|

시장보고서

상품코드

1937328

탄화규소 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Silicon Carbide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

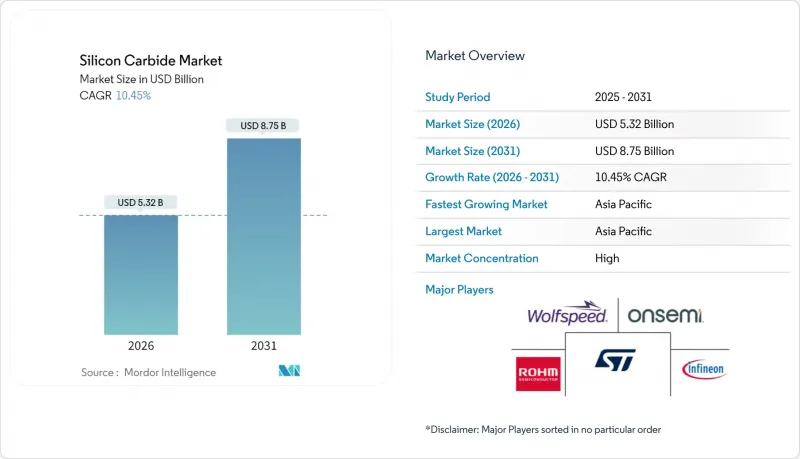

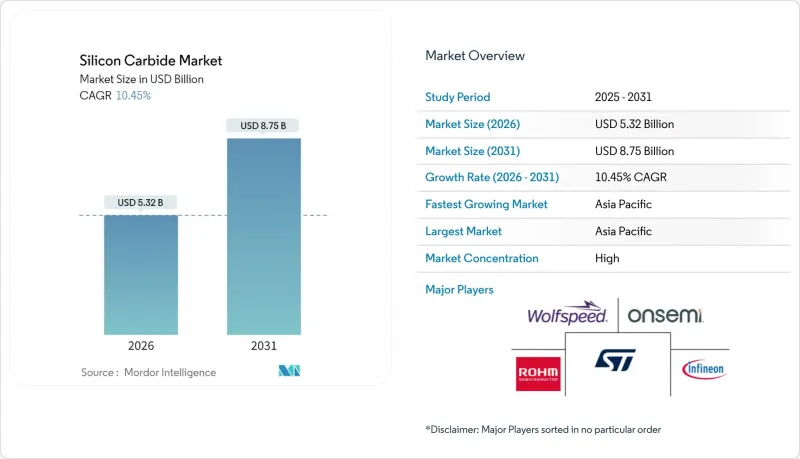

2026년 탄화규소 시장 규모는 53억 2,000만 달러로 추정되며, 2025년 48억 2,000만 달러에서 성장하여 2031년에는 87억 5,000만 달러에 달할 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR)은 10.45%에 달할 것으로 예상됩니다.

이러한 성장 모멘텀은 200mm 웨이퍼로의 전환에서 비롯되었습니다. 인피니언이 2025년 2월에 처음 실현한 이 기술은 기판당 칩 생산량을 거의 두 배로 늘리고 단가를 낮출 수 있습니다. 전기자동차(EV) 제조업체의 800V 아키텍처로의 전환, 재생에너지용 인버터의 98% 효율화 추구, 데이터센터 운영자의 냉각 비용 25-40% 절감 목표가 수요 확대를 더욱 가속화하고 있습니다. 정부의 지원책이 성장을 가속화하고 있습니다. 미국의 CHIPS법에서는 Wolfspeed사의 노스캐롤라이나 공장에 7억 5,000만 달러가 지원되었고, 유럽의 CHIPS법에서는 ST마이크로일렉트로닉스의 이탈리아 공장에 50억 유로가 배분되어 지역 내 공급 안정성이 강화되었습니다. 아시아태평양은 규모의 우위를 유지하고 있지만, 서방 국가들의 주권 확보를 위한 노력이 공급망 지도를 재구성하고 있습니다. 한편, 양자 포토닉스 연구가 파워 일렉트로닉스 이외의 새로운 분야에서 탄화규소 시장의 가능성을 열어주고 있습니다.

세계 탄화규소 시장 동향 및 인사이트

파워 일렉트로닉스 분야 수요 급증

자동차 제조사들이 800V 구동 시스템으로 전환하는 가운데, 온세미의 EliteSiC M3e 제품군에서 알 수 있듯이 100kHz 이상의 스위칭이 가능한 SiC MOSFET이 요구되고 있습니다. 이 제품은 기존 노드 대비 턴오프 손실을 절반으로 줄였습니다. 인피니언의 1200V CoolSiC 디바이스는 추가 절연 없이 900V 이상의 충전기 작동을 가능하게 하여 EV 플랫폼의 보급을 가속화하고 있습니다. 데이터센터 사업자들은 SiC 기반 정류기가 변환 효율을 98%까지 향상시켜 냉각 비용을 25-40% 절감했다고 보고하고 있습니다. 이러한 사용 사례가 결합되어 2050년까지 웨이퍼 수요는 실리콘 기판과 동등한 수준에 도달할 것으로 예상됩니다. 산업용 모터 구동 장치, 철도 견인 시스템, 서버 전원공급장치가 고주파 영역에서 실리콘 IGBT를 능가하는 광대역 갭 솔루션으로 전환함에 따라 탄화규소 시장은 지속적으로 확대되고 있습니다.

재생에너지 분야에서의 활용 확대

Fraunhofer ISE의 3.3kV SiC 트랜지스터는 중전압 계통에 직접 연결 가능한 98.4% 효율의 태양광 인버터를 구현하여 대형 변압기가 필요 없는 태양광 인버터를 구현합니다. 태양광발전 설비에서 실리콘 다이오드 대비 시스템 효율이 2% 향상되고, 에너지 손실이 70% 감소. 풍력 터빈에서는 SiC의 열전도율을 활용하여 추가 냉각 없이 200℃의 로터측 온도에 대응할 수 있습니다. SiC 기반의 양방향 컨버터는 수요 피크 시 네트워크를 안정화시키는 V2G(차량에서 전력망으로) 체계를 지원합니다. 분산형 발전을 의무화하는 유럽의 정책 프레임워크는 고성능 인버터에 대한 수요를 가속화하여 탄화규소 시장의 장기적인 성장 모멘텀을 유지하고 있습니다.

변동하는 원자재 비용

웨이퍼 원자재 비용은 SiC 디바이스 비용의 55-70%를 차지합니다. 에너지 집약적인 에이치체슨법은 2,000℃ 이상에서 가동되고 1kg당 10.5-13kWh를 소비하기 때문에 전력 가격의 급등은 현금 비용에 직접적으로 반영됩니다. 2024년 러시아-우크라이나 사태로 인한 공급 차질로 원료 조달이 어려워지고, 중국의 환경 규제로 인해 전 세계 금속 실리콘 생산량의 70%가 주기적으로 생산이 중단되고 있습니다. 200mm 결정으로 대형화하려면 새로운 용광로와 CVD 반응기가 필요하며, 자본 부담이 증가합니다. Susteon의 파일럿 재활용 기술은 메탄 열분해를 통해 원료 비용을 kg당 10-20달러로 낮추고 CO2 배출량을 75%까지 줄일 수 있을 것으로 예상되지만, 상용화까지는 몇 년이 걸릴 것으로 예상됩니다.

부문 분석

흑색 SiC는 낮은 제조 비용과 연마재, 내화물 및 야금 첨가제에 대한 적합성으로 인해 2025년 매출의 41.56%를 차지했습니다. 흑색 탄화규소 시장 규모는 규모의 경제를 실현하는 대형 아체슨 용광로의 혜택을 받고 있습니다. 그린 SiC는 생산량은 적지만 파워 디바이스 및 양자 포토닉스 공장의 고순도 수요 증가에 따라 13.05%라는 가장 높은 CAGR을 기록했습니다. ST마이크로일렉트로닉스가 노르셰이핑 공장에서 200mm 그린 SiC 웨이퍼로 전환하면서 슬라이스당 다이 생산량이 거의 두 배로 증가하여 스케일업의 이점을 보여주었습니다.

장치 제조업체는 녹색 SiC에 프리미엄을 지불합니다. 이는 낮은 결함 밀도로 인해 칩 수율이 향상되고, 현장 서비스에서 평균 고장 간격(MTBF)이 길어지기 때문입니다. 전기자동차(EV) 및 재생에너지용 인버터 보급에 따라 생산 학습 곡선을 통해 블랙 SiC와의 가격 차이가 축소될 것으로 예상되며, 탄화규소 시장 내 잠재적 수익 기반이 확대될 것으로 예상됩니다. 특수 야금 및 세라믹 변종은 내산성과 내열 충격 안정성을 중시하는 석유화학, 항공우주, 방위 산업 분야의 틈새시장을 공략하고 단일 부문의 변동성 위험을 완화하는 견고한 제품 라인을 뒷받침합니다.

본 탄화규소 보고서는 제품 유형별(블랙 SiC, 그린 SiC, 기타 제품), 용도별(철강제조, 에너지, 자동차, 항공우주/방위 산업, 전자/반도체, 기타 용도), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류하여 조사하였습니다. 시장 예측은 금액 기준(USD)으로 제공됩니다.

지역별 분석

아시아태평양은 2025년 전 세계 매출의 52.12%를 차지하며 11.96%의 CAGR로 성장하고 있습니다. 이는 광동천우반도체, 한천과기 등 중국에서 진행 중인 28개의 웨이퍼 프로젝트가 뒷받침하고 있습니다. 한국의 IDM 기업들은 현대자동차와 기아자동차에 SiC 공정 노드를 추가하고, 대만의 파운드리 클러스터는 팹리스 반도체 제조업체에 유연한 생산능력을 제공하고 있습니다. 인도는 RIR 파워 일렉트로닉스가 오디샤 주에 6억 2,000만 달러를 투자하여 국내 최초로 전용 라인을 건설하면서 탄화규소 시장에 진출했습니다.

북미에서는 CHIPS 법에 따라 527억 달러의 특혜가 결정 성장부터 모듈 조립까지를 포괄하고 있습니다. 울프스피드의 노스캐롤라이나 공장은 세계 최대 규모의 SiC 소재 시설로, 보쉬의 캘리포니아 공장은 2026년 자동차 프로그램을 위한 200mm 웨이퍼 생산을 준비하고 있습니다. 테슬라와 GM이 지역 수요를 지원하고, 캐나다는 고순도 석영 원료를 공급하고, 멕시코는 조립 클러스터가 발전하고 있습니다.

유럽에서는 430억 유로(약 502억 3,000만 달러) 규모의 유럽판 칩스법을 통해 2030년까지 유럽 대륙의 반도체 점유율을 두 배로 늘리는 것을 목표로 하고 있습니다. 인피니언은 비용 효율화를 위해 오스트리아의 프론트엔드 생산능력을 말레이시아의 백엔드 라인으로 보완하여 비용 효율성을 높였습니다. 폭스바겐, BMW, 스텔란티스는 다년간의 오프 테이크 계약을 체결했습니다. 중동 및 아프리카의 소규모 시장에서는 유틸리티 규모의 태양광발전소 및 석유화학 히터용 SiC 디바이스를 수입하고 있으며, 공급은 유럽 및 아시아 OEM 제조업체에 의존하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.12Silicon Carbide Market size in 2026 is estimated at USD 5.32 billion, growing from 2025 value of USD 4.82 billion with 2031 projections showing USD 8.75 billion, growing at 10.45% CAGR over 2026-2031.

Momentum originates from the shift to 200 mm wafers, first realized by Infineon in February 2025, which nearly doubles chip output per substrate and lowers unit costs. Demand gains are sharpened by electric-vehicle (EV) makers migrating to 800 V architectures, renewable-energy inverters seeking 98% efficiency, and data-center operators targeting 25-40% cooling cost cuts. Government incentives amplify growth: the U.S. CHIPS Act granted USD 750 million to Wolfspeed's North Carolina plant, while the European Chips Act allocated EUR 5 billion to STMicroelectronics' Italian fab, bolstering regional supply security. Asia-Pacific retains scale advantages, yet Western sovereignty initiatives are redrawing supply-chain maps even as quantum-photonic research opens new, non-power electronics horizons for the silicon carbide market.

Global Silicon Carbide Market Trends and Insights

Surging Demand from Power Electronics

Automotive OEMs transitioning to 800 V drivetrains now specify SiC MOSFETs capable of switching above 100 kHz, as shown by onsemi's EliteSiC M3e family that halves turn-off losses versus prior nodes. Infineon's 1200 V CoolSiC devices enable chargers operating beyond 900 V without extra insulation, accelerating EV platform adoption. Data-center operators report 25-40% cooling savings when SiC-based rectifiers lift conversion efficiency to 98%. Together, these use cases push wafer demand toward parity with silicon substrates by 2050. The silicon carbide market continues to broaden as industrial motor drives, rail traction, and server power supplies migrate to wide-band-gap solutions that outclass silicon IGBTs at high frequencies.

Increasing Utilization in Renewable Energy

Fraunhofer ISE's 3.3 kV SiC transistors deliver 98.4% efficient solar inverters that connect directly to medium-voltage grids, eliminating bulky transformers. Solar installations achieve 2% additional system efficiency and 70% lower energy losses versus silicon diodes, while wind turbines use SiC's thermal conductivity to handle 200 °C rotor-side temperatures without extra cooling. Bidirectional converters built on SiC underpin vehicle-to-grid schemes that stabilize networks during peak demand. European policy frameworks mandating distributed generation intensify pull for high-performance inverters, sustaining long-term momentum for the silicon carbide market.

Fluctuating Cost of Raw Materials

Wafer inputs form 55-70% of the SiC device cost. The energy-intensive Acheson route runs above 2,000 °C and consumes 10.5-13 kWh per kg, so power-price spikes feed straight into cash costs. Russian-Ukrainian supply disruptions tightened feedstock availability in 2024, while Chinese environmental curbs periodically idle 70% of global silicon metal output. Upsizing to 200 mm crystals demands fresh furnaces and CVD reactors, adding capital strain. Pilot recycling flows from Susteon promise 75% CO2 cuts and USD 10-20 per kg feedstock via methane pyrolysis, though commercialization sits years away.

Other drivers and restraints analyzed in the detailed report include:

- Fast Adoption of SiC Ceramics in Extreme-Temperature Equipment

- Government Incentives for Wide-Bandgap fabs

- Availability of Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Black SiC retained 41.56% of 2025 revenue due to its lower manufacturing costs and suitability for abrasives, refractories, and metallurgical additives. The silicon carbide market size for black grades benefits from large Acheson furnaces that achieve economies of scale. Green SiC, though smaller in volume, embodies the highest 13.05% CAGR as high-purity demand rises from power-device and quantum-photonic fabs. STMicroelectronics' switch to 200 mm green-SiC wafers in Norrkoping nearly doubles die output per slice, illustrating scale-up benefits.

Device makers pay premiums for green SiC because lower defect densities translate to higher chip yields and longer mean-time-to-failure in field service. As EV and renewable inverters proliferate, production learning curves are forecast to narrow the price gap versus black SiC, enlarging addressable revenue pools inside the silicon carbide market. Specialized metallurgical and ceramic variants serve petrochemical, aerospace, and defense niches that value oxidation resistance and thermal shock stability, supporting a robust product spectrum that cushions suppliers against single-segment volatility.

The Silicon Carbide Report is Segmented by Product Type (Black Silicon Carbide, Green Silicon Carbide, and Other Products), Application (Steel Manufacturing, Energy, Automotive, Aerospace and Defense, Electronics and Semiconductors, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 52.12% of global revenue in 2025 and expands at a 11.96% CAGR, sustained by 28 active Chinese wafer projects spanning Guangdong Tianyu Semiconductor and Hantian Technology. South Korean IDMs add SiC process nodes to serve Hyundai and Kia, while Taiwan's foundry cluster offers flexible capacity to fabless chipmakers. India entered the silicon carbide market when RIR Power Electronics invested USD 620 million in Odisha, building the country's first dedicated line.

North America benefits from USD 52.7 billion in CHIPS Act incentives that cover everything from crystal growth to module assembly. Wolfspeed's North Carolina site will be the world's largest SiC materials facility, and Bosch's California fab readies 200 mm wafers for 2026 automotive programs. Tesla and GM anchor regional demand while Canada supplies high-purity quartz feedstock and Mexico evolves assembly clusters.

Europe advances through a EUR 43 billion (~USD 50.23 billion) Chips Act aimed at doubling the continental semiconductor share by 2030. Infineon augments Austrian front-end output with Malaysian back-end lines for cost efficiency, while Volkswagen, BMW, and Stellantis lock multi-year offtake contracts. Smaller Middle East and African markets import SiC devices for utility-scale solar farms and petrochemical heaters, relying on European and Asian OEMs for supply.

- Blasch Precision Ceramics, Inc.

- Christy Refactories

- CoorsTek Inc.

- CUMI EMD.

- Elkem ASA

- ESD-SIC

- Imerys

- Infineon Technologies AG

- Kymera International

- Morgan Advanced Materials

- Navarro SiC

- NGK INSULATORS, LTD.

- ROHM Co., Ltd.

- Saint-Gobain

- Schunk Ingenieurkeramik

- Semiconductor Components Industries, LLC

- Semiconductor Components Industries, LLC (onsemi)

- STMicroelectronics

- Tateho Chemical

- Washington Mills

- Wolfspeed, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand from Power-Electronics

- 4.2.2 Incresing Utilization in Renewable Energy

- 4.2.3 Fast Adoption of SiC Ceramics in Extreme-Temperature Equipment

- 4.2.4 Government incentives for wide-band-gap fabs

- 4.2.5 Growing Usage in Aerospace and Defence Industry

- 4.3 Market Restraints

- 4.3.1 Fluctuating Cost of Raw Materials

- 4.3.2 Availability of Substitues

- 4.3.3 Tight particulate-emission norms for SiC grinding plants

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Black Silicon Carbide

- 5.1.2 Green Silicon Carbide

- 5.1.3 Other Products (Metallurgical-grade SiC, etc.)

- 5.2 By Application

- 5.2.1 Steel Manufacturing

- 5.2.2 Energy

- 5.2.3 Automotive

- 5.2.4 Aerospace and Defense

- 5.2.5 Electronics and Semiconductors

- 5.2.6 Other Applications (Industrial Manufacturing, Abrasives and Ceramics, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Indonesia

- 5.3.1.7 Vietnam

- 5.3.1.8 Malaysia

- 5.3.1.9 Philippines

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Turkey

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 South Africa

- 5.3.5.5 Nigeria

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Blasch Precision Ceramics, Inc.

- 6.4.2 Christy Refactories

- 6.4.3 CoorsTek Inc.

- 6.4.4 CUMI EMD.

- 6.4.5 Elkem ASA

- 6.4.6 ESD-SIC

- 6.4.7 Imerys

- 6.4.8 Infineon Technologies AG

- 6.4.9 Kymera International

- 6.4.10 Morgan Advanced Materials

- 6.4.11 Navarro SiC

- 6.4.12 NGK INSULATORS, LTD.

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 Saint-Gobain

- 6.4.15 Schunk Ingenieurkeramik

- 6.4.16 Semiconductor Components Industries, LLC

- 6.4.17 Semiconductor Components Industries, LLC (onsemi)

- 6.4.18 STMicroelectronics

- 6.4.19 Tateho Chemical

- 6.4.20 Washington Mills

- 6.4.21 Wolfspeed, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Growing Innovation in High Frequency and Quantum Tech Applications