidence to fund new tooling and capacity. Proven recyclability, mature crash performance data, and scalable production tip the balance of extrusion over competing lightweighting options such as magnesium or carbon fiber.

Battery Thermal-Management Enclosures Require Complex Hollow Extrusions

As battery chemistries tolerate narrower temperature windows, multi-chamber extrusions combine structural mounting with liquid-coolant paths in a single part, cutting joints and leak points. Future solid-state batteries concentrate heat, intensifying cooling needs that sheet metal cannot meet. Integrated manifolds lower pressure drop and weight, while surface treatments boost corrosion resistance in glycol environments. Standardized pack designs across vehicle lines allow extrusion houses to realize economies of scale and refine alloy recipes for superior thermal conductivity. Continuous-weld hollow profiles also simplify assembly, enabling high-volume EV production.

Scarcity of More Than 35 MN Press Lines for Large EV Profiles

Presses above 35 MN account for less than one-fifth of installed automotive capacity, yet EV skateboard frames and battery enclosures require the extended lineal lengths these machines provide. A single high-tonnage line costs USD 50-100 million and needs up to three years from order to commissioning, slowing supply response. The design complexity further limits the number of qualified toolmakers. Regional imbalances persist: Asia leads installed base, while North American and European EV output surges past local capability, forcing expensive oversize component imports. Consequently, OEMs sign multi-year capacity reservations with large-press operators, altering traditional spot-buy sourcing models.

Other drivers and restraints analyzed in the detailed report include:

- Near-Shoring of Tier-1 Extrusion Capacity (USMCA, EU-CBAM)

- Rising EV Penetration Accelerates Lightweight Body-In-White Adoption

- LME Aluminum Price Volatility & Supply-Chain Speculation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery enclosures and thermal modules deliver the fastest 9.79% CAGR through 2031 as EV packs proliferate. Body structure elements still generated the largest 37.21% slice of the automotive aluminum extrusion market size in 2025, underscoring aluminum's crash-worthiness. The automotive aluminum extrusion market benefits from gigacasting, which necessitates extruded reinforcement rails around cast mega-components. Controlled deformation characteristics in crash-management systems lower repair costs. Exterior trim maintains a steady share thanks to corrosion resistance and premium finish opportunities. Interior modules like seat frames gain traction in luxury segments that chase every kilogram of savings.

The component mix evolves with multi-functional designs integrating cooling, routing, and structural load paths in a single profile. Suppliers leverage finite-element modeling to optimize wall thickness and incorporate bosses without machining. Closed-loop recycling of off-cuts meets OEM recycled-content quotas, further tying buyers to extrusion partners. Additive friction stir welding joins long extrusions without heat-affected zones, enabling contiguous side-sill assemblies that replace multiple stampings. As EV adoption accelerates, battery-specific components will rise from niche to mainstream, reshaping order books across global presses.

Passenger cars accounted for 51.84% of 2025 volumes and are forecast to grow at a 9.80% CAGR-the highest among vehicle classes-because consumer EV uptake outpaces infrastructure build-out for heavier segments. Light commercial vans follow as e-commerce logistics fleets electrify inner-city routes. Medium and heavy trucks lag due to battery-energy density limits, but present upside once megawatt charging matures. Aluminum extrusions in buses improve corrosion resistance, lowering lifetime operating costs for public transit agencies.

Passenger EV programs feature higher extrusion kilograms per vehicle than combustion variants, driving per-unit revenue growth even in flat volume scenarios. OEM platforms share common extruded sub-frames across sedan, crossover, and hatchback derivatives, boosting economies of scale. Commercial vehicles emphasize payload, so extruded floor beams and roof bows substitute press-formed steel, offsetting battery mass. As regulatory milestones tighten, passenger car aluminum intensity remains the bellwether for supplier capacity planning.

The Automotive Aluminum Extrusion Market Report is Segmented by Component Type (Body Structure, Crash-Management Systems, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Alloy Series (6xxx Heat-Treatable and More), Press Capacity (Less Than or Equal To15 MN, 16-25 MN, 26-35 MN, and More Than 35 MN), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 39.55% of 2025 demand, and its 9.83% CAGR keeps the region in pole position. China alone smelted over a high amount of primary aluminum in 2024, furnishing cost-competitive billet to downstream extrusion clusters. Domestic EV sales exceed 8 million units, guaranteeing local offtake. Japan contributes high-end alloy R&D, while South Korea leverages automotive assembly expertise. Integrating bauxite mines to final crash rails compresses lead times and dampens cost volatility.

North America's growth is supported by announced investments in extrusion presses and recycling capacity. Novelis's Bay Minette mill adds 600,000 tonnes of capacity, fully integrated with scrap re-melt for closed-loop supply. Hydro's Pennsylvania upgrade further embeds regional capability. USMCA rules of origin and antidumping duties on Chinese extrusions fortify the domestic share. Abundant hydropower in Canada cuts billet carbon footprint, supporting OEM sustainability pledges .

Europe's high energy prices and CBAM implementation squeeze legacy smelters but stimulate low-carbon initiatives. Norwegian hydro-powered ingot and broader adoption of scrap feedstock mitigate cost headwinds. Premium-segment OEMs in Germany and Sweden specify advanced hollow profiles for gigacast reinforcement, enabling suppliers to command value-added margins. Recycling mandates demand traceable scrap loops, promoting data-rich supply chains that reward digitalized extruders.

- Constellium SE

- Novelis Inc.

- Norsk Hydro ASA

- Kaiser Aluminum Corp.

- UACJ Corp.

- Arconic Corp.

- Kobe Steel Ltd.

- Benteler International

- Bonnell Aluminum

- Hindalco Industries Ltd.

- Guangdong Hongtu

- ETEM Automotive

- Talco Aluminium Company

- Granges AB

- Press-Metal Aluminium

- Sapa Extrusions

- Exlabesa

- Walter Klein GmbH

- Omnimax International

- Innoval Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fleet Co2 & Fuel-Economy Mandates In US, EU, China

- 4.2.2 Battery Thermal-Management Enclosures Require Complex Hollow Extrusions

- 4.2.3 Near-Shoring Of Tier-1 Extrusion Capacity (USMCA, EU-CBAM)

- 4.2.4 Rising EV Penetration Accelerates Lightweight Body-In-White Adoption

- 4.2.5 Cost-Out & Scrap-Recycling Gains From Closed-Loop Extrusion Lines

- 4.2.6 Gigacasting-Extrusion Hybrid Chassis Architectures In Premium EVs

- 4.3 Market Restraints

- 4.3.1 Scarcity Of More Than 35 Mn Press Lines For Large EV Profiles

- 4.3.2 LME Aluminum Price Volatility & Supply-Chain Speculation

- 4.3.3 Engineering Plastics & CFRP Alternatives For Interiors

- 4.3.4 EU-CBAM & Regional Carbon-Tax Pass-Through Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Component Type

- 5.1.1 Body Structure

- 5.1.2 Crash-Management Systems

- 5.1.3 Battery Enclosures and Thermal Modules

- 5.1.4 Exterior Trim and Roof Rails

- 5.1.5 Interior Modules

- 5.1.6 Other Components

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy-Duty Trucks

- 5.2.4 Buses and Coaches

- 5.3 By Alloy Series

- 5.3.1 6xxx Heat-Treatable

- 5.3.2 7xxx High-Strength

- 5.3.3 5xxx Non-Heat-Treatable

- 5.3.4 Scandium & Novel Alloys

- 5.4 By Press Capacity

- 5.4.1 Less than or equal to 15 MN

- 5.4.2 16-25 MN

- 5.4.3 26-35 MN

- 5.4.4 More than 35 MN

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Constellium SE

- 6.4.2 Novelis Inc.

- 6.4.3 Norsk Hydro ASA

- 6.4.4 Kaiser Aluminum Corp.

- 6.4.5 UACJ Corp.

- 6.4.6 Arconic Corp.

- 6.4.7 Kobe Steel Ltd.

- 6.4.8 Benteler International

- 6.4.9 Bonnell Aluminum

- 6.4.10 Hindalco Industries Ltd.

- 6.4.11 Guangdong Hongtu

- 6.4.12 ETEM Automotive

- 6.4.13 Talco Aluminium Company

- 6.4.14 Granges AB

- 6.4.15 Press-Metal Aluminium

- 6.4.16 Sapa Extrusions

- 6.4.17 Exlabesa

- 6.4.18 Walter Klein GmbH

- 6.4.19 Omnimax International

- 6.4.20 Innoval Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment