|

시장보고서

상품코드

1939002

미국의 농업기계 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

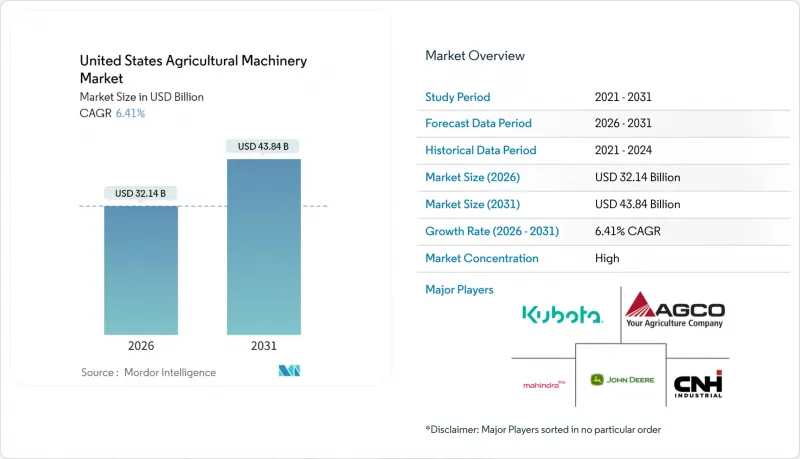

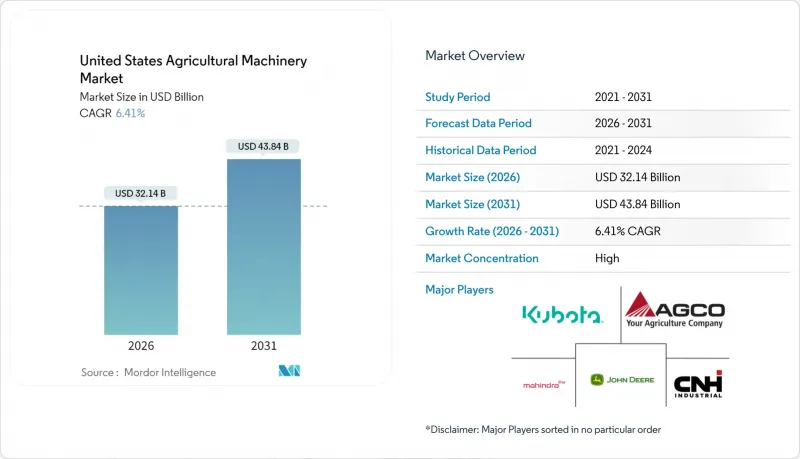

미국의 농업기계 시장은 2025년에 302억 달러로 평가되었으며, 2026년 321억 4,000만 달러에서 2031년까지 438억 4,000만 달러에 달할 것으로 예측됩니다.

예측 기간(2026-2031년) 동안 CAGR은 6.41%로 예상됩니다.

기후변화 대응을 위한 실천, 정밀기술로의 전환, 전기화 투자에 대한 연방정부의 인센티브는 주기적인 시장 변동을 상쇄하는 데 도움이 될 것입니다. 장비 소유주들은 운영 비용 절감과 지속가능성 목표 달성을 위해 기능 향상에 집중하고 있으며, 텔레매틱스, 예지보전, 자율주행 대응 시스템에 대한 수요가 증가하고 있습니다. 대리점 통합으로 애프터서비스 네트워크가 개선되는 한편, 리스 및 구독 옵션은 금리 상승의 영향을 완화하는 데 기여합니다. 물 부족이 심화되고 배출 규제가 강화되는 가운데 미국 농업기계 시장에서 관개 부문의 높은 성장률이 두드러집니다.

미국 농업기계 시장 동향과 인사이트

정밀농업용 개보수 키트 보급 확대

개조 솔루션을 통해 농가는 기존 농기계의 수명을 연장하는 동시에 데이터 기반 개선을 통해 비료와 농약 사용량을 최대 30%까지 절감할 수 있습니다. 트랙터 1대당 5만 달러의 개조 투자비용은 자율주행 대응 신규 장비에 필요한 40만 달러보다 훨씬 낮은 수준이며, 보통 3년 이내에 투자 회수가 가능합니다. 중규모 밭작물 농장에서는 부채를 늘리지 않고 비용 경쟁력을 유지하기 위해 이러한 솔루션의 도입이 확대되고 있습니다. 장비 판매업체는 개조 키트 설치 및 조정을 통한 추가 서비스 수익을 얻을 수 있어 고객 관계 강화 및 수익성 향상으로 이어집니다. 모듈식 업그레이드의 확산으로 장비 교체 주기가 길어짐에 따라 OEM 업체들은 판매량에서 소프트웨어와 통합 서비스로 초점을 옮기고 있습니다.

주요 OEM 제조사별 전동화 로드맵

존디어는 2026년 최초의 완전 전기-자율주행 대응 트랙터를 출시할 예정이며, 배터리 공급을 위해 크라이젤 일렉트릭에 투자했습니다. AGCO는 2024년 Fendt e100 Vario를 시험 도입하고, 전기 파워트레인에 중점을 둔 연구개발비를 60% 증액했습니다. 현재 배터리 밀도로 전기 트랙터는 120마력 미만의 용도에 국한되어 있는데, 이는 과수원, 채소 농장, 낙농장의 요구 사항에 부합합니다. 미국 천연자원보존국(NRCS)은 구매 비용의 50% 이상을 부담하는 비용 분담 프로그램을 제공하여 소규모 농장의 재정적 장벽을 낮추고 있습니다. 제조업체들은 향후 배터리 기술 향상으로 고마력 적용이 가능해질 것으로 예상하고 있으며, 현재 부품 공급업체들은 미국 내 배터리 및 인버터 생산 확대를 추진하고 있습니다.

딜러 기술자 부족

농기계 서비스 산업은 심각한 인력 부족에 직면해 있습니다. 서비스 거점 통합으로 실점포 수가 줄어들어 중요한 파종기 및 수확기 대응 시간이 길어지고 있습니다. 현대의 정밀 농기계는 고도의 진단 능력을 필요로 하고, 지방 노동시장에서 확보할 수 있는 기술을 넘어서고 있기 때문에 제조업체(OEM)는 원격 지원 서비스 확대와 모듈식 부품 교환 시스템을 도입해야 합니다. 이러한 노동력 제약으로 인해 농가의 농기계 구매가 억제되는 경향이 있습니다.

부문 분석

트랙터는 2025년 기준 미국 농업기계 시장에서 50.62%의 점유율을 유지하며 경작, 파종, 자재 취급에 있어 필수적인 역할을 하고 있습니다. 이 부문의 매출 성장은 고출력 모델에서 비롯된 것이며, 특수 농업용 소형 트랙터에 전기 구동 시스템 채택이 확대되고 있는 것도 이 부문의 매출 성장에 기여했습니다. 관개시설은 규모는 작지만 2031년까지 CAGR 9.26%라는 가장 높은 성장률을 달성할 것으로 예상됩니다. 센터 피벗, 점적 관개 라인, 센서 제어 밸브를 포함한 현대식 관개 시스템은 실시간 토양 수분 데이터를 통합하여 물 소비량을 최대 25%까지 줄일 수 있습니다. 이러한 성장은 서부 지역의 지하수 규제와 연방정부의 WaterSMART 프로그램에 의한 인센티브와 일치합니다.

경운-경작 시스템에서는 각 제조사가 가변 심경 기술을 채택하여 토양 교란을 줄였습니다. 무경운 농법의 확대에도 불구하고 꾸준한 성장세를 유지하고 있습니다. 첨단 파종 및 식재 장비는 단립 파종을 가능하게 하여 발아율 향상과 정밀한 시비를 실현합니다. 수확기 수요는 작물 가격과 연동되지만, 예측 주행 속도 자동화 기능을 갖춘 신형 콤바인은 연료 효율과 처리 능력을 향상시켜 갱신 수요를 견인하고 있습니다. 농가들은 신규 기계 구매보다는 자율주행 안내 및 가변 속도 제어 장치를 통한 기존 장비의 업그레이드를 선택하는 경향이 강해지고 있으며, 그 결과 부품 및 디지털 서비스 수익이 장비 판매액보다 더 많이 발생하고 있습니다. 모든 장비 카테고리에서 센서 시스템과 ISOBUS 호환 컨트롤러가 브랜드에 의존하지 않는 생태계를 구축하여 제조업체의 락인(lock-in)을 완화하고 있습니다. 이에 따라 기존 제조사들은 트랙터 시장에서의 지위를 유지하기 위해 오픈 API를 제공할 것을 요구받고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트 지원(3개월)

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The United States agricultural machinery market was valued at USD 30.2 billion in 2025 and estimated to grow from USD 32.14 billion in 2026 to reach USD 43.84 billion by 2031, at a CAGR of 6.41% during the forecast period (2026-2031).

Federal incentives for climate-smart practices, precision technology retrofits, and electrification investments help counterbalance cyclical market fluctuations. Equipment owners focus on upgrading capabilities to reduce operational costs and achieve sustainability goals, increasing demand for telematics, predictive maintenance, and autonomous-ready systems. Dealer consolidation improves after-sales service networks, while leasing and subscription options help mitigate the impact of higher interest rates. The irrigation segments demonstrate higher growth rates in the United States agricultural machinery market, driven by increasing water scarcity and stricter emissions regulations.

United States Agricultural Machinery Market Trends and Insights

Widespread Adoption of Precision-Ag Retro-Fit Kits

Retro-fit solutions enable farmers to extend their existing fleet's lifespan while reducing fertilizer and pesticide usage by up to 30% through data-driven improvements. The investment of USD 50,000 per tractor for retrofitting is significantly lower than the USD 400,000 required for new autonomous-ready equipment, typically resulting in a return on investment within three years. Mid-scale row-crop farms increasingly adopt these solutions to maintain cost competitiveness without increasing debt. Equipment dealers benefit from additional service revenue through installation and calibration of retrofit kits, which strengthens customer relationships and improves profitability. The growing adoption of modular upgrades extends equipment replacement cycles, causing Original Equipment Manufacturers (OEMs) to shift their focus from unit sales to software and integration services.

Electrification Road-Maps by Major Original Equipment Manufacturers

Deere & Company plans to launch its first all-electric, autonomous-capable tractor in 2026 and has invested in Kreisel Electric for battery supply. AGCO introduced the Fendt e100 Vario to pilot fleets in 2024, supported by a 60% increase in research and development spending focused on electric powertrains. Current battery density limits electric tractors to under-120-horsepower applications, which align with the requirements of fruit, vegetable, and dairy farms. The Natural Resources Conservation Service (NRCS) offers cost-share programs that can cover over 50% of purchase costs, reducing financial barriers for small farms. While manufacturers expect future battery technology improvements to enable higher-horsepower applications, current progress has encouraged component suppliers to expand United States battery and inverter production.

Dealer Technician Shortage

The equipment service industry faces a significant labor shortage. The consolidation of service locations has reduced the number of physical stores, increasing response times during critical planting and harvest periods. Modern precision equipment requires specialized diagnostic capabilities that exceed the skills available in rural labor markets, compelling Original Equipment Manufacturers (OEMs) to expand remote support services and implement modular component replacement systems. These labor constraints have led farmers to restrict their purchases of agricultural machinery.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Telematics-Based Predictive Maintenance

- Climate-Smart Grant Incentives

- Lengthy Environmental Protection Agency Tier 5 Emission Compliance Lead-Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractors maintain a 50.62% share of the United States agricultural machinery market in 2025, demonstrating their essential role in tillage, seeding, and material handling. The segment's revenue growth stems from high-horsepower models, while compact tractors increasingly incorporate electric drivetrains for specialty farming applications. Irrigation equipment, though a smaller segment, is projected to achieve the highest growth rate at 9.26% CAGR through 2031. Modern irrigation systems, including center pivots, drip lines, and sensor-controlled valves, integrate real-time soil moisture data, reducing water consumption by up to 25%. This growth aligns with Western state groundwater regulations and federal WaterSMART program incentives.

In plowing and cultivating systems, manufacturers incorporate variable-depth tillage technology to reduce soil disruption, maintaining steady growth despite increasing no-till farming practices. Advanced seeding and planting equipment enable precise single-kernel placement, improving emergence rates and supporting precise nutrient application. While harvesting machinery demand correlates with row-crop prices, new combines featuring predictive ground-speed automation improve fuel efficiency and throughput, driving replacement demand. Farmers increasingly opt to upgrade existing equipment with autonomous guidance and variable-rate controllers instead of purchasing new machinery, resulting in parts and digital service revenue exceeding equipment sales. Across equipment categories, sensor systems and ISOBUS-compatible controllers establish brand-independent ecosystems, reducing manufacturer lock-in and requiring traditional manufacturers to provide open APIs to maintain tractor market position.

The United States Agricultural Machinery Market Report is Segmented by Product Type (Tractors, Plowing and Cultivating Machinery, and More), and by Farm Size (Less Than 500 Acres, 500-2, 000 Acres, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- CLAAS KGaA mbH

- KUHN SAS

- Same Deutz-Fahr S.P.A.

- Kinze Manufacturing

- Horsch, LLC

- Ploeger Oxbo Group B.V.

- Argo Tractors S.p.A.

- Netafim Limited (An Orbia Business)

- Valmont Industries, Inc.

- Yanmar Holdings Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Widespread Adoption of Precision-Ag Retro-Fit Kits

- 4.2.2 Electrification Road-Maps by Major Original Equipment Manufacturers

- 4.2.3 Rising Adoption of Telematics-Based Predictive Maintenance

- 4.2.4 Climate-Smart Grant Incentives

- 4.2.5 Surge in Bespoke Equipment Leasing Models

- 4.2.6 Venture-Backed Robotics Start-Ups Targeting Speciality Crops

- 4.3 Market Restraints

- 4.3.1 Dealer Technician Shortage

- 4.3.2 Patchy Rural 5G Coverage for Connected Machinery

- 4.3.3 Volatile Commodity-Price Swings Curbing Farm Capital Expenditure

- 4.3.4 Lengthy Environmental Protection Agency Tier 5 Emission Compliance Lead-times

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Tractors

- 5.1.2 Plowing and Cultivating Machinery

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.2.4 Other Plowing and Cultivating Machinery

- 5.1.3 Planting Machinery

- 5.1.3.1 Seed Drills

- 5.1.3.2 Planters

- 5.1.3.3 Spreaders

- 5.1.3.4 Other Planting Machinery

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Other Harvesting Machinery

- 5.1.5 Haying and Forage Machinery

- 5.1.5.1 Mowers

- 5.1.5.2 Balers

- 5.1.5.3 Other Haying and Forage Machinery

- 5.1.6 Irrigation Machinery

- 5.1.6.1 Sprinkler Irrigation

- 5.1.6.2 Drip Irrigation

- 5.1.6.3 Other Irrigation Machinery

- 5.1.7 Other Agricultural Machinery

- 5.2 By Farm Size

- 5.2.1 Less Than 500 acres

- 5.2.2 500-2,000 acres

- 5.2.3 More Than 2,000 acres

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial NV

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra Ltd.

- 6.4.6 CLAAS KGaA mbH

- 6.4.7 KUHN SAS

- 6.4.8 Same Deutz-Fahr S.P.A.

- 6.4.9 Kinze Manufacturing

- 6.4.10 Horsch, LLC

- 6.4.11 Ploeger Oxbo Group B.V.

- 6.4.12 Argo Tractors S.p.A.

- 6.4.13 Netafim Limited (An Orbia Business)

- 6.4.14 Valmont Industries, Inc.

- 6.4.15 Yanmar Holdings Co., Ltd.