|

시장보고서

상품코드

1937359

커넥티드 약물전달 기기 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Connected Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

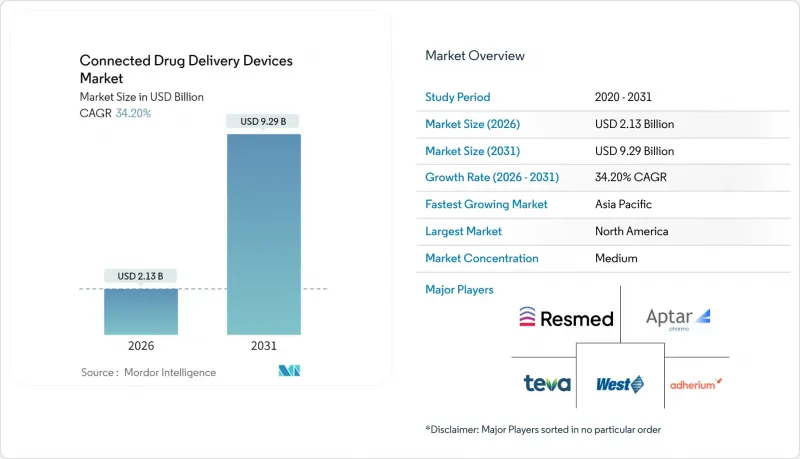

커넥티드 약물전달 기기 시장 규모는 2025년 15억 9,000만 달러에서 2026년에는 21억 3,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 34.2%를 기록하며 2031년까지 92억 9,000만 달러에 달할 것으로 예측됩니다.

이러한 지속적인 확대는 전 세계 만성질환의 증가, 디지털 헬스 기술의 급속한 보급, 그리고 리얼월드 데이터(RWE)를 무작위 대조 시험과 동등하게 취급하는 규제 변화와 맞물려 있습니다. 미국 식품의약국(FDA)의 2024년 '리얼월드 데이터 프로그램' 확대는 제약사가 디바이스의 가치를 검증할 수 있는 방법을 재구성했습니다. 한편, 90만 4,000달러의 연방 보조금으로 지원된 그래핀 기반 에너지 수확 기술의 획기적인 발전은 배터리가 필요 없는 센서의 실현을 약속하고 있습니다. CMS의 2025년 의사 보상 일정에서 확인된 가치 기반 상환 시스템의 병행 발전은 복약 순응도를 포착하는 하드웨어에 대한 직접적인 인센티브를 창출하고 있습니다. 동시에 FDA가 2024년 3월에 발표한 지침 초안은 개발자가 모든 커넥티드 디바이스 신청서에 강력한 사이버 보안 프레임워크를 포함하도록 요구하고 있습니다.

세계 커넥티드 약물전달 기기 시장 동향 및 인사이트

만성질환 증가 추세

급성기 치료에서 장기 투약 요법으로의 전환이 진행됨에 따라, 기존에는 정맥주사 클리닉에서만 가능했던 복잡한 생물학적 제제를 환자가 집에서 투여할 수 있는 커넥티드 자동주사기 개발이 요구되고 있습니다. 바이오젠이 LEQEMBI를 피하투여 형태로 전환한 사례는 원격투여가 신경퇴행성 질환 치료에 대한 접근성을 확대할 수 있는 좋은 사례입니다. 지역적으로 분산된 희귀질환 환자군도 원격 모니터링이 필요하며, 실시간 바이오마커 피드백은 개별화된 용량 조정을 지원합니다. 복약 불이행으로 인해 미국 의료 시스템에 연간 1,000억 달러의 손실이 발생하는 가운데, 지불 기관들은 연결성을 경제적 필요성으로 인식하기 시작했습니다.

원격 모니터링 및 원격의료에 대한 수요 확대

원격 플랫폼은 현재 라이브 스트림을 분석하여 증상이 나타나기 전에 악화를 예측합니다. FDA가 커넥티드 디바이스 데이터를 승인함에 따라 시판 후 조사가 가능해져 제품 표시 주장을 강화할 수 있습니다. 양방향 원격의료를 통해 임상의는 복용량 미세 조정을 장치에 직접 전송할 수 있습니다. COVID-19의 충격으로 도입 주기가 빨라졌고, 일본과 싱가포르는 신속한 출시를 촉진하기 위해 신속 승인 루트를 만들었습니다. 만카인드사의 흡입 시스템은 5G 대응 엣지 처리 피드백 루프를 통해 인슐린의 실시간 적정화를 지원하는 사례입니다.

기존 일회용 제품 대비 높은 비용

기존 흡입기나 펜형 장치와 비교하여 200-400%의 가격 차이가 존재하기 때문에 무보험 계층의 도입에 걸림돌로 작용하고 있습니다. 하드웨어 외에도 지속적인 클라우드 서비스 이용료가 정기적인 지출을 증가시킵니다. 서비스형 디바이스(Device-as-a-Service, DaaS) 번들이 대안으로 떠오르고 있지만, 지불자 측의 회의적인 태도는 여전히 강한 상황입니다. 시장의 세분화로 인해 단위 비용 절감으로 이어지는 규모의 경제가 실현되지 못하고 있습니다. 전용 청구 코드가 미정비되어 있어 투자대비 효과 평가가 여전히 어려운 상황입니다.

부문 분석

2025년 매출의 59.62%를 차지하는 통합형 커넥티드 디바이스는 9억 5,000만 달러 규모의 커넥티드 약물전달 기기 시장 규모에 해당합니다. 제약회사는 측정 정확도와 규제 적합성을 보장하는 턴키 시스템을 선호하기 때문입니다. 스마트 인슐린 펜이 가장 큰 하위 부문을 형성하고 있으며, 일라이 릴리는 GLP-1 약물 수요에 대응하기 위해 30억 달러 규모의 생산능력 투자를 진행하고 있습니다. 센서 후착형은 기반 규모는 작지만, 약제 처방 변경 없이 연결성을 구현해 연 35.45%의 성장세를 보이고 있습니다.

커넥티드 흡입기 센서(예: Adherium의 Hailie 플랫폼)는 소아 임상시험에서 복약 순응도를 180% 향상시켰습니다. 웨어러블 주사기용 애드온은 대용량 바이오의약품을 대상으로 하며, 주사펜용 센서는 기존 제품군의 가치를 극대화합니다. 하이브리드 구조가 부상하면서 기업은 통합 대시보드 내에서 고부가가치 통합 장치와 비용 효율적인 개조 솔루션을 함께 제공할 수 있게 되었습니다.

2025년에는 Bluetooth Low Energy가 64.38%의 출하량 점유율을 차지할 것으로 예상되며, NFC는 36.4%의 CAGR로 성장할 것으로 예상됩니다. NFC의 패시브 모드는 대기 전류를 거의 제로에 가깝게 억제하여 수년간의 수명을 가능하게 합니다. 단거리 통신은 해킹 위험을 줄이고, 규제 당국의 감시에도 대응할 수 있습니다. 한편, 저전력 셀룰러 모듈은 스마트폰과 페어링할 필요 없이 전 세계에 도달할 수 있어 노년층의 요구에 부응하고 있습니다.

RFID와 QR코드 식별 기술은 복잡한 연결성보다 가격이 우선시되는 상황에서 여전히 유효합니다. Nordic의 멀티 프로토콜 칩은 BLE, NFC, Thread, Zigbee를 단일 다이에 통합하여 옵션 간 부품 비용을 균일화하고 설계의 자유도를 확대합니다.

지역별 분석

북미의 44.10%의 점유율은 메디케어의 적용 범위, 성숙한 전자건강기록(EHR)의 보급, FDA의 실세계 데이터 지원 등에 기인합니다. CMS의 복약 순응도 모니터링에 대한 상환은 의료 서비스 제공자의 투자 부담을 줄여주고, 연방 사이버 보안 가이드라인은 통일된 보호 조치를 규정하고 있습니다. 캐나다와 멕시코는 규제조화협정을 통해 국경 간 제품 도입을 간소화하고 있습니다.

아시아태평양은 36.2%의 CAGR로 가장 빠르게 성장하는 시장입니다. 일본 PMDA는 워싱턴 DC에 사무소를 개설하여 해외 신청자를 지원하고 있으며, 중국에서는 2024년 사상 최대인 48건의 혁신신약을 승인하는 등 혁신에 대한 의욕이 높아지고 있습니다. 지역 반도체 생산능력과 5G의 광범위한 보급이 의료기기의 연결성을 뒷받침하고 있습니다. 인도는 정부의 의료기술 현지화 지원책에 힘입어 유망하지만, 가격 통제로 인해 수익률에 압박을 받고 있습니다.

유럽에서는 MDR(의료기기 규정)의 통일화가 진행되는 한편, GDPR(일반 데이터 보호 규정)과 향후 시행 예정인 AI 법이 겹치면서 컴플라이언스 주기가 길어지고 있습니다. 영국은 브렉시트 이후에도 MDR을 광범위하게 준수하면서 신속 승인 제도를 통해 세계 공급업체를 유치하고 있습니다. 독일과 프랑스가 주요 수요를 견인하고 있으며, 북유럽 국가들은 연결형 흡입기에 대한 국민보험 적용을 시범적으로 도입하여 조기 보급을 촉진하고 있습니다.

남미, 중동, 아프리카는 만성질환 증가와 원격의료 시범사업에 힘입어 총 두 자릿수 성장을 기록하고 있습니다. 인프라 격차와 단편적인 상환 제도로 인해 단기적인 보급률이 저조하지만, 국제 지원 기관들이 시범 프로그램에 자금을 지원하여 의료 종사자들이 커넥티드 딜리버리 운영을 익힐 수 있도록 하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The connected drug delivery devices market is expected to grow from USD 1.59 billion in 2025 to USD 2.13 billion in 2026 and is forecast to reach USD 9.29 billion by 2031 at 34.2% CAGR over 2026-2031.

Continuous expansion aligns with the worldwide rise in chronic illnesses, rapid digital-health uptake, and a regulatory pivot that treats real-world evidence as equal to randomized trials. The FDA's 2024 Real-World Evidence Program expansion has reshaped how pharmaceutical firms validate device value, while breakthroughs in graphene-based energy harvesting financed by a USD 904,000 federal grant promise battery-free sensors. Parallel progress in value-based reimbursement-confirmed by CMS's 2025 Physician Fee Schedule-creates direct incentives for adherence-capturing hardware. At the same time, the FDA's March 2024 draft guidance compels developers to embed robust cybersecurity frameworks into every connected device submission.

Global Connected Drug Delivery Devices Market Trends and Insights

Rising Prevalence of Chronic Diseases

Long-term medication courses are replacing acute regimens, pushing developers to craft connected auto-injectors that patients can use at home for complex biologics once limited to infusion clinics. Biogen's move to subcutaneous forms of LEQEMBI shows how remote dosing broadens access for neurodegenerative therapies. Rare-disease populations spread across geographies also need remote oversight, and real-time biomarker feedback supports personalised dose adjustment. With non-adherence costing the U.S. system USD 100 billion yearly, payers now view connectivity as an economic necessity.

Growing Demand for Remote Monitoring & Tele-Health

Remote platforms now analyse live streams to predict exacerbations before symptoms surface. FDA acceptance of connected device data enables post-market studies that strengthen label claims. Bidirectional tele-health lets clinicians send dosing tweaks directly to devices.The COVID-19 shock compressed adoption cycles, while Japan and Singapore have created accelerated approval lanes that encourage rapid launches. Inhalation systems from MannKind illustrate 5G-enabled, edge-processed feedback loops that support real-time insulin titration.

High Device Cost vs. Conventional Disposables

Price gaps of 200-400% versus legacy inhalers or pens deter adoption among uninsured populations. Beyond hardware, ongoing cloud-service fees add recurring expenses. While device-as-a-service bundles offer an alternative, payer skepticism remains high. Market fragmentation prevents scale efficiencies that could compress unit costs. Lack of dedicated billing codes still clouds return-on-investment assessments.

Other drivers and restraints analyzed in the detailed report include:

- Advances in BLE & NFC Miniaturisation

- Direct-to-Cloud Low-Power Cellular IoT Adoption

- Cyber-Security & Patient-Data-Privacy Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated Connected Devices represented 59.62% of 2025 revenues, equal to USD 0.95 billion of connected drug delivery devices market size, as pharma companies favour turnkey systems that guarantee measurement accuracy and regulatory alignment. Smart insulin pens form the largest sub-segment; Eli Lilly's USD 3 billion investment in capacity aims to meet GLP-1 drug demand. Sensor retrofits, although capturing a smaller base, are growing 35.45% a year by enabling connectivity without altering drug formulations.

Connected inhaler sensors, such as Adherium's Hailie platform, recorded 180% adherence improvement in paediatric tests. Wearable-injector add-ons target large-volume biologics, while injection-pen sensors unlock legacy franchises. Hybrid architectures are emerging, letting firms offer premium integrated devices alongside cost-efficient retrofits within unified dashboards.

Bluetooth Low Energy commanded 64.38% deliveries in 2025, yet NFC is projected to rise at 36.4% CAGR. NFC's passive mode curbs standby current to near zero, allowing multi-year lifespan. Short-range comms cut hacking exposure, answering regulator scrutiny. Low-power cellular modules, meanwhile, target global reach without phone pairing, resonating with elderly demographics.

RFID or QR identifiers remain relevant where price sensitivity trumps elaborate connectivity. Multi-protocol chips from Nordic now embed BLE, NFC, Thread, and Zigbee on a single die, equalising bill-of-materials across options and broadening design freedom.

Connected Drug Delivery Devices Market Report is Segmented by Product Type(Connected Sensors [Connected Inhaler Sensors and More] and Integrated Connected Devices [Connected Inhalers and More), Technology (Bluetooth, Near-Field Communication and More), End User (Healthcare Providers, Homecare and More), Application (Respiratory Diseases, Diabetes and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 44.10% share stems from Medicare coverage, mature EHR penetration, and FDA support for real-world data. CMS reimbursement for adherence monitoring cushions provider investment, while federal cybersecurity guidance sets uniform guardrails. Canada and Mexico leverage regulatory alignment pacts that simplify cross-border launches.

Asia-Pacific is the fastest-growing theatre, advancing 36.2% CAGR. Japan's PMDA opened a Washington DC office to coach foreign applicants, and China's record 48 first-in-class drug approvals in 2024 signal growing innovation appetite. Regional semiconductor capacity and pervasive 5G coverage underpin device connectivity. India, buoyed by government incentives for med-tech localisation, shows promise though price controls pose margin pressure.

Europe offers harmonised MDR rules but layers on GDPR and an upcoming AI Act, lengthening compliance cycles. The United Kingdom maintains broad MDR parity post-Brexit yet courts global suppliers with fast-track options. Germany and France anchor substantial demand; Nordic nations experiment with national reimbursement for connected inhalers, spurring early adoption.

South America, the Middle East, and Africa collectively post double-digit growth, driven by rising chronic disease incidence and tele-health pilots. Infrastructure gaps and fragmented reimbursement still temper near-term penetration rates, but global donors fund pilot programs that familiarise clinicians with connected delivery.

- Resmed

- FindAir Sp. z o.o.

- Novo Nordisk

- Teva Pharmaceutical Industries

- Adherium

- West Pharmaceutical Services

- Aptar Pharma

- Ypsomed

- Phillips-Medisize (Molex)

- Medtronic

- Insulet

- Becton Dickinson & Co.

- Amiko Digital Health Limited.

- Enable Injections

- Insulclock S.L.

- Johnson & Johnson

- NuvoAir Inc.

- Amgen

- GlaxoSmithKline

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of chronic diseases

- 4.2.2 Growing demand for remote monitoring & tele-health

- 4.2.3 Advances in BLE & NFC miniaturisation

- 4.2.4 Direct-to-cloud low-power cellular IoT adoption

- 4.2.5 Energy-harvesting power modules reduce battery waste

- 4.2.6 Value-based reimbursement rewarding adherence data

- 4.3 Market Restraints

- 4.3.1 High device cost vs. conventional disposables

- 4.3.2 Cyber-security & patient-data-privacy gaps

- 4.3.3 E-waste compliance pressure on single-use electronics

- 4.3.4 Lack of interoperability standards across EHRs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product

- 5.1.1 Connected Sensors

- 5.1.1.1 Connected Inhaler Sensors

- 5.1.1.2 Connected Injection-Pen Sensors

- 5.1.1.3 Wearable-Injector Add-on Sensors

- 5.1.2 Integrated Connected Devices

- 5.1.2.1 Connected Inhalers

- 5.1.2.1.1 Metered-Dose Inhalers

- 5.1.2.1.2 Dry-Powder Inhalers

- 5.1.2.2 Connected Injection Devices

- 5.1.2.2.1 Smart Insulin Pens

- 5.1.2.2.2 Connected Auto-Injectors

- 5.1.2.2.3 Wearable Injectors

- 5.1.2.3 Connected Nebulizers

- 5.1.2.1 Connected Inhalers

- 5.1.1 Connected Sensors

- 5.2 By Technology

- 5.2.1 Bluetooth Low Energy (BLE)

- 5.2.2 Near-Field Communication (NFC)

- 5.2.3 Low-Power Cellular (LTE-M / NB-IoT)

- 5.2.4 RFID / QR Code

- 5.2.5 Other Technologies

- 5.3 By End User

- 5.3.1 Healthcare Providers (Hospitals, Clinics)

- 5.3.2 Patients / Homecare

- 5.3.3 Pharma & Biotech Companies

- 5.3.4 Payers & Remote-Monitoring Platforms

- 5.4 By Application

- 5.4.1 Respiratory Diseases

- 5.4.2 Diabetes

- 5.4.3 Oncology

- 5.4.4 Other Chronic Diseases

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 ResMed Inc.

- 6.3.2 FindAir Sp. z o.o.

- 6.3.3 Novo Nordisk A/S

- 6.3.4 Teva Pharmaceutical Industries Ltd

- 6.3.5 Adherium Limited

- 6.3.6 West Pharmaceutical Services Inc.

- 6.3.7 Aptar Pharma

- 6.3.8 Ypsomed AG

- 6.3.9 Phillips-Medisize (Molex)

- 6.3.10 Medtronic plc

- 6.3.11 Insulet Corporation

- 6.3.12 Becton Dickinson & Co.

- 6.3.13 Amiko Digital Health Limited.

- 6.3.14 Enable Injections

- 6.3.15 Insulclock S.L.

- 6.3.16 Johnson & Johnson (Janssen)

- 6.3.17 NuvoAir Inc.

- 6.3.18 Amgen Inc.

- 6.3.19 GlaxoSmithKline plc

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment