|

시장보고서

상품코드

1937426

에어 브레이크 시스템 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Air Brake System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

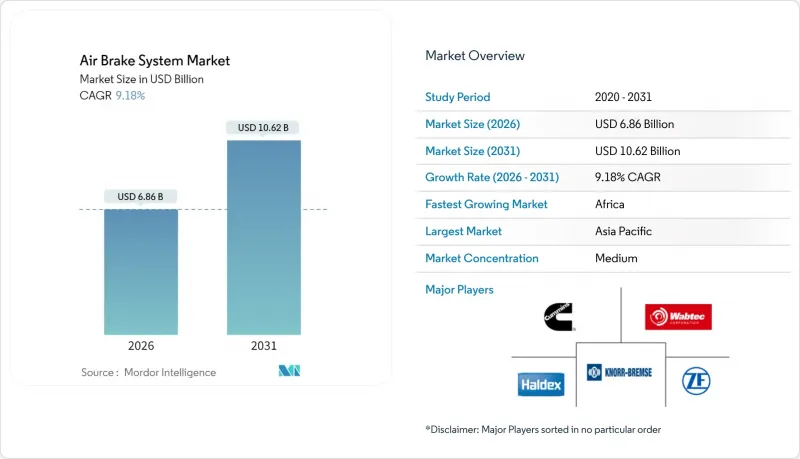

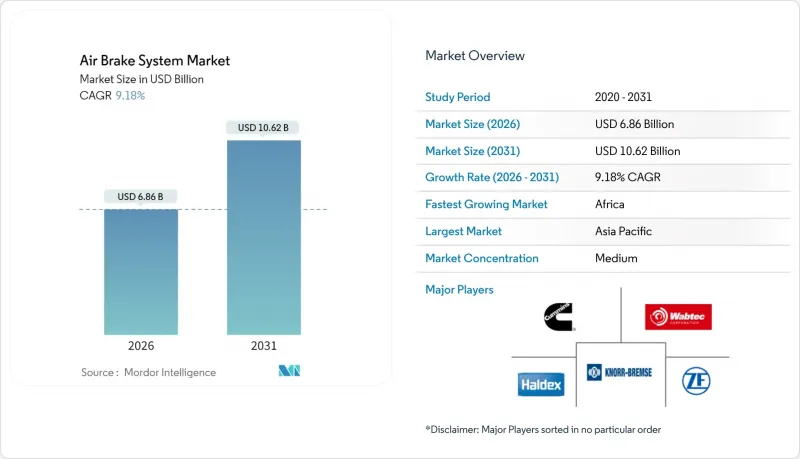

세계의 에어 브레이크 시스템 시장은 2025년에 62억 8,000만 달러로 평가되었으며, 2026년 68억 6,000만 달러에서 2031년까지 106억 2,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 9.18%로 예상됩니다.

미국 환경보호청(EPA)이 2027년형부터 도입하는 대형 차량에 대한 3단계 온실가스 규제 등 규제 요인으로 인해 디젤 및 무공해 파워트레인에 대응하는 전기공압식 아키텍처에 대한 OEM 투자가 가속화되고 있습니다. ADAS(첨단 운전자 보조 시스템)의 통합으로 정밀한 제동 성능에 대한 요구가 더욱 높아지고 있으며, 공급업체들은 자동긴급제동(AEB) 기능과 연동되는 전자제어장치(ECU)와 센서 제품군을 개발해야 하는 상황에 직면해 있습니다. 컴프레서의 재설계는 엔진 구동식에서 전동식으로 전환하여 기생 손실을 줄이고, 수소 연료전지 및 배터리 전기자동차에 대응할 수 있도록 하였습니다. 이러한 기술적 전환점과 총소유비용(TCO) 절감에 대한 차량 수요는 주요 에어 브레이크 시스템 시장 지역 전체에서 장거리 운송 애플리케이션을 위한 조달 선택이 디스크 브레이크 또는 하이브리드 구성으로 기울어지면서 경쟁의 역학이 재편되고 있습니다.

세계 에어 브레이크 시스템 시장 동향 및 인사이트

전동화 대응 공압 아키텍처

자동차 제조업체들은 공압 회로가 배터리 전기 및 수소 연료전지 구동 시스템과 원활하게 통합될 수 있도록 브레이크 시스템을 재설계하고 있습니다. ZF는 약 500만 대의 브레이크 바이 와이어 하드웨어를 도입하는 주문을 받아 대규모 도입의 실용성을 입증하고, 차량에 회생제동 대응을 위한 즉각적인 경로를 제공했습니다. 캐나다 정부가 VMAC의 고전압 컴프레서 프로그램을 지원한 것은 전기식 보조 부품에 대한 국가적 우선순위를 보여주는 것입니다. 전기식 컴프레서는 크랭크샤프트의 저항을 제거하여 항속거리 향상과 탄소배출 강도를 낮출 수 있습니다. 한편, 통합된 열 관리 소프트웨어는 재생 브레이크와 마찰 브레이크를 연동하여 반복적인 정지 시 열 축적을 방지합니다. 이러한 시스템이 유럽의 파일럿 차량에서 세계 양산으로 전환되는 가운데, 모듈식 전기 컴프레서 플랫폼을 장악하는 공급업체는 전체 에어 브레이크 시스템 시장에서 지속적인 소프트웨어 업데이트를 통해 수익원을 확보할 수 있습니다.

무공해 대형 트럭에 대한 규제 추진

미국 환경보호청(EPA)의 3단계 기준은 2032년까지 8등급 트럭의 이산화탄소 배출량을 25% 감축하는 것을 목표로 하고 있으며, 캘리포니아주의 선진적인 클린 트럭 규제와 연계하여 제조업체에 오일 프리 운전을 위한 공압 시스템 재설계를 요구하고 있습니다. 유럽연합(EU)의 CO2 기준도 비슷한 목표를 가지고 있으며, 에너지 효율이 높은 브레이크 시스템을 장착한 차량에 인센티브를 부여하는 규정 준수 인센티브를 포함하고 있습니다. 공급업체는 윤활식 컴프레서를 드라이 러닝 유닛으로 교체하는 한편, 전기 회생 사이클에 따른 수요 변동에 대응하기 위해 공기 저장 용량을 확대해야 합니다. 10년 후를 내다본 규제 명확화로 수소 시제품의 선주문이 촉진되고, 낮은 작동 사이클에서도 정밀한 압력을 유지하는 전기 공기 밸브의 채택이 가속화되면서 에어 브레이크 시스템 시장에도 영향을 미치고 있습니다.

에어 브레이크 라인과 밸브의 높은 유지보수 비용

전자식 밸브와 센서의 증가로 인해 정비소 청구액이 증가하고 있으며, 특히 보정된 진단 도구가 없는 차량에서 정비소 청구액이 증가하고 있습니다. Knorr-Bremse는 2024년 상용차 매출의 30.1%를 애프터마켓 수익이 차지할 것으로 예상하며, 서비스 수요 증가를 강조했습니다(knorr-bremse.com). Bendix의 ACom AE 툴은 전 세계 확장 가능한 공기 처리 모듈을 위한 고장 코드 오버레이를 제공하지만, 기술자가 새로운 인증을 받아야 하기 때문에 신흥 경제국에서의 도입 속도를 제한하고 있습니다. 고사양 나일론 호스, 수분 분리 카트리지, 펌웨어 라이선스 비용과 같은 추가적인 지속적인 비용이 에어 브레이크 시스템 시장의 단기적인 성장을 억제하고 있습니다.

부문 분석

에어 드럼 브레이크 설계는 비용 효율성과 서비스 측면에서 광범위한 인지도를 반영하여 2025년 에어 브레이크 시스템 시장 규모의 45.78%를 차지했습니다. 디스크식은 NHTSA의 제동거리 규제 강화 이후 장거리 트랙터에 보급되었으나, 절대적인 수량에서는 드럼식을 밑돌고 있습니다. 전기공압식 서브부문은 현재 극히 일부이지만, AEB(자동긴급제동), 차선유지지원, 군집주행 테스트에서 밀리초 단위의 압력 제어가 요구됨에 따라 8.55%의 CAGR로 가장 빠르게 성장하고 있습니다. 하이브리드 드럼-디스크 구성은 조향축은 디스크 성능을 원하지만 구동축은 유지보수가 적은 드럼에 의존하는 함대를 위한 과도기적 틈새시장을 채우고 있습니다. 정밀 제어 장치로 공기 소비를 15% 줄일 수 있기 때문에 보조 에너지를 절약해야 하는 배터리 전기 섀시에서 전기 공압 솔루션에 대한 관심이 증가하고 있으며, 에어 브레이크 시스템 산업 전반에서 그 중요성이 커지고 있습니다.

기존의 드럼식 플랫폼도 계속 진화하고 있습니다. 대형 주철 부품 제조업체는 연비를 저해하는 통 모양의 질량 페널티를 상쇄하기 위해 중량 최적화 웹 가공을 진행하고 있습니다. 한편, 디스크식 추진파는 로터 오프셋 설계와 볼트-온식 캘리퍼 모듈을 통한 패드 교환의 신속성을 강조하며 휠 엔드 당 25%의 작업 시간 단축을 주장하고 있습니다. 2026년부터 2031년까지 전자식 슬랙 어저스터 센서가 장착된 개조 키트가 애프터마켓 매출을 견인할 것으로 예상되며, 라이닝 마모를 예측하는 데이터 분석의 교차 판매가 이루어질 것으로 전망됩니다. 이러한 상호 작용은 균형 잡힌 공존을 암시하지만, 가치의 원천은 소프트웨어 지원 디스크 및 전기 공압식 변형으로 이동하여 금세기 후반까지 에어 브레이크 시스템 시장은 유동적 인 상태를 유지할 것입니다.

2025년 에어 브레이크 시스템 시장 규모에서 소형 상용차가 34.88%로 가장 큰 점유율을 차지했습니다. 이는 특히 아시아 E-Commerce 회랑에서 도시 지역 배송의 성장에 기인합니다. 잦은 정지 및 시동 사이클은 빠른 압력 회복을 요구하며, OEM 제조업체는 모듈식 공기 건조기와 결합된 2단 압축기를 선호합니다. 판매량은 적지만, 대형 트럭은 제로 에미션 목표에 따라 무급유 압축기, 이중화 ECU, 고정밀 압력 센서가 필수적이기 때문에 7.52%의 CAGR로 확대될 것으로 예상됩니다. 이 분야는 기술 혁신의 온상이기도 합니다. 다임러의 600kWh 'eActros 600'은 회생 브레이크와 마찰 브레이크를 함께 사용하며, 이로 인해 공급업체들은 배터리 충전 상태에 따라 공기압 임계값을 미세하게 조정해야 하는 어려움을 겪고 있습니다.

강성 작업차와 덤프트럭은 먼지와 마모가 심한 환경에서 운행되는 경우가 많아 디스크 씰의 수명이 짧아지기 때문에 자동 조절식 드럼 어셈블리의 역할이 중요합니다. 버스와 장거리 버스는 승객의 편안함과 안전을 최우선으로 하여 비상 정지 시 차체의 흔들림을 최소화하는 전기 공기압 제어를 채택하고 있습니다. 오프로드 및 광산용 운반 차량에는 30bar 이상의 정격 용량을 가진 이중 회로 챔버와 진흙의 침입을 견딜 수 있는 밀폐형 슬랙 조절기가 요구됩니다. 모든 클래스에서 사용 사례가 확대됨에 따라 제품 포트폴리오는 모듈성을 유지해야 하며, 에어 브레이크 시스템 시장이 운영 주기와 규제 요건에 따라 다양화됨에 따라 수익성을 유지해야 합니다.

지역별 분석

2025년 아시아태평양은 에어 브레이크 시스템 시장의 44.83%를 차지했습니다. 이는 중국의 압도적인 상용차 생산과 인도의 광범위한 고속도로 현대화에 힘입은 것입니다. 중국 OEM 업체들은 2030년 전동화 목표 달성을 위해 ECU와 드라이 컴프레서를 빠르게 통합하고 있습니다. 한편, 일본의 Tier 1 공급업체는 예지보전 대시보드용 정밀 센서를 공급하고 있습니다. 동남아시아의 열대 기후로 인해 디스크 브레이크 냉각에 어려움이 있어, 공급업체와 현지 조립업체가 공동 개발 프로그램을 통해 로터 코팅과 벤트 형상의 커스터마이징을 진행하고 있습니다.

아프리카는 기반은 작지만 급속한 도시화, 광업 부문의 확대, 그리고 안정적인 제동 성능을 갖춘 현대식 트럭을 필요로 하는 범아프리카 무역 통로의 정비로 인해 2031년까지 CAGR 9.88%의 성장이 예상됩니다. 남아프리카공화국과 나이지리아는 규제 조정을 주도하고 있으며, ECE R13 규정을 준수하기 위해 브레이크 성능 기준을 단계적으로 상향 조정하고 있습니다. 고온 환경에서의 디스크 페이드 우려로 인해 첨단 브레이크 도입이 늦어지고 있지만, 케냐의 시험 차량은 물 분사 냉각 쉴드를 결합한 하이브리드 드럼-디스크 구성을 시험 운행하여 온도 급상승을 완화하기 위해 노력하고 있습니다.

북미와 유럽은 성숙하면서도 기술 집약적인 수요 패턴을 보이고 있습니다. EPA 3단계 및 EU의 무공해 규제는 전기 공압식 브레이크 바이 와이어 구조로의 전환을 촉진하고 프리미엄 가격을 형성하고 있습니다. 개조 시장은 활황을 유지하고 있습니다. 이는 강화되는 자동긴급제동(AEB) 및 차선 이탈 방지 규제가 운행 중인 차량에도 적용되기 때문에 지속적인 수익이 보장되기 때문입니다. 2024년 주철 드럼 및 밸브 공급망에서 공급 부족이 두드러졌지만, 멕시코와 동유럽의 생산능력 증설로 인해 병목 현상이 완화되고 있습니다. 그 결과, 에어 브레이크 시스템 시장은 이 세 경제권의 지역 정책의 엄격함, 기술 준비도, 기후변화에 대한 고려를 반영할 것으로 예상됩니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The global Air Brake Systems market was valued at USD 6.28 billion in 2025 and estimated to grow from USD 6.86 billion in 2026 to reach USD 10.62 billion by 2031, at a CAGR of 9.18% during the forecast period (2026-2031).

Regulatory catalysts such as the United States Environmental Protection Agency's Phase 3 greenhouse-gas standards for heavy-duty vehicles, which begin with model year 2027, are accelerating OEM investment in electropneumatic architectures supporting diesel and zero-emission powertrains. Integration of advanced driver assistance systems (ADAS) has further raised precision-braking requirements, pushing suppliers to develop electronic control units (ECUs) and sensor suites that synchronize with automatic emergency braking (AEB) functionality. Compressor redesign shifting from engine-driven to electric cuts parasitic losses and readies vehicles for hydrogen fuel-cell or battery-electric operation. These technology inflections, coupled with fleet demand for lower total cost of ownership, are reshaping competitive dynamics and tipping procurement choices toward disc-brake or hybrid configurations in long-haul applications across every major air brake systems market region.

Global Air Brake System Market Trends and Insights

Electrification-Ready Pneumatic Architectures

OEMs are re-engineering brake systems so the pneumatic circuit integrates seamlessly with battery-electric and hydrogen fuel-cell drivetrains. ZF secured orders to deploy brake-by-wire hardware across nearly 5 million vehicles, proving large-scale viability and giving fleets an immediate path to regenerative braking compatibility. Canada's support of VMAC's high-voltage compressor program signals national prioritization of electric auxiliary components. Electric compressors eliminate crankshaft drag, improving range and lowering carbon intensity, while integrated thermal-management software coordinates regenerative and friction braking to avoid heat buildup during repeated stops. As these systems migrate from pilot fleets in Europe to series production worldwide, suppliers that master modular electric compressor platforms will secure recurring software-update revenue streams throughout the air brake systems market.

Regulatory Push for Zero-Emission Heavy Trucks

The EPA's Phase 3 standards target a 25% reduction in carbon dioxide for Class 8 trucks by 2032 and dovetail with California's Advanced Clean Trucks regulation, forcing manufacturers to redesign pneumatic systems for oil-free operation. The European Union's CO2 standards echo these targets and embed compliance incentives that reward vehicles with energy-efficient braking. Suppliers must therefore substitute lubricated compressors with dry-running units while enlarging air-storage capacity to balance fluctuating demands from electric regenerative cycles. Regulatory clarity over a 10-year horizon encourages fleet pre-orders of hydrogen prototypes, pushing the air brake systems market toward faster adoption of electropneumatic valves that maintain precise pressure at lower duty cycles.

High Maintenance Cost of Air-brake Lines and Valves

The growing count of electronically modulated valves and sensors raises workshop bills, especially in fleets that lack calibrated diagnostic tools. Knorr-Bremse expanded aftermarket revenue to 30.1% of commercial-vehicle sales during 2024, highlighting rising service demand knorr-bremse.com. Bendix's ACom AE tool offers fault-code overlays for global scalable air-treatment modules, but technicians require new certifications, which limits adoption velocity in emerging economies. Higher-specification nylon hoses, moisture separation cartridges, and firmware licensing fees add recurring costs that temper the near-term growth of the air brake systems market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of ADAS Requires Higher-Precision Braking

- Fleet Demand for Total-Cost-of-Ownership Reduction Via Air-disc Conversion

- Disc-brake Heat-fade Issues in Tropical Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air drum brake designs retained 45.78% of the air brake systems market size in 2025, reflecting cost efficiency and widespread service familiarity. Disc variants penetrated long-haul tractors after NHTSA's stricter stopping-distance rule but still sit below drums in absolute volume. The electropneumatic subset, although only a fraction today, is growing fastest at an 8.55% CAGR as AEB, lane-keeping, and platooning pilots demand millisecond-level pressure modulation. Hybrid drum-disc configurations fill a transitional niche for fleets that want disc performance on steer axles yet still rely on lower-maintenance drums on drive axles. Because precision controllers can trim air consumption by 15%, electropneumatic solutions are drawing interest from battery-electric chassis that must conserve auxiliary energy, broadening their relevance across the air brake systems industry.

Traditional drum platforms are not standing still. Large cast-iron suppliers are machining weight-optimized webs to offset the barrel-shaped mass penalties that hamper fuel economy. Conversely, disc advocates emphasize rotor offset designs and bolt-on caliper modules that accelerate pad swaps, claiming 25% labor reduction per wheel end. From 2026 to 2031, retrofit kits featuring electronic slack-adjuster sensors are forecast to lift aftermarket revenue, enabling meaningful cross-selling of data analytics to predict lining wear. This interplay suggests a balanced coexistence, yet the value pool will migrate toward software-supported disc and electropneumatic variants, keeping the air brake systems market in flux for the rest of the decade.

Light commercial vehicles represented the largest 34.88% slice of the 2025 air brake systems market size, owing to urban delivery growth, especially in Asia's e-commerce corridors. Frequent stop-start duty cycles demand rapid pressure recovery, driving OEM preference for two-stage compressors paired with modular air-dryers. Though lower in unit sales, heavy-duty trucks are forecast to expand at 7.52% CAGR, underpinned by zero-emission targets that obligate oil-free compressors, redundant ECUs, and high-accuracy pressure sensors. The segment also acts as an innovation incubator: Daimler's 600 kWh eActros 600 adopts blended regenerative and friction braking, which forces suppliers to fine-tune air-pressure thresholds based on battery state of charge.

Rigid vocational vehicles and dump trucks often operate in dusty, abrasive environments that shorten disc-seal life, making a role for self-adjusting drum assemblies. Buses and coaches prioritize passenger comfort and safety, adopting electropneumatic logic that minimizes pitch during panic stops. Off-highway and mining haulers require high-capacity dual-circuit chambers rated beyond 30 bar, with sealed slack adjusters that withstand mud ingress. Broadening use-cases across every class ensures that product portfolios must remain modular, defending margins as the air brake systems market diversifies by duty cycle and regulatory overlay.

The Air Brake System Market is Segmented by Brake Type (Drum Air Brake, Disc Air Brake, Hybrid Drum-Disc Systems and More), Vehicle Type (Light Commercial Vehicles, Medium-Duty Trucks, Heavy-Duty Trucks, and More), Component (Compressor, Governor and Valves, Storage Tank, and More), Sales Channel (OEM, and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 44.83% of the air brake systems market in 2025, anchored by China's outsized commercial-vehicle production and India's sprawling highway modernization. Chinese OEMs are quickly integrating ECUs and dry compressors to backstop the country's 2030 electrification quotas, while Japanese tier-ones supply precision sensors that feed predictive-maintenance dashboards. In Southeast Asia, the tropical climate challenges disc-brake cooling, prompting joint-development programs between suppliers and local assemblers to customize rotor coatings and vent geometries.

Africa, though starting from a modest base, is forecast to post a 9.88% CAGR through 2031 thanks to rapid urbanization, mining-sector expansion, and pan-African trade corridors that demand modern trucks with reliable braking. South Africa and Nigeria are spearheading regulatory harmonization, gradually raising brake-performance standards to align with ECE R13 provisions. Disc-fade concerns under high ambient heat have slowed advanced-brake deployment, but pilot fleets in Kenya are trialing hybrid drum-disc setups paired with water-piqued cooling shields to mitigate temperature spikes.

North America and Europe exhibit mature but technology-intensive demand patterns. EPA Phase 3 and the EU's zero-emission mandates compel a shift toward electropneumatic brake-by-wire architectures, fostering premium pricing. The retrofit market remains vibrant because tightening AEB and lane-departure regulations apply to in-service vehicles, guaranteeing recurring revenue. Supply-chain kinks for cast-iron drums and valves were pronounced in 2024, yet capacity additions in Mexico and Eastern Europe are easing bottlenecks. Consequently, the air brake systems market will mirror regional policy stringency, technology readiness, and climate considerations across these three economic blocs.

- ZF Friedrichshafen AG

- Knorr-Bremse AG

- Wabtec (WABCO) Corp.

- Haldex AB

- Cummins Inc. (Meritor Inc.)

- Nabtesco Corp.

- Bendix CVS LLC

- TSE Brakes Inc.

- SORL Auto Parts Inc.

- Brakes India Ltd.

- Continental AG

- Federal-Mogul Motorparts

- Bendix Commercial Vehicle Systems LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification-ready pneumatic architectures

- 4.2.2 Regulatory push for zero-emission heavy trucks

- 4.2.3 Rising adoption of advanced driver-assistance systems (ADAS) requiring higher-precision braking

- 4.2.4 Fleet demand for total-cost-of-ownership reduction via air-disc conversion

- 4.2.5 Smart compressor integration with telematics (under-reported)

- 4.2.6 Hydrogen fuel-cell truck programs demanding oil-free air supply (under-reported)

- 4.3 Market Restraints

- 4.3.1 High maintenance cost of air-brake lines & valves

- 4.3.2 Disc-brake heat-fade issues in tropical climates

- 4.3.3 Supply-chain crunch for cast-iron components (under-reported)

- 4.3.4 Cyber-security risks in electronically controlled braking systems (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Brake Type

- 5.1.1 Drum Air Brake

- 5.1.2 Disc Air Brake

- 5.1.3 Hybrid Drum-Disc Systems

- 5.1.4 Electropneumatic (E-PBS)

- 5.2 By Vehicle Type

- 5.2.1 Light Commercial Vehicles

- 5.2.2 Medium-Duty Trucks

- 5.2.3 Heavy-Duty Trucks

- 5.2.4 Buses & Coaches

- 5.2.5 Off-Highway & Mining Trucks

- 5.3 By Component

- 5.3.1 Compressor

- 5.3.2 Governor & Valves

- 5.3.3 Storage Tank

- 5.3.4 Slack Adjuster

- 5.3.5 Brake Chamber

- 5.3.6 Electronic Control Unit & Sensors

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Sweden

- 5.5.3.8 Poland

- 5.5.3.9 Russia

- 5.5.3.10 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Indonesia

- 5.5.4.7 Thailand

- 5.5.4.8 Vietnam

- 5.5.4.9 Philippines

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Kenya

- 5.5.6.5 Morocco

- 5.5.6.6 Algeria

- 5.5.6.7 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 ZF Friedrichshafen AG

- 6.4.2 Knorr-Bremse AG

- 6.4.3 Wabtec (WABCO) Corp.

- 6.4.4 Haldex AB

- 6.4.5 Cummins Inc. (Meritor Inc.)

- 6.4.6 Nabtesco Corp.

- 6.4.7 Bendix CVS LLC

- 6.4.8 TSE Brakes Inc.

- 6.4.9 SORL Auto Parts Inc.

- 6.4.10 Brakes India Ltd.

- 6.4.11 Continental AG

- 6.4.12 Federal-Mogul Motorparts

- 6.4.13 Bendix Commercial Vehicle Systems LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment