|

시장보고서

상품코드

1937438

염소 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Chlorine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

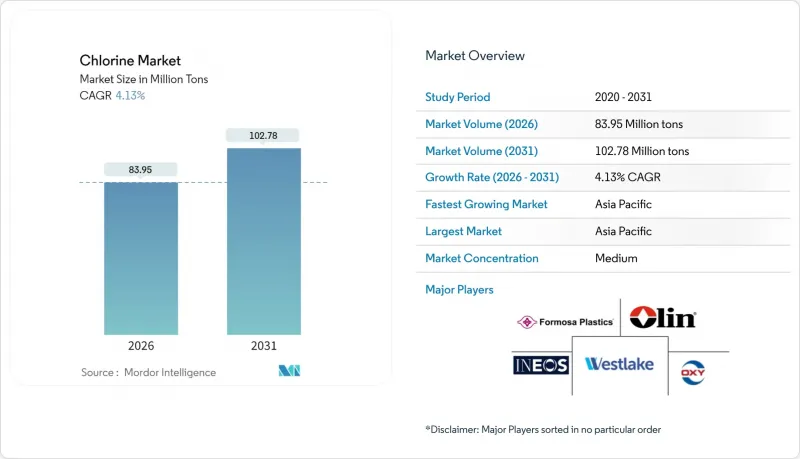

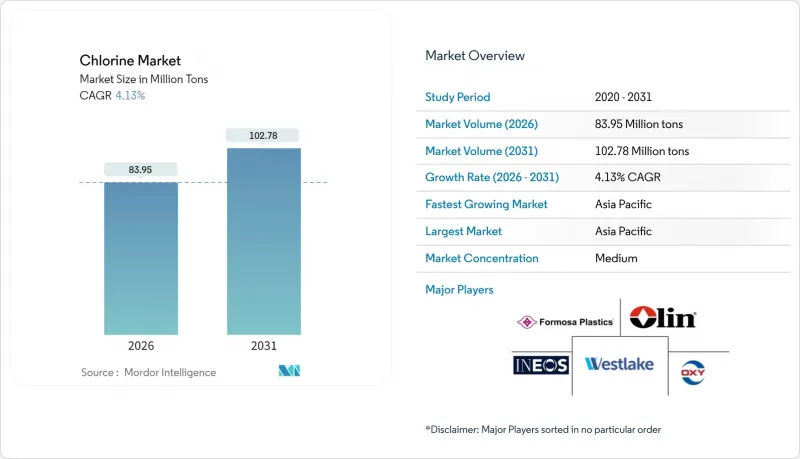

염소 시장은 2025년 8,062만 톤에서 2026년에는 8,395만 톤으로 성장할 것으로 예상되며, 2026년부터 2031년까지 CAGR 4.13%를 기록하며 2031년까지 1억 278만 톤에 달할 것으로 예측됩니다.

꾸준한 인프라 투자, 확대되는 지자체 수처리 프로그램, 증가하는 의약품 중간체 생산량으로 인해 이 제품은 세계 프로세스 체인에서 필수적인 위치를 유지하고 있습니다. 멤브레인 셀 기술은 낮은 에너지 소비와 강화되는 환경 규제를 배경으로 주요 지역 모두에서 기존 생산 방식을 능가하고 있습니다. 배관, 케이블 절연체, 플렉서블 필름용 염화비닐 수지 수요의 지속적인 증가는 기초 원료의 소비를 견고하게 뒷받침하는 한편, 고체 전지 조사, 반도체 에칭제, 고순도 중간체 분야는 염소 공급업체에게 새로운 비즈니스 기회를 확대시키고 있습니다. 아시아태평양은 물량 성장을 주도하고, 통합 석유화학 허브가 물류 비용 절감과 자체 발전 시설에 대한 접근성을 활용하면서 주요 수출 거점으로서의 지위를 유지할 것으로 예상됩니다.

세계 염소 시장 동향 및 전망

인프라 및 포장 분야의 PVC 수요 급증

식수 및 폐수처리용 PVC 배관망은 특히 중국, 인도, 인도네시아, 베트남에서 정부 주도의 주택 건설 및 교통 회랑 건설이 진행됨에 따라 다년간 염소 수요를 견인하고 있습니다. 소비재 포장 분야에서는 PVC의 내구성과 밀폐성을 인정받아 EC 물류센터의 수요 증가를 뒷받침하고 있습니다. 대규모 프로젝트는 국가 부양책의 일환으로 자금을 조달하기 때문에 경기 침체기에도 중단되는 경우가 드물어 염소 시장에 예측 가능한 기반을 제공합니다. 통합 염소알칼리 제조업체는 경쟁력 있는 염화비닐 모노머 공급을 위해 공장을 에너지 절약형 멤브레인 장치로 개조하여 연안 산업단지 내 점유율을 공고히 하고 있습니다. 동남아시아의 압출 성형 능력의 꾸준한 증가는 건설업체와 가공업체가 저렴한 염소계 수지에 구조적으로 의존하고 있다는 것을 입증합니다.

도시 하수 처리에 대한 신속한 투자

아시아태평양 회랑의 메가시티의 인구 밀도는 대규모 중앙집중식 처리 플랜트와 교외 지역용 모듈식 시스템을 모두 필요로 합니다. 병원균에 대한 최종 장벽으로 염소 처리가 가장 경제적이기 때문에 현지 전해장치 및 패키지형 차아염소산나트륨의 조달 수요는 지속될 것입니다. 브라질, 남아프리카공화국, 필리핀에서는 재생수에 대한 3차 소독이 의무화되어 향후 취수량이 역대 최고 수준을 넘어설 것으로 예상됩니다. 산업단지에서는 액체 배출 제로 정책을 채택하고, 염소 접촉 시간을 반복하는 이중 루프 재사용을 추진하고 있습니다. 장비 공급업체는 도시 전체의 지속가능성 헌장에 따라 화학제품의 지속적인 소비 계약을 촉진하고 염분 배출을 최소화하는 저염막 전지로의 전환을 지적하고 있습니다.

개발도상국의 수은 셀 플랜트 단계적 폐지 강화 강화

미나마타 조약의 의무적 준수에 따라 동남아시아, 동유럽, 아프리카 일부 지역에 남아있는 수은 시설은 가동을 중단하거나 고비용의 전환을 강요받고 있습니다. 전환기 가동 중단으로 인해 지역 염화비닐 수지 가공업체와 섬유 표백 공장에 대한 염소 공급이 일시적으로 제한되는 한편, 국경을 넘는 수입 흐름으로 인해 화물 운임이 상승하고 있습니다. 멤브레인 장비에 대한 개조 자금을 조달할 수 없는 중소기업은 업계에서 철수하고, 지역적 통합이 진행되고 있습니다. 기존 슬러지 연못의 환경 복원에는 본래 확장 계획을 뒷받침해야 할 운전 자금이 투입되고 있습니다. 개보수를 완료한 사업자는 고가의 수입품으로 단기적인 공급 부족을 보완하고 있으며, 이는 계약 협상의 변동 요인으로 작용하고 있습니다.

부문 분석

EDC/PVC는 2025년 기준 염소 시장 점유율의 33.29%를 차지했으며, 이는 파이프 프로파일 및 필름 분야에서 폴리머의 다재다능함을 반영합니다. 수요 집중으로 인해 통합형 제조업체는 염수 회로를 안정적인 기저부하로 가동할 수 있어 높은 가동률과 예측 가능한 현금 흐름을 실현할 수 있습니다. 한편, 이소시아네이트 및 산소 화합물이 차지하는 염소 시장 규모는 2026년부터 2031년까지 연평균 4.41%의 CAGR로 확대될 것으로 예상됩니다. 이는 폴리우레탄 폼이 에너지 절약형 건축물과 경량 차량 내장재의 단열재로 채택되고 있기 때문입니다. 고마진 분야로의 진출 의지가 높아지면서 생산자들은 전용 고순도 루프 및 모듈형 반응 장치를 구축하여 벌크 VCM 계약을 넘어서는 유연성을 확보하고 있습니다.

클로로메탄류와 용매는 냉동, 실리콘 웨이퍼 세정, 제초제 합성에서 안정적인 수요가 있으며, 건설 사이클의 영향을 덜 받는 특성을 가지고 있습니다. 에피클로로히드린은 해상 풍력 구조물의 내식성 코팅에 사용되는 수성 에폭시 수지에서 점진적인 수요 확대가 예상됩니다. 염소로부터 생산되는 무기 화학제품은 식수 처리 및 배기가스 처리용 응집제 블렌드의 기반이 되며, 특히 아시아의 신흥 지방 자치 단체에서 비순환적인 수요를 뒷받침하고 있습니다.

염소 시장 보고서는 용도별(EDC/PVC, 이소시아네이트 및 산소화제, 클로로메탄, 용매 및 에피클로로히드린, 무기화학, 기타 용도), 최종사용자 산업별(수처리, 제약, 화학, 제지/펄프, 플라스틱, 농약, 기타 최종사용자 산업), 지역별로 분석됩니다. 태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분석하였습니다.

지역별 분석

아시아태평양은 2025년 세계 수요의 64.13%를 차지하여 염소 시장의 중심지로서의 역할을 강조하고 있습니다. 정유에서 PVC까지 통합된 밸류체인, 중국 내 석탄화력 발전과의 근접성, 국내 배관 교체 계획이 탄탄한 국내 배관 교체 계획과 결합하여 이 지역의 이용률은 높은 수준을 유지하고 있습니다. 신흥 산업단지 내에 설치된 재생에너지 기반 멤브레인 장치에 힘입어 아시아태평양이 누리는 염소 시장 규모는 2031년까지 연평균 4.72%의 CAGR로 더욱 확대될 것으로 예상됩니다.

북미는 성숙한 시장인 동시에 기술적으로도 선진화된 지역입니다. 공정 자동화, 전극 코팅 개선, 특수 중간체용 자체 소비형 염소 루프에 대한 투자에 집중하고 있습니다. PCC그룹이 켐어스 미시시피 공장에서 진행하는 34만톤 규모의 프로젝트는 다운스트림에 있는 이산화티타늄 및 MDI 공장과 생산능력을 병설하여 공급망을 단축하고 운송 리스크를 줄이기 위한 움직임의 대표적인 사례입니다.

유럽에서는 높은 전력 요금과 야심찬 기후 규제를 반영하여 지속가능한 운영과 에너지 효율을 우선시하고 있습니다. 제약 및 고급 도료 분야의 탄탄한 고객 기반은 프리미엄급 제품 제공을 정당화하여 사업자에게 이익을 가져다 줍니다. 동시에 에너지 집약형 플랜트에서는 비용 압박에 대한 대응책으로 이전이나 친환경 전력 구매 계약에 대한 검토가 진행되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.05The Chlorine market is expected to grow from 80.62 million tons in 2025 to 83.95 million tons in 2026 and is forecast to reach 102.78 million tons by 2031 at 4.13% CAGR over 2026-2031.

Strong infrastructure spending, expanding municipal water treatment programs, and rising pharmaceutical intermediate output maintain the commodity's indispensable status in the worldwide process chain. Membrane-cell technology has overtaken legacy production methods in every leading region, encouraged by lower energy use and tightening environmental rules. A continued uplift in polyvinyl chloride demand for pipes, cable insulation, and flexible films keeps basic feedstock consumption robust, while solid-state battery research, semiconductor etchants, and high-purity intermediates broaden the addressable opportunity for chlorine suppliers. Asia-Pacific dominates volume growth and will remain the principal export base as integrated petrochemical hubs exploit lower logistics costs and access to captive power.

Global Chlorine Market Trends and Insights

Surging PVC Demand in Infrastructure and Packaging

PVC pipe networks for potable water and wastewater drive multi-year chlorine offtake, especially across China, India, Indonesia, and Vietnam where government-backed housing and transportation corridors are underway. The packaging of fast-moving goods favors PVC's toughness and sealing properties, supporting incremental demand from e-commerce distribution centers. Large-scale projects seldom pause during economic slowdowns because they are funded within national stimulus packages, giving the chlorine market a predictable baseline. Integrated chlor-alkali producers are retrofitting plants with energy-efficient membranes to supply vinyl chloride monomer competitively, solidifying their share in coastal industrial parks. The steady course of new extrusion capacity additions in Southeast Asia underlines the structural dependence of builders and converters on affordable chlorine-derived resins.

Rapid Urban Wastewater Investments

Population density in megacities across the Asia-Pacific corridor necessitates larger centralized plants as well as modular systems for peri-urban districts. Chlorination remains the most economical last-step barrier against pathogens, sustaining procurement of on-site electrolyzers and packaged hypochlorite. Regulations in Brazil, South Africa, and the Philippines now specify tertiary disinfection for reclaimed water, lifting future intake beyond historic peak levels. Industrial parks adopt zero-liquid-discharge policies, pushing dual-loop reuse that relies on repeated chlorine contact times. Equipment suppliers note a pivot toward low-salt-input membrane cells that minimize brine disposal, aligning with citywide sustainability charters and fostering repeat chemical consumption contracts.

Tightened Mercury-Cell Plant Phase-Outs in Developing Regions

Mandatory compliance with the Minamata Convention forces remaining mercury facilities in Southeast Asia, Eastern Europe, and parts of Africa offline or into costly conversions. Transitional shutdowns temporarily constrain chlorine availability for local PVC converters and textile bleach plants, while cross-border import flows lift freight rates. Smaller firms unable to finance membrane retrofits exit the industry, nudging regional consolidation. Environmental remediation of legacy sludge ponds absorbs working capital that might otherwise support expansion programs. Operators completing conversions hedge short-term supply gaps with higher-priced imports, contributing to volatility in contract negotiations.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical Off-Patent Boom Boosting Chlorination Intermediates

- Battery-Grade Lithium-Metal Chloride for Solid-State EV Batteries

- Escalating Renewable-Power-Driven Caustic Soda Oversupply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EDC/PVC retained 33.29% of the chlorine market share in 2025, mirroring the polymer's ubiquity across pipe, profile, and film categories. Demand concentration allows integrated players to run brine circuits at steady baseload, facilitating high-utilization rates and predictable cash flow. Meanwhile, the chlorine market size attributed to isocyanates and oxygenates is on track to rise at a 4.41% CAGR between 2026 and 2031 as polyurethane foam insulates energy-efficient buildings and lightweight vehicle interiors. Higher margin exposure incentivizes producers to carve out dedicated purity loops or modular reactors, adding flexibility beyond bulk VCM contracts.

Chloromethanes and solvents offer stable demand in refrigeration, silicon wafer cleaning, and herbicide synthesis, shielding volumes from construction cycles. Epichlorohydrin sees incremental lift from water-borne epoxy resins used in corrosion-resistant coatings for offshore wind structures. Inorganic chemicals carved from chlorine underpin coagulant blends for potable water and flue-gas treatment, anchoring non-cyclical intake, especially inside emerging Asian municipalities.

The Chlorine Market Report is Segmented by Application (EDC/PVC, Isocyanates and Oxygenates, Chloromethanes, Solvents and Epichlorohydrin, Inorganic Chemicals, and Other Applications), End-User Industry (Water Treatment, Pharmaceutical, Chemicals, Paper and Pulp, Plastic, Pesticides, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific captured 64.13% of global demand in 2025, underscoring its function as the epicenter of the chlorine market. The combination of integrated refinery-to-PVC value chains, proximity to coal-based power in China, and a robust domestic pipe replacement agenda keeps regional utilization high. The chlorine market size enjoyed by Asia-Pacific will rise further at a 4.72% CAGR to 2031, supported by renewable-powered membrane installations located within emerging industrial parks.

North America remains a mature but technologically advanced arena. Investments focus on process automation, electrode-coating upgrades, and captive chlorine loops for specialty intermediates. PCC Group's 340,000-ton project at Chemours' Mississippi site typifies moves to colocate capacity with downstream titanium dioxide and MDI plants, shortening supply chains and lowering transport risk.

Europe prioritizes sustainable operations and energy efficiency, reflecting high electricity tariffs and ambitious climate rules. Operators benefit from an established customer base in pharmaceuticals and high-end coatings, justifying premium-grade offerings. Concurrently, energy-intensive plants weigh relocation or green-power purchase agreements to offset cost pressures.

- Anwil (Orlen)

- Arkema

- Covestro AG

- DOW

- Ercros S.A

- Formosa Plastics Group

- Hanwha Solutions

- INEOS

- Kem One

- Kuhlmann Europe

- Nobian

- Occidental Petroleum Corporation

- Olin Corporation

- Shivtek Spechemi Industries Ltd

- Spolchemie (KAPRAIN a.s.)

- Tata Chemicals Limited

- Tosoh Corporation

- Vencorex

- Vynova Group (ICIG HOLDING SE)

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging PVC demand in infrastructure and packaging

- 4.2.2 Rapid urban wastewater investments

- 4.2.3 Pharmaceutical off-patent boom boosting chlorination intermediates

- 4.2.4 Battery-grade Li-metal chloride for solid-state EV batteries

- 4.2.5 Semiconductor etchant expansion in Asia fabs

- 4.3 Market Restraints

- 4.3.1 Tightened mercury-cell plant phase-outs in developing regions

- 4.3.2 Escalating renewable-power-driven caustic soda oversupply (price squeeze)

- 4.3.3 Growing bromine-based biocide substitution in cooling towers

- 4.4 Value Chain Analysis

- 4.5 Technological Snapshot

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

- 4.7 Pricing Analysis

- 4.8 Import and Export Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 EDC/PVC

- 5.1.2 Isocyanates and Oxygenates

- 5.1.3 Chloromethanes

- 5.1.4 Solvents and Epichlorohydrin

- 5.1.5 Inorganic Chemicals

- 5.1.6 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Water Treatment

- 5.2.2 Pharmaceutical

- 5.2.3 Chemicals

- 5.2.4 Paper and Pulp

- 5.2.5 Plastic

- 5.2.6 Pesticides

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Anwil (Orlen)

- 6.4.2 Arkema

- 6.4.3 Covestro AG

- 6.4.4 DOW

- 6.4.5 Ercros S.A

- 6.4.6 Formosa Plastics Group

- 6.4.7 Hanwha Solutions

- 6.4.8 INEOS

- 6.4.9 Kem One

- 6.4.10 Kuhlmann Europe

- 6.4.11 Nobian

- 6.4.12 Occidental Petroleum Corporation

- 6.4.13 Olin Corporation

- 6.4.14 Shivtek Spechemi Industries Ltd

- 6.4.15 Spolchemie (KAPRAIN a.s.)

- 6.4.16 Tata Chemicals Limited

- 6.4.17 Tosoh Corporation

- 6.4.18 Vencorex

- 6.4.19 Vynova Group (ICIG HOLDING SE)

- 6.4.20 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment