|

시장보고서

상품코드

1937339

알킬 폴리글리코사이드 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Alkyl Polyglycoside - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

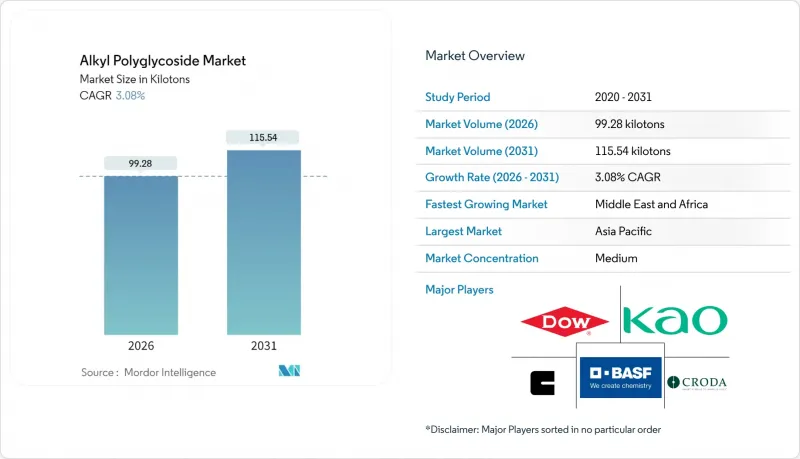

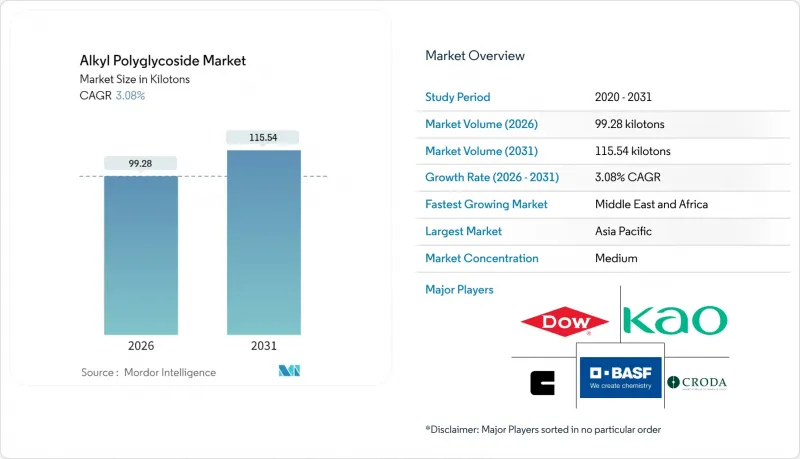

알킬 폴리글리코사이드 시장 규모는 2026년에는 99.28 킬로톤으로 추정되고, 2025년 96.31 킬로톤에서 성장이 전망됩니다.

2031년 예측치는 115.54 킬로톤으로 2026년부터 2031년까지 CAGR 3.08%로 성장할 것으로 예상됩니다.

유해한 비이온성 계면활성제 규제에 따른 단계적 폐지, 바이오 기반 원료로의 빠른 배합 전환, 원료 공급 안정화를 위한 꾸준한 생산능력 증설이 수요를 견인하고 있습니다. 가정용 및 퍼스널케어 제품 제조업체는 에코 라벨 기준을 충족하기 위해 알킬폴리글루코사이드 계면활성제를 지정하는 경향이 증가하고 있으며, 유전 서비스 기업은 환경 배출 제한을 충족하기 위해 APG 수화제를 채택하고 있습니다. 아시아 업체들은 팜유와 코코넛 오일에서 추출한 지방 알코올의 원료 조달에 있어 지리적 이점을 활용하여 수출 계약을 체결하고 있습니다. 한편, 유럽의 공급업체들은 지속가능성을 강조한 브랜딩을 통해 프리미엄 시장 지위를 확보하고 있습니다. 원료 가격의 변동과 베타 인, 아미노산 산화물과 경쟁하는 것, 통합 화학 대기업이 생산 규모를 확대하고 공정 노하우를 공유함에 따라 비용 곡선은 계속 개선되고 있습니다.

세계 알킬 폴리글리코사이드 시장 동향 및 인사이트

가정용 및 퍼스널케어 제품에서 바이오 기반 계면활성제에 대한 수요 확대

브랜드 오너는 에코라벨 인증 획득과 프리미엄 선반 공간 확보를 위해 황산염 무첨가, 식물 유래 성분을 중심으로 제품 포트폴리오를 재구축하고 있습니다. 다국적 소비재 업체들의 대량 주문으로 향후 수요를 예측할 수 있기 때문에 공급업체들은 생산능력 확대와 함께 씻어내는 제품과 씻어내지 않는 제품 각각에 특화된 등급 개선을 추진하고 있습니다. 배합 설계자는 알킬폴리글루코사이드 계면활성제의 저자극성, 효소와의 시너지 효과, 그리고 높은 세정력을 유지하면서 황산염이 없는 특성을 높이 평가하고 있습니다. 디지털 문해력이 높은 소비자들은 성분 표시를 꼼꼼히 살피기 때문에 소매업체들은 인식 가능한 당계면활성제가 함유된 완제품을 재고해야 한다는 압박을 받고 있습니다. 아시아 위탁생산 기업들은 APG를 통합한 턴키 솔루션을 제공함으로써 전 세계 개인 브랜드 소매업체들의 혁신 리드타임을 단축하고 있습니다.

노닐페놀에톡실레이트(NPE) 및 기타 유해 계면활성제 규제 단계적 폐지

유럽화학제품청(ECHA)은 NPE(노닐페놀에톡실레이트)의 대부분의 용도를 금지하여 전 세계 공급망에 파급되는 대체 프로그램을 가속화시켰습니다. 미국 TSCA(독성물질관리법)의 위험성 평가와 주정부 차원의 노력도 유럽의 태도를 반영하여 대체품 검증 기간을 단축하고 있습니다. 알킬폴리글루코사이드 계면활성제는 2차 알코올계 에톡실레이트 잔류물을 포함하지 않고 성능 사양을 충족하여 서류 작성 부담을 줄이고, 다운스트림 공정의 폐기물 처리 위험을 줄입니다. 조달 부서는 예외조항에 근거한 NPE계 재고 유지와 비교하여 APG로의 전환이 컴플라이언스 비용 절감으로 이어진다는 점을 지적하고 있습니다. 정책 방향이 명확하기 때문에 기술 위험에 대한 인식이 낮아지고, APG는 시설 청소 및 섬유 가공 분야에서 비이온성 대체품의 표준 선택이 되고 있습니다.

천연 지방 알코올 및 전분 원료 가격의 변동성

지방 알코올 비용은 알킬폴리글루코사이드의 변동비의 약 65%를 차지하기 때문에 생산자는 바이오디젤 의무화 및 날씨에 따른 수확 주기에 따른 원료 가격 변동에 영향을 받기 쉽습니다. C12-C14 알코올은 2023년 톤당 1,467달러까지 하락했다가 2024년 엘니뇨 현상으로 인한 팜유 수확량 감소의 영향으로 30% 이상 반등했습니다. 현물 가격의 급등은 분기별 가격 조정을 강요하고, 고정 소매 계약에 따라 운영되는 세제 배합 제조업체를 불안정하게 만듭니다. 일부 APG 공급업체들은 장기 플랜테이션 계약으로 리스크를 헤지하고 있지만, 가뭄, 노동력 부족, 식물 검역상의 제한으로 인해 여전히 납품이 제한될 수 있습니다. 투자자들은 신규 APG 플랜트에 자본을 배분할 때 이러한 불확실성을 고려하기 때문에 프로젝트 가동 기간이 길어질 수 있습니다.

부문 분석

지방 알코올 등급은 2025년 생산량의 42.10%를 차지할 것으로 예상되며, 이는 수십 년에 걸친 규모의 경제 효과와 세제용 알코올 크래커로부터의 라 우릴 알코올 공급원의 안정성을 뒷받침합니다. 제조 공정을 잘 알고 있기 때문에 색조, 냄새, 중합도의 균일성을 보장할 수 있으며, 이는 대중용 농축 세제에서 매우 중요한 특성입니다. 식물성 오일 유래 제품은 연속 에스테르 교환 및 효소 합성 기술을 통해 사이클 시간을 단축하고 탄소 강도를 낮출 수 있기 때문에 3.55%의 가장 높은 CAGR을 보이고 있습니다. 식물성 기름에서 추출한 알킬폴리글루코사이드 시장 규모는 아세안 및 남미 바이오디젤 클러스터의 급속한 원료 다양화를 반영하여 2025년 27.54 킬로톤에서 2031년 33.92 킬로톤으로 확대될 것으로 예상됩니다.

신흥 당류 및 옥수수 전분 기반 알킬폴리글루코사이드는 두 자릿수 조수익률을 자랑하는 틈새 퍼스널케어 제품 라인에 공급되어 미성숙한 공급망과 높은 단가를 보완하고 있습니다. 한편, 지방 알코올 생산자는 충돌 흐름 반응기를 개선하여 알코올과 포도당의 몰비를 3 : 1 미만으로 줄였습니다. 이를 통해 원료 투입량을 5% 절감하고 수율을 향상시키고 있습니다. 공급업체는 이러한 프로세스 혁신과 농장 원산지를 추적하는 블록체인 기반 추적성 모듈을 결합하여 유럽 소매업체의 추적성 요구 사항을 충족하고 있습니다. 식물성 기름 기술의 규모가 확대됨에 따라 지방 알코올 경로와의 가격 차이가 줄어들고, 기존의 부문 경계를 모호하게 하는 공동 투자 전략이 촉진되고 있습니다.

알킬폴리글루코사이드 시장 보고서는 제품 유형(지방 알코올, 설탕, 옥수수 전분, 식물성 기름, 기타), 용도(퍼스널케어 및 화장품, 가정용 제품, 산업용 세제, 농약, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카) 별로 분류됩니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

아시아태평양은 중국의 통합 석유화학단지와 동남아시아의 팜 오일의 근접성을 배경으로 2025년 세계 생산량의 45.90%를 차지했습니다. 지방 세제 혜택은 설포석회, APG, 베타 인 생산 라인에 대한 투자를 촉진하여 닝보와 상하이 주변에 경쟁력 있는 제조 클러스터를 형성하고 있습니다. 인도 뷰티 및 퍼스널케어 시장(2025년 기준 200억 달러 규모)에서 황산염이 없는 샴푸가 지방 도시로 확산됨에 따라 국내 APG 수요가 확대되고 있습니다. 태국과 말레이시아는 지방 알코올 원료 공급기지로서 입지를 굳히고 있으며, 방파콩과 콴탄의 생산기지에서 일본 OEM업체에 대량의 APG를 출하하고 있습니다.

중동 및 아프리카는 기반 규모는 작지만 2031년까지 CAGR 3.52%로 가장 빠르게 성장할 것으로 예상됩니다. 이는 각국 석유회사들이 증산회수 시험정에 환경 친화적인 첨가제를 요구하는 움직임에 따른 것입니다. 사우디 주바일의 다운스트림 사업에서는 에톡실레이트 생산라인에 인접한 APG 테스트 플랜트를 가동하여 단일 물류 구역 내에서 계면활성제 블렌딩을 가능하게 하고 있습니다. 남아프리카공화국의 상업용 세제 배합 제조업체는 슈퍼마켓의 개인 브랜드 지속가능성 점수표에 대응하기 위해 현지 배합 APG 농축액을 채택하고 있습니다. 지역 지자체는 친환경 조달 정책에 따라 공공 청소 계약 시 바이오 계면활성제를 우선적으로 채택하고 있어 안정적인 기반 수요를 형성하고 있습니다.

북미와 유럽의 수요는 적극적인 NPE(비이온성 계면활성제) 단계적 폐지 일정과 소매업체의 자발적 화학제품 감시목록에 힘입어 한 자릿수 성장률을 보이고 있습니다. 파일럿케미컬이 2026년부터 오하이오주에서 Bio IOS 기술을 독점적으로 제조할 수 있는 라이센스를 취득한 것은 미국 바이오 기반 계면활성제에 대한 새로운 자본 투입을 의미합니다. 유럽의 고급 부문에서는 비용과 발포성의 균형을 맞추기 위해 APG와 아미노산화물을 혼합하여 사용하고 있습니다. 한편, 캘리포니아의 조제업체들은 보다 안전한 소비자 제품 규제에 대응하기 위해 APG에 의존하고 있습니다. 남미는 절대량에서는 뒤쳐져 있지만 농약용 보조제 분야에서 탄력을 받고 있으며, APG의 낮은 식물독성을 활용하여 글리포세이트 대체제제로의 침투를 꾀하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05Alkyl Polyglycoside market size in 2026 is estimated at 99.28 kilotons, growing from 2025 value of 96.31 kilotons with 2031 projections showing 115.54 kilotons, growing at 3.08% CAGR over 2026-2031.

Demand is driven by regulatory phase-outs of hazardous non-ionic surfactants, rapid shifts in formulation toward bio-based ingredients, and steady capacity additions that stabilize the raw-material supply. Home-care and personal-care producers increasingly specify Alkyl polyglucoside surfactants to align with ecolabel criteria, while oil-field service companies adopt APG hydrotropes to meet environmental discharge limits. Asian manufacturers capitalize on their proximity to palm- and coconut-based fatty alcohols to secure export contracts, whereas European suppliers leverage sustainability branding to achieve premium positioning. Despite feedstock price fluctuations and competition from betaines and amino oxides, cost curves continue to improve as integrated chemical majors scale up production and share process expertise.

Global Alkyl Polyglycoside Market Trends and Insights

Growing Demand for Bio-Based Surfactants in Home and Personal-Care Formulations

Brand owners reposition product portfolios around non-sulfate, plant-derived ingredients to secure ecolabel certifications and capture premium shelf space. Volume commitments from multinational fast-moving consumer goods companies create forward visibility, encouraging suppliers to expand capacity and refine grades tailored to rinse-off and leave-on products. Formulators favor Alkyl polyglucoside surfactants for mildness, low irritation, and synergy with enzymes, enabling sulfate-free laundry detergents that still deliver high soil removal. Digital-savvy consumers scrutinize ingredient lists, pushing retailers to stock finished goods containing recognizable sugar-based surfactants. Asian contract manufacturers respond with turnkey offerings that integrate APGs, shortening innovation lead times for global private-label retailers.

Regulatory Phase-Out of Nonyl-Phenol Ethoxylates and Other Hazardous Surfactants

The European Chemicals Agency banned NPEs in most applications, triggering accelerated substitution programs that ripple across global supply chains. US TSCA risk evaluations and state-level initiatives mirror Europe's stance, compressing customer timelines to validate alternatives. Alkyl polyglucoside surfactants fulfill performance specifications without secondary alcohol ethoxylate residues, easing dossier preparation and reducing downstream disposal liabilities. Procurement teams cite lower compliance costs when transitioning to APGs versus maintaining NPE-based inventories under derogation clauses. The clear direction of policy lowers perceived technology risk, making APGs the default non-ionic replacement in institutional cleaning and textile processing.

Volatility in Natural Fatty-Alcohol and Starch Feedstock Prices

Fatty-alcohol costs represent roughly 65% of Alkyl polyglucoside variable expenses, leaving producers vulnerable to commodity swings tied to bio-diesel mandates and weather-linked harvest cycles. After dropping to USD 1,467 per ton in 2023, C12-C14 alcohols rebounded by more than 30% in 2024 due to El Nino-related palm-oil yield reductions. Spot spikes force quarterly price resets that unsettle detergent formulators operating under fixed retail contracts. Some APG suppliers hedge their risks with long-term plantation agreements; however, drought, labor shortages, and phytosanitary restrictions can still curtail deliveries. Investors weigh these uncertainties when allocating capital to greenfield APG plants, which can occasionally result in lengthened project gestation periods.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Additions and Backward Integration of Fatty-Alcohol Suppliers

- Rising Adoption of APG Hydrotropes in Alkaline Industrial Cleaning and Oil-Field Fluids

- Availability of Alternative Mild Surfactants (e.g., Betaines, Amino-Oxides)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fatty alcohol-based grades captured 42.10% of 2025 volume, underscoring decades of scale efficiencies and readily available lauryl alcohol streams from detergent-alcohol crackers. Their process familiarity assures consistent color, odor, and degree of polymerization, features critical to mass-market detergent concentrates. Vegetable-oil-derived variants exhibit the highest 3.55% CAGR, as continuous transesterification and enzymatic synthesis technologies enable shorter cycle times and lower carbon intensity. The Alkyl polyglucoside market size associated with vegetable-oil pathways is projected to expand from 27.54 kilotons in 2025 to 33.92 kilotons by 2031, reflecting rapid feedstock diversification among ASEAN and South American biodiesel clusters.

Up-and-coming sugar- and corn-starch-based APGs service niche personal-care lines that command double-digit gross margins, compensating for immature supply chains and higher unit costs. Meanwhile, fatty-alcohol producers refine impinging-stream reactors that reduce the alcohol-to-glucose molar ratio below 3:1, slicing raw-material inputs by 5% and enhancing yield. Suppliers pair these process strides with blockchain-enabled traceability modules that map the origins of plantations, satisfying traceability mandates from European retailers. As vegetable-oil technologies scale, price differentials versus fatty-alcohol routes narrow, inviting co-investment strategies that blur traditional segment boundaries.

The Alkyl Polyglucoside Market Report is Segmented by Product Type (Fatty Alcohol, Sugar, Corn-Starch, Vegetable Oil, and Other Product Type), Application (Personal Care and Cosmetics, Home-Care Products, Industrial Cleaners, Agricultural Chemicals, and Other Application), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region retained 45.90% of the global volume in 2025, driven by integrated petrochemical complexes in China and the proximity of palm oil in Southeast Asia. Provincial tax incentives encourage investment in sulfosuccinate, APG, and betaine lines, fostering a competitive manufacturing cluster around Ningbo and Shanghai. India's beauty and personal care sector, valued at USD 20 billion for 2025, amplifies domestic APG pull-through as sulfate-free shampoos penetrate Tier-II cities. Thailand and Malaysia consolidate their role as fatty-alcohol feedstock hubs, supplying Bangpakong and Kuantan sites that dispatch bulk APG to Japanese OEMs.

The Middle East and Africa are projected to post the fastest 3.52% CAGR through 2031, albeit from a smaller base, as national oil companies seek environmentally compatible additives for enhanced-oil-recovery pilot wells. Saudi downstream initiatives in Jubail include pilot APG units adjacent to ethoxylate trains, enabling surfactant blending within a single logistical zone. South African formulators of institutional cleaners adopt locally blended APG concentrates to meet supermarket private-label sustainability scorecards. Regional governments use green-procurement policies to prioritize bio-based surfactants for municipal cleaning contracts, building steady baseline demand.

North American and European volumes grow at modest single-digit rates underpinned by aggressive NPE withdrawal schedules and voluntary retailer chemical watch lists. Pilot Chemical's exclusive license to manufacture Bio IOS technology in Ohio from 2026 signals fresh capital injection into U.S. bio-based surfactants. European premium segments feature APG blends with amino-oxides to balance cost and foaming, while California formulators lean on APG to comply with Safer Consumer Products regulations. South America trails in absolute volume but registers momentum in crop-protection adjuvants, leveraging APG's low phytotoxicity to penetrate glyphosate replacement formulations.

- BASF

- Brillachem

- Clariant

- Croda International plc

- Dow

- Evonik Industries

- FENCHEM

- Galaxy Surfactants

- Kao Corporation

- Pilot Chemical Corp.

- Seppic (Arkema Group)

- Shanghai Chenhua International Trade Co., Ltd.

- Shanghai Fine Chemical Co., Ltd.

- Shanghai Sunwise Chemical Co., Ltd

- Silver Fern Chemical LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for bio-based surfactants in home and personal-care formulations

- 4.2.2 Regulatory phase-out of nonyl-phenol ethoxylates (NPEs) and other hazardous surfactants

- 4.2.3 Capacity additions and backward integration of fatty-alcohol suppliers

- 4.2.4 Rising adoption of APG hydrotropes in alkaline industrial cleaning and oil-field fluids

- 4.2.5 Cost-cutting high-gravity impinging-stream reactors enabling <3:1 alcohol-to-glucose ratios

- 4.3 Market Restraints

- 4.3.1 Volatility in natural fatty-alcohol and starch feedstock prices

- 4.3.2 Availability of alternative mild surfactants (e.g., betaines, amino-oxides)

- 4.3.3 Stringent RSPO/deforestation-free palm supply audits tightening raw-material access

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Fatty Alcohol

- 5.1.2 Sugar

- 5.1.3 Corn-starch

- 5.1.4 Vegetable Oil

- 5.1.5 Other Product Type

- 5.2 By Application

- 5.2.1 Personal Care and Cosmetics

- 5.2.2 Home-care Products

- 5.2.3 Industrial Cleaners

- 5.2.4 Agricultural Chemicals

- 5.2.5 Other Application

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Indonesia

- 5.3.1.6 Thailand

- 5.3.1.7 Malaysia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Nordic Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Qatar

- 5.3.5.4 Egypt

- 5.3.5.5 Nigeria

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Brillachem

- 6.4.3 Clariant

- 6.4.4 Croda International plc

- 6.4.5 Dow

- 6.4.6 Evonik Industries

- 6.4.7 FENCHEM

- 6.4.8 Galaxy Surfactants

- 6.4.9 Kao Corporation

- 6.4.10 Pilot Chemical Corp.

- 6.4.11 Seppic (Arkema Group)

- 6.4.12 Shanghai Chenhua International Trade Co., Ltd.

- 6.4.13 Shanghai Fine Chemical Co., Ltd.

- 6.4.14 Shanghai Sunwise Chemical Co., Ltd

- 6.4.15 Silver Fern Chemical LLC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment