|

시장보고서

상품코드

1938995

유럽의 종이 포장 시장 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe Paper Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

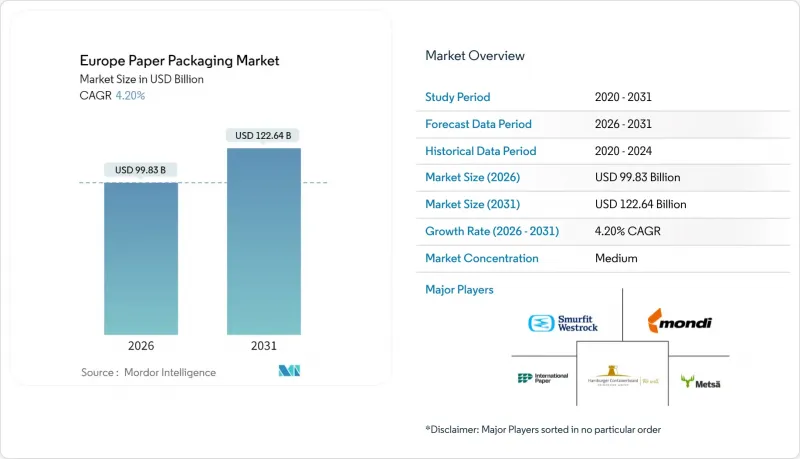

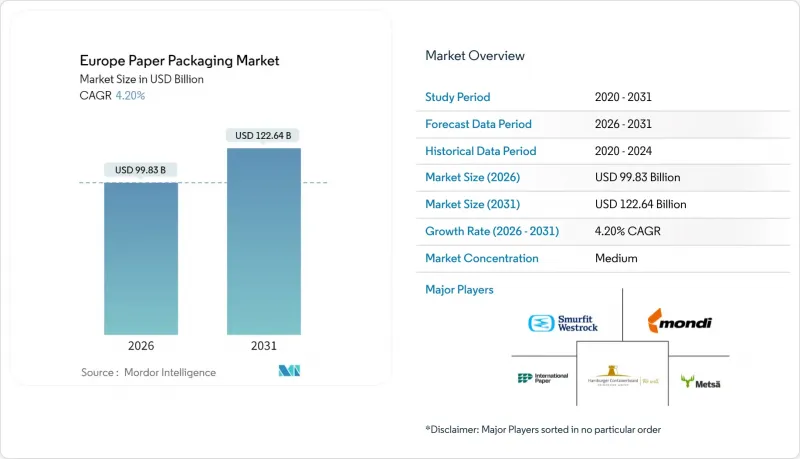

유럽의 종이 포장 시장은 2025년 958억 1,000만 달러에서 2026년에는 998억 3,000만 달러로 성장하며, 2026-2031년에 CAGR 4.20%로 추이하며, 2031년까지 1,226억 4,000만 달러에 달할 것으로 예측되고 있습니다.

이 시장의 성장은 유럽 대륙의 순환 경제 모델로의 규제 전환, 소매업체들의 광범위한 재활용 가능 포맷 선호, 고강도 골판지 소재의 지속적인 기술 혁신에 의해 촉진되고 있습니다. 섬유 기반 솔루션은 ISO 14040 수명주기 평가에서 확인된 재활용 용이성과 저탄소 강도를 결합하여 외식 산업, E-Commerce 및 밀키트 응용 분야에서 플라스틱을 점점 더 많이 대체하고 있습니다. 특히 북유럽의 제지 공장에 대한 업스트림 투자, 특히 재생원료 함유 판지의 생산능력에 대한 투자는 원자재 리스크를 줄이는 동시에 공급업체가 EU 탄소국경조정 메커니즘에 대응할 수 있게 해줍니다. 2024년 스머핏과 웨스트록의 합병을 포함한 활발한 합병 활동은 경쟁을 강화하고 수직적 통합을 가속화하며, 주요 기업이 버진 섬유와 재생 섬유 공급을 확보하고, 운송 비용을 최적화하며, 유럽 전역의 고객 기반에서 지속가능한 조달 감사를 표준화할 수 있도록 합니다. 에너지 가격 변동에 따른 단기적인 투입비용 상승 압력으로 이익률이 압박을 받고 있습니다. 그러나 온라인 소매의 보급, 퀵커머스의 편리함, 그리고 점점 더 엄격해지는 일회용 플라스틱 금지 조치로 인해 포장재 수요가 증가함에 따라 다운스트림 수요는 견고하게 유지되고 있습니다.

유럽 종이 포장 시장 동향과 인사이트

식품 및 음료 분야에서 지속가능하고 재활용 가능한 포장재에 대한 수요 증가

유럽의 식품 및 음료 브랜드들은 2030년까지 100% 재활용 가능한 포장 목표를 약속하고 있으며, 다층 플라스틱보다 섬유 소재를 우선시하는 조달 평가 기준을 도입하고 있습니다. 주요 유통업체들은 단일 소재의 섬유 트레이를 선호하고 있으며, 2025년 5월 마크스앤스펜서가 종이 섬유로 만든 레디밀 트레이를 도입한 사례는 이를 잘 보여줍니다. 증류주 제조업체와 양조장들은 스카치 위스키용 90% 종이병과 같은 주력 제품을 출시하여 종이가 환경에 미치는 영향이 적다는 소비자 인식을 강화하고 있습니다. 초콜릿 바 포장지를 대상으로 한 수명주기 연구 결과, 모든 중간 카테고리에서 종이가 방향성 폴리프로필렌(OPP)보다 온실 가스 배출량이 적은 것으로 확인되었습니다. 2026년 8월 시행 예정인 25ppb PFAS 규제에 대응하기 위해 포장 가공업체는 코팅 기술 공급업체와의 협력을 강화하고, 브랜드 소유자의 공개 지속가능성 로드맵에 따라 제품 재설계를 조정할 것입니다. ISO 14040 준수가 국경 간 중앙 조달 입찰에서 의무화됨에 따라 검증된 제조 공정 데이터(크래들 투 게이트)를 보유한 종이 솔루션은 다국적 식품 및 음료 그룹 전체에서 우선 공급업체로 선정될 수 있습니다.

E-Commerce 택배 물량 급증

유럽의 온라인 소매 구매는 두 자릿수 성장을 유지하고 있으며, 풀필먼트 센터의 박스 수와 보조 완충재의 급격한 증가를 촉진하고 있습니다. 옴니채널 식품 소매업체와 전문 소매업체들이 유통망을 강화한 결과, 영국의 골판지 소비량은 2010-2024년 12.6% 증가했습니다. 아마존은 2025년 1월 유럽 사업에서 100% 재생한 종이 파우치와 보드 봉투로 전환한 결과, 2018년 이후 10억 개 이상의 일회용 플라스틱 배송 봉투를 줄였다고 보고했습니다. 몬디와 CMC Packaging Automation이 공동 개발한 솔루션과 같은 자동 최적 크기 포장 설비는 주문형 박스 치수를 생성하여 종이 사용량을 최대 40%까지 줄이고, 트럭 적재 효율을 향상시킵니다. 도시 지역의 식료품 퀵커머스 시장은 2021년 250억 유로에서 2025년까지 720억 유로로 급성장할 것으로 예상되며, 10분 이내 배송 시간 내에 제품의 무결성을 유지할 수 있는 치수 최적화된 2차 포장이 요구되고 있습니다. 이 때문에 컨버터 업체들은 EC 사업자가 요구하는 대량 생산 규모와 브랜딩 유연성을 모두 충족시키기 위해 고속 다이 커팅 가공, 디지털 인쇄를 통한 커스터마이징, 인라인 품질관리 센서를 우선적으로 도입하고 있습니다.

삼림파괴 우려와 원자재 공급 불안정성에 대한 우려

2025년 시행되는 EU 삼림파괴 규제에 따라 지역적 위치정보에 기반한 산림 구획까지 추적이 의무화되며, 컨버터가 위성 검증과 블록체인 원장을 도입하는 과정에서 조달 비용이 3-5% 증가할 것으로 예측됩니다. 북유럽 제재소에서는 전력비 급등과 정기적인 작업 중단으로 인한 가동 중단이 발생하고 있으며, 버진 펄프 공급량도 부족하여 바이어들은 프리미엄 가격으로 현물 시장에서 조달할 수밖에 없는 상황입니다. 빌레루드의 생산성 향상 프로그램은 펄프 가격 상승과 원료 부족으로 인한 이익률 압박을 상쇄하기 위한 업계 전반의 시급성을 강조하고 있습니다. 밀짚, 미스칸사스 등 대체 섬유는 성형 섬유 식품 용기에서 주목받고 있지만, 섬유 길이와 백색도 편차로 인해 고화질 인쇄 패키지에 채택이 제한적입니다. 이베리아 반도와 발트해 연안의 산림에 대한 지역적 다각화는 집중화 위험을 줄이는 한편, 물류 체인을 연장하고 탄소발자국 감소 효과를 부분적으로 상쇄하고 있습니다. 중기적으로 제지공장은 이해관계자에게 안심감을 제공하고, 강화되는 실사 감사에 대응하기 위해 폐쇄형 물순환 시스템과 삼림 재생에 박차를 가하고 있습니다.

부문 분석

골판지 상자는 2025년 매출의 37.92%를 차지할 것으로 예상되며, 이는 풀필먼트, 산업 및 식료품 유통 채널 전반에서 골판지 상자가 주력 포맷으로 자리매김하고 있음을 강조합니다. 유럽 골판지 포장 시장 규모는 EC 소포의 급증, 맞춤형 인쇄 수요, 내압 강도를 유지하면서 화물 배출량을 줄이는 경량화의 지속적인 발전으로 인해 꾸준히 성장할 것으로 예측됩니다. 액체용 카톤은 2031년까지 연평균 복합 성장률(CAGR) 5.12%로 가장 높은 성장세를 보일 것으로 예상되며, 대체 유음료, 상온 보관이 가능한 주스 라인, 다층 플라스틱 사용 감소를 위한 브랜드 주도의 노력에 의해 주도될 것으로 보입니다.

접이식 카톤과 같은 2차 제품은 의약품 블리스터 포장의 오버랩, 정밀한 주름 가공과 광택 바니시를 통한 디스플레이 효과를 중시하는 고 그래픽 퍼스널케어 제품 포장에 있어서도 계속 중요성이 유지될 것입니다. 종이봉투와 소매용 가방은 전국적인 일회용 비닐봉투 사용 금지로 인해 다시 활기를 되찾고 있습니다. 식료품점에서는 재사용시 내구성을 높이기 위해 내습성 첨가제를 첨가한 크라프트지 제품으로 전환이 진행되고 있습니다. 특수 틈새 시장(찢어지지 않는 냉동용 봉투, 성형 섬유 트레이, 성형 펄프 완충재)은 대응 가능 물량이 확대되고 있지만, 골판지는 여전히 지역 전체 컨버터 공장 가동률과 설비투자의 정당성을 지원하는 핵심 제품입니다.

2025년에는 재생지 등급이 55.98%의 점유율을 차지할 것으로 예측됩니다. 이는 엄격한 사용 후 소비자 내용물 목표와 국내 제지 공장에 공급되는 견고한 회수 시스템의 결과입니다. 유럽 종이 포장 시장에서 재생 라이너의 점유율은 CBAM(Carbon Border Adjustment Mechanism)으로 인해 저탄소 재생 시트에 비해 버진 등급의 수입 비용이 높아짐에 따라 확대될 것으로 예측됩니다. 고품질 화이트 탑 테스트 라이너는 인쇄 가능한 표면이 필요한 디스플레이 지원 케이스에서 선호되는 반면, 갈색 테스트 라이너는 표준 운송용 상자에 주로 사용됩니다.

순수한 인쇄 재현성과 우수한 강성이 요구되는 고급 화장품 선물 상자, 의료기기 설명서, 접이식 상자에는 여전히 버진 펄프 기판이 필수적입니다. 분산형 또는 압출형 배리어 층을 갖춘 복합 판지는 수증기 및 내유성이 중요한 중간 영역을 차지하지만, PFAS 단계적 폐지 위험으로 인해 단기적인 확장은 억제되고 있습니다. 공급망에서는 강도와 부드러움의 균형을 맞추기 위해 스칸디나비아산 침엽수 공예와 이베리아산 유칼립투스 경재를 결합한 이중 소싱 전략이 주류로 자리 잡고 있습니다. 제지 공장은 유통업체와 순환형 파트너십을 구축하여 유통센터에서 폐골판지(OCC)를 회수함으로써 순환 시간을 단축하고 식품 등급 재생 소재에 필수적인 원료 순도를 보장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The Europe paper packaging market is expected to grow from USD 95.81 billion in 2025 to USD 99.83 billion in 2026 and is forecast to reach USD 122.64 billion by 2031 at 4.20% CAGR over 2026-2031.

The market gains momentum from the continent's regulatory shift toward circular economy models, widespread retailer preference for curbside-recyclable formats, and continuous technology upgrades in high-strength corrugated substrates. Fiber-based solutions increasingly displace plastic in food service, e-commerce, and meal-kit applications because they combine ease of recycling with lower carbon intensity confirmed in ISO 14040 life-cycle assessments. Upstream investments in recycled-content board capacity, especially at Nordic mills, mitigate raw-material risk while positioning suppliers for EU Carbon Border Adjustment Mechanism compliance. Heightened merger activity, including the 2024 Smurfit-WestRock combination, tightens competition and accelerates vertical integration, allowing majors to secure virgin and recycled fiber supplies, optimize freight costs, and standardize sustainable sourcing audits across pan-European customer bases. Near-term input-cost headwinds linked to energy volatility squeeze margins; nevertheless, downstream demand remains resilient because online retail penetration, quick-commerce convenience, and increasingly stringent single-use-plastic bans jointly lift packaging volumes.

Europe Paper Packaging Market Trends and Insights

Rising demand for sustainable and recyclable packaging in Food and Beverage

European food and beverage brands publicly commit to 100% recyclable packaging targets for 2030, prompting procurement scorecards that prioritize fiber over multilayer plastics. Leading grocers impose shelf-readiness criteria that reward mono-material fiber trays, as shown by Marks & Spencer's rollout of paper-fiber ready-meal trays in May 2025. Distillers and brewers showcase flagship launches such as a 90% paper bottle for Scotch whisky, reinforcing consumer perception that paper embodies lower environmental impact. Life-cycle studies covering chocolate bar wrappers confirm lower greenhouse-gas footprints for paper against oriented polypropylene in every midpoint category. Packaging converters intensify collaboration with coating-technology suppliers to meet upcoming 25 ppb PFAS limits in August 2026, aligning product reformulations with brand owners' public sustainability roadmaps. As ISO 14040 compliance becomes mandatory for cross-border central procurement tenders, paper solutions with verified cradle-to-gate data sets gain preferred-supplier status across multinational F&B groups.

Rapid surge in e-commerce parcel volumes

European online retail purchases maintain double-digit growth, fueling a steep rise in box counts and ancillary cushioning across fulfillment centers. Corrugated consumption in the United Kingdom increased 12.6% between 2010 and 2024 as omnichannel grocers and specialty retailers upgraded distribution networks. Amazon reports the elimination of more than 1 billion single-use plastic mailers since 2018 by converting its European operations to 100% recyclable paper pouches and board envelopes in January 2025. Automated right-size packaging equipment, such as solutions codeveloped by Mondi and CMC Packaging Automation, generates on-demand box dimensions that cut paper use up to 40% while improving truck-cubic-utilization metrics. Urban grocery quick-commerce, projected to jump from EUR 25 billion in 2021 to EUR 72 billion by 2025, requires dimensionally optimized secondary packs that preserve product integrity in 10-minute delivery windows. Consequently, converters prioritize high-speed die-cutting, digital print customization, and inline quality-control sensors to meet both volume scale and branding agility demanded by e-commerce merchants.

Deforestation concerns and raw-material supply volatility

The EU Deforestation Regulation, effective 2025, mandates traceability back to geolocated forest plots, adding 3-5% to procurement overhead as converters implement satellite verification and blockchain ledgers. Nordic sawmill capacity interruptions, stemming from electricity-cost surges and periodic labor stoppages, and thin virgin-fiber availability, are forcing buyers to tap spot markets at premium prices. Billerud's productivity program underscores industry-wide urgency to offset margin compression arising from pulp price spikes and raw-material scarcity. Alternative fibers such as wheat straw and miscanthus attract attention for molded-fiber food bowls, yet inconsistent fiber length and brightness curtail adoption for high-definition print packs. Geographic diversification toward Iberian and Baltic forests mitigates concentration risk but extends logistics chains, partially reversing carbon-footprint gains. Over the medium term, mills expedite closed-loop water systems and reforestation commitments to reassure stakeholders and comply with tightening due diligence audits.

Other drivers and restraints analyzed in the detailed report include:

- EU Single-Use Plastics Directive accelerating fiber substitution

- Advancements in lightweight, high-strength corrugated technology

- Improving recyclability of flexible plastics narrowing advantage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corrugated boxes held 37.92% of 2025 revenue, underscoring their status as the workhorse format across fulfillment, industrial, and grocery distribution channels. Europe's paper packaging market size for corrugated boxes is projected to compound steadily, given e-commerce parcel proliferation, customized print runs, and continuous lightweighting gains that lower freight emissions without forfeiting crush strength. Liquid cartons post the fastest 5.12% CAGR through 2031, propelled by dairy-alternative beverages, shelf-stable juice lines, and brand-led commitments to curb multilayer plastics usage.

Secondary products such as folding cartons maintain relevance for pharmaceutical blister overwraps and high-graphic personal-care packs where precise creasing and glossy varnishes create shelf appeal. Paper sacks and retail bags regain momentum as national bans phase out single-use plastic carriers, with grocers switching to kraft options featuring wet-strength additives for reuse durability. Specialty niches-tear-resistant freezer bags, shaped formed-fiber trays, and molded-pulp void-fill expand addressable volumes, yet corrugated remains the anchor that underpins converter plant utilization rates and capex justification across the region.

Recycled grades captured 55.98% share in 2025, an outcome of stringent post-consumer content targets and robust collection systems that feed domestic mills. Europe paper packaging market share for recycled liner is expected to widen as CBAM makes imports of virgin grades more expensive relative to low-carbon recycled sheet. High-quality white-top testliner gains favor in display-ready cases requiring printable surfaces, while brown testliner dominates standard shipping cartons.

Virgin-fiber substrates remain indispensable for premium cosmetics gift boxes, medical device manuals, and folding cartons demanding pristine print fidelity and superior stiffness. Composite paperboard featuring dispersion or extrusion barriers occupies a middle ground where water-vapor and fat resistance are critical, yet PFAS-phase-out risk tempers near-term expansion. Supply chains gravitate toward dual-sourcing strategies, combining Scandinavian softwood kraft with Iberian eucalyptus hardwood to balance strength and smoothness. Mills engage in circularity partnerships with retailers to backhaul OCC (old corrugated containers) from distribution centers, shortening loop time and securing feedstock purity levels imperative for food-grade recycled content.

The Europe Paper Packaging Market Report is Segmented by Product Type (Folding Cartons, Corrugated Boxes, Paper Bags and Sacks, and More), Material Type (Virgin Fiber Paper, and More), End-User Industry ( Healthcare and Pharmaceutical, Personal Care and Household, and More), Packaging Format (Primary Packaging, Secondary Packaging, and Tertiary Packaging), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Smurfit WestRock

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Svenska Cellulosa Aktiebolaget SCA

- Metsa Board Oyj

- Mayr-Melnhof Karton AG

- Prinzhorn Holding GmbH

- Progroup AG

- Schumacher Packaging GmbH

- Klingele Papierwerke GmbH & Co. KG

- Graphic Packaging Holding Company

- RAJA Groupe

- VPK Packaging Group NV

- RDM Group (Reno De Medici S.p.A.)

- Lucart S.p.A.

- Essity AB

- Palm GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for sustainable and recyclable packaging in FandB

- 4.2.2 Rapid surge in e-commerce parcel volumes

- 4.2.3 EU Single-Use Plastics Directive accelerating fiber substitution

- 4.2.4 Advancements in lightweight, high-strength corrugated technology

- 4.2.5 Growth of meal-kit and quick-commerce requiring right-sized packs

- 4.2.6 EU Carbon Border Adjustment Mechanism driving recycled mills

- 4.3 Market Restraints

- 4.3.1 Deforestation concerns and raw material supply volatility

- 4.3.2 Improving recyclability of flexible plastics narrowing advantage

- 4.3.3 Energy-price shocks raising mill operating costs

- 4.3.4 PFAS-phase-out uncertainty in barrier-coated papers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECAST (VALUE)

- 5.1 By Product Type

- 5.1.1 Folding Cartons

- 5.1.2 Corrugated Boxes

- 5.1.3 Paper Bags and Sacks

- 5.1.4 Liquid Cartons

- 5.1.5 Other Paper Packaging

- 5.2 By Material Type

- 5.2.1 Virgin Fiber Paper

- 5.2.2 Recycled Paper

- 5.2.3 Composite Paperboard

- 5.3 By End-user Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Healthcare and Pharmaceutical

- 5.3.4 Personal Care and Household

- 5.3.5 E-commerce and Retail

- 5.3.6 Tobacco

- 5.3.7 Other End-user Industries

- 5.4 By Packaging Format

- 5.4.1 Primary Packaging

- 5.4.2 Secondary Packaging

- 5.4.3 Tertiary Packaging

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock

- 6.4.2 Mondi plc

- 6.4.3 International Paper Company

- 6.4.4 Stora Enso Oyj

- 6.4.5 Svenska Cellulosa Aktiebolaget SCA

- 6.4.6 Metsa Board Oyj

- 6.4.7 Mayr-Melnhof Karton AG

- 6.4.8 Prinzhorn Holding GmbH

- 6.4.9 Progroup AG

- 6.4.10 Schumacher Packaging GmbH

- 6.4.11 Klingele Papierwerke GmbH & Co. KG

- 6.4.12 Graphic Packaging Holding Company

- 6.4.13 RAJA Groupe

- 6.4.14 VPK Packaging Group NV

- 6.4.15 RDM Group (Reno De Medici S.p.A.)

- 6.4.16 Lucart S.p.A.

- 6.4.17 Essity AB

- 6.4.18 Palm GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment