|

시장보고서

상품코드

1939008

탄산칼슘 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

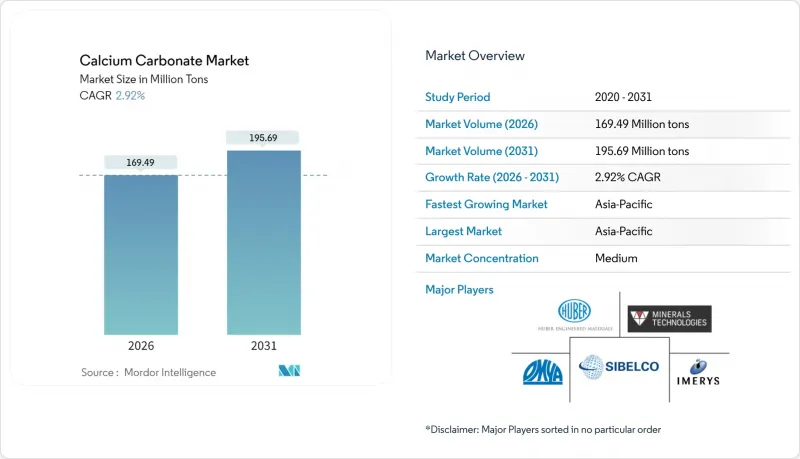

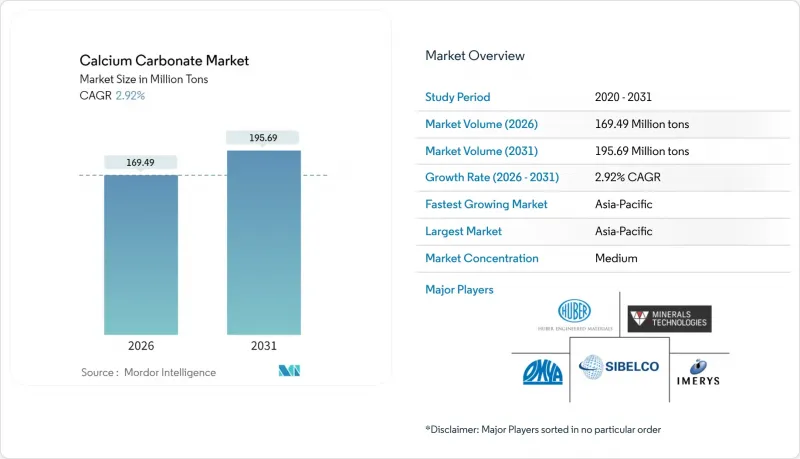

2026년 탄산칼슘 시장 규모는 1억 6,949만 톤으로 추정되며, 2025년 1억 6,468만 톤으로부터 성장이 전망됩니다. 2031년의 예측치는 1억 9,569만 톤으로, 2026-2031년에 CAGR 2.92%로 확대할 전망입니다.

이러한 꾸준한 물량 기반 성장은 플라스틱, 종이, 건축자재, 의약품, 농업 분야에서 비용절감용 충진제 및 성능 향상제로서의 역할을 입증하고 있습니다. 신흥 국가의 인프라 투자 증가, E-Commerce에 따른 포장 및 종이 제품의 지속적인 수요, 칼슘 보충제를 함유한 건강 및 영양 제품으로의 꾸준한 전환은 수요를 더욱 강화시키고 있습니다. 광산에서 응용까지 일관 생산 능력을 갖춘 제조업체는 유리한 물류 체계와 최종 용도 사양에 맞는 등급 조정 능력의 혜택을 누리고 있습니다. 한편, 환경 규제 강화로 인해 에너지 절약형 분쇄설비, 저탄소 침전라인, 재생석회석 원료에 대한 투자가 가속화되면서 주요 지역 전체에서 비용구조 재구축이 진행되고 있습니다.

세계 탄산칼슘 시장 동향 및 전망

건설 및 인프라 개발 가속화

아시아태평양의 유틸리티 지출이 급증하면서 건설업체들이 시멘트, 폴리머 개질 콘크리트, 건축용 페인트, 실란트용 비용 효율적인 광물성 필러를 찾는 가운데 탄산칼슘 시장이 성장하고 있습니다. 통합 생산업체는 이러한 수요에 대응하기 위해 생산 능력을 확대했다: 이멜리스는 앨라배마주 사일라카우가 공장의 생산량을 두 배로 늘려 건설용 자재 공급과 북미 고객에 대한 리드타임을 개선했습니다. 도시계획 담당자들의 저탄소 건축자재 추진도 ReMined(100% 사전소비자 재생 탄산칼슘) 등의 제품 수요를 증가시키고 있습니다. 이 제품은 강도와 내구성의 기준을 유지하면서 제품에 내재된 탄소량을 줄입니다. 이러한 지속가능성 관련 틈새 시장을 통해 판매업체는 대량판매가 꾸준히 증가하는 상황에서도 더 높은 이익률을 확보할 수 있습니다.

플라스틱 및 폴리머의 용도 확대

나노 스케일 연삭 기술과 표면 처리 화학의 급속한 발전으로 필름 마스터배치 엔지니어링 플라스틱 등급의 성능 한계가 향상되었습니다. 나노 탄산칼슘은 포장재의 인장강도, 배리어성, 열 안정성을 높이고 투명성을 유지하여, 컨버터는 수지 사용량을 중량 대비 최대 5%까지 줄일 수 있습니다. 중국 제조업체인 후베이 미결정 신소재는 생분해성 폴리머에 분산된 100나노미터 미만의 입자를 통해 필름 강화와 분해 속도 미세 조정을 동시에 실현하는 방법을 입증하여 순환 경제 포장의 요구 사항을 직접적으로 지원합니다. 자동차 제조업체와 전자제품 브랜드는 경량화, 내열성, 재활용성 등의 목표를 달성하기 위해 이러한 기능성 필러의 채택을 확대하고 있습니다.

탄산칼슘과 관련된 건강 위험

분진을 흡입할 수 있는 탄산칼슘 분진에 대한 근로자의 노출로 인해 규제 감시가 강화되고 있으며, 공장 및 하류 공장의 허용 노출 한계치를 낮추고 더 엄격한 봉쇄 기준을 요구하고 있습니다. 나노입자의 독성학은 여전히 연구 중이며, 식품 및 의약품 용도 승인을 위해서는 광범위한 위험 평가가 일상적으로 필요하며, 이는 상용화 일정을 연장하고 규정 준수 비용을 증가시킬 수 있습니다. 자본이 부족한 소규모 생산자들은 폐쇄 루프 처리나 고효율 여과 장비 도입에 어려움을 겪는 경우가 많아 공급의 유연성을 제약하는 경우가 많습니다.

부문 분석

풍부한 석회암 광상과 저에너지 제분 공정으로 인해 분쇄된 탄산칼슘은 2025년 수요의 76.92%를 차지하며 탄산칼슘 시장의 핵심으로 남을 것입니다. 기초지, 폴리올레핀 필름, 레미콘 등 대량 소비 분야에서는 분쇄 탄산칼슘의 우수한 가성비가 결정적인 요인으로 작용하고 있습니다. 그러나 침강 탄산칼슘(PCC)은 좁은 입자 크기 분포, 높은 밝기, 맞춤형 표면 화학적 특성에 대해 고객이 프리미엄을 지불함에 따라 2031년까지 연평균 복합 성장률(CAGR) 3.31%로 성장 속도를 가속화하고 있습니다. 이러한 변화는 연구진이 대두 우레아제를 이용한 효소 유도 침전을 실현함으로써 PCC의 적용 범위를 확대할 수 있는 비용 절감 경로를 제시했습니다.

성숙한 GCC 제조업체들은 탄산 반응 장치의 고가의 설비 투자를 피하면서 PCC 성능에 근접하기 위해 분급 분쇄 시스템 및 건식 코팅 장치를 갖춘 플랜트 개조를 진행하고 있습니다. 한편, PCC 공급업체들은 다국적 고객사의 중요성이 커지는 조달 기준인 탄소발자국 감축을 위해 사내 이산화탄소 포집 설비와 재생에너지 투입량 확대를 추진하고 있습니다. 이러한 전략이 수렴되면서 경쟁은 치열해지고 있지만, 건설, 플라스틱, 생명과학 산업 수요 프로파일 차이를 고려할 때 두 하위 부문의 탄산칼슘 시장 규모는 꾸준히 확대될 것으로 예측됩니다.

본 탄산칼슘 보고서는 유형별(미분쇄 탄산칼슘, 침전 탄산칼슘), 용도별(건축자재용 원료, 영양 보충제, 열가소성 플라스틱 첨가제, 충진제 및 안료 등), 최종사용자 산업별(제지, 플라스틱, 접착제 및 실란트, 건설 등), 지역별(아시아태평양, 북미, 남미, 유럽, 아시아태평양, 유럽, 중동 및 아프리카, 중동 및 아프리카) 아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분석됩니다.

지역별 분석

아시아태평양은 2025년 탄산칼슘 시장의 48.25%를 차지할 것으로 예상되며, 2031년까지 연평균 복합 성장률(CAGR) 3.62%로 확대될 것으로 예측됩니다. 중국은 지역 수요의 대부분을 차지하고 있으며, 이멜리스는 우후, 청양, 악양에 시설을 운영하며 포장, 건설, 생명과학 분야의 고객에게 공급하고 있습니다. 동남아시아 국가에서도 코팅지 및 PVC 파이프의 생산능력이 확대되고 있으며, 지역 수요 기반이 확대되고 있습니다.

북미는 기술 등급을 우선시하고 엄격한 품질관리를 특징으로 하는 첨단인 플라스틱 및 의약품 공급망을 통해 탄탄한 기반을 유지하고 있습니다. 최근 앨라배마와 조지아 주에 대한 투자는 운송시 배출량을 줄이고 신속한 기술 지원을 보장하기 위해 현지 조달에 대한 이 지역의 의지를 지원합니다. 유럽에서는 엄격한 탄소 저감 규제와 채석장 복원 규정으로 인해 재생 원료와 에너지 절약형 침전 플랜트가 중요시되고 있습니다. 남미에서는 브라질과 아르헨티나의 건설 붐과 더불어 농업 비즈니스의 성장이 토양 처리제 소비를 촉진하고 있습니다. 중동에서는 석유화학 콤비네이션 및 대규모 인프라 프로젝트에서 안정적인 수요가 예상됩니다. 한편, 아프리카의 채석 잠재력은 미개발이지만 유망하며, 특히 이집트, 나이지리아, 남아프리카공화국이 주목받고 있습니다. 고품질 석회암 광상의 지역적 분산은 앞으로도 무역 흐름과 지역 가격에 계속 영향을 미칠 것이지만, 현지에 설치된 침전 플랜트 및 고도화된 분쇄 기지 구축으로 인해 세계 탄산칼슘 시장의 운송 부담은 점차 감소하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05Calcium Carbonate market size in 2026 is estimated at 169.49 million tons, growing from 2025 value of 164.68 million tons with 2031 projections showing 195.69 million tons, growing at 2.92% CAGR over 2026-2031.

This steady volume-based growth underscores the mineral's entrenched role as both a cost-saving filler and a performance enhancer in plastics, paper, construction materials, pharmaceuticals, and agriculture. Demand is reinforced by rising infrastructure outlays in emerging economies, sustained packaging and paper requirements tied to e-commerce, and a steady pivot toward health-and-nutrition products that incorporate calcium supplements. Producers with integrated mine-to-application capabilities are benefiting from favorable logistics and the ability to tailor grades to end-use specifications. Meanwhile, environmental regulations are accelerating investment in energy-efficient grinding, low-carbon precipitation lines, and recycled limestone feedstocks, reshaping cost structures across every major region.

Global Calcium Carbonate Market Trends and Insights

Accelerating Construction and Infrastructure Development

Surging public-works spending across Asia-Pacific is boosting the calcium carbonate market as builders seek cost-effective mineral fillers for cement, polymer-modified concrete, architectural coatings, and sealants. Integrated producers have ramped up capacity to meet this requirement: Imerys doubled output at its Sylacauga, Alabama unit to supply construction-grade material and improve lead times for North American customers. Urban planners' push for low-carbon building materials is also raising demand for products such as ReMined, a 100% pre-consumer recycled calcium carbonate that reduces embodied carbon while maintaining strength and durability benchmarks. These sustainability-linked niches allow sellers to command higher margins even as bulk volumes grow steadily.

Expanding Plastic and Polymer Applications

Rapid advances in nano-scale grinding and surface-treatment chemistries have shifted the performance ceiling for film, masterbatch, and engineered-plastic grades. Nano-calcium carbonate enhances tensile strength, barrier properties, and thermal stability in packaging while preserving clarity, letting converters cut resin intensity by up to 5% on a weight basis. Chinese producer Hubei Micro Crystal New Materials demonstrated how sub-100 nm particles dispersed in biodegradable polymers can both toughen films and fine-tune degradation rates, directly supporting circular-economy packaging mandates. Automotive OEMs and electronics brands are increasingly specifying these functional fillers to meet lightweighting, heat-resistance, and recyclability targets.

Health Hazards Associated with Calcium Carbonate

Worker exposure to respirable calcium carbonate dust has sharpened regulatory oversight, prompting lower permissible exposure limits and more stringent containment norms in mills and downstream plants. Nanoparticle toxicology remains under study, and approvals for food or pharma applications now routinely require extensive risk assessments, which can prolong commercialization timelines and inflate compliance costs. Small producers with limited capital often struggle to install closed-loop handling and high-efficiency filtration, constraining supply flexibility.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand from the Paper and Packaging Industry

- Rising Healthcare and Pharmaceutical Usage

- Environmental and Mining Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ground calcium carbonate continues to anchor the calcium carbonate market, claiming 76.92% of 2025 demand thanks to abundant limestone deposits and low-energy milling routes. In volume-driven sectors such as basic paper, polyolefin film, and ready-mix concrete, GCC's favorable price-performance ratio remains decisive. Yet precipitated calcium carbonate is setting the pace with a 3.31% CAGR through 2031 as customers pay premiums for narrow particle-size distribution, higher brightness, and customizable surface chemistry. This shift was underscored when researchers achieved enzyme-induced precipitation using soybean urease, signaling cost-reduction paths that could widen PCC's reach.

Mature GCC producers are therefore retooling plants with classified grinding systems and dry-coating units to edge closer to PCC performance without incurring the steep capex of carbonation reactors. Meanwhile, PCC suppliers are scaling captive carbon-dioxide recovery and renewable-energy inputs to shrink their carbon footprint, an increasingly important procurement criterion for multinational customers. As these strategies converge, competitive intensity is rising, but the calcium carbonate market size for both sub-segments is projected to expand steadily, given differentiated demand profiles across construction, plastics, and life-science industries.

The Calcium Carbonate Report is Segmented by Type (Ground Calcium Carbonate and Precipitated Calcium Carbonate), Application (Raw Substance for Construction Material, Dietary Supplement, Additive for Thermoplastics, Filler and Pigment, and More), End-User Industry (Paper, Plastic, Adhesives and Sealants, Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East, and Africa).

Geography Analysis

Asia-Pacific dominated the calcium carbonate market with a 48.25% share in 2025 and is projected to advance at a 3.62% CAGR through 2031. China accounts for the lion's share of regional demand; Imerys operates facilities in Wuhu, Qingyang, and Yueyang to supply packaging, construction, and life-science customers. Southeast Asian economies are also adding coated-board and PVC-pipe capacity, broadening the regional demand base.

North America maintains a solid foothold owing to advanced plastics and pharmaceutical supply chains that prioritize technical grades and stringent quality control. Recent investments in Alabama and Georgia underscore the region's appetite for localized supply that cuts freight emissions and ensures rapid technical support. Europe's stringent carbon-reduction and quarry-rehabilitation rules make recycled feedstocks and energy-efficient precipitation plants critical. South America is leveraging construction booms in Brazil and Argentina alongside agribusiness growth that lifts soil-treatment consumption. The Middle East sees steady demand from petrochemical complexes and large-scale infrastructure projects, while Africa's quarrying potential remains underdeveloped but promising, particularly in Egypt, Nigeria, and South Africa. Geographic dispersion of high-grade limestone deposits will continue to influence trade flows and regional pricing, but localized precipitation units and upgraded grinding hubs are gradually trimming transport intensity across the global calcium carbonate market.

- ACCM

- GCCP Resources Limited

- Gulshan Polyols Ltd.

- Huber Engineered Materials

- Imerys

- Jordan Carbonate Company

- Manaseer Group

- Minerals Technologies Inc.

- Nigtas

- OKUTAMA KOGYO CO.,LTD.

- Omya International AG

- Provencale SA

- SaudiCarbonate

- SCHAEFER KALK GmbH & Co. KG

- Shiraishi Group

- Sibelco

- SigmaRoc Plc

- VMPC Joint Stock Company.

- Zantat Sdn. Bhd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Construction and Infrastructure Development

- 4.2.2 Expanding Plastic and Polymer Applications

- 4.2.3 Growing Demand from the Paper and Packaging Industry

- 4.2.4 Rising Healthcare and Pharmaceutical Usage

- 4.3 Market Restraints

- 4.3.1 Health Hazards Associated with Calcium Carbonate

- 4.3.2 Environmental and Mining Regulations

- 4.3.3 Logistics and Supply Chain Challenges

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

- 4.6 Import/Export Trade Statistics

5 Market Size and Growth Forecasts (Volume)

- 5.1 Type

- 5.1.1 Ground Calcium Carbonate (GCC)

- 5.1.2 Precipitated Calcium Carbonate (PCC)

- 5.2 Application

- 5.2.1 Raw Substance for Construction Material

- 5.2.2 Dietary Supplement

- 5.2.3 Additive for Thermoplastics

- 5.2.4 Filler and Pigment

- 5.2.5 Component of Adhesives

- 5.2.6 Desulfurization of Fuel Gas

- 5.2.7 Neutralizing Agent in Soil

- 5.2.8 Other Applications

- 5.3 End-user Industry

- 5.3.1 Paper

- 5.3.2 Plastic

- 5.3.3 Adhesives and Sealants

- 5.3.4 Construction

- 5.3.5 Paints and Coatings

- 5.3.6 Pharmaceutical

- 5.3.7 Automotive

- 5.3.8 Agriculture

- 5.3.9 Rubber

- 5.3.10 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Australia and New Zealand

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Iran

- 5.4.5.4 Iraq

- 5.4.5.5 Kuwait

- 5.4.5.6 Qatar

- 5.4.5.7 Rest of the Middle-East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Rest of Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ACCM

- 6.4.2 GCCP Resources Limited

- 6.4.3 Gulshan Polyols Ltd.

- 6.4.4 Huber Engineered Materials

- 6.4.5 Imerys

- 6.4.6 Jordan Carbonate Company

- 6.4.7 Manaseer Group

- 6.4.8 Minerals Technologies Inc.

- 6.4.9 Nigtas

- 6.4.10 OKUTAMA KOGYO CO.,LTD.

- 6.4.11 Omya International AG

- 6.4.12 Provencale SA

- 6.4.13 SaudiCarbonate

- 6.4.14 SCHAEFER KALK GmbH & Co. KG

- 6.4.15 Shiraishi Group

- 6.4.16 Sibelco

- 6.4.17 SigmaRoc Plc

- 6.4.18 VMPC Joint Stock Company.

- 6.4.19 Zantat Sdn. Bhd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Emerging Importance of Green Applications

- 7.3 Advancements in High-Performance Plastics and Polymers