|

시장보고서

상품코드

1937439

화장품 향수 유리병 포장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cosmetic Perfumery Glass Bottle Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

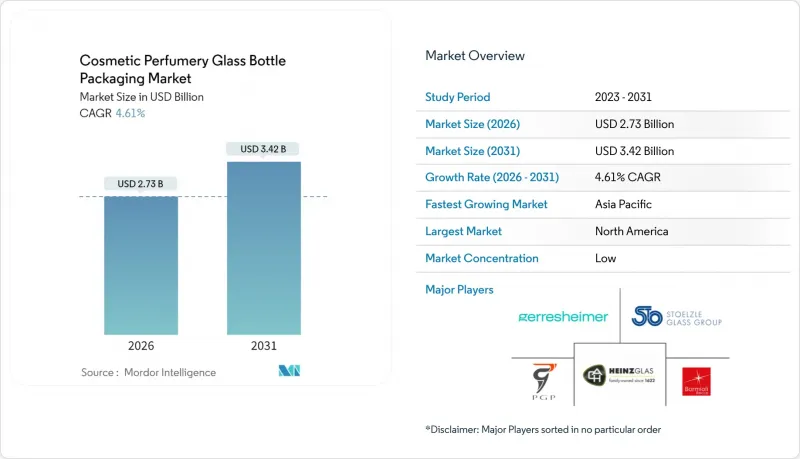

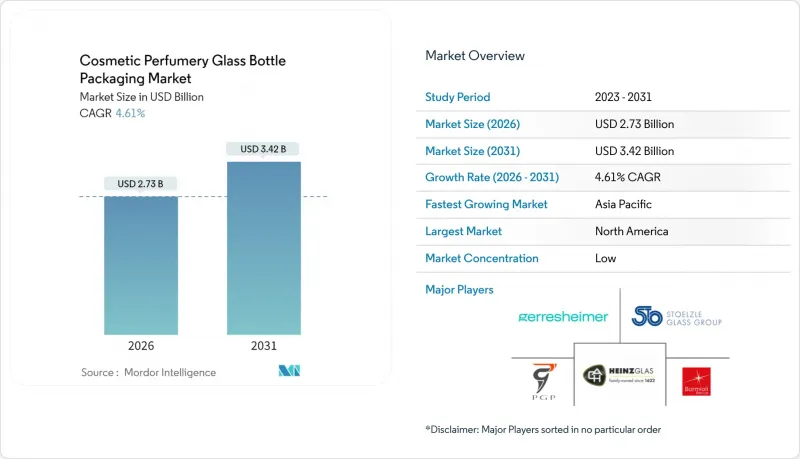

화장품 향수 유리병 포장 시장은 2025년에 26억 1,000만 달러로 평가되었으며, 2026년 27억 3,000만 달러에서 2031년까지 34억 2,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 4.61%로 예상됩니다.

이러한 완만하지만 견고한 성장 궤적은 공급망 변동성을 극복할 수 있는 업계의 능력과 대체 소재보다 유리를 선호하는 프리미엄화 추세를 활용하려는 태도를 반영합니다. 시장 확대는 특히 2030년까지 모든 포장재를 재활용할 수 있도록 하는 EU 규정 2025/40을 비롯한 혁신적인 규제 변화를 배경으로 이루어지고 있습니다. 이 규정은 품질 저하 없이 무한히 재활용이 가능한 유리를 전략적 우위로 자리매김하고 있습니다. 업계를 재편하는 거시적 요인은 지속가능성의 요구와 고급품으로서의 포지셔닝 전략이 교차하는 지점으로 집약됩니다. 뷰티 및 향수 제품의 프리미엄화 물결은 브랜드의 전통과 제품의 신뢰성을 전달할 수 있는 미적 우위를 가진 포장에 대한 수요를 주도하고 있습니다. 동시에 E-Commerce의 확대는 이중의 압력을 만들어 내고 있습니다. 브랜드는 디지털 마케팅을 위해 시각적으로 매력적인 포장을 필요로 하는 한편, 파손으로 인한 반품을 최소화하기 위한 충격 방지 솔루션도 요구하고 있습니다.

세계 화장품 향수 유리병 포장 시장 동향 및 인사이트

뷰티 및 향수 제품의 프리미엄화

고급 뷰티 및 향수 브랜드는 제품의 품질과 브랜드 역사를 구현하는 수단으로 유리 포장을 포지셔닝하는 추세가 강화되면서 플라스틱 대체품으로부터의 사양 변경을 촉진하고 있습니다. 이러한 추세는 특히 유리 포장이 진정성과 명성의 상징으로 여겨지는 신흥 시장에서 고급 화장품에 대한 프리미엄 가격 지불 의향이 높아짐에 따라 가속화되고 있습니다. 프리미엄화 효과는 선순환을 만들어 냅니다. 제품 가격의 상승은 유리 포장의 비용을 정당화하고, 유리 포장은 고급스러운 포지셔닝을 강화하여 가격 상승을 가능하게 합니다. 고급 향수 신제품 발표에는 플라스틱으로는 재현할 수 없는 독특한 모양, 색상, 장식 요소를 갖춘 맞춤형 유리병이 항상 채택되어 고급스러움을 상징하는 소재로서의 입지를 확고히 하고 있습니다. 디지털 마케팅은 이러한 추세를 더욱 가속화시키고 있으며, 유리 포장은 소셜 미디어와 EC 플랫폼에서 사진에 잘 어울리기 때문에 시각적 차별화에 투자하는 브랜드에게 부가가치를 창출하고 있습니다.

무한한 재활용이 가능한 유리로 지속가능성 추진

규제 프레임워크와 기업의 지속가능성에 대한 노력과 함께 플라스틱 대체품에 비해 유리 포장의 무한한 재활용성이라는 유리 포장의 장점이 강조되고 있습니다. EU의 포장 및 포장 폐기물 규정은 2030년까지 모든 포장재의 재활용을 의무화하고 있으며, 유리는 74%의 재활용률을 달성한 반면, 플라스틱의 재활용 실적은 매우 저조한 실정입니다. 유리 재활용은 폐쇄형 루프 시스템을 형성하며, O-I의 탄소 중립 제품인 'Estampe' 병에서 알 수 있듯이 사용한 유리(카렛)를 품질 저하 없이 최대 82%까지 새로운 병의 원료로 재사용할 수 있습니다. 기업의 지속가능성 전략에서 유리 포장이 Scope 3 배출량 감소에 기여하는 바가 점점 더 많이 인식되고 있습니다. SGD Pharma와 같은 브랜드는 화장품 용도에 특화된 디자인으로 소비 후 재활용 소재를 20% 함유한 병을 출시하고 있습니다. 이러한 지속가능성에 대한 노력은 특히 친환경을 중시하고 유리를 플라스틱을 대체할 수 있는 좋은 대안으로 여기는 Z세대 소비자들에게 큰 공감을 불러일으키고 있습니다.

플라스틱 포장의 비용 및 중량 우위

플라스틱 포장은 특히 가격 민감도가 높고 고급 소재의 선택이 제한적인 대중 화장품 분야에서 유리의 채택을 가로막는 큰 비용적, 물류적 우위를 유지하고 있습니다. 플라스틱 용기는 동급 유리 포장에 비해 일반적으로 40-60% 저렴하고 무게도 훨씬 가벼워 운송 비용과 대량 유통에 따른 탄소발자국을 줄일 수 있습니다. 고도의 플라스틱 배합 기술로 투명 폴리머와 표면처리를 통해 유리의 미관을 재현하는 사례가 증가하고 있으며, 유리에 따른 비용 부담 없이 고급스러움을 연출할 수 있게 되었습니다. 무게 차이는 특히 대형 제품이나 여러 제품 세트에서 두드러지며, 유리 포장은 플라스틱 대체품에 비해 운송 비용을 두 배로 증가시킬 수 있습니다. 이커머스의 성장과 함께 브랜드가 비용 효율적인 배송을 실현하는 동시에 파손으로 인한 반품 및 고객 불만을 최소화하기 위해 포장을 최적화하는 과정에서 이러한 우려는 더욱 증폭되고 있습니다.

부문 분석

2025년 기준, 향수는 화장품 향수 유리병 포장 시장의 46.28%를 차지하고 있으며, 향수 제조업체들이 복잡한 향기 프로파일을 유지하기 위해 불활성 유리 용기에 의존하고 있음을 보여줍니다. 이 압도적인 점유율은 화장품 향수 유리병 포장 시장에서 단독으로 가장 큰 비중을 차지한다는 것을 의미합니다. 이 부문은 맞춤형 플라콘과 고급 브랜드 이미지의 확립된 연관성 덕분에 비용 상승 국면에서도 브랜드가 높은 가격대를 유지할 수 있게 해줍니다. 디자이너 브랜드의 강력한 마케팅 지원으로 안정적인 재주문량을 유지하여 화장품 향수 유리병 포장 시장은 인접한 뷰티 카테고리의 수요 변동에 대한 저항력을 유지하고 있습니다.

네일케어 분야는 규모는 상대적으로 작지만 2031년까지 CAGR 6.05%로 확대되며, 추적 대상 제품 중 가장 높은 성장률을 보이고 있습니다. 이는 소비자들이 살롱 품질의 래커를 맞춤형 유리병에 담아 주문 제작하는 추세에 따른 것입니다. 인플루언서들의 네일아트에 대한 관심 확대가 시장 규모를 키웠고, 제제 제조사들은 용매의 휘발을 최소화하기 위해 유리 용기를 선호하고 있습니다. 스킨케어 및 헤어케어 제품 라인은 한 자릿수 중반의 성장률을 보이고 있으며, 레티놀 세럼, 앰플, 고농축 마스크의 효과를 상징하는 유리 스포이드 보틀과 트리트먼트 병이 성장세를 보이고 있습니다. 메이크업 제품에서는 유리의 사용이 제한적이지만, 고급 브랜드가 한정판 페이스 미스트와 쿠션 컴팩트 리필용으로 장인정신이 깃든 병을 사용하면서 화장품 향수 유리병 포장 시장은 여러 미용 관습에 걸쳐 다양성을 유지하고 있습니다.

지역별 분석

북미는 2025년 세계 화장품 향수 유리병 포장 시장 매출의 37.10%를 차지했습니다. 이는 디자이너 향수 시장, 구독형 뷰티 박스, 빈 용기 반납을 통해 소비자에게 보상하는 강력한 회수 프로그램이 주도하고 있습니다. 고급 브랜드는 장인정신이 깃든 유리병을 브랜드 아이콘으로 계속 홍보하고 있으며, D2C 스타트업은 폐기물을 줄이기 위해 리필용 포드를 도입하고 있습니다. 캐나다의 확대된 생산자 책임 제도는 유리 폐기물의 회수를 보조하고 있으며, 이는 지역 용해로에 공급되어 화장품 향수 유리병 포장 시장 규모를 지원하는 폐쇄 루프 스트림을 촉진하고 있습니다.

아시아태평양은 급성장 동력으로서 2031년까지 CAGR 5.36%로 확대될 것으로 예상됩니다. 이는 TikTok에서 시작된 뷰티 트렌드와 중국, 인도, 인도네시아의 가처분 소득 증가가 견인하고 있습니다. 중국 본토의 향수 수요 증가로 인해 주문 제작 병의 주문 기록이 갱신되고 있으며, 인도 소비자층은 두꺼운 벽면 유리를 진품의 증거로 간주하는 경향이 강해져 화장품 향수 유리병 포장 시장에 대한 수요가 증가하고 있습니다. 국내 K-Beauty 수출기업은 유효성분을 활성화까지 분리 보존하는 이실형 유리 앰플을 개발하는 등 국내 연구개발이 기존 포맷을 획기적으로 진화하고 있음을 보여주고 있습니다.

유럽은 EU 규정 2025/40의 규제력과 그라스, 에더오버슈타인, 팔마와 같은 유서 깊은 향수 산업 클러스터의 지원을 받고 있습니다. 성숙한 회수 시스템을 통해 생산자는 높은 카렛(유리 파편) 회수율을 달성할 수 있으며, 화장품 향수 유리병 포장 시장 진입 기업은 가격을 압박하는 버진 배치 추가 비용 없이 브랜드의 탄소 목표를 달성할 수 있습니다. 동유럽은 낮은 에너지 요금을 활용하여 가치 중심의 부싯돌 병을 공급하는 반면, 서유럽의 컨버터는 장식의 우수성과 고급스러운 마감에 초점을 맞추고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The cosmetic perfumery glass bottle packaging market was valued at USD 2.61 billion in 2025 and estimated to grow from USD 2.73 billion in 2026 to reach USD 3.42 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031).

This moderate yet resilient growth trajectory reflects the sector's ability to navigate supply-chain volatility while capitalizing on premiumization trends that favor glass over alternative materials. The market's expansion occurs against a backdrop of transformative regulatory shifts, particularly EU Regulation 2025/40, which mandates that all packaging be recyclable by 2030. This regulation positions glass as a strategic advantage, given its infinite recyclability without degradation in quality. Macro forces reshaping the industry center on sustainability mandates intersecting with luxury positioning strategies. The premiumization wave in beauty and fragrance products drives demand for aesthetically superior packaging that conveys brand heritage and product integrity. Simultaneously, e-commerce expansion creates dual pressures: brands require visually compelling packaging for digital marketing while needing impact-resistant solutions to minimize breakage-related returns.

Global Cosmetic Perfumery Glass Bottle Packaging Market Trends and Insights

Premiumisation of Beauty and Fragrance Products

Premium beauty and fragrance brands increasingly position glass packaging as a tangible expression of product quality and brand heritage, driving specification shifts away from plastic alternatives. This trend accelerates as consumer willingness to pay premium prices for luxury cosmetics increases, particularly in emerging markets where glass packaging is seen as a symbol of authenticity and prestige. The premiumization effect creates a virtuous cycle: higher product prices justify the costs of glass packaging, while glass packaging reinforces premium positioning and enables further price increases. Luxury fragrance launches consistently specify custom glass flacons with unique shapes, colors, and decorative elements that plastic cannot replicate, cementing glass as the material of choice for high-end positioning. Digital marketing amplifies this trend, as glass packaging photographs better for social media and e-commerce platforms, creating additional value for brands that invest in visual differentiation.

Sustainability Push for Infinitely-Recyclable Glass

Regulatory frameworks and corporate sustainability commitments converge to favor the infinite recyclability advantage of glass packaging over plastic alternatives. The EU's Packaging and Packaging Waste Regulation mandates that all packaging be recyclable by 2030, with glass achieving 74% recycling rates compared to significantly lower plastic recycling performance. Glass recycling creates a closed-loop system where post-consumer cullet can constitute up to 82% of new bottle content without quality degradation, as demonstrated by O-I's carbon-neutral Estampe bottle. Corporate sustainability strategies are increasingly recognizing the contribution of glass packaging to Scope 3 emissions reduction, with brands like SGD Pharma launching bottles with 20% post-consumer recycled content, specifically designed for cosmetics applications. The sustainability narrative resonates particularly strongly with Gen Z consumers, who prioritize environmental credentials and view glass as a superior alternative to plastic.

Plastic Packaging Cost and Weight Advantage

Plastic packaging maintains significant cost and logistics advantages that hinder the adoption of glass, particularly in mass-market cosmetic segments where price sensitivity limits the selection of premium materials. Plastic containers typically cost 40-60% less than equivalent glass packaging, while weighing substantially less, which reduces shipping costs and the carbon footprint associated with high-volume distribution. Advanced plastic formulations are increasingly replicating glass aesthetics through clear polymers and surface treatments, enabling premium positioning without the costs associated with glass. The weight differential becomes particularly pronounced for large-format products and multi-product sets, where glass packaging can double shipping costs compared to plastic alternatives. E-commerce growth amplifies these concerns as brands optimize packaging for cost-effective fulfillment while minimizing damage-related returns and customer dissatisfaction.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Demand for Aesthetic, Impact-Resistant Packs

- Laser-Enabled Personalisation and Anti-Counterfeit Engraving

- Volatile Energy and Soda-Ash Input Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Perfumes accounted for a 46.28% portion of the cosmetic perfumery glass bottle packaging market in 2025, underscoring how fragrance houses rely on inert glass containers to preserve complex scent profiles. This dominant foothold equates to the single-largest slice of the cosmetic perfumery glass bottle packaging market share. The segment benefits from a well-established association between bespoke flacons and luxury positioning, enabling brands to maintain premium price points even during cost-inflation cycles. Strong marketing support from designer labels sustains steady reorder volumes, keeping the cosmetic perfumery glass bottle packaging market resilient to demand swings in adjacent beauty categories.

Nail care, although still comparatively smaller, is expanding at a 6.05% CAGR through 2031, the fastest growth among all tracked products, as consumers trade up to salon-quality lacquers packaged in custom glass vials. Growing influencer interest in nail art has expanded the addressable market, and formulators prefer glass to minimize solvent evaporation. Skin-care and hair-care lines report mid-single-digit advances as glass dropper bottles and treatment jars signal efficacy for retinol serums, ampoules, and concentrated masks. Although make-up remains selective in its use of glass, prestige brands tap artisanal flacons for limited-edition face mists and cushion-compact refills, keeping the cosmetic perfumery glass bottle packaging market diversified across multiple beauty rituals.

The Cosmetic Perfumery Glass Bottle Packaging Market Report is Segmented by Product Type (Perfumes, Skin Care, Nail Care, Hair Care, and More), Capacity (0-50 Ml, 50-150 Ml, and >150 Ml), Color (Flint, Amber, Frosted, Special-Coloured, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.10% of the worldwide cosmetic perfumery glass bottle packaging market revenue in 2025, driven by its established designer-fragrance ecosystem, subscription beauty boxes, and robust take-back programs that reward consumers for returning empty primary containers. Prestige houses continue to champion artisanal glass flacons as brand icons, while direct-to-consumer startups integrate refill pods to cut waste. Canada's Extended Producer Responsibility regime subsidizes cullet collection, which feeds regional furnaces and supports a closed-loop stream that bolsters the cosmetic perfumery glass bottle packaging market size.

The Asia-Pacific region is the sprinting growth engine, with a 5.36% CAGR to 2031, driven by TikTok-driven beauty trends and rising disposable incomes in China, India, and Indonesia. Mainland China's fragrance awakening triggers record custom-flacon briefs, and Indian consumers increasingly associate heavy-walled glass with authenticity, steering incremental demand toward the cosmetic perfumery glass bottle packaging market. South Korea's K-Beauty exporters innovate dual-chamber glass ampoules that keep active powders separate until activation, demonstrating how regional R&D leapfrogs legacy formats.

Europe remains anchored by regulatory muscle EU Regulation 2025/40 and storied perfumery clusters in Grasse, Idar-Oberstein, and Parma. Producers harvest high cullet ratios from mature collection schemes, allowing cosmetic perfumery glass bottle packaging market participants to hit brand carbon targets without price-crippling virgin-batch surcharges. Eastern Europe supplies value-centric flint bottles, leveraging lower energy tariffs, while Western converters focus on decoration excellence and luxury finishing.

- Verescence France SASU

- Gerresheimer AG

- Pochet SAS

- HEINZ-GLAS GmbH & Co. KGaA

- Bormioli Luigi S.p.A.

- Vitro, S.A.B. de C.V.

- PGP Glass Private Limited

- Stoelzle Glass Group

- Zignago Vetro S.p.A.

- Berlin Packaging LLC

- Saver Glass SAS

- Pragati Glass Pvt Ltd

- Baralan International S.p.A.

- Lumson S.p.A.

- vetroelite packaging s.r.l

- Feemio Group Co., Ltd.

- Brandsamor Commerce LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumisation of beauty and fragrance products

- 4.2.2 Sustainability push for infinitely-recyclable glass

- 4.2.3 E-commerce demand for aesthetic, impact-resistant packs

- 4.2.4 Laser-enabled personalisation and anti-counterfeit engraving

- 4.2.5 EU-2025/40 regulation favouring recyclable mono-material packs

- 4.2.6 Electrified and lightweight furnaces cutting cost and CO2

- 4.3 Market Restraints

- 4.3.1 Plastic packaging cost and weight advantage

- 4.3.2 Volatile energy and soda-ash input prices

- 4.3.3 EU packaging-minimisation rules curbing heavy, ornate flacons

- 4.3.4 High e-commerce breakage / return rates for fragile glass

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Perfumes

- 5.1.2 Skin Care

- 5.1.3 Nail Care

- 5.1.4 Hair Care

- 5.1.5 Other Product Type

- 5.2 By Capacity

- 5.2.1 0-50 ml

- 5.2.2 50-150 ml

- 5.2.3 >150 ml

- 5.3 By Color

- 5.3.1 Flint

- 5.3.2 Amber

- 5.3.3 Frosted

- 5.3.4 Special-coloured

- 5.3.5 Other Color

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verescence France SASU

- 6.4.2 Gerresheimer AG

- 6.4.3 Pochet SAS

- 6.4.4 HEINZ-GLAS GmbH & Co. KGaA

- 6.4.5 Bormioli Luigi S.p.A.

- 6.4.6 Vitro, S.A.B. de C.V.

- 6.4.7 PGP Glass Private Limited

- 6.4.8 Stoelzle Glass Group

- 6.4.9 Zignago Vetro S.p.A.

- 6.4.10 Berlin Packaging LLC

- 6.4.11 Saver Glass SAS

- 6.4.12 Pragati Glass Pvt Ltd

- 6.4.13 Baralan International S.p.A.

- 6.4.14 Lumson S.p.A.

- 6.4.15 vetroelite packaging s.r.l

- 6.4.16 Feemio Group Co., Ltd.

- 6.4.17 Brandsamor Commerce LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment