|

시장보고서

상품코드

1939045

바이오연료 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Biofuels - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

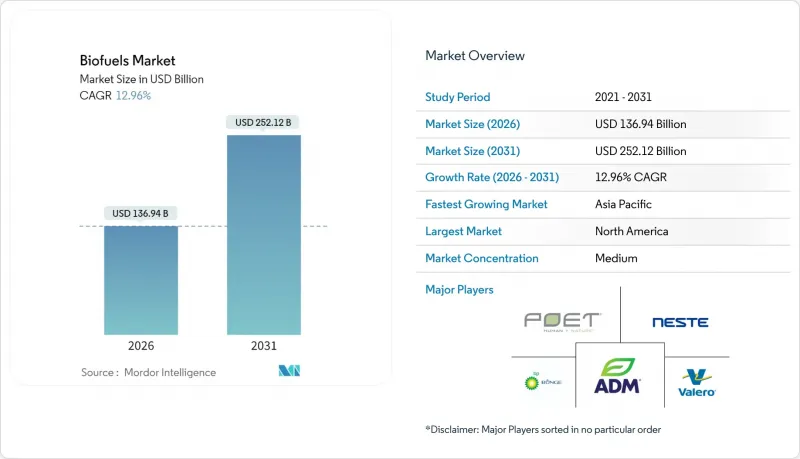

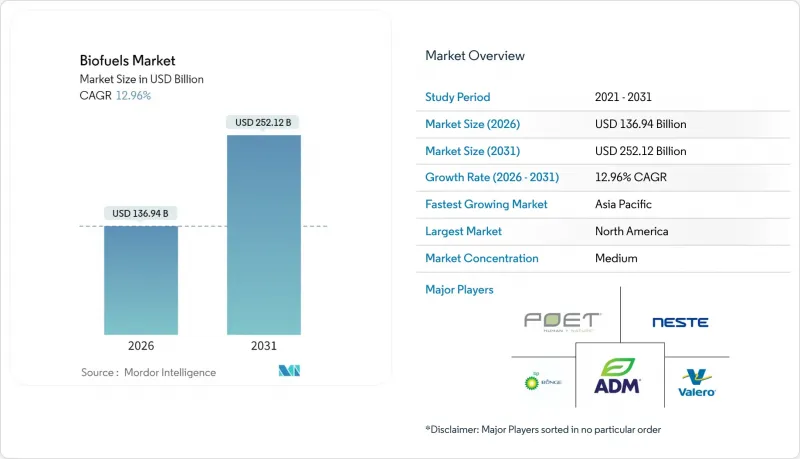

바이오연료 시장은 2025년 1,212억 3,000만 달러에서 2026년에는 1,369억 4,000만 달러로 성장하여 2026년부터 2031년까지 CAGR 12.96%를 기록하며 2031년까지 2,521억 2,000만 달러에 달할 것으로 예측됩니다.

운송 분야, 특히 항공 분야의 탈탄소화 요구가 높아지고 석유 메이저들의 대규모 투자가 도입 장벽을 완화하는 생산능력 증설을 추진하고 있습니다. 1세대 작물 유래 연료에서 폐기물 유래 및 합성생물학 솔루션으로의 빠른 기술 전환으로 수명주기 배출량이 개선되고 원료 리스크가 감소하고 있습니다. 동시에 북미의 세제 혜택과 아시아의 혼합 의무화로 인해 생산자들에게 가격 안정성을 보장하는 장기 오프 테이크 계약이 촉진되고 있습니다. 주요 기업들이 발표한 43개의 정유소 전환 및 신규 건설 프로젝트를 통해 2030년까지 수백만 톤의 생산능력이 추가될 것으로 예상됩니다. 이로 인해 경쟁이 심화되고, 공급망 재구축과 재생 연료와 화석연료의 비용차이가 줄어들고 있습니다.

세계 바이오연료 시장 동향과 전망

아시아 및 남미 지역의 운송 부문 혼합 의무 강화

아시아 및 남미 국가에서는 정부의 혼합비율 상향 조정으로 원료 배분 및 생산기지 배치에 변화가 일어나고 있습니다. 인도네시아의 B40 프로그램만으로도 바이오디젤 소비량은 연간 1,315만 킬로리터로 증가하여 디젤 수입을 줄이고 90억 달러의 외환 지출을 절감할 수 있을 것으로 예상됩니다. 인도는 2025년까지 에탄올 20% 혼합을 빠르게 추진하고 있으며, 증류 설비와 물류 자산에 대한 투자를 동시에 추진하고 있습니다. 필리핀과 태국에서도 유사한 정책이 지역적으로 추진력을 얻고 있으며, 브라질은 전통적인 에탄올 기반을 유지하고 있습니다. 이러한 의무화는 농촌지역 소득 향상, 원유 수입비용 억제, 예측 가능한 수요 확보를 통해 플랜트 증설의 리스크 감소에 기여하고 있습니다. 이 모든 것이 결합되어 세계 바이오연료 시장의 급격한 성장 전망을 뒷받침하고 있습니다.

북미에서 재생 디젤 수요를 주도하는 넷제로 기업 간 전력 구매 계약 체결

주요 물류 및 소매 브랜드는 현재 규정된 최소 기준을 초과하는 저탄소 연료 공급을 보장하는 다년간의 구매 계약을 체결하고 있습니다. DHL 그룹은 네스테와의 제휴를 통해 2030년까지 연간 30만 톤의 지속가능한 항공 연료(SAF) 조달을 목표로 하고 있습니다. 캘리포니아주 저탄소 연료 기준(LCFS)은 참여 기업이 온실가스 크레딧을 현금화할 수 있으며, 그 가치는 실제 연료 가격을 초과하는 경우가 많아 장기적인 경제성을 더욱 향상시키고 있습니다. 이러한 기업의 노력으로 생산자들은 수익 전망을 명확히 할 수 있으며, 미국과 캐나다 전역에 새로운 수소화 처리 시설 건설을 위한 부채 대출을 확보할 수 있게 됩니다.

원자재 가격 변동(대두, 유채, 식용유)으로 인한 생산자 수익률 압박

대두유, 식용유, 수지의 가격은 2024년 40-60% 변동하여 정제업체들의 수익률을 압박하고 헤지 전략을 복잡하게 만들었습니다. 유럽에서 폐유 수입 부정과 관련된 혼란은 가격 상승과 동시에 추적성 문제를 야기했습니다. 생산자들은 임업 폐기물이나 도시 슬러지 등의 잔재물로 다각화하여 변동성에 대응하고 있지만, 전처리 공정은 자본 비용과 복잡성을 수반합니다. 따라서 단기 수익성은 원자재 조달 포트폴리오의 유연성과 원자재 가격 변동을 상쇄할 수 있는 견고한 신용시장에 의존하고 있습니다.

부문 분석

지속가능한 항공 연료(SAF)의 공급량은 작지만 CAGR 34.98%로 확대되고 있으며, 항공사의 즉각적인 배출 감소 요구와 지원 정책을 반영하고 있습니다. 바이오에탄올은 미국 E10과 브라질 E27 혼합연료에 정착되어 있어 여전히 가장 큰 점유율을 차지하고 있습니다. 그러나 수소화 처리 기술이 SAF, 재생 디젤, 바이오나프타를 동시에 생산할 수 있는 특성으로 인해 기존 파이프라인에 적합한 드롭인 분자로의 자본 이동이 진행되고 있습니다.

2세대 바이오디젤은 추운 지역에서의 신형 엔진 시스템과의 호환성 문제로 인해 성장이 둔화되고 있습니다. 한편, 재생 디젤은 우수한 세탄가와 화석 디젤과 동등한 수준의 인프라 구축으로 시장 점유율을 확대. 바이오 프로판과 같은 고부가가치 제품별로는 프로젝트 경제성을 더욱 향상시키고 있습니다. 이에 따라 세계 바이오연료 시장은 다른 분야에서의 수요가 예상되며, 탄소배출권 평가액이 높은 연료로 전환되고 있습니다.

1세대 연료는 여전히 매출의 67.62%를 차지하고 있으며, 주로 브라질의 사탕수수 에탄올과 미국의 옥수수 에탄올이 주도하고 있습니다. 1세대 경로의 세계 바이오연료 시장 규모는 완만하게 증가할 것으로 예상되나, 선진적인 대안이 확대됨에 따라 상대적인 점유율은 감소할 것으로 보입니다. 3세대 조류 프로젝트는 유전공학과 광생물반응기의 발전으로 생산비용이 두 자릿수 감소하면서 현재 15.92%의 CAGR을 보이고 있습니다.

최근 대학 연구에 따르면, 유전자 변형 미세조류는 폐유의 85%를 수소화 처리에 적합한 지질로 전환할 수 있으며, 이를 통해 토지 이용 문제를 완화할 수 있을 것으로 기대됩니다. 란자젯의 에탄올에서 SAF(지속가능한 항공 연료)를 생산하는 플랜트 등 2세대 셀룰로오스 기반 시설은 마침내 상업적 규모의 처리 능력을 달성하고 효소 효율의 향상을 입증하고 있습니다. 4세대 합성생물학은 아직 상용화 전 단계이지만, 회수한 CO2로부터 직접 연료 합성을 가능하게 하기 위해 벤처 자금을 모으고 있습니다.

바이오연료 시장 보고서는 연료 유형(바이오에탄올, 바이오디젤, 바이오디젤, 재생 디젤 등), 세대(1세대, 3세대 등), 원료(당작물, 전분작물, 조류 등), 기술(발효, 에스테르교환, 수소화처리 등), 용도(도로교통, 항공, 선박, 발전 및 난방), 지역(북미, 유럽, 아시아태평양 등)(북미, 유럽, 아시아태평양 등)으로 분류되어 있습니다.

지역별 분석

북미는 성숙한 옥수수 에탄올 플랜트, 대두유 기반 재생 디젤의 성장, 그리고 관대한 세제 혜택에 힘입어 2025년 전 세계 바이오연료 시장의 42.56%를 차지할 것으로 예상됩니다. 재생 디젤의 설비 용량은 2025년까지 52억 갤런으로 두 배로 증가하고, 캘리포니아주의 저탄소 연료 기준(LCFS)이 국내 공급량의 거의 전량을 소비하기 때문에 안정적인 가격 하한선이 형성될 것입니다. 이 지역의 명확한 정책은 생산자들이 신속하게 자금을 조달할 수 있게 해주며, 견고한 곡물 가공 인프라는 안정적인 원료 공급을 보장합니다. 최근 멕시코의 의무화 연장과 캐나다의 청정연료 규제는 지역 수요를 더욱 확대할 것입니다.

유럽에서는 재생에너지 지침 III에 따라 2030년까지 재생에너지 비율 42.5%를 목표로 설정하고 팜유 원료 사용을 단계적으로 폐지하는 등 변화가 진행되고 있습니다. 독일은 2025년부터 전년도 온실가스 배출권 이월을 금지하고, 의무이행 주체가 즉시 첨단 바이오연료를 구매하도록 하고 있습니다. 중국산 바이오디젤에 대한 반덤핑 관세는 무역 경로를 전환하고, 국내 HVO의 프리미엄 가격을 상승시켜 현지 생산능력의 증대를 촉진하고 있습니다. 복잡한 정책 믹스는 기술 혁신을 촉진하는 반면, 원자재 제약으로 인해 물량 성장은 완만한 속도에 머물러 있습니다.

아시아태평양이 16.78%로 가장 높은 CAGR을 기록했습니다. 인도네시아의 B40 의무화 정책은 연간 1,315만 킬로리터의 바이오디젤을 흡수하여 150억 달러의 외환 지출을 줄이는 동시에 소규모 팜유 농가의 소득을 지원하고 있습니다. 인도가 2025년까지 에탄올 20% 혼합을 목표로 하는 움직임은 곡물-당밀 에탄올 수요를 증가시켜 1,000기의 압축 바이오가스 플랜트 시장을 창출할 것입니다. 중국의 합작 사업, 예를 들어 BP가 자오(Jiaao)의 건설 예정 SAF 라인에 출자하고 있는 사례는 항공 분야의 탈탄소화에 대한 의지를 보여주고 있습니다. 풍부한 농업 잔류물, 원유 가격 상승 위험 증가, 재정적 인센티브가 결합되어 아시아는 세계 바이오연료 시장에서 독보적인 성장 동력이 되고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 애널리스트의 3개월간 지원

자주 묻는 질문

목차

제1장 소개

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측(금액·수량)

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KSM 26.03.09The Biofuels market is expected to grow from USD 121.23 billion in 2025 to USD 136.94 billion in 2026 and is forecast to reach USD 252.12 billion by 2031 at 12.96% CAGR over 2026-2031.

Growing decarbonization mandates in transportation, especially aviation, and scaled investments from oil majors are driving capacity additions that ease adoption barriers. Rapid shifts in technology from first-generation crop-based fuels toward waste-derived and synthetic biology solutions are improving life-cycle emissions and reducing feedstock risk. At the same time, government tax credits in North America and blending mandates in Asia are prompting long-term offtake contracts that stabilize prices for producers. Competitive intensity is rising because 43 refinery conversion and greenfield projects announced by leading petroleum companies will add multimillion-ton capacity before 2030, reshaping supply chains and narrowing cost gaps between renewable and fossil fuels.

Global Biofuels Market Trends and Insights

Transport-sector blend mandates intensifying in Asia & South America

Asian and South American governments are implementing higher blending requirements, which are reshaping feedstock allocation and production footprints. Indonesia's B40 program alone lifts biodiesel consumption to 13.15 million kiloliters annually, cutting diesel imports and saving USD 9 billion in foreign exchange. India is fast-tracking its move to 20% ethanol blending by 2025, which drives parallel investment in distillation and logistics assets. Similar policies in the Philippines and Thailand add regional momentum, while Brazil keeps its long-standing ethanol platform. These mandates support rural incomes, curb crude import bills, and establish predictable demand that de-risks plant expansions. Together, they underpin the steep growth outlook for the global biofuels market.

Net-zero-aligned corporate PPAs driving renewable diesel demand in North America

Major logistics and retail brands now sign multiyear purchase agreements that guarantee low-carbon fuel supply beyond regulatory minimums. DHL Group intends to source 300,000 tons of SAF annually by 2030 under a partnership with Neste . California's Low Carbon Fuel Standard enables participating firms to monetize greenhouse-gas credits, which are often valued above the physical fuel price, thereby further sweetening long-term economics. These corporate commitments provide producers with clearer revenue visibility, enabling them to secure debt financing for new hydrotreatment units across the United States and Canada.

Volatile Feedstock Prices (Soy, Rapeseed, UCO) Squeezing Producer Margins

Soybean oil, used cooking oil, and tallow prices swung 40-60% during 2024, eroding margins and complicating hedge strategies for refiners. Fraud-related disruptions in European waste-oil imports inflated prices while creating challenges to traceability. Producers are countering volatility by diversifying into residues such as forestry waste and municipal sludges, although preprocessing adds capital cost and complexity. Near-term profitability, therefore, depends on agile feedstock portfolios and robust credit markets that offset commodity swings.

Other drivers and restraints analyzed in the detailed report include:

- SAF tax incentives in the EU & U.S. Inflation Reduction Act

- Palm feedstock phase-out prompting algae & waste-oil investment in Europe

- Infrastructure bottlenecks in collecting agri-residues in India & Indonesia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sustainable aviation fuel volumes scale from a small base at a 34.98% CAGR, reflecting airlines' need for immediate emissions cuts and supportive mandates. Bioethanol retains the lion's share because it is entrenched in U.S. E10 and Brazilian E27 blends. Yet hydrotreatment's ability to co-produce SAF, renewable diesel, and bio-naphtha is shifting capital toward drop-in molecules that fit existing pipelines.

Second-generation biodiesel is plateauing because of compatibility issues with newer engine systems in cold climates. In contrast, renewable diesel gains market share thanks to its superior cetane numbers and parity with fossil diesel in terms of infrastructure. High-value co-products such as bio-propane further enhance project economics. The global biofuels market is therefore shifting toward fuels with cross-sector appeal and higher carbon credit valuation.

First-generation fuels still account for 67.62% of sales, driven primarily by sugarcane ethanol in Brazil and corn ethanol in the United States. The global biofuels market size for first-generation pathways is expected to rise modestly; however, the relative share will decline as advanced options scale. Third-generation algae projects now demonstrate 15.92% CAGR after genetics and photobioreactor advances cut production costs by double digits.

Recent university studies show that engineered microalgae can convert 85% of waste oil into lipids suitable for hydrotreatment, thereby reducing land-use concerns. Second-generation cellulosic facilities, such as LanzaJet's ethanol-to-SAF plant, are finally hitting commercial throughput and proving enzyme efficiency gains. Fourth-generation synthetic biology remains pre-commercial but attracts venture funding because it promises direct fuel synthesis from captured CO2.

The Biofuels Market Report is Segmented by Fuel Type (Bioethanol, Biodiesel, Renewable Diesel, and More), Generation (First-Generation, Third-Generation, and More), Feedstock (Sugar Crops, Starch Crops, Algae, and More), Technology (Fermentation, Trans-Esterification, Hydrotreatmen, and More), End-Use (Road Transport, Aviation, Marine, and Power Generation and Heating), and Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America is expected to control 42.56% of the global biofuels market in 2025, driven by mature corn ethanol plants, the growth of soybean oil-based renewable diesel, and generous tax credits. Installed renewable diesel capacity doubles to 5.2 billion gallons by 2025, and California's LCFS consumes nearly the entire domestic pool, creating a stable price floor. The region's policy clarity enables producers to secure financing quickly, while robust grain handling infrastructure ensures a stable feedstock flow. Mexico's recent mandate extensions and Canada's clean fuel regulations further enlarge regional demand.

Europe is transforming as the Renewable Energy Directive III sets a 42.5% renewable energy target by 2030 and phases out the use of palm oil feedstocks. Germany banned carry-over of prior-year greenhouse-gas certificates starting in 2025, forcing obligated parties to purchase more advanced biofuels immediately. Anti-dumping duties on Chinese biodiesel reroute trade and raise premiums for domestic HVO, encouraging local capacity additions. The complex policy mix fosters technological innovation while keeping volume growth moderate due to feedstock constraints.

Asia-Pacific posts the highest regional CAGR at 16.78%. Indonesia's B40 mandate absorbs 13.15 million kiloliters of biodiesel annually and saves USD 15 billion in foreign exchange, while supporting the incomes of smallholder palm farmers . India's march toward 20% ethanol by 2025 boosts demand for grain and molasses ethanol and seeds the market for 1,000 compressed-biogas plants. China's joint ventures, such as BP's stake in Jiaao's upcoming SAF line, signal intent to decarbonize aviation. Ample agricultural residues, rising oil-price exposure, and supportive fiscal incentives combine to make Asia an unrivaled growth engine for the global biofuels market.

- Abengoa Bioenergy SA

- Archer Daniels Midland Co.

- BP p.l.c.

- Cargill Inc.

- Chevron Renewable Energy Group Inc.

- Cosan S.A. / Raizen

- Eni S.p.A. (Eni Sustainable Mobility)

- Gevo Inc.

- Green Plains Inc.

- LanzaTech Global Inc.

- Neste Oyj

- POET LLC

- Petrobras

- Shell p.l.c.

- TotalEnergies SE

- Valero Energy Corp. (Diamond Green Diesel)

- Verbio Vereinigte BioEnergie AG

- Wilmar International Ltd.

- Aemetis Inc.

- Amyris Inc.

- Clariant AG

- Enerkem Inc.

- Pacific Ethanol (Alto Ingredients)

- Orsted A/S (Power-to-X Bio-methanol)

- Pacific Biodiesel Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Transport-sector Blend Mandates Intensifying in Asia & South America

- 4.2.2 Net-Zero-Aligned Corporate PPAs Driving Renewable Diesel Demand in North America

- 4.2.3 SAF (Sustainable Aviation Fuel) Tax Incentives in the EU & U.S. Inflation Reduction Act

- 4.2.4 Phasing-Out of Palm-based Feedstocks Prompting Algae & Waste-Oil Investments in EU

- 4.2.5 Emergence of Bio-naphtha for Petro-Chem Feedstock Decarbonisation

- 4.3 Market Restraints

- 4.3.1 Volatile Feedstock Prices (Soy, Rapeseed, UCO) Squeezing Producer Margins

- 4.3.2 Infrastructure Bottlenecks in Collecting Agri-Residues in India & Indonesia

- 4.3.3 Indirect Land-Use-Change (ILUC) Sustainability Caps in Europe

- 4.3.4 Competition from Drop-in e-Fuels in Long-haul Aviation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value & Volume)

- 5.1 By Fuel Type

- 5.1.1 Bioethanol

- 5.1.2 Biodiesel (FAME)

- 5.1.3 Renewable Diesel / HVO

- 5.1.4 Sustainable Aviation Fuel (SAF)

- 5.1.5 Bio-naphtha and Other Drop-in Biofuels

- 5.2 By Generation

- 5.2.1 First-Generation (Sugar & Starch)

- 5.2.2 Second-Generation (Cellulosic)

- 5.2.3 Third-Generation (Algae-based)

- 5.2.4 Fourth-Generation (Synthetic Biology/Photobiological)

- 5.3 By Feedstock

- 5.3.1 Sugar Crops (Sugarcane, Sugar Beet)

- 5.3.2 Starch Crops (Corn, Wheat, Cassava)

- 5.3.3 Oilseeds (Soy, Rapeseed, Palm)

- 5.3.4 Used Cooking Oil and Animal Fat

- 5.3.5 Lignocellulosic Agri-Residues

- 5.3.6 Algae

- 5.4 By Technology

- 5.4.1 Fermentation

- 5.4.2 Trans-esterification

- 5.4.3 Hydrotreatment (HVO/SAF)

- 5.4.4 Gasification and FT-Synthesis

- 5.4.5 Pyrolysis and Upgrading

- 5.5 By End-use Sector

- 5.5.1 Road Transport

- 5.5.2 Aviation

- 5.5.3 Marine

- 5.5.4 Power Generation and Heating

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 France

- 5.6.2.3 United Kingdom

- 5.6.2.4 Denmark

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Indonesia

- 5.6.3.4 Japan

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Abengoa Bioenergy SA

- 6.4.2 Archer Daniels Midland Co.

- 6.4.3 BP p.l.c.

- 6.4.4 Cargill Inc.

- 6.4.5 Chevron Renewable Energy Group Inc.

- 6.4.6 Cosan S.A. / Raizen

- 6.4.7 Eni S.p.A. (Eni Sustainable Mobility)

- 6.4.8 Gevo Inc.

- 6.4.9 Green Plains Inc.

- 6.4.10 LanzaTech Global Inc.

- 6.4.11 Neste Oyj

- 6.4.12 POET LLC

- 6.4.13 Petrobras

- 6.4.14 Shell p.l.c.

- 6.4.15 TotalEnergies SE

- 6.4.16 Valero Energy Corp. (Diamond Green Diesel)

- 6.4.17 Verbio Vereinigte BioEnergie AG

- 6.4.18 Wilmar International Ltd.

- 6.4.19 Aemetis Inc.

- 6.4.20 Amyris Inc.

- 6.4.21 Clariant AG

- 6.4.22 Enerkem Inc.

- 6.4.23 Pacific Ethanol (Alto Ingredients)

- 6.4.24 Orsted A/S (Power-to-X Bio-methanol)

- 6.4.25 Pacific Biodiesel Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

- 7.2 Next-Gen Electro-Bio-Refineries Integrating Green H2