|

시장보고서

상품코드

1937378

벤젠-톨루엔-자일렌(BTX) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Benzene-Toluene-Xylene (BTX) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

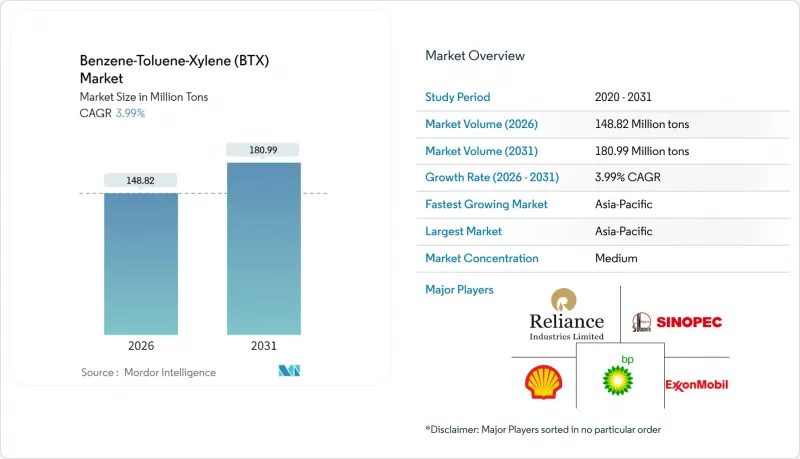

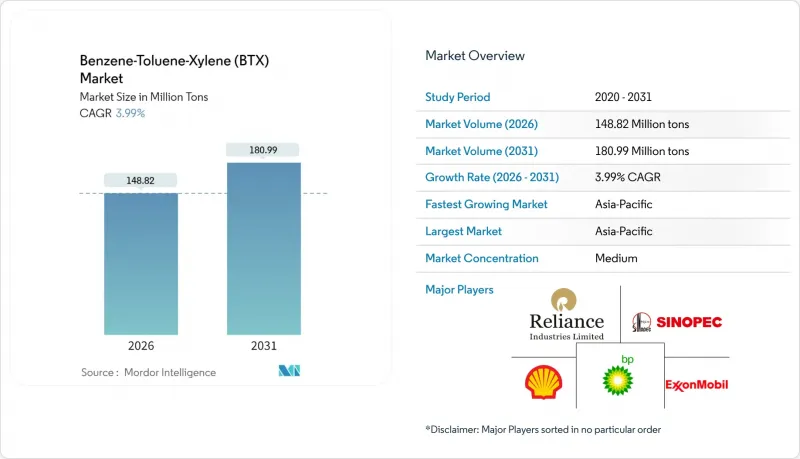

벤젠-톨루엔-자일렌(BTX) 시장 규모는 2026년에는 1억 4,882만 톤으로 추정됩니다.

이는 2025년 1억 4,311만 톤에서 성장한 수치이며, 2031년에는 1억 8,099만 톤에 달할 것으로 예측됩니다. 2026년부터 2031년까지 CAGR 3.99%로 성장할 것으로 예상됩니다.

플라스틱, 합성섬유, 특수 화학제품에 대한 견조한 다운스트림 수요로 인해 전 세계 방향족 단지는 높은 가동률을 유지하고 있습니다. 한편, 아시아태평양의 신규 생산능력 증가는 무역의 흐름을 바꾸고 경쟁 압력을 강화하고 있습니다. PET용 파라자일렌 수요 증가, 폴리우레탄 폼의 톨루엔디 이소시아네이트 수요 회복, 바이오매스 및 파이로플라스틱 공법의 상용화가 결합하여 BTX 시장의 꾸준한 물량 기반 확대를 뒷받침하고 있습니다. 지역 간 불균형이 두드러지는데, 아시아태평양은 원가 우위의 원료를 확보하고 통합형 플랜트를 활용하고 있습니다. 북미는 생산비용 상승과 수입 증가로 어려움을 겪고 있으며, 유럽은 환경규제 강화에 따른 합리화를 추진하고 있습니다. 고비용 사업자는 가격 변동이 심한 환경에서 내성을 추구하기 때문에 경쟁 행동은 원료 통합, 기술 현대화, 선택적 통합으로 향하고 있습니다.

세계 벤젠-톨루엔-자일렌(BTX) 시장 동향과 인사이트

신규 방향족 복합단지 설비투자 붐(아시아-중동)

아시아태평양에서는 2030년까지 545만 톤의 벤젠 생산능력 증설을 계획하고 있으며, 이 중 329만 톤은 인도에서 생산할 예정입니다. 이는 수출 지향적 무역을 위해 설계된 정유소 업그레이드 및 신규 프로젝트에 의해 뒷받침되고 있습니다. 사우디의 다운스트림 통합도 비슷한 궤적을 따르고 있습니다. Aramco Sinopec-Yaslef의 프레임워크는 원료의 시너지 효과를 극대화하기 위해 180만 톤의 혼합원료 크래커와 함께 150만 톤의 방향족 복합시설을 목표로 하고 있습니다. 이러한 투자 붐의 배경에는 규모의 경제, 유리한 나프타 콘덴세이트 공급원, 증가하는 아시아 수요에 대한 근접성 등이 있습니다. 생산능력 확대는 지역 내 자급률을 높이는 한편, 유럽과 북미에서 생산되는 범용 벤젠과 혼합 자일렌 등급의 공급과잉 위험을 증가시킵니다. 따라서 비용 곡선의 변위는 원료 측면에서 우위를 점하고 있는 통합형 사업자에게 유리하게 작용하고, 독립형 고비용 정유사에는 압력을 가할 것입니다.

급증하는 PET 수요로 인해 파라자일렌 수급은 계속 타이트한 상태입니다.

2023년, 중국의 PET병 수지 및 섬유용 파라자일렌 생산능력의 급속한 확장을 배경으로 세계 생산량은 5,700만 톤을 넘어섰습니다. 성숙한 시장에서는 지속가능성 법규에 따라 재생 PET의 채택이 증가하고 있으며, 회수 인프라가 부족한 인구 밀집 지역에서는 신규 파라자일렌에 대한 수요가 지속적으로 증가하고 있습니다. 수급이 타이트한 상황에서 파라자일렌은 혼합 자일렌 원료 대비 프리미엄을 유지하며 벤젠-톨루엔 부문의 수익률 하락을 상쇄하고 있습니다. 생산자 경제는 파라자일렌과 PET의 연동성으로부터 혜택을 받고 있으며, 이러한 연동성은 정유소와 통합 폴리에스테르 체인 간의 장기 계약을 뒷받침하고 있습니다.

발암성에 따른 직업적 노출 규제

벤젠이 1군 발암물질로 분류됨에 따라 작업장 내 노출 한계치가 강화되어 유럽연합(EU)에서는 특정 표면처리 공정에서 20mg/m3까지 낮추었습니다. 규제 준수를 위해서는 지속적인 모니터링, 증기 회수 장치, 활성탄 흡착 시스템 도입이 필요하며, 생산, 저장, 운송의 전 과정에서 운영 비용이 증가합니다. 석유화학 공장에서는 작업자의 안전을 보장하기 위해 밀폐형 로딩 암, 질소 불활성화, 고급 개인보호구에 대한 투자가 이루어지고 있습니다. 이러한 조치는 자본 집약적이지만 사고 위험과 잠재적 법적 책임을 줄이기 위해 BTX 시장에서 운영하기 위한 필수적인 가정입니다.

부문 분석

벤젠은 2025년 BTX 시장에서 38.21%의 점유율을 유지했는데, 이는 포장, 자동차, 건설 분야의 수요를 뒷받침하는 스티렌계 수지, 나일론, 페놀 수지의 가치사슬에 깊숙이 통합된 덕분입니다. 선택적 톨루엔 불균등화, 수소화 탈알킬화, 접촉 개질을 통해 안정적인 공급이 보장되고 있지만, 벤젠의 원가 구조는 경질 나프타의 크랙 가격과 지역 간 조달 격차에 영향을 받기 쉬운 상태입니다. 북미 가동률은 2024년 72% 내외로 유지될 것이며, 마진 축소 전망으로 인해 2025년에는 70% 이하로 떨어질 가능성이 있습니다. 2024년 10월까지 일시적으로 발생한 차익거래 기회로 인해 아시아로부터의 수입이 미국 벤젠 유입량의 60% 이상을 차지했습니다. 그러나 가격 차이가 줄어들면서 이러한 유입량은 감소할 것으로 예상됩니다. 전환의 유연성으로 인해 정제업체는 벤젠과 파라자일렌의 생산을 전환할 수 있지만, 개질 제품의 품질에 대한 물리적 제약으로 인해 한계가 있습니다.

톨루엔은 취급량이 적은 TDI의 회복과 용제 수요의 진화에 힘입어 2031년까지 가장 높은 CAGR 4.44%를 기록할 것으로 예상됩니다. UOP의 타토레이, 중국석유화공(Sinopec)의 MST와 같은 불균등화 기술은 잉여 톨루엔을 고부가가치 벤젠 및 파라자일렌으로 전환하여 유리한 벤젠-톨루엔 스프레드 활용을 목표로 하고 있습니다. 촉매 수명 연장과 수소 소비량 감소로 공정 경제성이 향상되어 중동의 복합시설에서 다운스트림 확장을 위한 자체 벤젠 공급원 확보를 목적으로 한 개조에 대한 관심이 높아지고 있습니다. 자일렌 이성질체는 벤젠과 톨루엔의 공급원을 포괄적으로 연결하는 역할을 합니다. 파라자일렌은 PET 수요의 성장을 뒷받침하고, 오르톡실렌은 PVC 가소제용 무수프탈산의 원료가 되고, 메톡실렌은 이소프탈산 수지의 수요를 뒷받침합니다. 자일렌의 공급량은 개질장치의 처리 강도와 개질 분별 수율에 따라 달라지지만, 부족한 부분은 기회를 포착한 수입으로 보충하고 있어 BTX 시장의 세계화가 진행 중임을 알 수 있습니다.

벤젠-톨루엔-자일렌(BTX) 시장 보고서는 유형별(벤젠, 톨루엔, 자일렌), 용도별(에틸벤젠, 사이클로헥산, 알킬벤젠, 쿠멘, 니트로벤젠, 페인트 및 코팅, 접착제-잉크, 폭발물, 화학 중간체, 용매, 단량체), 지역별(아메리카, 유럽, 아시아태평양, 중동, 아프리카, 유럽, 아시아태평양) 아메리카, 유럽, 아시아태평양, 중동 및 아프리카)로 분류됩니다. 시장 예측은 톤 단위로 제공됩니다.

지역별 분석

아시아태평양은 2025년 BTX 시장에서 62.35%로 압도적인 점유율을 차지했으며, 중국, 인도, 한국의 통합 정유소 및 석유화학 허브를 중심으로 2031년까지 4.12%의 가장 빠른 CAGR을 유지할 것으로 예상됩니다. 중국에서만 2025년 하반기에 신규 자일렌 생산능력 308만 8,000톤을 가동할 계획이며, 주로 자체 PET 라인용 파라자일렌을 타겟으로 하고 있습니다. 인도는 2030년까지 가동될 것으로 알려진 329만 톤의 벤젠 생산능력으로 인해 일반 등급 제품 수출국으로 부상하고 있습니다. 규모의 우위에도 불구하고, 여러 신규 프로젝트가 동시에 가동되기 때문에 이 지역은 공급과잉 위험에 직면해 있습니다. 이는 중국 경쟁사의 지속적인 손실로 인해 HD현대코스모가 1억 4천만 달러에 인수한 사례에서도 알 수 있습니다. 그러나 E-Commerce 중심의 포장 수요 증가, 견조한 자동차 생산, 인프라 사업 등이 안정적인 수요 흡수를 뒷받침하고 있습니다.

북미 BTX 공급 구조는 사니아와 오하이오의 모노스타렌 생산설비 가동 중단으로 인해 축소되는 추세입니다. 이로 인해 지역 내 벤젠 자급률이 낮아지고, 아시아 및 중동으로부터의 수입 의존도가 높아지고 있습니다. 천연가스 기반 에탄 분해에 의한 리포메이트 방향족 생산량 증가는 다운스트림 수요 부진으로 어려움을 겪고 있는 벤젠 시장에서 벤젠 공급을 압박하고 있습니다. 유럽에서는 2023년 이후 방향족 화합물 및 크래커 설비를 1,400만 톤 감축하는 합리화 작업이 진행 중입니다. 사업자들은 탄소 가격제 및 VOC 지침에 대응하기 위해 설비 교체에 나서고 있으며, 수익성 악화에 직면해 있습니다. 정책 주도의 에너지 비용 상승은 경쟁력을 더욱 약화시켜 자산 전환 및 폐쇄를 촉진하고 있습니다.

중동지역은 유리한 나프타-콘덴세이트 공급원을 기반으로 얌부 등의 거점에 신설된 혼합원료 크래커와 통합된 저현금 비용의 BTX 생산이 가능합니다. 수출 지향성은 아프리카 및 남아시아의 수요 부족 해소에 적합하며, 아시아에 대한 지리적 근접성은 운송 수단 선택의 폭을 넓게 유지합니다. 남미와 아프리카는 소규모 수요 지역이지만, 자동차 조립 라인의 생산량 증가와 팬데믹으로 지연된 건설 프로젝트가 재개되면서 그 중요성이 커지고 있습니다. 유리한 지역으로의 BTX 생산의 지리적 재편은 무역 패턴을 재편하고, 역사적으로 세계 수급 격차를 균형 있게 유지해 온 차익거래의 기회를 축소시킬 수 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09Benzene-Toluene-Xylene (BTX) market size in 2026 is estimated at 148.82 Million tons, growing from 2025 value of 143.11 Million tons with 2031 projections showing 180.99 Million tons, growing at 3.99% CAGR over 2026-2031.

Robust downstream demand for plastics, synthetic fibers and specialty chemicals keeps global aromatics complexes operating at high utilization rates, while new capacity in Asia-Pacific shifts trade flows and intensifies competitive pressure. Accelerating para-xylene off-take for PET, resurging toluene di-isocyanate demand from polyurethane foam, and the commercialization of biomass- and pyro-plastic routes collectively reinforce a steady, volume-based expansion of the BTX market. Regional imbalances are pronounced: Asia-Pacific secures cost-advantaged feedstocks and leverages integrated complexes, North America wrestles with elevated production costs and rising imports, and Europe undergoes rationalization in response to tightening environmental regulation. Competitive behavior gravitates toward feedstock integration, technology modernization and selective consolidation as high-cost players seek resilience in a cyclical pricing environment.

Global Benzene-Toluene-Xylene (BTX) Market Trends and Insights

CAPEX boom in new aromatics complexes (Asia and Middle-East)

The Asia-Pacific plans to add 5.45 million tons of additional benzene capacity by 2030, including 3.29 million tons in India, underpinned by refinery upgrades and grassroots projects tailored for export-oriented trade. Saudi downstream integration follows a similar trajectory: the Aramco-Sinopec-Yasref framework targets a 1.5 million-ton aromatics complex colocated with a 1.8 million-ton mixed-feed cracker to maximize feedstock synergy. Economies of scale, advantaged naphtha and condensate streams, and proximity to rising Asian demand underpin this investment wave. While the capacity infusion will deepen regional self-sufficiency, it raises the risk of oversupply for commodity benzene and mixed xylene grades produced in Europe and North America. Cost-curve displacement, therefore, favors integrated, feedstock-advantaged operators and pressures independent, higher-cost refiners.

Surging PET demand keeps para-xylene balances tight

Global para-xylene output topped 57 million tons in 2023 on the back of China's rapid capacity build-out devoted to PET bottle resin and textile filament. Sustainability legislation drives the adoption of recycled PET in mature markets, yet virgin para-xylene volumes continue to rise in populous economies with limited collection infrastructure. Tight balances have sustained para-xylene premiums over mixed xylene feedstocks, offsetting margin weakness in benzene and toluene pools. Producer economics benefit from the para-xylene-PET linkage, and the dynamic supports long-range contracts between refineries and integrated polyester chains.

Carcinogenicity-driven occupational exposure curbs

Benzene's classification as a Group 1 carcinogen underpins workplace exposure limits that tighten to as low as 20 mg/m3 for certain surface-treatment operations in the European Union. Compliance requires continuous monitoring, vapor recovery units, and active-carbon adsorption systems, adding operating costs across production, storage, and transport. Petrochemical sites invest in hermetic loading arms, nitrogen inerting, and advanced personal protective equipment to safeguard workers. Although capital-intensive, these measures reduce incident risk and potential liabilities, making compliance an essential prerequisite for operating in the BTX market.

Other drivers and restraints analyzed in the detailed report include:

- Automotive and construction rebound lifts TDI/paints solvent demand

- Refinery-petchem integration unlocking captive BTX extraction

- Paints/adhesives VOC regulations favor low-aromatic blends

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Benzene retained a 38.21% BTX market share in 2025, supported by deep integration into styrenics, nylon, and phenolics value chains that anchor demand across packaging, automotive, and construction. Selective toluene disproportionation, hydrodealkylation, and catalytic reforming ensure a steady supply, yet benzene's cost structure remains vulnerable to light-naphtha cracks and regional sourcing disparities. North American operating rates drifted near 72% in 2024, and forecast margin compression could push utilization below 70% in 2025. Imports from Asia supplied more than 60% of U.S. benzene inflows through October 2024 as arbitrage windows briefly opened; parity pricing is expected to narrow those inflows. Conversion flexibility allows refiners to swing between benzene and para-xylene, but physical constraints on reformate quality impose limits.

Toluene, although representing a smaller volume base, exhibits the fastest 4.44% CAGR through 2031, driven by the recovery of TDI and the evolution of solvent demand. Disproportionation technologies such as UOP's Tatoray and Sinopec's MST aim to exploit favorable benzene-toluene spreads by converting surplus toluene into high-value benzene and para-xylene. Improved catalyst lifetimes and lower hydrogen consumption enhance process economics, prompting retrofit interest among Middle Eastern complexes targeting captive benzene supply for downstream expansions. Xylene isomers collectively bridge the benzene and toluene pools: para-xylene captures PET growth, ortho-xylene feeds phthalic anhydride for PVC plasticizers, and meta-xylene underpins isophthalic resin demand. Although xylene availability follows reformer severity and reformate fractionation yields, opportunistic imports accommodate shortfalls, underscoring the increasingly globalized BTX market.

The Benzene-Toluene-Xylene (BTX) Market Report is Segmented by Type (Benzene, Toluene, and Xylene), Application (Ethylbenzene, Cyclohexane, Alkylbenzene, Cumene, Nitrobenzene, Paints and Coatings, Adhesives and Inks, Explosives, Chemical Intermediates, Solvents, Monomer), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

The Asia-Pacific region held a commanding 62.35% BTX market share in 2025 and sustained the fastest 4.12% CAGR to 2031, driven by integrated refinery-petrochemical hubs in China, India, and South Korea. China alone plans to schedule 3.088 million tons of new xylene capacity for H2 2025, primarily targeting para-xylene for captive PET lines. India's 3.29 million tons of benzene capacity announced for start-up by 2030 positions the country as a rising exporter of merchant grades. Despite its scale advantages, the region faces an oversupply risk as multiple grassroots projects come online concurrently, as evidenced by HD Hyundai Cosmo's acquisition for USD 104 million, following sustained losses attributed to Chinese competition. Nonetheless, e-commerce-led packaging growth, resilient automotive output, and infrastructure programs underpin steady volume absorption.

North America's BTX supply landscape contracts as styrene monomer units in Sarnia and Ohio shut down, lowering regional benzene self-sufficiency and increasing import reliance from Asia and the Middle East. Elevated natural-gas-based ethane cracking caps reformate aromatics output, squeezing benzene supply in a market already challenged by flat downstream demand. Europe continues a rationalization pathway that removed 14 million tons of aromatics and cracker capacity since 2023; operators confront carbon-pricing schemes and VOC directives requiring plant upgrades that strain return profiles. Policy-driven energy costs further erode competitiveness, prompting asset swaps or closures.

The Middle East rests on advantaged naphtha and condensate streams, enabling low cash-cost BTX production integrated with new mixed-feed crackers at sites such as Yanbu. Export orientation suits emerging deficits in Africa and South Asia, while proximity to Asia keeps freight optionality wide open. South America and Africa comprise smaller demand centers but gain relevance as automotive assembly lines ramp up and building projects resume following pandemic-delayed timelines. The geographic restructuring of BTX production toward advantaged regions reshapes trade patterns and might compress arbitrage windows that historically balanced global deficits.

- BASF

- BP p.l.c.

- Chevron Phillips Chemical Company LLC

- China Petrochemical Corporation

- China National offshore Oil Corporation (CNOOC)

- Dow

- ENEOS Corporation

- Exxon Mobil Corporation

- Formosa Plastics Group.

- GS Caltex Corporation

- INEOS

- IRPC Public Company Limited

- JFE Chemical Corporation

- JX Nippon Oil & Gas Exploration Corporation (ENEOS)

- Mitsubishi Gas Chemical Trading, Inc.

- MOLGROUP

- OCI COMPANY Ltd.

- Reliance Industries Limited

- SABIC

- Shell plc

- S-OIL CORPORATION

- TotalEnergies

- YEOCHUN NCC CO., LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CAPEX boom in new aromatics complexes (Asia and Middle-East)

- 4.2.2 Surging PET demand keeps para-xylene balances tight

- 4.2.3 Automotive and construction rebound lifts TDI/paints solvent demand

- 4.2.4 Refinery-petchem integration unlocking captive BTX extraction

- 4.2.5 Pyro-plastic and biomass routes commercialising drop-in BTX

- 4.3 Market Restraints

- 4.3.1 Carcinogenicity-driven occupational exposure curbs

- 4.3.2 Paints/adhesives VOC regulations favour low-aromatic blends

- 4.3.3 Octane-for-aromatics trade-off in gasoline pool after E10 rollout

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Benzene

- 5.1.2 Toluene

- 5.1.3 Xylene

- 5.1.3.1 Ortho-xylene

- 5.1.3.2 Meta-xylene

- 5.1.3.3 Para-xylene

- 5.2 By Application

- 5.2.1 Benzene

- 5.2.1.1 Ethylbenzene

- 5.2.1.2 Cyclohexane

- 5.2.1.3 Alkylbenzene

- 5.2.1.4 Cumene

- 5.2.1.5 Nitrobenzene

- 5.2.1.6 Other Applications

- 5.2.2 Toluene

- 5.2.2.1 Paints and Coatings

- 5.2.2.2 Adhesives and Inks

- 5.2.2.3 Explosives

- 5.2.2.4 Chemical Intermediates

- 5.2.3 Xylenes

- 5.2.3.1 Solvents

- 5.2.3.2 Monomer

- 5.2.3.3 Other Applications

- 5.2.1 Benzene

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BASF

- 6.4.2 BP p.l.c.

- 6.4.3 Chevron Phillips Chemical Company LLC

- 6.4.4 China Petrochemical Corporation

- 6.4.5 China National offshore Oil Corporation (CNOOC)

- 6.4.6 Dow

- 6.4.7 ENEOS Corporation

- 6.4.8 Exxon Mobil Corporation

- 6.4.9 Formosa Plastics Group.

- 6.4.10 GS Caltex Corporation

- 6.4.11 INEOS

- 6.4.12 IRPC Public Company Limited

- 6.4.13 JFE Chemical Corporation

- 6.4.14 JX Nippon Oil & Gas Exploration Corporation (ENEOS)

- 6.4.15 Mitsubishi Gas Chemical Trading, Inc.

- 6.4.16 MOLGROUP

- 6.4.17 OCI COMPANY Ltd.

- 6.4.18 Reliance Industries Limited

- 6.4.19 SABIC

- 6.4.20 Shell plc

- 6.4.21 S-OIL CORPORATION

- 6.4.22 TotalEnergies

- 6.4.23 YEOCHUN NCC CO., LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment