|

시장보고서

상품코드

1939017

세제 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Detergents - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

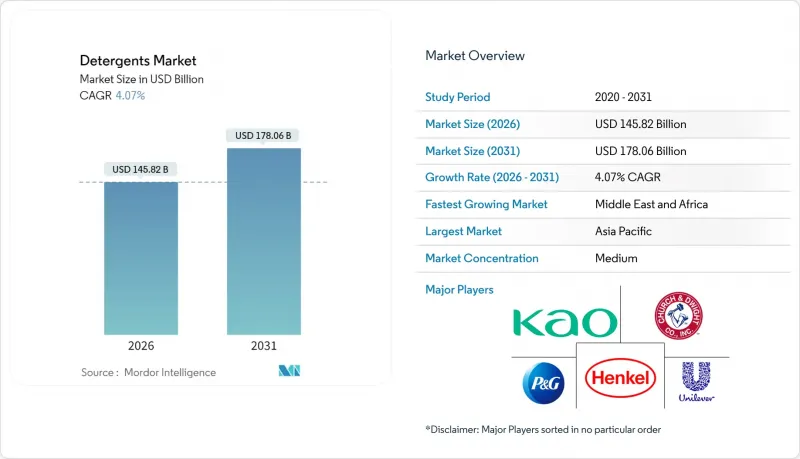

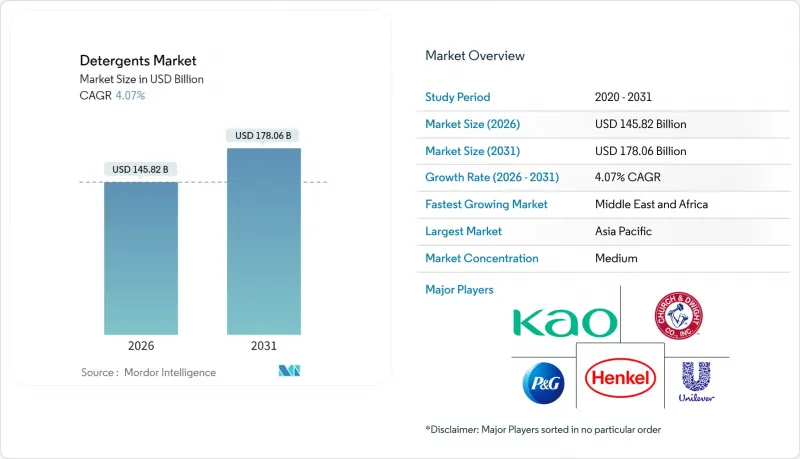

세제 시장은 2025년에 1,401억 2,000만 달러로 평가되며, 2026년 1,458억 2,000만 달러에서 2031년까지 1,780억 6,000만 달러에 달할 것으로 예측되고 있습니다. 예측 기간(2026-2031년)의 CAGR은 4.07%로 전망되고 있습니다.

구조적 변화는 가정용 에너지 사용량을 줄이는 냉수용 효소, 초농축형을 촉진하는 탄소 가격 정책, 생분해성 계면활성제의 채택을 가속화하는 규제 요건에 기인합니다. 아시아태평양은 세탁기의 급속한 보급으로 수요를 견인하고 있으며, 북미와 중국에서는 소비자 직접 판매(D2C) 구독 서비스가 라스트마일 경제를 재정의하고 있습니다. 경쟁은 여전히 치열하며, 프록터 앤 갬블, 유니레버, 헨켈은 효소 기술과 농축 포드를 활용하여 프리미엄 가격을 유지하고 있습니다. 한편, 지역 전문 기업은 가뜩이나 어려운 가계 예산에 대응하는 소포장 포장으로 점유율을 확대하고 있습니다. 팜핵유와 효소의 원료 비용 변동은 중견 브랜드의 이익률을 압박하고 있지만, 공급 제약을 피할 수 있는 조류 유래 및 발효 기반 계면활성제에 대한 투자를 가속화하고 있습니다.

세계 세제 시장 동향과 인사이트

신흥 국가 세탁기 보급률 상승

인도의 자동세탁기 보유율은 2020년 14%에서 2024년 28%로 증가하여 1인당 세제 사용량 증가로 이어지고 있습니다. 드럼세탁기는 손세탁에 비해 30-40% 더 많은 세제가 필요하기 때문입니다. 250ml의 소형 액상팩이나 10회분 소봉투는 40% 이상의 이익률을 유지하면서 저렴한 가격으로 도입이 가능합니다. 인도네시아나 베트남에서도 비슷한 보급 곡선을 보이고 있으며, 가전제품 보조금과 할부금 제도가 기여하고 있습니다. 현재 배합 설계자들은 30분, 20℃ 사이클에 최적화된 효소를 지정하고 있으며, BASF의 라바지 프로테아제는 35% 에너지 절감으로 동등한 수준의 오염 제거 효과를 발휘합니다.

세제 분야 E-Commerce 및 D2C 채널의 빠른 성장세

브랜드가 소매업체의 25-35% 마킹을 피하면서 소비자 구독은 2024년 42억 달러로 전년 대비 38% 성장한 것으로 나타났습니다. 낮은 고객 확보 비용(가입자당 18달러)과 3차 배송 후 해지율이 15% 미만인 점이 수익성을 지원하고 있습니다. 북미에서 32%, 중국에서 41%에 달하는 온라인 판매는 당일 배송 물류와 성분 투명성을 강조하는 인플루언서 마케팅이 주도했습니다. 액체 세제와 동등한 농축 포드 스트립은 70% 더 가볍고, 라스트 마일 운송 비용을 0.12달러 절감하고, 포장 폐기물을 60% 줄입니다.

엄격한 국제 및 지역 화학물질 규제

2023년 10월, 유럽화학물질청(ECHA)은 REACH 규정 부속서 XVII에 따라 마이크로플라스틱의 사용을 제한하고, 씻어내는 세제에 의도적으로 사용하는 것을 금지했습니다. 전환 기간은 4년 12년까지입니다. 2024년 4월, 미국 환경보호청(EPA)은 PFAS 규제를 확대하여 제조업체가 계면활성제 및 가공 보조제에 포함된 퍼플루오로알킬 물질 및 폴리플루오로알킬 물질이 10억분의 1을 초과하지 않음을 증명하도록 의무화했습니다. 이에 따라 산업용 및 상업용 세정제에서 기존의 불소계 계면활성제가 사실상 금지되었습니다. 이러한 규제는 신속한 재조합을 위한 연구개발 예산이 부족한 중소 지역 브랜드에 불균형적인 영향을 미칩니다. 반면, 다국적 기업은 연간 50만 톤이 넘는 세계 생산량으로 컴플라이언스 비용을 분산시킬 수 있습니다.

부문 분석

2025년 음이온 계면활성제는 세제 시장 점유율의 45.84%를 차지했습니다. 이는 남아시아 및 아프리카에서 분말 및 액체 세제의 주력 제품을 지원하는 저가의 선형 알킬벤젠 설포네이트에 힘입은 것입니다. 비이온성 알코올 에톡실레이트 및 알킬 폴리글루코사이드는 빠른 최종 생분해성 평가와 EU의 '28일 이내 호기성 분해' 규제에 힘입어 CAGR 4.95%를 나타낼 것으로 예측됩니다. 헨켈은 2024년 Persil Sensitive의 배합을 재검토하여 LAS의 40%를 옥수수 전분에서 추출한 알킬 폴리글루코사이드로 대체했습니다. 이를 통해 제품의 성능은 유지하면서 수생 독성을 35% 감소시켰습니다.

양이온성 4급 암모늄계 계면활성제는 그 양전하가 음이온계와의 공배합을 제한하므로 유연제 이외의 분야에서는 틈새 시장으로 존재합니다. 미국 환경보호청(EPA)의 쿼타늄계 화합물에 대한 감시 강화에 따라 보다 빠르게 생분해되는 에스테르계 쿼타늄 대체품의 시험 도입이 추진되고 있습니다. 양성 이온성 코카미드 프로파일 베타인은 2024년사용량의 6%를 차지하여 중동 및 북아프리카의 경수 시장에서 발포성을 안정화시킬 것입니다. 또한 광범위한 pH 안정성을 가지고 있으며, 미네랄 킬레이트제를 피하는 냉수용 포드에 적합합니다.

지역별 분석

아시아태평양은 2025년 세계 총량의 44.10%를 차지할 것으로 예상되며, 인도와 인도네시아의 세탁기 보유량 2배 증가, 중국의 탄탄한 E-Commerce, 효소가 풍부한 액체 세제의 고급화 추세에 힘입어 성장세를 이어갈 것으로 보입니다. 블루문(Blue Moon), 리비(Libby)와 같은 현지 유명 브랜드는 온라인 직접 판매과 특제 향료로 중국 액체 세제 시장의 38%를 점유하고 있습니다. 인도 시장은 2024년 7.2% 성장했으며, 세탁기 첫 구매층을 겨냥한 저가형 250ml 팩이 주도했습니다. 성숙한 시장인 일본과 한국에서는 바이오 유래 이세티온산 계면활성제가 30%의 얼룩 분해 촉진 효과로 주목받고 있습니다.

중동 및 아프리카은 도시화로 인해 1인당 소비량이 3kg을 넘어설 것으로 예상되며, CAGR이 4.78%로 가장 높은 성장이 예상됩니다. 사우디의 '비전 2030'에 따른 인프라 구축으로 세탁기 보급률이 65%에 육박하면서 경수 대응 포드에 대한 수요가 확대되고 있습니다. 남아공 시장은 2024년 수량 기준으로 5.8% 증가했습니다. 이는 간헐적인 전력 공급이 필요한 저온 세탁 사이클에서도 우수한 성능을 발휘하는 효소 강화 분말 세제가 주도하고 있습니다. 사하라 이남 아프리카 농촌지역은 봉지 가격대의 분말세제가 주류를 이루고 있지만, 라고스나 나이로비에서는 프론트 로더 세탁기의 보급과 함께 액체세제에 대한 수요가 증가하고 있습니다.

유럽과 북미는 성장률이 둔화되고 있는 반면, 지속가능성 분야에서 혁신을 주도하고 있습니다. 독일에서는 환경 인증 제품이 2024년 세제 매출의 42%를 차지했습니다. 미국에서는 포드 시트형 제품이 세탁량의 32%를 차지하며, 캐나다와 영국 식료품점의 리필 스테이션은 포장을 40% 줄였습니다. 남미는 2024년 4.2% 성장할 것입니다. 분말세제는 여전히 68%의 점유율을 유지하고 있지만, 세탁기 보유율이 55% 이상의 브라질과 아르헨티나의 도시 지역에서는 액체세제가 증가하는 추세입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 개요

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSA 26.03.05The Detergents Market was valued at USD 140.12 billion in 2025 and estimated to grow from USD 145.82 billion in 2026 to reach USD 178.06 billion by 2031, at a CAGR of 4.07% during the forecast period (2026-2031).

Structural shifts stem from cold-water enzymes that reduce household energy use, carbon-pricing policies favoring ultra-concentrated formats, and regulatory mandates that accelerate the adoption of biodegradable surfactants. The Asia-Pacific region continues to drive demand, largely due to the rapid adoption of washing machines, while direct-to-consumer (D2C) subscription services are redefining last-mile economics in North America and China. Competitive intensity remains high: Procter & Gamble, Unilever, and Henkel leverage enzyme technology and concentrated pods to command premium pricing, whereas regional specialists gain share with sachet distribution that meets tight household budgets. Input-cost volatility in palm-kernel oil and enzymes compresses margins for mid-tier brands yet hastens investment in algae-derived and fermentation-based surfactants that bypass constrained supply chains.

Global Detergents Market Trends and Insights

Rising Washing-Machine Penetration in Emerging Economies

Automatic washer ownership in India increased from 14% in 2020 to 28% in 2024, resulting in a rise in per-capita detergent usage, as drum cycles require 30%-40% more product than hand-washing. Smaller 250ml liquid packs and 10-wash sachets help keep entry prices low while sustaining margins above 40%. Similar adoption curves in Indonesia and Vietnam benefit from appliance subsidies and installment-payment schemes. Formulators now specify enzymes optimized for 30-minute, 20°C cycles, with BASF's Lavergy protease delivering equivalent stain removal at 35% lower energy consumption.

Boom in E-Commerce and D2C Channels for Detergents

Direct-to-consumer subscriptions generated USD 4.2 billion in 2024, representing a 38% year-over-year growth as brands bypass retailers' 25%-35% markup. Lower acquisition costs (USD 18 per subscriber) and churn below 15% after the third delivery underpin profitability. Online sales reached 32% in North America and 41% in China, driven by same-day logistics and influencer marketing that emphasize ingredient transparency. Concentrated pods and strips, 70% lighter than equivalent liquids, shave USD 0.12 from last-mile freight while reducing packaging waste by 60%.

Stringent Global and Regional Chemical Regulations

In October 2023, the European Chemicals Agency, under REACH Annex XVII, restricted microplastics, banning their intentional use in rinse-off detergents with transition periods of 4 to 12 years. In April 2024, the US Environmental Protection Agency expanded PFAS restrictions, requiring manufacturers to certify that surfactants and processing aids contain no per- and polyfluoroalkyl substances above 1 part per billion, effectively banning legacy fluorosurfactants in industrial and institutional cleaning products. These regulations disproportionately affect smaller regional brands, which lack the R&D budgets for rapid reformulation, while multinationals spread compliance costs over global volumes exceeding 500,000 metric tons annually.

Other drivers and restraints analyzed in the detailed report include:

- Consumer Shift to Eco-Friendly and Biodegradable Formulations

- Cold-Water Enzyme Breakthroughs Cut Energy Use

- Raw-Material Price Volatility (Surfactants, Enzymes)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anionic surfactants held 45.84% of the Detergents market share in 2025, supported by low-cost linear alkylbenzene sulfonates that anchor powder and liquid staples in South Asia and Africa. Non-ionic alcohol ethoxylates and alkyl polyglucosides, prized for rapid ultimate biodegradation, are forecast to grow at a 4.95% CAGR, lifted by EU rules requiring aerobic breakdown within 28 days. Henkel reformulated Persil Sensitive in 2024 by substituting 40% of LAS with corn-starch-derived alkyl polyglucosides, thereby lowering aquatic toxicity by 35% while retaining the product's performance.

Cationic quaternary ammonium surfactants remain niche outside fabric softeners because their positive charge limits co-formulation with anionics. EPA scrutiny of quats is prompting pilots of faster-biodegrading ester-quat alternatives. Zwitterionic cocamidopropyl betaine, 6% of 2024 volume, stabilizes foam in hard-water markets across the Middle East and North Africa, and its broad pH stability suits cold-water pods that avoid mineral chelators.

The Detergents Market Report is Segmented by Type (Anionic, Cationic, Non-Ionic, and Zwitterionic), Application (Laundry, Household Cleaning, Dishwashing, Fuel Additives, Biological Reagents, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region accounted for 44.10% of the global 2025 volume, driven by a doubling of washing-machine ownership in India and Indonesia, robust e-commerce in China, and a shift toward premiumization of enzyme-rich liquids. Local champions such as Blue Moon and Liby hold a 38% share of China's liquid category through direct online engagement and tailored fragrances. India's market expanded by 7.2% in 2024, driven by affordable 250 ml packs targeting first-time machine users. Mature Japan and South Korea focus on bio-based isethionate surfactants that accelerate soil release by 30%.

The Middle East & Africa are forecast to deliver the fastest growth, with a 4.78% CAGR, as urbanization lifts per-capita consumption above 3 kg. Saudi Arabia's Vision 2030 infrastructure push raises washer penetration toward 65%, spurring demand for hard-water-tolerant pods. South Africa's market increased by 5.8% in volume in 2024, driven by enzyme-fortified powders that perform well in cold cycles, a necessity amid intermittent electricity supply. Sachet-priced powders dominate rural Sub-Saharan Africa, but liquid formats are gaining traction in Lagos and Nairobi as front-load adoption increases.

Europe and North America register slower growth but lead sustainability innovation. Germany's eco-labeled segment reached 42% of 2024 detergent sales. US pods and strips command 32% of laundry volume, and refill stations in Canadian and UK grocers reduce packaging by 40%. South America grew by 4.2% in 2024; powders still hold a 68% share, but liquids are rising in urban Brazil and Argentina, alongside washer ownership above 55%.

- Blue Moon Group

- Church & Dwight Co., Inc.

- Guangzhou Liby Group Co. Ltd

- Henkel AG & Co. KGaA

- Johnson & Johnson Private Limited

- Kao Corporation

- Lion Corporation

- Nice Group

- Procter & Gamble

- Reckitt Benckiser Group plc

- RSPL Group

- SC Johnson

- Seventh Generation Inc.

- Unilever

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising washing-machine penetration in emerging economies

- 4.2.2 Boom in e-commerce and D2C channels for detergents

- 4.2.3 Consumer shift to eco-friendly/biodegradable formulations

- 4.2.4 Cold-water enzyme breakthroughs cut energy use

- 4.2.5 Carbon-tax driven demand for ultra-concentrates

- 4.3 Market Restraints

- 4.3.1 Stringent global and regional chemical regulations

- 4.3.2 Raw-material price volatility (surfactants, enzymes)

- 4.3.3 Micro-plastic filtration mandates raise reformulation costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Anionic Detergents

- 5.1.2 Cationic Detergents

- 5.1.3 Non-ionic Detergents

- 5.1.4 Zwitterionic (Amphoteric) Detergents

- 5.2 By Application

- 5.2.1 Laundry Cleaning Products

- 5.2.2 Household Cleaning Products

- 5.2.3 Dishwashing Products

- 5.2.4 Fuel Additives

- 5.2.5 Biological Reagents

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Spain

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Blue Moon Group

- 6.4.2 Church & Dwight Co., Inc.

- 6.4.3 Guangzhou Liby Group Co. Ltd

- 6.4.4 Henkel AG & Co. KGaA

- 6.4.5 Johnson & Johnson Private Limited

- 6.4.6 Kao Corporation

- 6.4.7 Lion Corporation

- 6.4.8 Nice Group

- 6.4.9 Procter & Gamble

- 6.4.10 Reckitt Benckiser Group plc

- 6.4.11 RSPL Group

- 6.4.12 SC Johnson

- 6.4.13 Seventh Generation Inc.

- 6.4.14 Unilever

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment