|

시장보고서

상품코드

1937427

공간 오믹스 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Spatial OMICS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

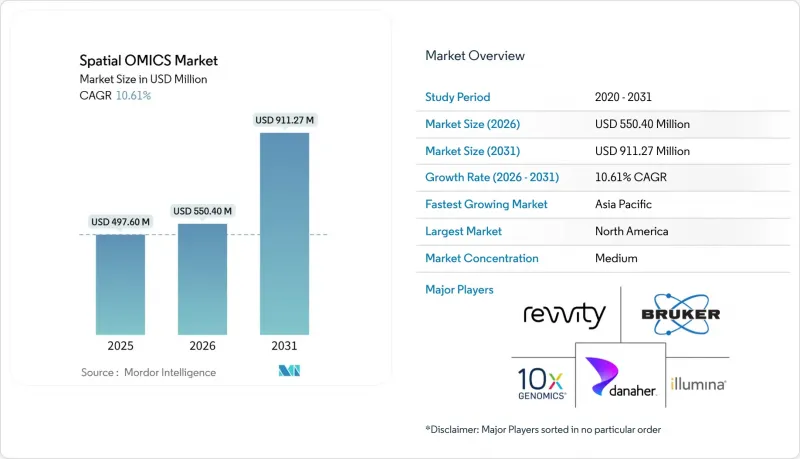

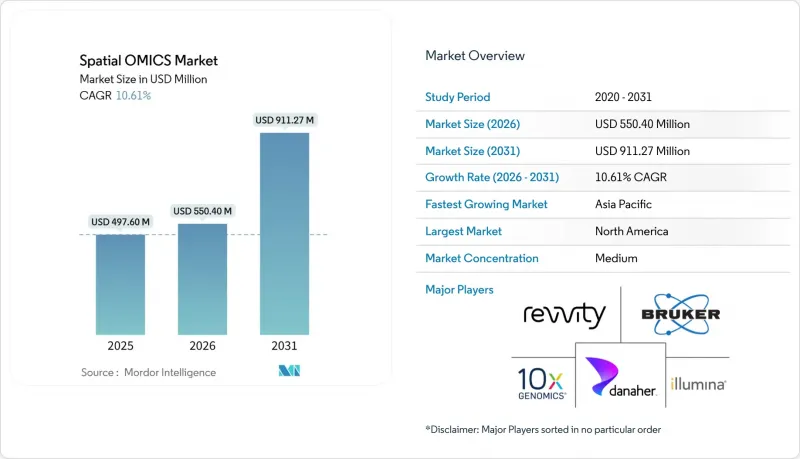

2026년 공간 오믹스 시장 규모는 5억 5,041만 달러로 추정되며, 2025년 4억 9,760만 달러에서 성장이 전망됩니다. 2031년에는 9억 1,104만 달러에 달하고, 2026년부터 2031년까지 CAGR 10.61%로 확대될 전망입니다.

이러한 견조한 성장의 배경에는 빠르게 성숙하고 있는 공간 전사체학-단백질체학-유전체학 기술, 정밀의료의 사용 사례 확대, 지속적인 공적 자금 투입 등이 있습니다. 클라우드 네이티브 분석 기술, 종양학 분야에서의 사용 사례 확대, 산업 재편이 스페이시오믹스 시장의 성장 전망을 견인하는 반면, 장비 비용과 규제 조화가 주요 장벽으로 남아있습니다. 북미는 연구 인프라와 규제 명확성으로 인해 우위를 유지했지만, 아시아태평양은 바이오의약품 투자가 활발하게 이루어지고 있는 점을 반영하여 가장 빠른 성장세를 보였습니다. 브루커의 나노스트링 인수와 퀀텔릭스의 아코야 인수 제안과 같은 전략적 인수는 풀스택 공간 생물학 역량을 둘러싼 경쟁이 심화되고 있음을 보여줍니다.

세계 공간 오믹스 시장 동향과 인사이트

암 및 유전성 질환의 높은 부담

암 연구는 공간 생물학 분야에서 가장 큰 연구비 배분 대상이며, 미국 국립암연구소는 2024 회계연도에 종양학 연구에 72억 2,000만 달러의 예산을 책정하고 있습니다. 공간 전사체학은 표준 벌크 시퀀싱으로 포착할 수 없는 내성 메커니즘과 전이 패턴을 규명하기 위해 조직 내 종양 서브클론의 식별과 간질과의 상호작용을 가시화합니다. 이러한 유용성으로 인해 종합암센터 및 제약회사 안전팀에서 수요가 증가하고 있습니다. 면역세포 침윤의 정밀한 매핑은 체크포인트 억제제 설계를 유도하고, 다중 이미징 질량 사이토메트리는 발견한 마커의 단백질 수준 발현을 검증합니다. 신경퇴행성 질환 등 비종양 분야에서도 유사한 워크플로우가 채택되고 있는 가운데, 지속적인 종양학 펀딩은 스페이시오믹스 시장에 안정적인 수익 기반을 보장하고 있습니다.

오믹스 기술의 발전과 맞춤형 의료에 대한 요구

10x Genomics의 Xenium 5K는 세포당 5,000개의 유전자를 세포 내 해상도로 분석하며, AI 세분화을 통합하여 데이터 해석을 효율화합니다. 일루미나가 2026년 출시할 예정인 전트랜스스크립션 공간 플랫폼은 편향되지 않은 발견으로의 전환을 시사하고 있습니다. 스탠포드 대학의 데이터 오션(Data Ocean)과 같은 클라우드 이니셔티브를 통해 중규모 연구소에서도 온프레미스 클러스터 없이도 테라바이트 규모의 공간 데이터세트를 분석할 수 있게 되었습니다. 전사체, 단백질, 대사체의 각 층을 동일한 좌표 내에서 통합함으로써 치료법 매칭에 도움이 되는 보다 풍부한 환자별 지도를 생성할 수 있습니다. 이러한 발전으로 차세대 시퀀싱 패널을 공간적 맥락에서 보완하고자 하는 병리 검사실로 공간 오믹스 시장이 확대되고 있습니다.

높은 장비 및 데이터 스토리지 비용

턴키 방식의 공간 플랫폼은 50만-200만 달러, 단일 세포 단백질체학은 세포당 최대 50달러의 비용이 소요되어 학계 예산에 부담을 주고 있습니다. 이미징 데이터세트는 보통 수 테라바이트 규모에 달하기 때문에 고성능 스토리지에 대한 투자가 필수적입니다. 번역 유전체학 연구소는 조직 마이크로어레이로의 전환으로 샘플당 지출을 8분의 1로 줄였지만, 데이터 관리 비용은 여전히 발생하고 있습니다. 클라우드 렌탈은 설비투자를 운영비용으로 전환하지만, 데이터 전송 비용은 계속 발생합니다. 높은 진입장벽으로 인해 자원이 부족한 연구소에서 도입이 늦어지고 있으며, 공간 오믹스 시장의 침투를 억제하고 있습니다.

부문 분석

공간 트랜스크립틱스는 2025년 40.93%의 매출 점유율을 유지하며 확고한 워크플로우를 확보했습니다. 그러나 멀티플렉스 이미징 질량 사이토메트리와 크로노스(KRONOS) 규모의 기반 모델이 픽셀 수준의 정확도로 단백질을 식별하는 가운데, 단백질체학은 2031년까지 19.11%의 CAGR로 성장할 것으로 예상됩니다. 통합된 전사-단백질 스택은 희귀한 세포 상태를 주석화할 때 위음성을 줄여줍니다. 분자 픽셀화 기술은 광학계를 필요로 하지 않고, 세포당 1,000개의 인접 구역에 걸쳐 76종의 단백질을 분석할 수 있어 형광의 한계를 극복했습니다. 멀티오믹스 통합이 성숙해짐에 따라 공간오믹스 시장은 이러한 플랫폼 간의 상호보완적인 라이선싱의 혜택을 누리고 있습니다.

Hitachi의 OhmX 분석기와 같은 새로운 공간 유전체학 워크플로는 분석 대상을 구조적 변이 및 전체 조직 내 메틸화 환경으로 확대합니다. 각 벤더들은 크로스모달 키트를 번들로 제공하고 있으며, 이는 연구소가 단일 모달리티의 업그레이드가 아닌 전체 파이프라인을 현대화할 수 있도록 유도하고 있으며, 그 결과 공간 오믹스 시장의 평균 판매 가격 상승을 주도하고 있습니다.

2025년에는 연구소의 설비 투자 우선순위로 인해 장비가 45.02%의 점유율을 차지하며 하드웨어 분야의 공간 오믹스 시장 규모를 뒷받침했습니다. 그러나 AI 해석이 멀티테라바이트 규모의 데이터세트에 필수적인 요소로 떠오르면서, 소비 기반 소프트웨어 구독은 연간 20.21%의 속도로 성장하고 있습니다. AWS와의 제휴를 통해 스타트업은 클라우드 퍼스트 알고리즘을 도입할 수 있으며, 온프레미스 컴퓨팅 비용을 절감하면서 지속적인 수익을 확보할 수 있습니다. 기기 제조사들은 분석 파이프라인의 프리로딩을 강화하고, 시약 구매를 클라우드 대시보드에 연동하여 고객 인클로저를 강화하고 있습니다.

STew, Seurat 공간분석 애드온 등의 오픈 소스 공개는 커뮤니티 도입을 촉진하는 한편, 엔터프라이즈급 신뢰성에 대한 수요를 불러일으키고 있습니다. 소프트웨어가 가치의 더 큰 비중을 차지함에 따라 벤처 캐피탈은 데이터 레이어 기업에 집중하고 있으며, 공간 오믹스 시장에 신규 진입자와 경쟁을 불러일으키고 있습니다.

공간오믹스 시장 보고서는 기술별(공간 전사체학, 공간 유전체학, 공간 유전체학, 공간 단백질체학), 제품별(기기, 소모품, 소프트웨어), 샘플별(FFPE 및 생동결), 용도별(진단, 중개연구 등), 최종사용자별(학술 및 중개연구기관 등), 지역별(북미, 유럽 등)로 구성되어 있습니다. 번역 연구기관 등), 지역(북미, 유럽 등)으로 구성되어 있습니다. 시장 예측, 금액(달러), 시장 예측, 금액(달러)

지역별 분석

북미는 NIH MOHD 프로그램, NCI 종양학 예산, FDA 규제 명확화를 배경으로 2025년 매출의 41.74%를 차지했습니다. 캘리포니아와 매사추세츠에 집중된 클러스터는 독자적인 생태계를 유지하고 있으며, 10x Genomics社만 2024년 6억 1,080만 달러의 매출을 기록할 것으로 예상하고 있습니다. 제약사와의 제휴가 추가 수요를 불러일으키며 기기, 시약, 분석 분야의 스페이시오믹스 시장을 확대하고 있습니다.

아시아태평양은 중국, 일본, 인도의 정밀 의료 계획의 전개와 의료 기술 제조의 확대로 인해 18.36%의 CAGR로 성장하고 있습니다. 2021년 이후 지역 VC 투자는 22% 감소한 반면, 공적 자금이 부족분을 보충하고 저렴한 인건비가 세계 벤더들의 현지 생산을 촉진하고 있습니다. AWS 리전 존을 포함한 클라우드 인프라는 데이터센터의 병목현상을 해소하고, 공간 오믹스 시장의 보급을 촉진하고 있습니다.

유럽은 'Horizon Europe' 보조금과 MDR 준수 임상 네트워크를 활용하여 꾸준히 성장하고 있습니다. 독일, 영국, 프랑스가 도입의 핵심을 담당하고 있으며, 네덜란드와 스위스의 소규모 생태계에서는 프로토콜 혁신이 진행되고 있습니다. 브렉시트로 인해 이중 규제 대응이 필요하게 되었지만, 런던의 연구 병원에서는 여전히 영향력 있는 공간 분석 연구가 발표되고 있습니다. 국경을 넘나드는 컨소시엄을 통해 다중 시설 시험을 가속화하고, 스페이스 오믹스 시장에 지속적인 기여를 하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05spatial omics market size in 2026 is estimated at USD 550.41 million, growing from 2025 value of USD 497.60 million with 2031 projections showing USD 911.04 million, growing at 10.61% CAGR over 2026-2031.

Robust momentum stems from fast-maturing spatial transcriptomics, proteomics and genomics technologies, widening precision-medicine use cases, and sustained public funding. Cloud-native analytics, rising oncology applications and industry consolidation amplify growth prospects for the spatial omics market, while instrument cost and regulatory harmonization remain key hurdles. North America retained dominance thanks to research infrastructure and regulatory clarity, yet Asia-Pacific delivered the quickest expansion, reflecting strong biopharma investment. Strategic acquisitions such as Bruker's purchase of NanoString and Quanterix's bid for Akoya underline an arms-race for full-stack spatial biology capabilities.

Global Spatial OMICS Market Trends and Insights

High Burden of Cancer & Genetic Diseases

Cancer accounts for the largest research allocation in spatial biology, with the US National Cancer Institute earmarking USD 7.22 billion for oncology research in fiscal 2024. Spatial transcriptomics pinpoints tumor sub-clones and stromal interactions inside intact tissue, informing resistance mechanisms and metastasis patterns that standard bulk sequencing misses. This utility spurs rising demand from comprehensive cancer centers and pharma safety teams. Better mapping of immune-cell infiltration guides checkpoint-inhibitor design, while multiplexed imaging mass cytometry validates protein-level expression of discovered markers. Persistent oncology funding guarantees a stable revenue base for the spatial omics market, even as non-oncology fields such as neurodegeneration adopt similar workflows.

Omics-Technology Advances & Personalized Medicine Demand

10x Genomics' Xenium 5K reads 5,000 genes per cell at subcellular resolution, integrating AI segmentation to streamline data interpretation. Illumina's forthcoming whole-transcriptome spatial platform, slated for 2026 launch, signals a pivot toward unbiased discovery. Cloud initiatives, such as Stanford's Data Ocean, let mid-size labs analyze terabyte-scale spatial datasets without on-premise clusters. Combining transcript, protein and metabolite layers inside the same coordinates creates richer patient-specific maps that inform therapeutic matching. These advances expand the spatial omics market into pathology labs looking to complement next-generation sequencing panels with spatial context.

High Cost of Instruments & Data Storage

Turn-key spatial platforms list between USD 500,000 and USD 2 million, while single-cell proteomics can cost up to USD 50 per cell, stressing academic budgets. Imaging datasets routinely top multiple terabytes, compelling investment in high-performance storage. The Translational Genomics Research Institute cut per-sample spend eight-fold by moving to tissue microarrays yet still absorbed data-management fees. Cloud rentals shift capex to opex but data-egress charges persist. High entry thresholds slow adoption in resource-constrained labs, tempering spatial omics market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Adoption in Drug Discovery & Development

- Rising Government Funding & Initiatives

- Complex Regulatory & Standardization Hurdles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spatial transcriptomics retained 40.93% revenue in 2025, securing entrenched workflows. Yet proteomics tracks a 19.11% CAGR to 2031 as multiplexed imaging mass cytometry and KRONOS-scale foundation models locate proteins with pixel-level precision. Integrated transcript-protein stacks reduce false negatives when annotating rare cell states. Molecular Pixelation now interrogates 76 proteins across 1,000 neighboring zones per cell without optics, overcoming fluorescence limits. As multi-omic integration matures, the spatial omics market benefits from complementary licensing across these platforms.

Emerging spatial genomics workflows such as Hitachi's OhmX Analyzer extend analysis to structural variants and methyl-landscapes within intact tissue. Vendors bundle cross-modal kits, prompting laboratories to modernize entire pipelines instead of upgrading single modalities, thereby driving higher average selling prices inside the spatial omics market.

Instruments held 45.02% share in 2025 as labs prioritized capital investment, anchoring the spatial omics market size for hardware. Consumption-based software subscriptions, however, are scaling at 20.21% yearly as AI interpretation becomes indispensable for multi-terabyte datasets. AWS alliances let start-ups deploy cloud-first algorithms, trimming on-premise compute cost while capturing recurring revenue. Instrument makers increasingly pre-load analytical pipelines, linking reagent purchases to cloud dashboards and locking in customers.

Open-source releases, including STew and Seurat spatial add-ons, enrich community adoption yet drive demand for enterprise-grade reliability. As software claims a larger slice of value, venture capital gravitates toward data-layer companies, bringing fresh entrants and heightened competition to the spatial omics market.

The Spatial Omics Market Report is Segmented by Technology (Spatial Transcriptomics, Spatial Genomics, and Spatial Proteomics), Product (Instruments, Consumables, and Software), Sample (FFPE and Fresh-Frozen), Application (Diagnostics, Translational Research and More), End User (Academic & Translational Institutes and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD),

Geography Analysis

North America contributed 41.74% revenue in 2025 on the back of the NIH MOHD program, the NCI oncology budget and FDA regulatory clarity. Concentrated clusters in California and Massachusetts help sustain proprietary ecosystems, with 10x Genomics alone booking USD 610.8 million in 2024 sales. Pharma alliances funnel additional demand, elevating the spatial omics market across instrumentation, reagents and analytics.

Asia-Pacific is expanding at 18.36% CAGR as China, Japan and India roll out precision-medicine blueprints and scale medtech manufacturing. Despite a 22% decline in regional VC since 2021, public funds are filling gaps, and lower labor costs entice global vendors to localize production. Cloud infrastructures, including AWS regional zones, circumvent data-center bottlenecks, thereby fostering broader adoption of the spatial omics market.

Europe posts steady growth, leveraging Horizon Europe grants and MDR-aligned clinical networks. Germany, the United Kingdom and France anchor deployment, while smaller ecosystems in the Netherlands and Switzerland push protocol innovation. Brexit introduces dual-regime compliance but London research hospitals continue to publish high-impact spatial studies. Cross-border consortiums accelerate multi-site trials, ensuring sustained contribution to the spatial omics market.

- 10x Genomics

- Illumina

- Danaher (Leica / Cytiva)

- Bruker (NanoString Technologies)

- Akoya Biosciences

- Vizgen

- Resolve Biosciences

- Revvity, Inc.

- Bio-Techne

- Ionpath

- S2 Genomics

- Dovetail Genomics (Cantata Bio)

- Fluidigm (Standard BioTools)

- Thermo Fisher Scientific

- Oxford Nanopore Technologies

- Agilent Technologies

- Roche Diagnostics (Ventana)

- Seven Bridges Genomics

- Ultivue

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Burden Of Cancer & Genetic Diseases

- 4.2.2 Omics-Technology Advances & Demand For Personalized Medicine

- 4.2.3 Adoption In Drug Discovery & Development

- 4.2.4 Rising Government Funding & Initiatives

- 4.2.5 Emergence Of Spatial Multi-Omics Integration Platforms

- 4.2.6 Cloud-Native Spatial Data-Analysis Services Lower Entry Barriers

- 4.3 Market Restraints

- 4.3.1 High Cost Of Instruments & Data Storage

- 4.3.2 Complex Regulatory & Standardization Hurdles

- 4.3.3 Scarcity Of High-Quality FFPE Reference Standards

- 4.3.4 Fragmented IP Landscape Delaying Open Data Standards

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Spatial Transcriptomics

- 5.1.2 Spatial Genomics

- 5.1.3 Spatial Proteomics

- 5.2 By Product

- 5.2.1 Instruments

- 5.2.2 Consumables

- 5.2.3 Software

- 5.3 By Sample

- 5.3.1 FFPE

- 5.3.2 Fresh-Frozen

- 5.4 By Application

- 5.4.1 Diagnostics

- 5.4.2 Translational Research

- 5.4.3 Drug Discovery & Development

- 5.4.4 Single-Cell Analysis

- 5.4.5 Cell Biology

- 5.5 By End-User

- 5.5.1 Academic & Translational Institutes

- 5.5.2 Pharmaceutical & Biotechnology Companies

- 5.5.3 CROs & CDMOs

- 5.5.4 Others

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 10x Genomics

- 6.3.2 Illumina Inc.

- 6.3.3 Danaher (Leica / Cytiva)

- 6.3.4 Bruker (NanoString Technologies)

- 6.3.5 Akoya Biosciences

- 6.3.6 Vizgen

- 6.3.7 Resolve Biosciences

- 6.3.8 Revvity, Inc.

- 6.3.9 Bio-Techne

- 6.3.10 Ionpath

- 6.3.11 S2 Genomics

- 6.3.12 Dovetail Genomics (Cantata Bio)

- 6.3.13 Fluidigm (Standard BioTools)

- 6.3.14 Thermo Fisher Scientific

- 6.3.15 Oxford Nanopore Technologies

- 6.3.16 Agilent Technologies

- 6.3.17 Roche Diagnostics (Ventana)

- 6.3.18 Seven Bridges Genomics

- 6.3.19 Ultivue

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment