|

시장보고서

상품코드

1937400

동남아시아의 컨설팅 서비스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South-East Asia Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

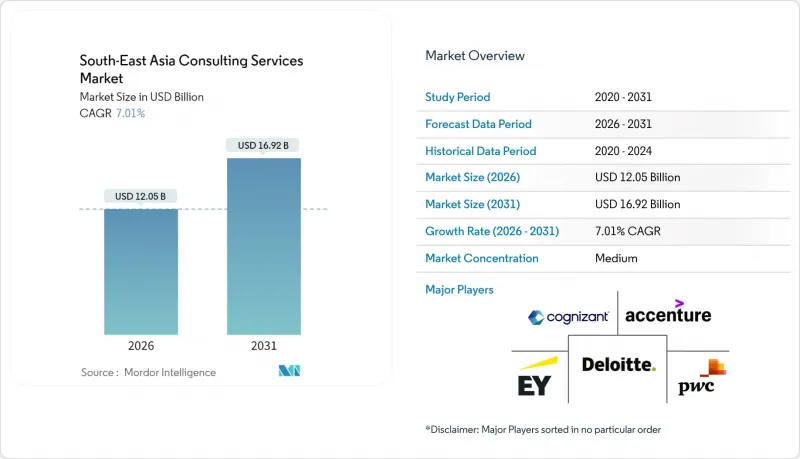

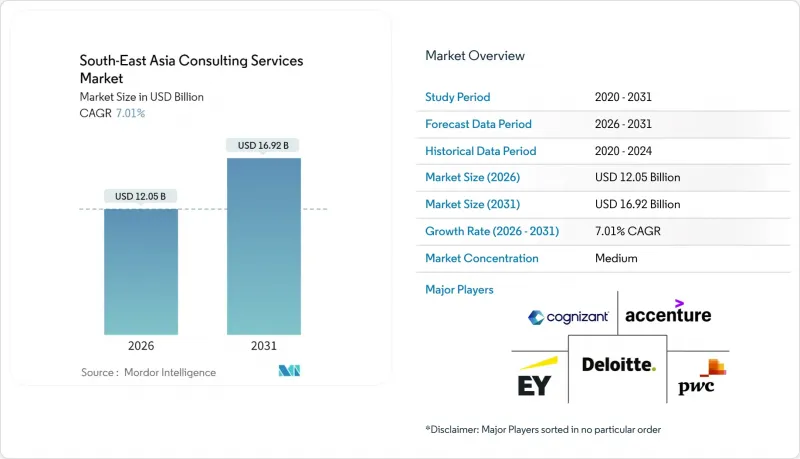

동남아시아의 컨설팅 서비스 시장 규모는 2026년에 120억 5,000만 달러로 추정됩니다.

이는 2025년 112억 6,000만 달러에서 성장한 수치이며, 2031년에는 169억 2,000만 달러에 달할 것으로 예측됩니다. 2026년부터 2031년까지 CAGR 7.01%로 확대될 것으로 예상됩니다.

아세안 10개국 전체에서 컨설팅 수요를 확대하는 주요 요인은 정부 주도의 견고한 디지털화 로드맵, 의무화된 지속가능성 보고, 그리고 중소기업의 급속한 성장입니다. 레거시 애플리케이션의 현대화와 AI 플랫폼 통합을 서두르는 기업들은 IT 및 디지털 컨설팅 분야에 가장 큰 지출을 집중하고 있습니다. 한편, 투명성 높은 환경 정보 공개가 촉진되면서 지속가능성 및 ESG 컨설팅에 대한 수요가 확대되고 있습니다. 동시에 단발성 프로젝트에서 구독형 자문 모델로의 전환이 진행되어 지속적인 지원을 원하는 고객의 니즈에 따라 수익 사이클이 재구성되고 있습니다. 클라우드 네이티브 딜리버리 및 독립형 인재 플랫폼을 활용하는 전문 컨설팅 회사가 가격과 기동성에서 기존 기업에 도전장을 내밀고 있습니다. 또한, 중국+1 공급망 재편으로 제조업이 베트남, 태국, 말레이시아로 진출하면서 국경을 초월한 규제 대응 업무에 대한 수요가 창출되고 있습니다.

동남아시아 컨설팅 서비스 시장 동향과 인사이트

디지털 퍼스트 트랜스포메이션 프로그램

싱가포르의 '스마트 국가 구상', 말레이시아의 '디지털 투자청'과 같은 정부 프로그램은 지역 전체의 혁신 프로젝트에 총 4,800억 달러를 투자하고 있습니다. 인도네시아가 27,000개의 공공부문 앱을 9개의 슈퍼 앱으로 통합하려는 계획은 전문적인 자문을 필요로 하는 변경 관리, 사이버 보안, 클라우드 마이그레이션 업무의 복잡성을 여실히 보여줍니다. 싱가포르의 Analytics.gov 플랫폼은 현재 1,600명 이상의 공공부문 사용자를 지원하고 있으며, 데이터 거버넌스, AI 모델 구축, 다기관 프로세스 조정에 필요한 컨설팅 업무의 중요성을 강조하고 있습니다. 태국 전력공사는 전력망 최적화를 위해 PLEXOS를 채택하여 에너지 사업 전반에 걸쳐 자원 계획 컨설팅에 대한 수요가 증가하고 있음을 보여주고 있습니다. 이러한 노력은 엔터프라이즈 아키텍처, 거버넌스, 인력 역량 강화와 관련된 다년간의 계약이 동남아시아 컨설팅 서비스 시장에서 안정적인 수익원이 될 수 있는 이유를 입증하고 있습니다.

급성장하는 중소기업과 스타트업이 필요로 하는 확장성 있는 조언 제공

아세안 기업의 97%를 차지하는 중소기업(MSME)은 3,000억 달러의 자금 부족에 직면해 있으며, 정부 및 지원 기관은 컨설팅 지원 접근을 보조하고 있다[HSBC.com]. 기존 하루 350-1,500달러보다 훨씬 저렴한 구독 모델이 확산되면서 기업가들은 하루 250-1,600달러의 독립적인 전문가의 온콜 지도를 확보할 수 있게 되었습니다. InnoVen Capital의 190건의 대출로 뒷받침되는 베트남의 벤처 생태계는 고성장 스타트업의 자금 조달, 유닛 이코노미, 시장 진입 전략 컨설팅에 대한 높은 수요를 보여주고 있습니다. 아세안 사회적 기업 개발 프로그램 4.0과 같은 제도적 프로그램은 최대 4만 달러의 교육 및 종자 보조금을 제공하여 컨설팅 고객 기반을 더욱 확장하고 있습니다. 창업자들이 지속가능한 수익성을 우선시하는 가운데, 자본 효율성과 ESG 통합에 정통한 컨설턴트에 대한 수요가 증가하면서 동남아시아 컨설팅 서비스 시장의 장기적인 성장 모멘텀이 강화되고 있습니다.

기업 내 컨설팅 부문 확대

DBS 등 금융기관들은 일상적인 분석 업무, 사이버 보안, DevOps 업무에서 외부 자문사에 대한 의존도를 낮추기 위해 사내 디지털 전환 팀을 육성하고 있습니다. 이러한 전담 부서는 조직적 노하우가 축적되고 기업 문화와 긴밀하게 연계되어 실행 속도에서 외부 컨설턴트와 동등하거나 그 이상의 성과를 내는 사례가 늘고 있습니다. 이 모델을 채택하는 기업이 늘어남에 따라 일상적인 자문 업무의 일부가 사내로 이전되고, 상품화된 서비스의 매출 성장이 둔화되고 있습니다. 하지만, 복잡한 다시장 변화, 낯선 규제 변화, 독립적인 이사회의 감사 등은 여전히 외부의 객관성을 요구하고 있으며, 고부가가치 프로젝트에 대한 수요는 여전히 유지되고 있습니다. 컨설팅 기업은 전문성 강화와 사내 팀에서 재현하기 어려운 성과연동형 계약 제공으로 대응하고 있습니다.

부문 분석

IT 및 디지털 컨설팅은 2025년 매출의 37.02%를 차지할 것으로 예상되며, 기업들이 레거시 스택 폐기, 클라우드 네이티브 아키텍처 채택, AI 워크로드 배포를 서둘러야 할 필요성을 강조하고 있습니다. 동남아시아의 컨설팅 서비스 시장 규모는 하이퍼스케일 클라우드 투자와 공공 부문의 디지털화 요구에 따라 꾸준히 확대될 것으로 예상됩니다. 지속가능성 및 ESG 컨설팅은 17.55%의 CAGR로 성장하고 있으며, 싱가포르의 2025년 ESG 보고 의무화 및 태국의 FTSE 러셀 기준에 따른 SET ESG 등급 리브랜딩에 힘입어 성장세를 보이고 있습니다. 고객들은 디지털과 ESG를 통합한 로드맵을 강력하게 요구하고 있으며, 기업들은 기술자들에게 탄소 회계 프레임워크에 대한 교차 교육을 실시하고 있습니다. 전략 및 업무 컨설팅은 제조업의 '중국+1' 전략 전환의 혜택을 누리고, 리스크 및 컴플라이언스 자문은 데이터 현지화 방법의 차이로 인한 배포 아키텍처의 분열을 활용하고 있습니다. HR 컨설팅은 기술직의 30-70%가 미충원된 상황에서 인력분석 및 인력계획 프로젝트를 추진하며 견조한 성장세를 유지하고 있습니다.

컨설팅 기업들은 현재 AI 코파일럿을 도입하여 문서 검토 및 시나리오 모델링을 자동화함으로써 스프린트 주기를 단축하고 자문 마진을 개선하고 있습니다. 택트 소셜 컨설팅(Tact Social Consulting)과 같은 기업은 하이퍼스케일러와 제휴하여 클라우드 크레딧과 ESG 어드바이저리를 묶어 태국 전역의 기업 파일럿 프로젝트를 수주하고 있습니다. 성과 기반 요금 체계가 시간당 요금 모델을 대체하는 가운데, 공급자들은 비용 절감, 위험 감소 또는 탄소 감축 지표를 통해 가치를 정량화하고 있으며, 이는 투명성을 추구하는 CFO들의 공감을 불러일으키는 접근 방식입니다. 동남아시아 컨설팅 서비스 시장에서 디지털 어드바이저리 매출 비중은 지속가능성 업무의 급격한 증가에도 불구하고 2031년까지 35% 이상을 유지할 것으로 예측됩니다. 이는 기술과 ESG의 요구가 융합된 지속적인 쌍끌이 성장 패턴을 보여주고 있습니다.

금융 서비스 분야는 2025년 지출의 27.05%를 차지할 것이며, 종합적인 디지털 뱅킹 로드맵, 오픈 API 지원, 엄격한 자금세탁방지 대책이 그 기반이 될 것입니다. 태국의 KB은행 산하 KBTG와 베트남의 MSB-Backbase 제휴는 옴니채널 플랫폼과 AI 기반 신용 엔진에 대한 기관투자의 상징입니다. 에너지 및 유틸리티 분야는 14.06%의 CAGR로 가장 빠른 성장세를 보이고 있으며, 태국의 PLEXOS 도입, 인도네시아 동자바 최초의 디지털 변전소 등 송전망 현대화 및 재생에너지 통합 프로젝트가 주도하고 있습니다. 제조업 컨설팅 수요는 전자기기, 자동차 기업이 공급망 재구축을 추진하면서 급증. 한편, 통신사들은 5G와 데이터센터 확충에 고액의 설비투자를 집중하면서 인프라 자문사를 끌어들이고 있습니다.

인도네시아의 9대 슈퍼앱 통합으로 정부 및 공공부문 프로젝트가 급증하면서 프로그램 관리 사무소, 사이버 보안, 서비스 디자인 전문 지식에 대한 수요가 증가하고 있습니다. 소매 및 E-Commerce 분야에서는 모바일 지갑이 2025년까지 4억 4,000만 계정으로 증가할 것으로 예상되는 가운데, 고객 경험의 재설계와 사기 분석에 초점을 맞추고 있습니다. 의료 서비스 제공자들은 청구 처리 시간을 단축하고 환자 분류를 개선하기 위해 클라우드로의 전환을 추진하고 있으며, HIPAA를 준수하는 대체 솔루션과 레거시 시스템 폐지에 대한 컨설팅 기회가 생겨나고 있습니다. 이러한 분야가 결합되어 견조한 프로젝트 파이프라인을 유지하고 있으며, 이는 동남아시아 컨설팅 서비스 시장이 아시아 신흥 경제권에서 자문 사업의 중심지임을 다시 한 번 입증하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The South-East Asia consulting services market size in 2026 is estimated at USD 12.05 billion, growing from 2025 value of USD 11.26 billion with 2031 projections showing USD 16.92 billion, growing at 7.01% CAGR over 2026-2031.

Robust government-led digitalization roadmaps, mandatory sustainability reporting, and rapid SME formation are the primary forces expanding advisory demand across the ten ASEAN member states. Enterprises racing to modernize legacy applications and integrate AI platforms are channeling the largest spending into IT and Digital Consulting, while the push for transparent environmental disclosures propels Sustainability and ESG advisory uptake. Concurrently, a pivot from episodic projects to subscription-based advisory models is reshaping revenue cycles as clients favor continuous support. Boutiques leveraging cloud-native delivery and independent talent platforms now challenge incumbents on price and agility, while China+1 supply-chain realignment sends manufacturers to Vietnam, Thailand, and Malaysia, unlocking cross-border regulatory workstreams.

South-East Asia Consulting Services Market Trends and Insights

Digital-first Transformation Programmes

Government programmes such as Singapore's Smart Nation initiative and Malaysia's Digital Investment Office are collectively injecting USD 48 billion into regional transformation projects . Indonesia's plan to merge 27,000 public-sector apps into nine super-apps exemplifies the complexity of change management, cybersecurity, and cloud migration tasks that demand specialized advice. Singapore's Analytics.gov platform, now supporting more than 1,600 public-sector users, highlights the consultative work required to govern data, build AI models, and align multi-agency processes. Thailand's electricity authority chose PLEXOS for grid optimization, signaling rising need for resource-planning advisory across energy utilities. Together these initiatives demonstrate why multi-year engagements around enterprise architecture, governance, and talent upskilling form a resilient revenue stream for the South-East Asia consulting services market.

SME and Start-up Boom Demanding Scalable Advice

Ninety-seven percent of ASEAN businesses are MSMEs, and they face a USD 300 billion funding deficit, prompting governments and donors to subsidize advisory access [HSBC.COM]. Subscription models priced well below the traditional USD 350-1,500 daily rate are gaining ground, enabling founders to secure on-call guidance using independent experts billing USD 250-1,600 per day. Vietnam's venture ecosystem, supported by InnoVen Capital's 190 loans, illustrates the appetite for fundraising, unit economics, and go-to-market consulting among high-growth startups. Institutional programs such as the ASEAN Social Enterprise Development Programme 4.0 supply training and seed grants up to USD 40,000, further widening the advisory client base. As founders prioritize sustainable profitability, demand rises for consultants versed in capital efficiency and ESG integration, reinforcing long-term momentum for the Southeast Asia consulting services market.

Corporate In-house Consulting Build-outs

Financial institutions such as DBS have cultivated internal digital-transformation squads, reducing dependence on third-party advisors for day-to-day analytics, cybersecurity, and DevOps mandates. These captive units accumulate institutional knowledge and align tightly with corporate culture, often matching or outpacing external consultants on speed of execution. As more enterprises replicate the model, a portion of routine advisory spend migrates in-house, trimming revenue growth for commoditized services. However, complex multi-market transformations, unfamiliar regulatory changes, and independent board-mandated reviews still require external objectivity, preserving scope for high-value engagements. Consulting firms are responding by deepening specialization and offering outcome-based contracts that internal teams struggle to replicate.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of AI, Analytics and Cloud Platforms

- Government Digital-Economy Road-maps and FDI Inflows

- Price Erosion from Commoditized Offerings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT and Digital Consulting contributes 37.02% of 2025 revenue, underscoring enterprise urgency to decommission legacy stacks, adopt cloud-native architectures, and deploy AI workloads. The Southeast Asia consulting services market size for this segment is forecast to expand steadily alongside hyperscale cloud investments and public-sector digital mandates. Sustainability and ESG Consulting, growing at an 17.55% CAGR, gains momentum from Singapore's 2025 compulsory ESG reporting and Thailand's re-branded SET ESG Ratings that align with FTSE Russell standards . Clients increasingly demand integrated digital-plus-ESG roadmaps, prompting firms to cross-train technologists in carbon-accounting frameworks. Strategy and Operations Consulting benefits from manufacturers' China+1 shifts, while Risk and Compliance advisors capitalize on divergent data-localization laws that fragment deployment architectures. HR Consulting remains resilient as 30-70% of tech roles sit vacant, driving projects in talent analytics and workforce planning.

Consultancies now embed AI copilots into delivery, automating document review and scenario modeling, thus shortening sprint cycles and elevating advisory margins. Firms like Tact Social Consulting partner with hyperscalers to bundle cloud credits with ESG advisory, winning enterprise pilots across Thailand. As output-based fees displace billable-hour models, providers quantify value via cost savings, risk mitigation, or carbon-reduction metrics, an approach that resonates with CFOs seeking transparency. The South-East Asia consulting services market share of digital advisory revenue is projected to hold above 35% through 2031 despite the surge in sustainability work, indicating a durable dual-track growth pattern that fuses technology and ESG imperatives.

Financial Services represented 27.05% of 2025 spending, anchored by exhaustive digital banking roadmaps, open-API compliance, and stringent anti-money-laundering rules. KBank's KBTG unit and Vietnam's MSB-Backbase partnership are emblematic of institutions investing in omnichannel platforms and AI-enabled credit engines. Energy and Utilities produces the fastest expansion at 14.06% CAGR, fueled by grid modernization and renewable-integration projects such as Thailand's PLEXOS deployment and Indonesia's first digital substation in East Java. Manufacturing consulting demand swells as electronics and automotive firms replot supply chains, while telecom operators channel big-ticket capex into 5G and data-center buildouts, attracting infrastructure advisory.

Government and Public Sector engagements escalate with Indonesia's nine-super-app consolidation, pushing requirements for program management offices, cybersecurity, and service-design expertise. Retail and E-commerce assignments focus on customer-journey redesign and fraud analytics as mobile wallets multiply to an expected 440 million accounts by 2025. Healthcare providers pursue cloud migrations to compress claims-processing times and improve patient triage, opening avenues for HIPAA-analog compliance and legacy-system decommissioning consulting. Collectively, these verticals sustain a robust pipeline, reaffirming the South-East Asia consulting services market as the advisory hotspot within emerging Asian economies.

The Southeast Asia Consulting Services Market Report is Segmented by Service Type (HR Consulting, Financial Consulting, and More), End-User Industry (Financial Services, Life Sciences and Healthcare, IT and Telecommunications, and More), Consulting Model (Project-Based Advisory, Retainer-Based Advisory, and More), Firm Size (SMEs, and Large Enterprises), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- PricewaterhouseCoopers International Limited (PwC)

- Ernst and Young Global Limited

- KPMG International Limited

- McKinsey & Company, Inc.

- Boston Consulting Group, Inc.

- Bain & Company, Inc.

- Cognizant Technology Solutions Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- Mercer LLC

- Aon plc

- Protiviti Inc.

- A.T. Kearney, Inc.

- Roland Berger Holding GmbH

- L.E.K. Consulting LLC

- Frost & Sullivan, Inc.

- RSM International Limited

- YCP Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital-first transformation programmes

- 4.2.2 SME and start-up boom demanding scalable advice

- 4.2.3 Adoption of AI, analytics and cloud platforms

- 4.2.4 Government digital-economy road-maps and FDI inflows

- 4.2.5 Mandatory ESG-reporting fuelling sustainability advisory

- 4.2.6 China+1 supply-chain realignment into ASEAN

- 4.3 Market Restraints

- 4.3.1 Corporate in-house consulting build-outs

- 4.3.2 Price erosion from commoditised offerings

- 4.3.3 Shortage of bilingual domain experts

- 4.3.4 Data-sovereignty and residency barriers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 HR Consulting

- 5.1.2 Financial Consulting

- 5.1.3 IT and Digital Consulting

- 5.1.4 Strategy and Operations Consulting

- 5.1.5 Risk and Compliance Consulting

- 5.1.6 Sustainability and ESG Consulting

- 5.2 By End-user Industry

- 5.2.1 Financial Services

- 5.2.2 Life Sciences and Healthcare

- 5.2.3 IT and Telecommunications

- 5.2.4 Government and Public Sector

- 5.2.5 Energy and Utilities

- 5.2.6 Manufacturing

- 5.2.7 Retail and E-commerce

- 5.3 By Consulting Model

- 5.3.1 Project-based Advisory

- 5.3.2 Retainer-based Advisory

- 5.3.3 Managed Services / Outsourcing

- 5.3.4 Advisory-as-a-Service (Subscription)

- 5.4 By Firm Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Country

- 5.5.1 Singapore

- 5.5.2 Indonesia

- 5.5.3 Thailand

- 5.5.4 Vietnam

- 5.5.5 Philippines

- 5.5.6 Malaysia

- 5.5.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Limited

- 6.4.3 PricewaterhouseCoopers International Limited (PwC)

- 6.4.4 Ernst and Young Global Limited

- 6.4.5 KPMG International Limited

- 6.4.6 McKinsey & Company, Inc.

- 6.4.7 Boston Consulting Group, Inc.

- 6.4.8 Bain & Company, Inc.

- 6.4.9 Cognizant Technology Solutions Corporation

- 6.4.10 Tata Consultancy Services Limited

- 6.4.11 Wipro Limited

- 6.4.12 Mercer LLC

- 6.4.13 Aon plc

- 6.4.14 Protiviti Inc.

- 6.4.15 A.T. Kearney, Inc.

- 6.4.16 Roland Berger Holding GmbH

- 6.4.17 L.E.K. Consulting LLC

- 6.4.18 Frost & Sullivan, Inc.

- 6.4.19 RSM International Limited

- 6.4.20 YCP Holdings Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment