|

시장보고서

상품코드

1937332

트리니트로톨루엔(TNT) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Trinitrotoluene (TNT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

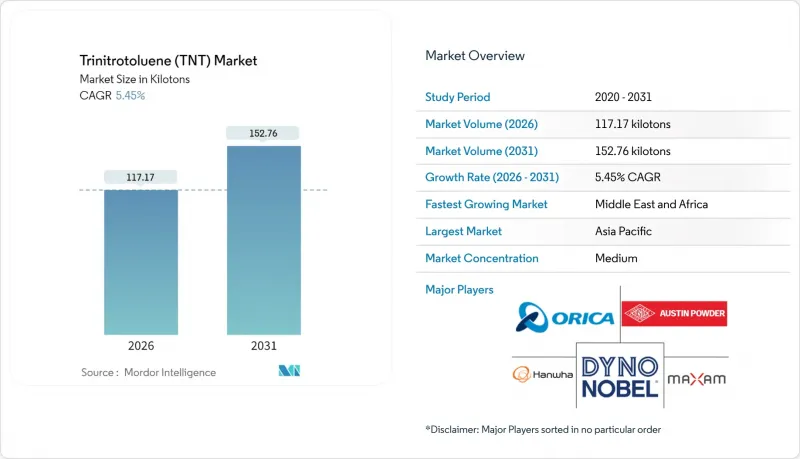

트리니트로톨루엔(TNT) 시장 규모는 2026년에는 117.17 킬로톤으로 추정되고 있습니다.

이는 2025년 111.12 킬로톤에서 성장한 수치이며, 2031년에는 152.76 킬로톤에 달할 것으로 예측됩니다. 2026년부터 2031년까지 CAGR 5.45%로 성장할 것으로 예상됩니다.

미국의 군사 분야의 국내 복귀, 경암광업의 견조한 수요, 톨루엔 원료 가격의 전년 대비 하락으로 인한 투입 비용의 완화가 현재의 성장 모멘텀을 뒷받침하고 있습니다. 40년간의 미국 수입 의존도가 높아지면서 공급망 보안에 대한 필요성이 대두되었고, 1986년 이후 처음으로 국내 TNT 시설 건설 계약이 체결되었습니다. 광업 분야에서는 수분 포화 시추공이나 심부 광석 채굴에서 흡습성 ANFO 배합제를 능가하는 성능을 가진 TNT 부스터가 선호되는 경향이 있습니다. 이러한 기본적인 촉진요인으로 인해 북미와 유럽의 환경적 역풍에도 불구하고 트리니트로톨루엔 시장은 꾸준히 확대될 것으로 예상됩니다.

세계 트리니트로톨루엔(TNT) 시장 동향과 인사이트

경암 채굴에서 폭발물 수요 증가

중국의 희토류 광산에서는 포화 시 에너지를 잃는 ANFO와 달리 기폭 속도를 유지할 수 있는 특성으로 인해 TNT로의 전환이 진행되고 있습니다. 이러한 추세는 호주의 리튬 경암 채굴 사업, 특히 그린부쉬와 필바라 지역에서도 확인되었으며, 현재 고실리카 광석의 에멀전 기둥 기폭에 TNT 부스터가 우선적으로 채택되고 있습니다. 한편, 인도에서는 솔라 인더스트리즈(Solar Industries)가 2024년 신공장을 가동하여 국내 석탄광업과 수출용 광업 수요를 모두 충족시킬 예정입니다. 광맥이 1,500m 이상 깊이 파내려가면서 수압이 증가함에 따라 TNT의 중요성이 더욱 커지고 있습니다. 그 결정 구조는 ANFO의 점화 불량을 유발하는 일반적인 문제인 고밀도화에 대한 내성을 제공합니다.

세계 국방 현대화 및 비축

중국은 2024년 국방예산을 거액으로 책정했고, 일본도 사상 최대 규모의 예산을 승인했습니다. 양국은 탄약 비축, 특히 TNT 충전 포탄의 비축을 중시하고 있습니다. 미 육군이 2031년까지 TNT의 연간 조달을 지속한다는 방침은 장기적인 조달 전략을 뒷받침하고 있습니다. 공급 부족을 보여주는 사례로 폴란드 Nitro-Chem사가 잠정 계약으로 미국 고객에게 TNT를 수출하고 있어 국내 생산이 확대될 때까지의 공급 공백이 부각되고 있습니다. 우크라이나에서 포병 사용이 급증함에 따라 NATO는 튀르키예와 한국의 생산능력 확대를 지원했습니다. 또한, STANAG 4170의 감도 감소 탄약 가이드라인을 준수함으로써 TNT-RDX 혼합물에 대한 수요가 증가하고 있습니다.

엄격한 환경 및 노동 규제

미국 환경보호청(EPA)이 제안한 폐쇄형 폐수처리 시스템은 생산비용 증가 요인이 될 수 있습니다. 미국 에너지부(DOE)는 공기 중 TNT 증기 농도 상한선을 엄격하게 적용하고, 환기 설비의 개보수를 요구하고 있습니다. 인도에서는 PESO가 2년마다 감사 제도를 도입하여 미준수 기업에 벌금을 부과하고 있습니다. REACH 규정에 따른 새로운 독성 시험 확대 의무는 유럽 전역의 소규모 생산자들에게 압박을 가하고 있습니다.

부문 분석

2025년 시장 규모의 71.62%를 군용이 차지하여 트리니트로톨루엔 시장에서 군용 비축이 얼마나 중요한지 알 수 있습니다. 미국 정부는 2025년 예산안에서 일반 탄약에 많은 예산을 책정하고 있으며, TNT 충전 탄약은 이 지출의 중요한 부분을 차지합니다. 이러한 재정적 약속은 군수 수요가 트리니트로톨루엔 시장 규모 형성에 있어 매우 중요한 역할을 하고 있다는 것을 뒷받침하며, 2030년까지 지속가능한 공급망의 필요성을 강조하고 있습니다. 또한, 이 부문이 NATO STANAG 4439 표준을 준수하는 것은 진입장벽을 높일 뿐만 아니라 프리미엄 가격을 유지하는 데에도 기여하고 있습니다.

광업 부문은 CAGR 5.88%로 가장 빠르게 성장하고 있습니다. 이러한 급격한 성장은 주로 심부 광석 채굴에서 ANFO(암모니아 질산염)의 오발화를 허용하지 않는 업계의 엄격한 기준에 기인합니다. 2024년, 중국의 희토류 생산에 대량의 TNT 부스터가 사용되었습니다. 이러한 소비율을 감안할 때, 2030년까지 트리니트로톨루엔 시장에서 광업 부문의 점유율이 확대될 것으로 예상됩니다. 건설 및 특수 용도는 전체 시장 규모에서 작은 비중을 차지하지만, 도시 터널 공사의 엄격한 진동 제한으로 인해 미충족 수요 영역이 부각되고 있습니다. 특히, 전자기폭장치와 TNT 카트리지의 병용을 소유자가 의무화하는 프로젝트에서 두드러집니다. 이러한 다양한 용도를 통해 트리니트로톨루엔 산업의 성장 궤적은 비용 압박과 성능 기대치의 미묘한 균형에 의해 형성되고 있습니다.

트리니트로톨루엔(TNT) 시장 보고서는 용도별(군사, 광업, 건설, 기타 용도) 및 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 기준 트리니트로톨루엔 시장의 46.02%를 차지했으며, 중국의 일대일로 구상과 인도의 방산장비 조달 확대가 이를 뒷받침하고 있습니다. 국내 수요의 두드러진 사례로, Solar Industries는 국방 관련 매출이 크게 증가했다고 보고했습니다. 일본의 전례 없는 예산 규모가 TNT 수요를 견인하고 있으며, 일본유화공업주식회사(NOF)의 일본 자위대와의 계약이 그 증거입니다. 한편, 인도네시아와 베트남의 광산에서는 습식 및 고실리카 함유 광상에서의 TNT 부스터 채택이 증가하고 있으며, 이는 아시아태평양의 시장 전망을 더욱 확고히 하고 있습니다.

북미의 성장은 2026년 말까지 연간 대량 생산을 시작할 예정인 미국 신공장이 견인할 것입니다. 이러한 움직임은 폴란드와 튀르키예로부터의 수입 의존도를 낮추기 위한 것입니다. 캐나다에서는 탄약 비축량이 급증하면서 지역 수요를 불러일으켰습니다. 그러나 중소기업은 새로운 EPA 규제로 인한 재정적 부담에 직면해 있습니다.

유럽에서는 REACH 규제가 강화되면서 유화폭약으로의 전환이 진행 중입니다. 그러나 영국 태스크포스 KINDRED의 우크라이나 지원을 위한 폴란드산 TNT 조달 사례는 여전히 지속적인 의존성을 보여주고 있습니다. 스위스 및 알프스 산맥의 터널에서 TNT는 여전히 정밀 폭파에 필수적입니다. 그러나 신규 진입 기업은 서류마다 부과되는 고액의 규제 수수료를 감당해야 합니다. 남미에서는 습하고 고지대라는 조건으로 알려진 리튬 삼각지대 및 동광대 광산에서 TNT가 선호되고 있습니다. 또한 브라질의 인프라 프로젝트가 현물 수요를 견인하는 한편, IBAMA의 인허가 지연이라는 과제에 직면해 있습니다.

중동 및 아프리카에서는 2031년까지 CAGR 5.65%가 예상되며, 사우디아라비아의 질산암모늄 투자가 활용되고 있습니다. 오리카, MAXAM과의 서비스 계약에 따른 이러한 투자가 물량 증가를 견인하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05The Trinitrotoluene (TNT) Market size in 2026 is estimated at 117.17 kilotons, growing from 2025 value of 111.12 kilotons with 2031 projections showing 152.76 kilotons, growing at 5.45% CAGR over 2026-2031.

Military reshoring in the United States, resilient demand from hard-rock mining, and input-cost relief from a year-on-year drop in toluene feedstock prices underpin current momentum. Supply-chain security imperatives emerged after four decades of U.S. import dependence, prompting a contract for the first domestic TNT facility since 1986. In mining, water-saturated boreholes and deep-ore extraction often favor TNT boosters that outperform hygroscopic ANFO formulations. These fundamental drivers position the trinitrotoluene market for steady expansion despite environmental headwinds in North America and Europe.

Global Trinitrotoluene (TNT) Market Trends and Insights

Increasing Demand for Explosives in Hard-Rock Mining

China's rare-earth mines are turning to TNT for its ability to maintain detonation velocity, a crucial factor as ANFO loses energy when saturated. This shift is reflected in Australia's lithium hard-rock operations, particularly in Greenbushes and the Pilbara, where TNT boosters are now the preferred method for initiating emulsion columns in high-silica ore. Meanwhile, in India, Solar Industries has responded to both domestic coal and export mining demands by inaugurating new plants in 2024. As ore bodies delve deeper than 1,500 meters, the intensifying water pressure underscores the importance of TNT. Its crystalline structure offers resistance to densification, a common issue that leads to ANFO misfires.

Global Defense Modernization and Stockpiling

China has set its 2024 defense budget at a hefty amount, while Japan has greenlit a historic budget, with both nations emphasizing ammunition stocks, particularly those using TNT-filled shells. The U.S. Army's commitment to sourcing TNT annually through 2031 underscores a long-term procurement strategy. Demonstrating the tight supply, Poland's Nitro-Chem has been exporting TNT to U.S. clients via interim agreements, highlighting a gap until domestic production scales up. Following a surge in artillery use in Ukraine, NATO backed capacity expansions in Turkey and South Korea. Furthermore, adherence to STANAG 4170's insensitive-munitions guidelines is bolstering the demand for TNT-RDX blends.

Stringent Environmental and Occupational Regulations

Proposed by the U.S. EPA, closed-loop wastewater treatment could increase production costs. The DOE has tightened airborne TNT vapor limits, necessitating ventilation retrofits. In India, PESO has instituted biennial audits, imposing fines for non-compliance. REACH's new mandate for extended toxicity studies is putting pressure on small producers across Europe.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Megaprojects Requiring Controlled Blasting

- Shale-Formation Fracturing Charges in Oil and Gas

- Shift Toward ANFO, Emulsions and Plastic Explosives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Military uses accounted for 71.62% of the 2025 volume, demonstrating the central role of ordnance stockpiling in the trinitrotoluene market. The U.S. government allocated a significant budget for conventional ammunition in its fiscal 2025 plan, with rounds filled with TNT making up a notable portion of this expenditure. Such a financial commitment underscores the pivotal role of military demand in shaping the trinitrotoluene market's size and emphasizes the need for resilient supply chains through 2030. Furthermore, the segment's adherence to NATO STANAG 4439 standards not only elevates entry barriers but also upholds premium pricing.

Mining is the fastest-growing segment, with a 5.88% CAGR. This surge is largely attributed to the industry's stringent standards, where misfires of ANFO in deep-ore extraction are simply not tolerated. In 2024, China's rare-earth production utilized a significant amount of TNT boosters. Given this consumption rate, the mining segment is poised to expand its share of the trinitrotoluene market by 2030. While construction and specialized applications together represent a smaller portion of the market volume, urban tunneling's strict vibration limits highlight areas of unmet demand. This is particularly true in projects where owners mandate the use of electronic detonators in conjunction with TNT cartridges. Throughout these diverse applications, the growth trajectory of the trinitrotoluene industry is shaped by a delicate balance between cost pressures and performance expectations.

The Trinitrotoluene (TNT) Market Report is Segmented by Application (Military, Mining, Construction, and Other Application) and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region held 46.02% of the trinitrotoluene market in 2025, bolstered by China's Belt and Road initiatives and India's increased defense acquisitions. Highlighting the domestic demand, Solar Industries reported a significant surge in defense sales. Japan's unprecedented budget fueled TNT demand, evident from NOF Corporation's contracts with the Self-Defense Forces. Meanwhile, miners in Indonesia and Vietnam are opting for TNT boosters in their wet, high-silica orebodies, further solidifying the market's outlook in the Asia-Pacific.

North America's growth is anchored by a new U.S. facility set to produce substantial volumes annually by late 2026. This move aims to curtail reliance on imports from Poland and Turkey. In Canada, a surge in ammunition stockpiles has sparked regional demand. However, smaller firms grapple with the financial strain of new EPA regulations.

Europe faces stringent REACH regulations and is witnessing a shift towards emulsions. Yet, the U.K.'s Task Force KINDRED's procurement of TNT from Poland to support Ukraine underscores a persistent reliance. In Switzerland and the Alpine tunnels, TNT remains crucial for precision blasting. However, newcomers to the market must navigate hefty regulatory fees per dossier. In South America, the lithium triangle and copper belt mines, known for their moisture-rich, high-altitude conditions, show a preference for TNT. Additionally, while Brazilian infrastructure projects are driving spot demand, they face hurdles with IBAMA licensing delays.

The Middle East and Africa, with a 5.65% CAGR through 2031, are capitalizing on Saudi investments in ammonium nitrate. These investments, in collaboration with Orica and MAXAM service contracts, are driving an uptick in volume.

- Austin Powder

- BME Mining (Omnia Group)

- Chemring Group PLC

- China Gezhouba Group Corporation

- China Poly Group Corporation

- Dyno Nobel

- Enaex

- Eurenco

- FORCIT GROUP

- Hanwha Group

- MAXAMCORP HOLDING SL

- NITRO-CHEM SA

- NOF CORPORATION

- Orica Limited

- Pakistan Ordnance Factories (POF)

- SBL Energy

- Sichuan Yahua Industrial Group Co., Ltd.

- Solar Industries India Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for explosives in hard-rock mining

- 4.2.2 Global defense modernisation and stockpiling

- 4.2.3 Infrastructure megaprojects requiring controlled blasting

- 4.2.4 Shale-formation fracturing charges in oil and gas

- 4.2.5 Precision micro-charge adoption in launch vehicles

- 4.3 Market Restraints

- 4.3.1 Stringent environmental and occupational regulations

- 4.3.2 Shift toward ANFO, emulsions and plastic explosives

- 4.3.3 Volatile toluene feedstock availability

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 Application

- 5.1.1 Military

- 5.1.2 Mining

- 5.1.3 Construction

- 5.1.4 Other Application

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Thailand

- 5.2.1.6 Malaysia

- 5.2.1.7 Vietnam

- 5.2.1.8 Indonesia

- 5.2.1.9 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Russia

- 5.2.3.6 Spain

- 5.2.3.7 Turkey

- 5.2.3.8 Nordic Countries

- 5.2.3.9 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Colombia

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Qatar

- 5.2.5.4 Egypt

- 5.2.5.5 South Africa

- 5.2.5.6 Nigeria

- 5.2.5.7 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Austin Powder

- 6.4.2 BME Mining (Omnia Group)

- 6.4.3 Chemring Group PLC

- 6.4.4 China Gezhouba Group Corporation

- 6.4.5 China Poly Group Corporation

- 6.4.6 Dyno Nobel

- 6.4.7 Enaex

- 6.4.8 Eurenco

- 6.4.9 FORCIT GROUP

- 6.4.10 Hanwha Group

- 6.4.11 MAXAMCORP HOLDING SL

- 6.4.12 NITRO-CHEM SA

- 6.4.13 NOF CORPORATION

- 6.4.14 Orica Limited

- 6.4.15 Pakistan Ordnance Factories (POF)

- 6.4.16 SBL Energy

- 6.4.17 Sichuan Yahua Industrial Group Co., Ltd.

- 6.4.18 Solar Industries India Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment