|

시장보고서

상품코드

1939041

빌딩 정보 모델링(BIM) : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Building Information Modeling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

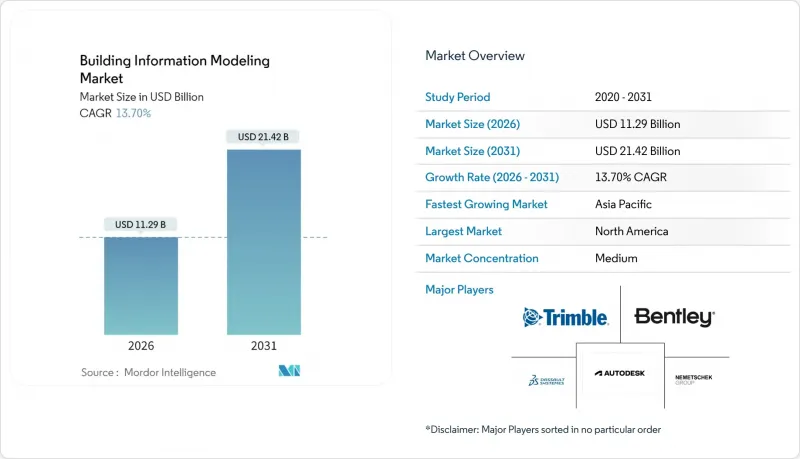

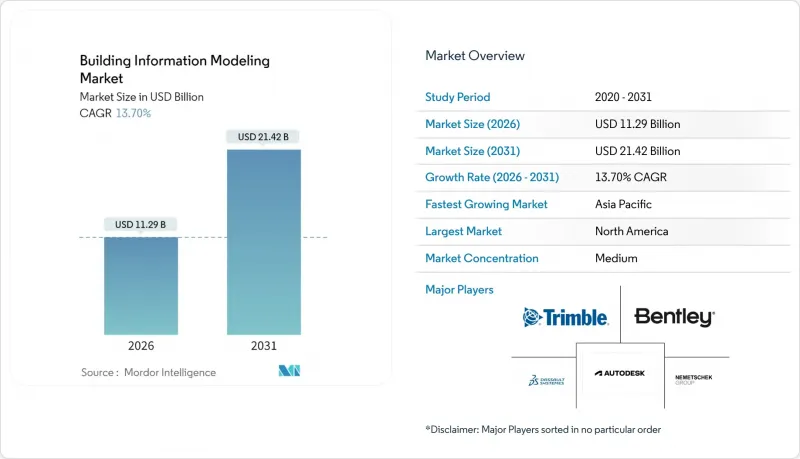

빌딩 정보 모델링(BIM) 시장은 2025년 99억 3,000만 달러에서 2026년에는 112억 9,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 13.7%를 기록하며 2031년까지 214억 2,000만 달러에 달할 것으로 예측됩니다.

건축, 엔지니어링, 건설, 운영 분야의 급속한 디지털 전환으로 인해 BIM은 단순한 시각화 도구에서 클라우드 기반의 협업 플랫폼으로 진화하고 있습니다. 정부의 규제 강화, 인공지능 및 디지털 트윈과의 통합, 중소기업의 초기 비용을 절감할 수 있는 SaaS의 보급 확대가 성장을 견인하고 있습니다. 각 벤더들은 4D 스케줄링, 5D 비용추정, 지속가능성 분석 등을 표준 기능으로 통합하고 있으며, 이로 인해 타사로의 전환 장벽은 여전히 높은 수준을 유지하고 있습니다. 치열한 경쟁으로 인해 상호운용성과 워크플로우 자동화를 향상시키는 지속적인 업그레이드가 이루어지고 있으며, 프로젝트 라이프사이클 전반에 걸쳐 사용자의 구독 생태계에 대한 의존도가 높아지고 있습니다.

세계 BIM 시장 동향과 인사이트

전자화 의무화 및 ISO 19650 준수, 전 세계 BIM 도입 가속화

공공 프로젝트에서 BIM 사용 의무화는 성숙한 건설 경제권 전체에서 디지털 전달 워크플로우의 표준화를 촉진하고 있습니다. 영국은 2025년까지 500만 파운드 이상의 공공 프로젝트에 레벨 3 BIM을 요구하고 있으며, 구조화된 데이터 교환을 촉진하여 조달 리스크를 줄이고 있습니다. 유럽 공공기관의 60% 이상이 공식적인 BIM 전략을 공개하고 있으며, 민간 개발업체에도 유사한 기준 준수를 촉구하고 있습니다. 미국 여러 주와 캐나다의 유사한 정책도 비슷한 파급효과를 가져오고 있습니다. ISO 19650에 기반한 표준화는 국경을 초월한 협업 간소화, 계약상의 모호성 해소, 신규 이해관계자의 온보딩 기간 단축을 실현하여 건축 정보 모델링 시장의 채택률을 직접적으로 높이고 있습니다.

디지털 트윈을 활용한 자산 라이프사이클 관리의 부상

소유주들은 BIM 모델과 IoT 센서를 연동하여 유지보수 최적화 및 다운타임 감소를 위한 라이브 디지털 트윈을 생성하는 사례가 증가하고 있습니다. 센서 연동형 트윈을 도입한 건물에서는 연간 운영비용이 5% 절감되고, 유지보수 대응 시간이 35% 단축된 것으로 보고되고 있습니다. 소유 비용의 80%를 차지하는 운영 단계에서 정량화된 절감 효과를 기대할 수 있기 때문에 시설 운영자들은 기존 모델을 데이터가 풍부한 트윈으로 업그레이드하는 움직임이 가속화되고 있습니다. 이를 통해 BIM 시장 도입의 운영 단계 전반에 걸쳐 소프트웨어 및 서비스 수익을 향상시킬 수 있습니다.

중소기업 계약업체에 대한 높은 라이선스 및 교육 비용

초기 라이선스 비용이 1만 달러가 넘을 수 있고, 연간 갱신료와 하드웨어 업그레이드로 인해 총소유비용이 증가하기 때문에 많은 중소기업들이 도입을 미루고 있습니다. 싱가포르의 생산성 솔루션 보조금 등 소프트웨어 비용의 최대 50%를 보조하는 자금 지원 프로그램이 부담을 일부 덜어주고 있지만, 비용 민감도는 당분간 BIM 시장의 발목을 잡을 것으로 보입니다.

부문 분석

소프트웨어는 67.30%의 매출 점유율(66억 8,000만 달러 상당)을 차지합니다. Revit, Archicad와 같은 설계 제품군은 모델 제작의 시작점이며, 통합된 4D/5D 기능은 이제 기본 장비로 인식되어 프리미엄 추가 기능으로 간주되지 않습니다. AI 기반 간섭 감지 기능을 포함한 지속적인 업데이트를 통해 고객 이탈률을 낮게 유지하며 BIM 시장을 지원하고 있습니다.

서비스 매출은 15.6%의 CAGR로 증가하고 있는데, 이는 발주자 및 계약자가 모델 개발, 조정 및 분석을 외부에 위탁하고 있기 때문입니다. 아웃소싱을 통해 기업은 고정적인 급여 부담 없이 부족한 인력을 활용할 수 있습니다. 유럽과 아시아의 복잡한 대중교통 계획에는 전문 BIM 컨설팅 회사가 많이 채택되어 서비스용 BIM 시장의 잠재적 규모를 확대하고 있습니다.

온프레미스 도입은 2025년 매출의 71.10%인 70억 6,000만 달러를 차지할 것으로 예상됩니다. 대규모 설계 사무소는 엄격한 데이터 주권 규정을 준수하는 로컬 서버를 선호합니다. FedRAMP, ISO 27001 등 보안 인증이 점차 우려를 완화하고 있지만, 정착된 워크플로우가 전환을 지연시키고 있습니다.

클라우드 도입은 CAGR 18.1%로 확대되고 있습니다. 구독형 라이선싱은 자본 지출을 줄이고 즉각적인 확장성을 실현하며, 분산된 프로젝트 팀이 실시간으로 모델을 공동 편집할 수 있도록 지원합니다. COVID-19 사태로 원격근무의 실용성이 입증된 후, 많은 기업들이 SaaS를 미래지향적인 업무 체계로 채택하고 있으며, BIM 시장의 무게 중심은 꾸준히 호스트형 솔루션으로 이동하고 있습니다.

지역별 분석

북미는 2025년 37억 1,000만 달러, 전 세계 매출의 37.40%를 창출할 것으로 예상됩니다. 연방 정부의 인프라 지출은 교통 및 공공 서비스 분야에서 디지털 전달 요구사항과 연계되어 광범위한 도입을 촉진하고 있습니다. 미국의 BIM 시장 규모는 조달 및 라이프사이클 관리를 간소화하는 표준화된 객체 라이브러리의 영향을 받고 있습니다.

유럽은 영국과 독일의 의무화 정책을 바탕으로 2위를 차지하고 있습니다. 2025년 지역 매출은 31억 2,000만 달러에 달할 것으로 예상되며, 2033년까지 두 배로 증가할 것으로 예상됩니다. 네메텍과 같은 지역 소프트웨어 대기업은 학술 연구와의 긴밀한 협력을 통해 탄탄한 기술 공급을 유지하면서 BIM 시장의 경쟁력을 높이고 있습니다.

아시아태평양은 14.6%의 CAGR로 가장 빠르게 성장하고 있습니다. 중국의 스마트 시티 구상, 일본의 노동력 부족 대책으로서의 자동화 추진, 인도의 확장하는 교통 회랑이 큰 수요를 창출하고 있습니다. 싱가포르에서는 정부가 소프트웨어 지출의 일부를 보조하는 정책을 시행하고 있으며, 정책 주도의 발전에서 지역 벤치마킹을 통해 BIM 시장의 추가 확대를 촉진하고 있습니다.

중동 및 아프리카는 규모는 작지만, 걸프 지역 국가들은 강한 성장세를 보이고 있습니다. 사우디의 NEOM과 같은 메가 프로젝트는 완전한 디지털 트윈 전략을 채택하여 새로운 지역 표준을 수립하고 있습니다. 현지 인력의 기술력 향상을 위한 역량 개발 프로그램이 진행 중이며, 수입 전문 지식에 대한 의존도를 점차 줄여나가고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The building information modeling market is expected to grow from USD 9.93 billion in 2025 to USD 11.29 billion in 2026 and is forecast to reach USD 21.42 billion by 2031 at 13.7% CAGR over 2026-2031.

Rapid digital transformation across architecture, engineering, construction and operations is expanding BIM from a visualization tool into a cloud-enabled collaboration platform. Growth is reinforced by tighter government mandates, integration with artificial intelligence and digital twins, and wider SaaS availability that lowers up-front costs for smaller firms. Vendors are also embedding 4D scheduling, 5D cost estimation and sustainability analytics as default capabilities, which keeps switching barriers high. Intense competition is prompting continuous upgrades that improve interoperability and workflow automation, deepening user reliance on subscription ecosystems throughout the project lifecycle.

Global Building Information Modeling Market Trends and Insights

E-mandates and ISO 19650 alignment accelerating global BIM uptake

Mandated BIM use on public projects is normalizing digital delivery workflows across mature construction economies. The United Kingdom's requirement for Level 3 BIM on public projects above GBP 5 million by 2025 encourages structured data exchanges that lower procurement risk. More than 60% of European public agencies now publish formal BIM strategies, which pushes private developers to follow the same standards. Comparable policies in several US states and provinces in Canada have the same cascading effect. Standardization around ISO 19650 simplifies cross-border collaboration, reduces contractual ambiguity and shortens onboarding time for new stakeholders, directly lifting adoption rates for the building information modeling market.

Rise of digital-twin-enabled asset lifecycle management

Owners increasingly connect BIM models with IoT sensors to generate live digital twins that optimize maintenance and reduce downtime. Buildings equipped with sensor-linked twins have reported 5% annual operating cost cuts and 35% faster maintenance response times. The promise of quantified savings during the 80% cost-of-ownership phase is compelling facility operators to upgrade legacy models into data-rich twins, which lifts software and service revenues throughout the operational stage of building information modeling market adoption.

High Licensing & Training Costs for SME Contractors

Initial seat licenses can exceed USD 10,000 while annual renewals and hardware upgrades increase total cost of ownership, causing many small firms to defer adoption. Funding programs such as Singapore's Productivity Solutions Grant that reimburses up to 50% of software expenses partially mitigate the burden, yet cost sensitivity remains a near-term drag on the building information modeling market.

Other drivers and restraints analyzed in the detailed report include:

- Green-building and net-zero compliance pressures

- Modular or off-site construction demanding seamless prefab coordination

- Interoperability & open-standards gaps across authoring tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software holds a 67.30% revenue share worth USD 6.68 billion. Authoring suites such as Revit and Archicad remain the entry point for model creation, with integrated 4D and 5D functions now interpreted as table stakes rather than premium add-ons. Continuous updates that incorporate AI-driven clash detection keep customer churn low, anchoring the building information modeling market.

Service revenue is rising at a 15.6% CAGR as owners and contractors outsource model development, coordination and analytics. Outsourcing gives firms access to scarce talent without fixed payroll commitments. Complex public-transportation schemes in Europe and Asia commonly appoint specialist BIM consultancies, expanding the addressable building information modeling market size for services.

On-premises installations represent USD 7.06 billion and 71.10% of 2025 revenue. Large design houses favor local servers that align with strict data-sovereignty rules. Security certifications such as FedRAMP and ISO 27001 are gradually easing those concerns, yet entrenched workflows slow migration.

Cloud deployments are growing at 18.1% CAGR. Subscription licensing lowers capital expenditure and delivers instant scalability, letting dispersed project teams co-author models in real time. After pandemic-driven remote work proved viable, many firms adopted SaaS to future-proof operations, steadily shifting the center of gravity of the building information modeling market toward hosted solutions.

The Building Information Modeling Market Report is Segmented by Solution (Software, Services), Deployment Mode (On-Premises, Cloud), Project Lifecycle Stage (Pre-Construction, Construction, Post-Construction), Application (Commercial Buildings, Residential Buildings, and More), End User (Architects and Designers, Engineers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated USD 3.71 billion and 37.40% of global revenue in 2025. Federal infrastructure spending tied to digital-delivery requirements fuels broad adoption across transportation and utilities. The building information modeling market size in the United States benefits from standardized object libraries that simplify procurement and lifecycle management.

Europe ranks second, anchored by mandates in the United Kingdom and Germany. The continent's 2025 revenue reached USD 3.12 billion and is on course to double by 2033. Regional software champions such as Nemetschek leverage close ties to academic research, which sustains a robust skills pipeline and keeps the building information modeling market competitive.

Asia-Pacific is the fastest-growing region at 14.6% CAGR. China's smart-city initiatives, Japan's automation push to counter labor shortages, and India's expanding transport corridors create substantial volume. Government incentives in Singapore that cover a portion of software expenditure make it the region's benchmark for policy-led progress, further enlarging the building information modeling market.

The Middle East and Africa remain smaller but exhibit strong momentum in Gulf states. Mega-projects like NEOM in Saudi Arabia adopt full digital-twin strategies, setting new regional standards. Capacity-building programs are underway to upskill local talent, gradually reducing reliance on imported expertise.

- Autodesk Inc.

- Nemetschek SE

- Bentley Systems Inc.

- Trimble Inc.

- Dassault Systemes SE

- Hexagon AB

- AVEVA Group PLC

- Asite Solutions Ltd

- RIB Software GmbH

- Graphisoft SE

- Allplan GmbH

- Topcon Positioning Systems Inc.

- Procore Technologies Inc.

- ACCA Software SPA

- Revizto SA

- CMiC Inc.

- Beck Technology Ltd

- Vectorworks Inc.

- Tekla Corporation (Trimble)

- Bimeye Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-mandates and ISO 19650 Alignment Accelerating Global BIM Uptake

- 4.2.2 Rise of Digital-Twin-enabled Asset Lifecycle Management

- 4.2.3 Green-Building and Net-Zero Compliance Pressures

- 4.2.4 Modular / Off-site Construction Demanding Seamless Prefab Coordination

- 4.2.5 Cloud adoption and SaaS pricing lowering entry barriers

- 4.2.6 AI-driven generative design and predictive analytics boosting productivity

- 4.3 Market Restraints

- 4.3.1 High Licensing and Training Costs for SME Contractors

- 4.3.2 Interoperability and Open-Standards Gaps Across Authoring Tools

- 4.3.3 Cyber-security and IP Protection Concerns in Cloud Workflows

- 4.3.4 Cultural Resistance to Process Re-engineering in Legacy Firms

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Software

- 5.1.1.1 Dimension

- 5.1.1.1.1 3D

- 5.1.1.1.2 4D

- 5.1.1.1.3 5D

- 5.1.1.1.4 6D

- 5.1.1.1.5 7D and Beyond

- 5.1.1.1 Dimension

- 5.1.2 Services

- 5.1.2.1 Consulting and Advisory

- 5.1.2.2 Implementation and Integration

- 5.1.2.3 Training and Support

- 5.1.2.4 Managed Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.3 By Project Lifecycle Stage

- 5.3.1 Pre-construction (Planning and Design)

- 5.3.2 Construction (Site Execution)

- 5.3.3 Post-construction (Operations and Maintenance)

- 5.4 By Application

- 5.4.1 Commercial Buildings

- 5.4.2 Residential Buildings

- 5.4.3 Industrial and Manufacturing Facilities

- 5.4.4 Infrastructure (Roads, Rail, Airports, Ports, Bridges)

- 5.4.5 Institutional (Healthcare, Education, Government)

- 5.4.6 Other Applications

- 5.5 By End User

- 5.5.1 Architects and Designers

- 5.5.2 Engineers (Structural, MEP)

- 5.5.3 Contractors and Builders

- 5.5.4 Owners and Developers

- 5.5.5 Facilities and Asset Managers

- 5.5.6 Consultants and Project Managers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Nordics

- 5.6.3.6 Rest of Europe

- 5.6.4 Middle East

- 5.6.4.1 United Arab Emirates

- 5.6.4.2 Saudi Arabia

- 5.6.4.3 Turkey

- 5.6.4.4 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Rest of Africa

- 5.6.6 Asia-Pacific

- 5.6.6.1 China

- 5.6.6.2 Japan

- 5.6.6.3 India

- 5.6.6.4 South Korea

- 5.6.6.5 Southeast Asia

- 5.6.6.6 Rest of Asia-Pacific

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Autodesk Inc.

- 6.4.2 Nemetschek SE

- 6.4.3 Bentley Systems Inc.

- 6.4.4 Trimble Inc.

- 6.4.5 Dassault Systemes SE

- 6.4.6 Hexagon AB

- 6.4.7 AVEVA Group PLC

- 6.4.8 Asite Solutions Ltd

- 6.4.9 RIB Software GmbH

- 6.4.10 Graphisoft SE

- 6.4.11 Allplan GmbH

- 6.4.12 Topcon Positioning Systems Inc.

- 6.4.13 Procore Technologies Inc.

- 6.4.14 ACCA Software SPA

- 6.4.15 Revizto SA

- 6.4.16 CMiC Inc.

- 6.4.17 Beck Technology Ltd

- 6.4.18 Vectorworks Inc.

- 6.4.19 Tekla Corporation (Trimble)

- 6.4.20 Bimeye Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment