|

시장보고서

상품코드

1937375

영국의 핀테크 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United Kingdom Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

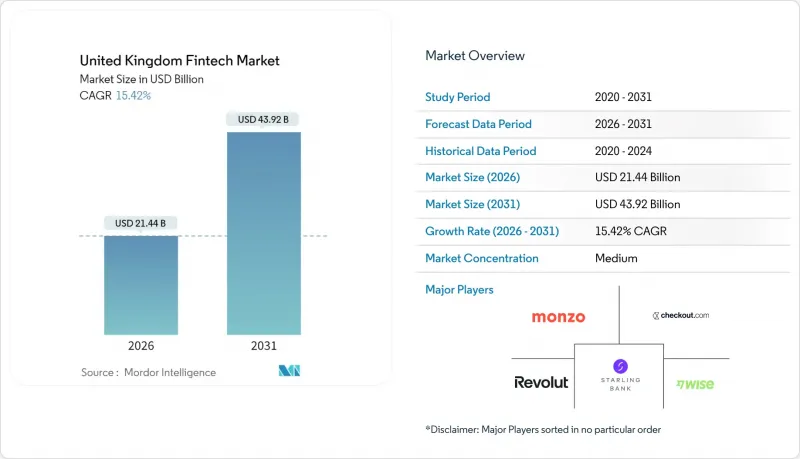

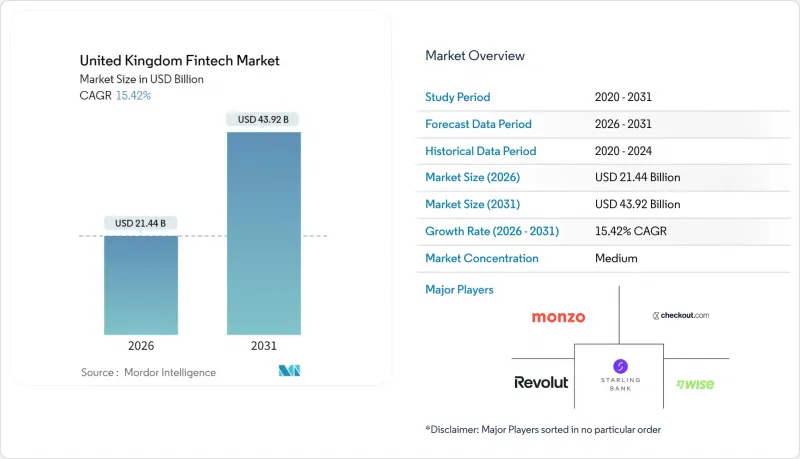

2026년 영국 핀테크 시장 규모는 214억 4,000만 달러로 추정되며, 2025년 185억 7,000만 달러에서 성장이 전망됩니다.

2031년에는 439억 2,000만 달러에 달할 것으로 예상되며, 2026년부터 2031년까지 CAGR 15.42%로 확대될 것으로 전망됩니다.

오픈뱅킹, 실시간 결제, 규제 샌드박스 프레임워크의 도입, 거시경제의 불확실성이 자금조달 패턴을 재편하는 가운데, 대응 가능한 수요를 확대하고 있습니다. 런던은 여전히 벤처 캐피털에게 매력적인 도시이지만, 맨체스터와 에든버러와 같은 지역 거점들도 전문 분야별로 틈새시장을 확보하고 있습니다. 네오뱅크는 성장 단계에서 수익화 단계로 넘어가고 있으며, 임베디드 금융은 소매업체와 핀테크 기업의 제휴 관계가 심화되고 있습니다. 기술, 특히 인공지능의 도입은 비용 효율적인 규모 확장을 지원하며 영국 핀테크 시장을 지속적인 두 자릿수 성장으로 이끌고 있습니다.

영국 핀테크 시장 동향 및 인사이트

오픈뱅킹 규제, API 기반 결제 활성화 가속화

2024년에는 7억 명의 영국 소비자가 오픈뱅킹 서비스를 적극적으로 이용하고, 제3자 제공업체를 위한 표준화된 API 액세스를 실현할 것으로 예상됩니다. 의무화된 데이터 공유로 인해 계좌 간 거래가 30% 증가하여 틈새 결제 업체들이 기존 카드 네트워크를 우회할 수 있게 되었습니다. 금융행위감독기구(FCA)가 주도하는 규제 설계는 영국 핀테크 시장을 경쟁 주도형 혁신의 벤치마킹 대상으로 삼고 있습니다. 결제 업체들은 현재 실시간 결제와 본인 확인 기능을 통합하여 가맹점 수수료를 절감하고 다양한 임베디드 금융 사용 사례를 촉진하고 있습니다. 상호운용성 향상은 고객의 전환 장벽을 낮추고, 기존 결제 처리업체에 대한 경쟁 압력을 강화하고 있습니다.

브렉시트 이후 규제 샌드박스, 세계 진입자 유치에 나서다.

2016년 이후 FCA의 샌드박스에는 55개 기업이 참여했으며, 디지털 증권 샌드박스는 2025년 3월에 12개의 국제적인 참여 기업을 추가로 받아들였습니다. 관리형 테스트 환경은 컴플라이언스 비용과 시장 출시 시간을 단축시켜 싱가포르와 미국의 기업들을 끌어들이고 있습니다. 2025년 1월에 발표된 새로운 AI 테스트 회랑은 알고리즘에 의한 신용 심사 및 자율 거래까지 그 범위를 확대합니다. FCA와 캐나다, 호주, 일본 규제 당국 간의 국경 간 양해각서는 여권 제도를 효율화하여 영국 핀테크 시장을 다국적 진출을 위한 성장 기업의 발판으로서 확고한 입지를 구축하고 있습니다.

영국 GDPR 및 레지스턴스 규정으로 인한 클라우드 컴플라이언스 비용 증가

2025년 3월까지 비즈니스 복원력 요건을 완전히 이행하기 위해서는 핵심 비즈니스 서비스에 대한 상세한 매핑과 심각하지만 현실적인 시나리오 테스트가 필요합니다. 하이퍼스케일 클라우드 제공업체를 이용하는 핀테크 기업은 엔드투엔드 관리 체계를 증명해야 하며, 이는 감사 빈도의 증가와 벤더 관리 비용의 증가로 이어집니다. 2025년 1월 시행되는 디지털 업무 복원력 법은 영국 GDPR 의무에 더해 ICT 위험 보고에 대한 추가 요건을 부과합니다. 중소기업은 기능 개발과 컴플라이언스 사이의 트레이드오프에 직면하고 있으며, 영국 핀테크 시장 전체에서 비용 곡선이 변화하고 있습니다.

부문 분석

2025년 기준 디지털 결제는 영국 핀테크 시장 규모의 32.15%를 차지했으며, 네오뱅킹은 2031년까지 19.18%의 CAGR로 가장 높은 성장 전망을 보이고 있습니다. Revolut과 Starling의 기록적인 수익성은 규모 확대 후 사업 단위 경제성의 실현 가능성을 입증하고 있습니다. Revolut은 2024년 7월 영국 은행 라이선스를 취득하고, 예치금을 통한 마진 확대와 제품 교차판매를 강화하기 위해 노력하고 있습니다. 지역 간 신용 격차가 확대되는 가운데, 중소기업을 위한 디지털 대출이 가속화되고 있습니다. 인슈어테크는 데이터 분석을 활용하여 인수 심사를 정교화하고, 디지털 투자는 AI 기반 포트폴리오 가시성의 혜택을 누리고 있습니다. 2024년 9월에 출범한 잉글랜드 은행의 AI 컨소시엄은 다양한 제안에서 알고리즘 혁신을 촉진하고 영국 핀테크 시장의 깊이를 더하고 있습니다.

네오뱅크의 고객 확보 비용은 소매업체의 결제 프로세스 내에 계좌를 통합하는 임베디드 금융 파트너의 등장으로 인해 낮아질 것입니다. 수익성 전환점은 암호화폐 거래 등 수수료 수입과 거래소 수입의 증가와 연동됩니다. 대체금융기관은 오픈뱅킹 데이터를 활용한 현금흐름 심사를 통해 중소기업의 심사 시간을 단축합니다. 웰스테크 기업은 소액 투자의 민주화를 추진하고, 인슈어테크 기업은 보험금 청구 자동화로 고객 만족도를 높입니다. 이러한 변화는 전반적으로 영국 핀테크 업계에서 진행 중인 구조적 재평가가 진행 중임을 보여줍니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05United Kingdom fintech market size in 2026 is estimated at USD 21.44 billion, growing from 2025 value of USD 18.57 billion with 2031 projections showing USD 43.92 billion, growing at 15.42% CAGR over 2026-2031.

Open banking adoption, real-time payments, and a supportive regulatory sandbox framework are expanding addressable demand even as macro-uncertainty reshapes funding patterns. London retains its magnetic pull for venture capital, yet regional hubs in Manchester and Edinburgh are capturing specialized niches. Neobanks move from growth to profitability, while embedded finance deepens retailer-fintech partnerships. Technology adoption, especially artificial intelligence, underpins cost-efficient scale-ups and positions the United Kingdom fintech market for sustained double-digit growth.

United Kingdom Fintech Market Trends and Insights

Open Banking Regulations Accelerate API-Based Payments

Seven million UK consumers actively used open-banking services in 2024, unlocking standardized API access for third-party providers. Mandatory data-sharing spurred a 30% rise in account-to-account transactions and enabled niche payment firms to bypass incumbent card networks. The regulatory design, championed by the Financial Conduct Authority (FCA), positions the United Kingdom fintech market as a benchmark for competition-led innovation. Payment providers now integrate real-time settlement and identity verification, lowering merchant fees and fuelling broader embedded-finance use cases. Elevated interoperability also reduces customer switching friction, intensifying competitive pressure on legacy processors.

Post-Brexit Regulatory Sandboxes Attract Global Entrants

Since 2016, the FCA sandbox has admitted 55 firms, and the Digital Securities Sandbox opened to 12 additional international participants in March 2025. Controlled testing cuts compliance costs and time-to-market, drawing firms from Singapore and the United States. A new AI-testing corridor, announced in January 2025, broadens the scope to algorithmic underwriting and autonomous trading. Cross-border memoranda between the FCA and Canadian, Australian, and Japanese regulators streamline passporting, thereby anchoring the United Kingdom fintech market as a launchpad for multi-jurisdictional scale-ups.

Rising Cloud-Compliance Costs Under UK GDPR and Resilience Rules

Full implementation of operational-resilience mandates by March 2025 requires granular mapping of important business services and severe-but-plausible scenario tests. Fintechs leveraging hyperscale cloud providers must evidence end-to-end controls, increasing audit frequency, and vendor-management expense. The Digital Operational Resilience Act, effective January 2025, layers additional ICT-risk reporting on top of UK GDPR obligations. Smaller firms face trade-offs between feature development and compliance, changing cost curves across the United Kingdom fintech market.

Other drivers and restraints analyzed in the detailed report include:

- Nationwide Faster Payments & RTP Infrastructure Boost Digital Wallet Uptake

- London Talent Pool and Venture Capital Density Catalyze Scale-Ups

- Digital Fraud and APP-Scam Losses Dent Consumer Trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital Payments retained 32.15% of the United Kingdom fintech market size in 2025, yet Neobanking posted the fastest outlook with a 19.18% CAGR to 2031. Record profitability at Revolut and Starling demonstrates viable unit-economics once scale is reached. Revolut secured a UK banking licence in July 2024, expanding deposit-funded margins and improving product cross-sell. Digital Lending to SMEs accelerates as regional credit gaps broaden. Insurtech deploys data analytics to refine underwriting, while Digital Investments benefit from AI-led portfolio visualization. The Bank of England's AI Consortium, launched in September 2024, catalyzes algorithmic innovation across propositions, adding depth to the United Kingdom fintech market.

Customer acquisition costs for neobanks fall as embedded-finance partners bundle accounts inside retail checkout journeys. Profitability inflection points align with higher interchange income and fee-based revenues, such as crypto trading. Alternative lenders leverage open-banking data for cash-flow underwriting, cutting decision times for SMEs. Wealth-tech providers democratize fractional investing, while Insurtech firms automate claims, raising user satisfaction. Collectively, these shifts underline the structural re-rating occurring in the United Kingdom fintech industry.

The United Kingdom Fintech Market is Segmented by Service Proposition (Digital Payments, Digital Lending and Financing, Digital Investments, Insurtech, and Neobanking), by End-User (Retail and Businesses), and by User Interface (Mobile Applications, Web / Browser, and POS / IoT Devices). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Revolut Ltd

- Monzo Bank Ltd

- Wise plc

- Starling Bank Ltd

- Checkout.com

- Zopa Bank Ltd

- OakNorth Bank plc

- Klarna Bank AB (UK Ops)

- Stripe Payments UK Ltd

- GoCardless Ltd

- Atom Bank plc

- Zepz

- PaySafe Group Ltd

- Tide Platform Ltd

- Onfido Ltd

- Soldo Ltd

- Nutmeg Saving & Investment Ltd

- Rapyd Financial Network (UK)

- Funding Circle UK

- PensionBee plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Open Banking Regulations Accelerating API-Based Payment Innovation in UK

- 4.2.2 Post-Brexit UK Regulatory Sandboxes Attracting Global Fintech Expansion

- 4.2.3 Nationwide Faster Payments & RTP Infrastructure Boosting Digital Wallet Adoption

- 4.2.4 London's FinServ Talent Pool & VC Funding Density Catalyzing Fintech Scale-ups

- 4.2.5 SME Demand for Alternative Lending Amid Bank De-Risking in UK Regions

- 4.2.6 Embedded Finance Partnerships with Retailers Scaling Consumer BNPL Penetration

- 4.3 Market Restraints

- 4.3.1 Heightened FCA Scrutiny on Financial Promotions Limiting Fintech Marketing Spend

- 4.3.2 Rising Cloud Compliance Costs under UK GDPR & Operational Resilience Rules

- 4.3.3 Digital Fraud & APP-Scam Losses Eroding Consumer Trust in Neobanks

- 4.3.4 Funding Contraction Post-2022 Valuation Reset Stalling Late-Stage Fintech Rounds

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment & Funding Trend Analysis

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Proposition

- 5.1.1 Digital Payments

- 5.1.2 Digital Lending and Financing

- 5.1.3 Digital Investments

- 5.1.4 Insurtech

- 5.1.5 Neobanking

- 5.2 By End-User

- 5.2.1 Retail

- 5.2.2 Businesses

- 5.3 By User Interface

- 5.3.1 Mobile Applications

- 5.3.2 Web / Browser

- 5.3.3 POS / IoT Devices

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Revolut Ltd

- 6.4.2 Monzo Bank Ltd

- 6.4.3 Wise plc

- 6.4.4 Starling Bank Ltd

- 6.4.5 Checkout.com

- 6.4.6 Zopa Bank Ltd

- 6.4.7 OakNorth Bank plc

- 6.4.8 Klarna Bank AB (UK Ops)

- 6.4.9 Stripe Payments UK Ltd

- 6.4.10 GoCardless Ltd

- 6.4.11 Atom Bank plc

- 6.4.12 Zepz

- 6.4.13 PaySafe Group Ltd

- 6.4.14 Tide Platform Ltd

- 6.4.15 Onfido Ltd

- 6.4.16 Soldo Ltd

- 6.4.17 Nutmeg Saving & Investment Ltd

- 6.4.18 Rapyd Financial Network (UK)

- 6.4.19 Funding Circle UK

- 6.4.20 PensionBee plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment